|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 689-691-691 Week:

May 03 –May 23, 2021 Presentation:

May 28, 2021 Source:

http://www.asahi.com/ajw/articles/14346249 Japan’s

Population Of Children Under 15 Shrank By 190,000 From A Year Earlier 44

Percent Of Japanese People Are In Favor Of Revisions In Constitution Two

In Five (19%) Indians Have Shown Willingness To Buy Pre-Owned/Second-Hand

Cars New

Prime Minister Of South Korea Kim Bu-Gyeom "Conformity" 38% Vs

"Nonconformity" 26% Public

Verification Of Personnel Hearings, 'Morality' 76 Percent Vs 'Policy Ability

Only' 19 Percent 3

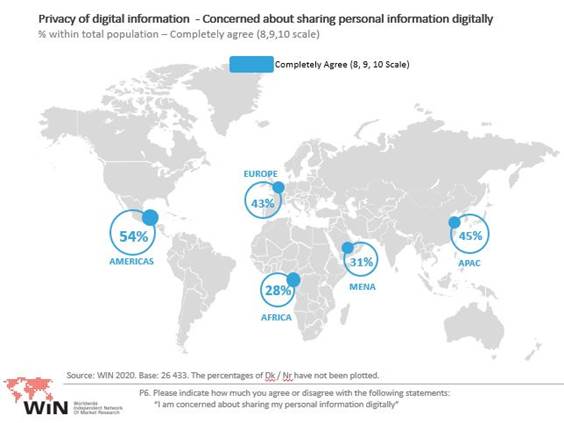

In 10 Pakistanis Concerned About Digitally Sharing Their Personal Information MENA

Advertiser Of The Month (April): Vimto 87

Percent Mauritians Think Social Media Makes People More Informed About

Current Affairs 63

Percent Gambians Get News From Television And 55 Percent Get From Social

Media Half

Of Tunisian Citizens 49 Percent Are In Favor Of Press Freedom Three

In Four (76%) Religious People Indicated A Likelihood To Donate To A

Charity One

In Eleven NHS Workers Plan To Leave Healthcare Sector After Pandemic 41%

Of 18-24 Year Olds Now Say Britain Should Have An Elected Head Of State Home

And EDC Are Real Estate Chains Get The Most Attention In Denmark Every

Third German Feels More Stressed In 2021 Than Before Corona, People With

Children Most Often Every

Second Cyclist Wears A Protective Helmet At Least Now And Then When Cycling 26

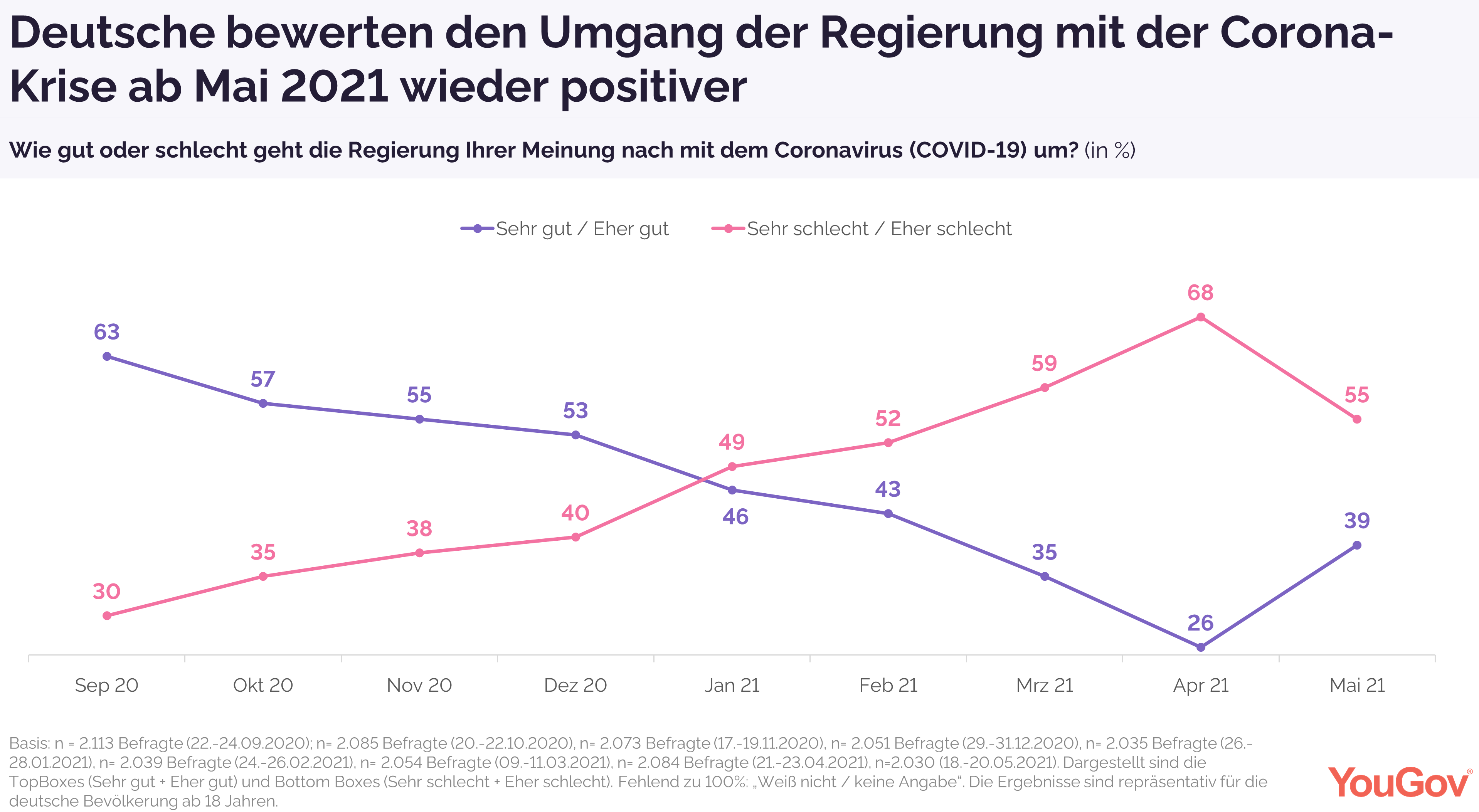

Percent Germans Praised The Government's Handling Of The Crisis In April 2021 A Quarter

Of 18-25 Years Old Say They Have Had Suicidal Thoughts Since The Start Of The

Crisis (27%) 9

May, Europe Day: The European Union In The Perception Of Italians 8

Out Of 10 Italians And Italians Agree: Excess Doses Of The Anti-Covid 19

Vaccine Must Be Shared Only

one in five Hungarians is vaccinated 70%

Of U.S. Social Media Users Never Or Rarely Post Or Share About Political,

Social Issues About

Six-In-Ten Americans Say Abortion Should Be Legal In All Or Most Cases Around

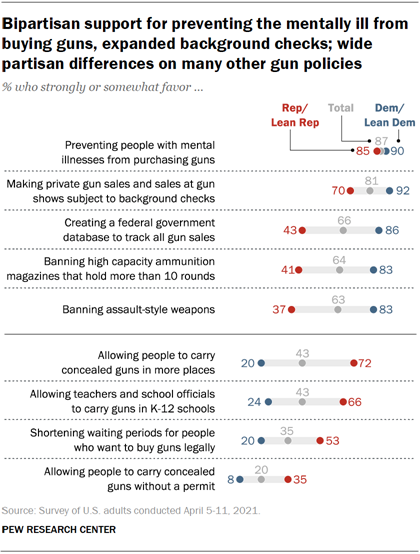

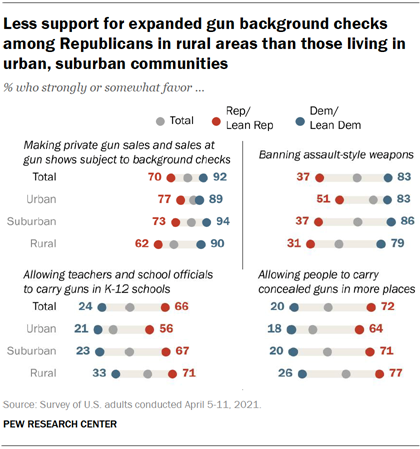

Half Of Americans (48%) See Gun Violence As A Very Big Problem In The Country

Today About

Four-In-Ten (41%) Americans Say News Organizations Are Growing In

Their Influence A

Third Of Large US Newspapers Experienced Layoffs In 2020, More Than In 2019 Liberals

(38%) in the Driver’s Seat over Conservatives (29%) as Vaccination Rollout

Hits its Stride New

Zealand Government Lead Over Opposition Down To 14% In April – Smallest Lead

Since January 2020 A

Huge Majority Of 93% Of Australians Said They Are More Likely To Buy Products

Made In Australia Nearly

Half (46%) Of Consumers In 17 Global Markets Use Zoom To Communicate

Regularly In

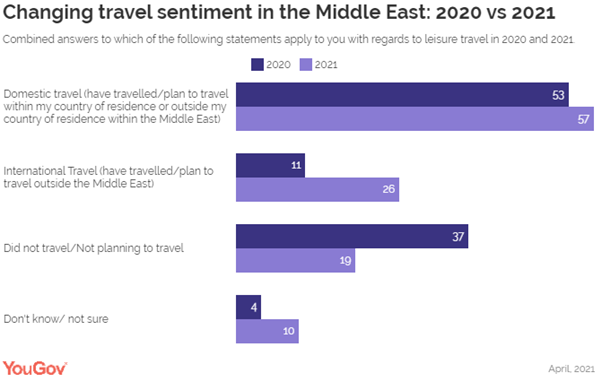

UAE And Saudi, The Intent To Travel Domestically Or Within The MENA Region

Increased Slightly 45%

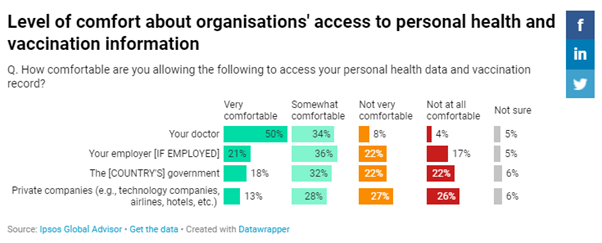

Of The Global Population Is Concerned About Sharing Their Personal

Information Digitally INTRODUCTORY NOTE

689-691-43-68/Commentary:

Japan’s

Population Of Children Under 15 Shrank By 190,000 From A Year Earlier

Japan’s

population of children under 15 shrank by 190,000 from a year earlier to an

estimated 14.93 million as of April 1, the 40th consecutive year of decline,

internal affairs ministry data showed. Children in

that age group account for 11.9 percent of the entire population, the lowest

level in the world, according to the ministry. The figure was 0.1 percentage

point down from the previous year. The

percentage has now dropped for 47 straight years. On the other

hand, people 65 or older account for 28.9 percent of the population, up 0.3

percentage point from the previous year. Although the

government has long vowed to battle the demographic change, the numbers show

that Japan’s declining birthrate and the graying of society have progressed

further. The ministry

released the numbers to mark Children’s Day, a national holiday, on May 5. Among those

under 15 years old, 7.65 million are boys and 7.28 million are girls. Japan has

3.24 million children between 12 and 14, and 2.65 million who are 2 years old

or younger, the data showed. The younger

the age, the smaller the ratio of the overall population. In 1950,

children under 15 accounted for 35.4 percent of the population because of the

first baby boom. But the

ratio started declining. In 1997,

people 65 or older made up 15.7 percent of the population, exceeding the 15.3

percent for those under 15. The ministry

compared Japan’s ratio of children with those in other countries with

populations of 40 million or more. Japan’s

percentage was the lowest, although the ministry said it was difficult to do

a strict comparison because the timing of the countries’ population surveys

was different. South

Korea’s ratio was the second lowest, at 12.2 percent as of July 1, 2020,

followed by Italy, at 13.3 percent as of July 1, 2018, and Germany, at 13.6 percent

as of Jan. 1, 2019. (Asahi

Shimbun) May 5, 2021 Source: http://www.asahi.com/ajw/articles/14342995 689-691-43-69/Country Profile

SUMMARY

OF POLLS

ASIA (China) The Population Of China Increased By 5.38 Percent To 1.41 Billion

In 2020 Census Compared With An Increase Of 5.84 Percent To 1.34 Billion In

The 2010 Census With growth having slowed ever since a

one-child policy was introduced in the late 1970s, the 2020 results of the

country’s once-a-decade census, published on Tuesday, showed the population

of mainland China increased 5.38 percent to 1.41 billion. That compared with

an increase of 5.84 percent to 1.34 billion in the 2010 census, and

double-digit percentage rises in all of China’s previous six official population

surveys dating back to 1953. (Asahi Shimbun) May 11, 2021 (Japan) Japan’s Population Of Children Under 15 Shrank By 190,000

From A Year Earlier Japan’s population of children under 15

shrank by 190,000 from a year earlier to an estimated 14.93 million as of

April 1, the 40th consecutive year of decline, internal affairs ministry data

showed.Children in that age group account for 11.9 percent of the entire

population, the lowest level in the world, according to the ministry. The

figure was 0.1 percentage point down from the previous year.The percentage

has now dropped for 47 straight years. (Asahi Shimbun) May 5, 2021 44 Percent Of Japanese People Are In Favor Of Revisions In

Constitution The Asahi Shimbun began the annual survey

on how the public views proposals for amending the Constitution, a key agenda

pushed by Shinzo Abe, who was prime minister from December 2012 to September

2020. The ruling Liberal Democratic Party, led by Prime Minister Yoshihide

Suga, is also seeking revisions. The Constitution, drafted during the

U.S.-led postwar occupation of Japan, has never been revised since it went

into force in 1947. (Asahi Shimbun) May 3, 2021 (India) Two In Five (19%) Indians Have Shown Willingness To Buy

Pre-Owned/Second-Hand Cars As the vaccination drive began in India and

Covid was believed to be under control early this year, three in ten (29%)

urban Indians said they were planning to buy a car, the data reveals.

However, the second wave of the pandemic has disrupted their planning and

only one in five (22%) out of them are likely to go ahead with their plan of

buying a car, while some (13%) have completely given up their plan or have

switched the category of the vehicle; to a two-wheeler now instead of a car

(10). (YouGov India) May 11, 2021 Nearly Two-Thirds Of Urban Indians (64%) Are Worried They

May Become Seriously Unwell Or Die Due To COVID YouGov’s Covid19 Public Monitor has been

tracking the public sentiment around the virus since last year when the

pandemic first broke out in the world. In May 2020, at the outset of

the pandemic, only 45% of urban Indians were worried about their personal

health getting affected due to covid. A year later as India faces a much

deadlier wave of the virus with limited healthcare facilities; this number

has gone up to 64%. (YouGov India) (Pakistan) 3 In 10 Pakistanis Concerned About Digitally Sharing Their

Personal Information According to a Gallup Pakistan Survey in

Pakistan (and similar surveys done by WIN International across the world),

30% Pakistanis agreed that they are concerned about sharing their personal

information. When asked about the necessity of sharing personal information,

24% Pakistanis think that sharing personal information is necessary nowadays.

43% Pakistanis (27% globally) are not fine with the privacy practices of most

data collectors asking for their personal information. As far as awareness

about digital rights and personal data privacy is concerned, 46% Pakistanis

are not aware of what happens with their personal information after they

share it with a data collector. (Gallup Pakistan) May 18, 2021 (South

Korea) New Prime Minister Of South

Korea Kim Bu-Gyeom "Conformity" 38% Vs "Nonconformity"

26% As a result of a survey of 1,000 adults on

the 11th to 13th days before the appointment of Prime Minister Kim, by Gallup

Korea (±3.1% points in the 95% confidence level of

the sample error), 38% of respondents said that Prime Minister Kim is

suitable for the post of Prime Minister. More than 26% of respondents said

they didn't. 36% declined to comment. The response that it was

appropriate both before and after the personnel hearing was more than the

response that it was inappropriate. In the April 20-22 survey

immediately after the Prime Minister's nomination, 34% of'conformity' and 18%

of'nonconformity'. In this survey, after the personnel hearing, opinion

reservations decreased, and both conformity and nonconformity consensus

increased. (Gallup Korea) 2021.05.14 Public Verification Of Personnel Hearings,

'Morality' 76 Percent Vs 'Policy Ability Only' 19 Percent Only 19% of respondents chose'private

verification for morality and public verification for policy capabilities'.5%

reserved their opinion. When asked whether morality and policy ability should

be prioritized when verifying candidates at the personnel hearing,'morality'

and'policy ability' were tied at 47% each. In particular, those in their 20s

and 30s who gave priority to'policy ability' were 65% and 62%, respectively,

higher than those of other age groups. (Gallup Korea) 2021-05-14 MENA (Kingdom

of Saudi Arabia) MENA Advertiser Of The Month (April): Vimto This Ramadan, Vimto came up with a campaign

that helped the brand win YouGov's Advertiser of the Month. Data from

YouGov BrandIndex shows the percentage of adults in KSA who saw

Vimto’s ad during the month of April shot up by 11 points from 19%

(April 1) to 30% (April 30). The campaign attracted participation

from across KSA which helped the Ad Awareness score of the

brand to shoot up from 19% on April 1 to 30% on

April 29. (YouGov MENA) (UAE) Global Village Has Emerged As The Top Mover This Year, With

A Change In Score Of +14.2 Compared To Ramadan 2020 In UAE YouGov BrandIndex data shows Global Village

has emerged as the top mover this year, with a change in score of +14.2

compared to Ramadan 2020. Despite ongoing Covid19 operating procedures in

place, Global Village decided to extend its open season into Ramadan this

year. This extension, coupled with it being the silver jubilee (25th year)

season, saw it promote its 25th world record-breaking event,

which clearly reached a wide audience in Ramadan. (YouGov MENA) AFRICA (Mauritius) 87 Percent Mauritians Think Social Media Makes People More

Informed About Current Affairs While a small share of citizens believe

that the use of social media such as Facebook, Twitter, and WhatsApp makes

people more susceptible to fake news and intolerance, a large majority say

social media informs them about current events and helps them have an impact

on political processes. The share of Mauritians who use social media every

day has more than doubled over the past six year, from 32% in 2014 to 69% in

2020. Overall, citizens believe the effect of social media on society is

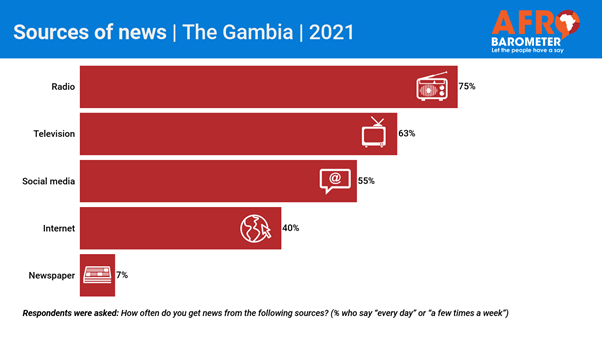

positive. (Afrobarometer) 5 May 2021 (Gambia) 63 Percent Gambians Get News From Television And 55 Percent

Get From Social Media An overwhelming majority of Gambians say

the media is in fact free to do its work without government interference. The

Gambia’s media environment has become somewhat less restrictive in recent

years, including a 2018 Supreme Court decision that the criminalization of

defamation is unconstitutional. The 2021 World Press Freedom Index ranked the

Gambia 85th out of 180 countries in media freedom, up two spots from the previous

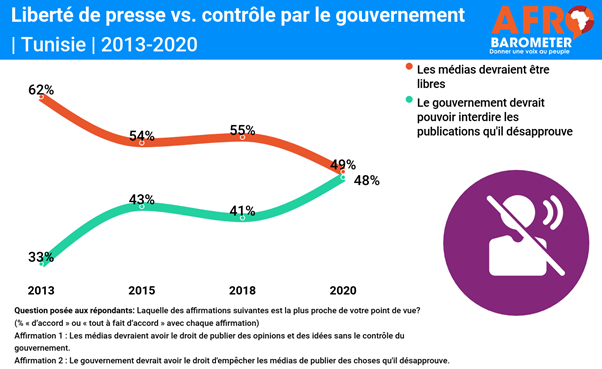

year. (Afrobarometer) 4 May 2021 (Tunisia) Half Of Tunisian Citizens 49 Percent Are In Favor Of Press

Freedom According to the survey, most citizens are

in favor of filtering press publications when they are false or hateful in

nature. The survey therefore revealed that most citizens believe that

the media and journalists“sometimes” or even

“often” disclose information which they know to be false. Yet half

of citizens believe that the government should be able to ban any publication

of content that it disapproves of, though a downward trend. (Afrobarometer) May 7, 2021 WEST

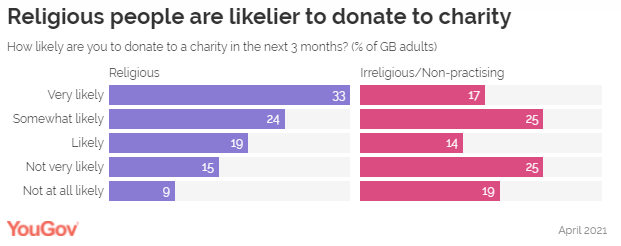

EUROPE (UK) Three In Four (76%) Religious People Indicated A Likelihood

To Donate To A Charity Asked about their likelihood to donate to a

charity in the next three months, three in four (76%) religious people

indicated a likelihood to do so, demonstrating a significantly higher

propensity than the irreligious and non-practising group (56%). The

difference may be at least partially explained by the fact that 17% of people

in the religious group cited their religious belief as a motivation towards

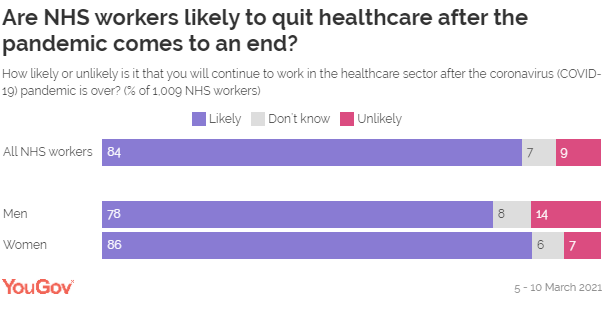

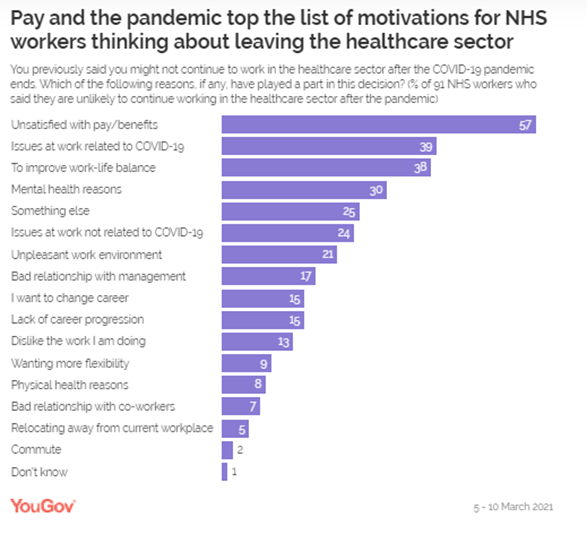

donating directly to a charity. (YouGov UK) May 05, 2021 One In Eleven NHS Workers Plan To Leave Healthcare Sector

After Pandemic YouGov’s research shows little difference

between roles within the NHS, with 9% of staff in patient-facing roles saying

it is unlikely for them to remain in the sector, as do 8% of those in

non-patient-facing positions. However, the figure is higher among male NHS

workers, one in seven of whom (14%) think it is unlikely they will work in

the healthcare sector when the pandemic ends, twice that of women (7%) who

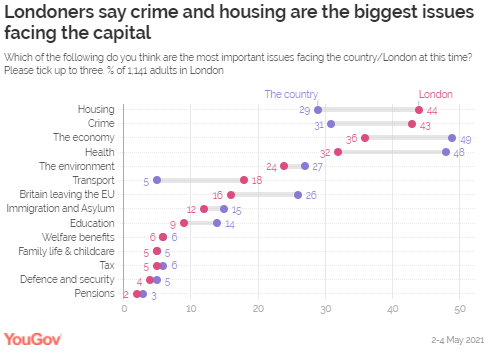

said the same. (YouGov UK) May 05, 2021 Two In Five People Point To Housing (44%) And Crime (43%)

As The Most Urgent Problems To Be Tackled By New Mayor Londoners are heading to the ballot boxes

today to elect or re-elect the next mayor. YouGov data shows that two in five

people point to housing (44%) and crime (43%) as the most urgent problems to

be tackled, while just over a third (36%) say it’s the economy. These issues

are followed by health (32%), the environment (24%) and transport (18%).

These issues largely match the main candidates’ pledges, with current mayor

Sadiq Khan promising to build more council homes, crack down on crime and

lower the cost of commuting. (YouGov UK) May 06, 2021 Four In Ten Britons Satisfied With Their Local Council, But

Most In The North Of England Feel They Get Less National Spending Than Other

Areas Britons are more likely to say they’re

satisfied than dissatisfied with the way their local council runs things,

according to a new Ipsos MORI poll. The poll was conducted with 8,352 people

aged 16+ across the United Kingdom. The survey reveals that two in five (40%)

say that they’re satisfied with the way their local council runs things while

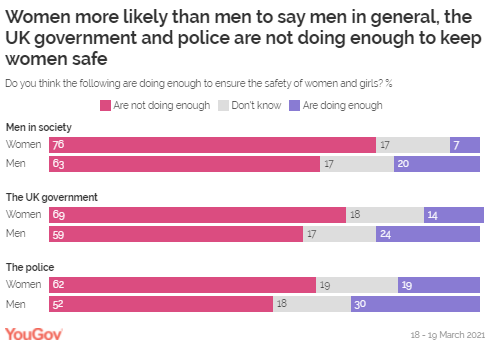

a quarter (25%) say they’re dissatisfied. (Ipsos MORI) 7 May 2021 Three Quarters Of British Women (76%) Say Men In Society

Don’t Pull Their Weight In Keeping Women And Girls Safe Three quarters of women (76%) say men in

society don’t pull their weight in keeping women and girls safe. Men tend to

agree (63%), although a fifth (20%) consider their gender overall to be doing

enough – almost three times the number of women who think so (7%). Seven in

ten women (69%) also say the government’s efforts are lacking, compared with

59% of men. A majority of women (62%) similarly feel the police aren’t doing

enough, while around half of men (52%) agree. (YouGov UK) May 10, 2021 Towards The End Of Last Year, Over Half Of The Public (53%)

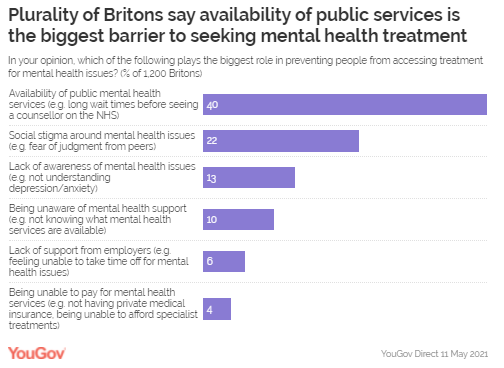

Said The Covid-19 Pandemic Had Negatively Affected Their Mental Wellbeing Data from YouGov Direct conducted during

Mental Health Awareness Week 2021 reveals that Britons are most likely to

believe that low availability of public services play the biggest role in

preventing people from accessing treatment. Two in five say capacity issues

such as long wait times (40%) are the largest barrier to seeking help, with

social stigma coming a distant second (22%). NHS England data from April

2021 revealed that the number of people on

waiting lists for all NHS treatment was at 4.7 million people – the highest number since records

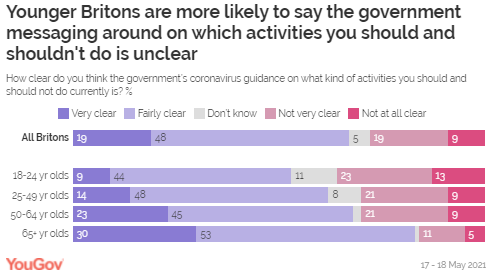

began in 2007. (YouGov UK) May 14, 2021 Three In Ten Britons Feel Less Certain

About Government’s Guidance For Which Activities You Should And Shouldn’t Do

And Say It’s Either Not Very (19%) Or Not At All Clear (9%) Critics are now attacking Boris Johnson for

a reopening approach marked by “confusion”, which includes allowing travel but

ministers saying you shouldn’t do it, and legalising hugging but advising “cautious cuddling”. But are the Britons as confused as

commentators insist? Not according to the public themselves. Two thirds of

people say the government’s guidance for which activities you should and

shouldn’t do is very (19%) or fairly (48%) clear. Around three in ten feel

less certain, however, and say it’s either not very (19%) or not at all clear

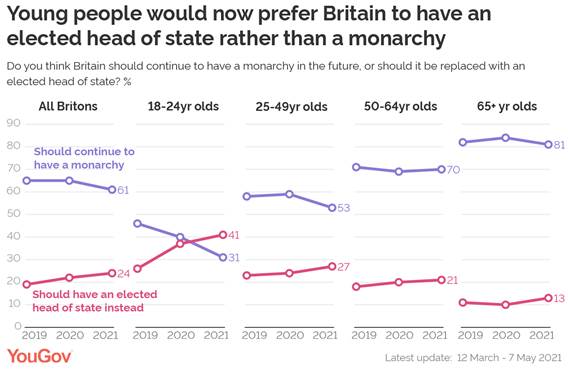

(9%). (YouGov UK) May 20, 2021 41% Of 18-24 Year Olds Now Say Britain Should Have An Elected

Head Of State Attitudes among young people to the

monarchy have changed substantially since 2019. YouGov data from a number of

our 2021 polls on the monarchy so far shows that 41% of 18-24 year olds now

say Britain should have an elected head of state, while only 31% would like

to see the monarchy continue. The results, which are likely to be cause for

concern for Buckingham Palace, come after a turbulent start to 2021, with

Harry and Meghan’s controversial Oprah interview in March and Prince Philip’s passing

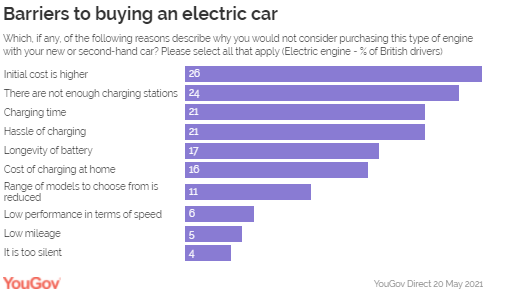

in April. (YouGov UK) May 21, 2021 Charging An Electric Car Vs Refuelling A Petrol Car, 14%

Think It’s Better; 13% Think It’s The Same, And 64% Think It’s Worse For all the positivity around the features

of electric cars, a major sticking point for Britons when it comes to EVs is

the hassle associated with charging a car compared to filling it up with

petrol. A comfortable majority of the public thinks battery-powered vehicles

are more inconvenient to run than petrol cars (64%), while just 14% think

petrol cars are worse in this area. This extends to aesthetics: in terms of

exterior design, three-quarters say they look the same or better (76%); when

asked about interior design, four in five (80%) think they’re superior, while

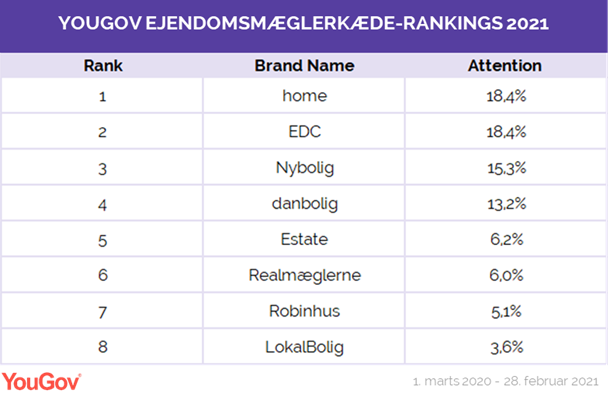

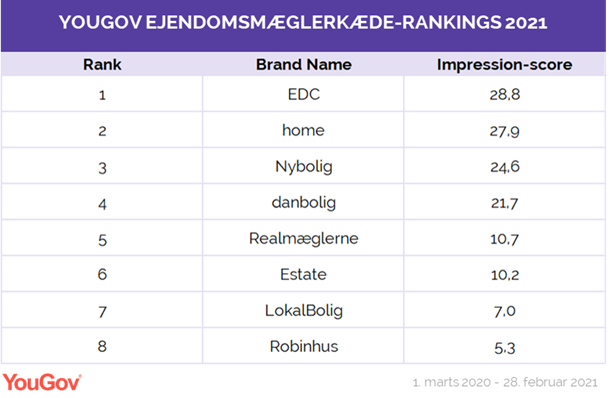

just 7% think they look inferior. (YouGov UK) May 21, 2021 (Denmark) Home And EDC Are Real Estate Chains Get The Most Attention

In Denmark When it comes to attention, home and EDC

share first place. An average of 18.4% of Danes have thus heard positive

or negative mention of these chains through advertising, news, word-of-mouth

or friends and family over the past year. In third and fourth place are

Nybolig (15.3%) and danbolig (13.2%). From the four big real estate

chains, there is a distance down to chains like Estate and Realmæglerne,

which are fighting for fifth place with an attention score of resp. 6.2%

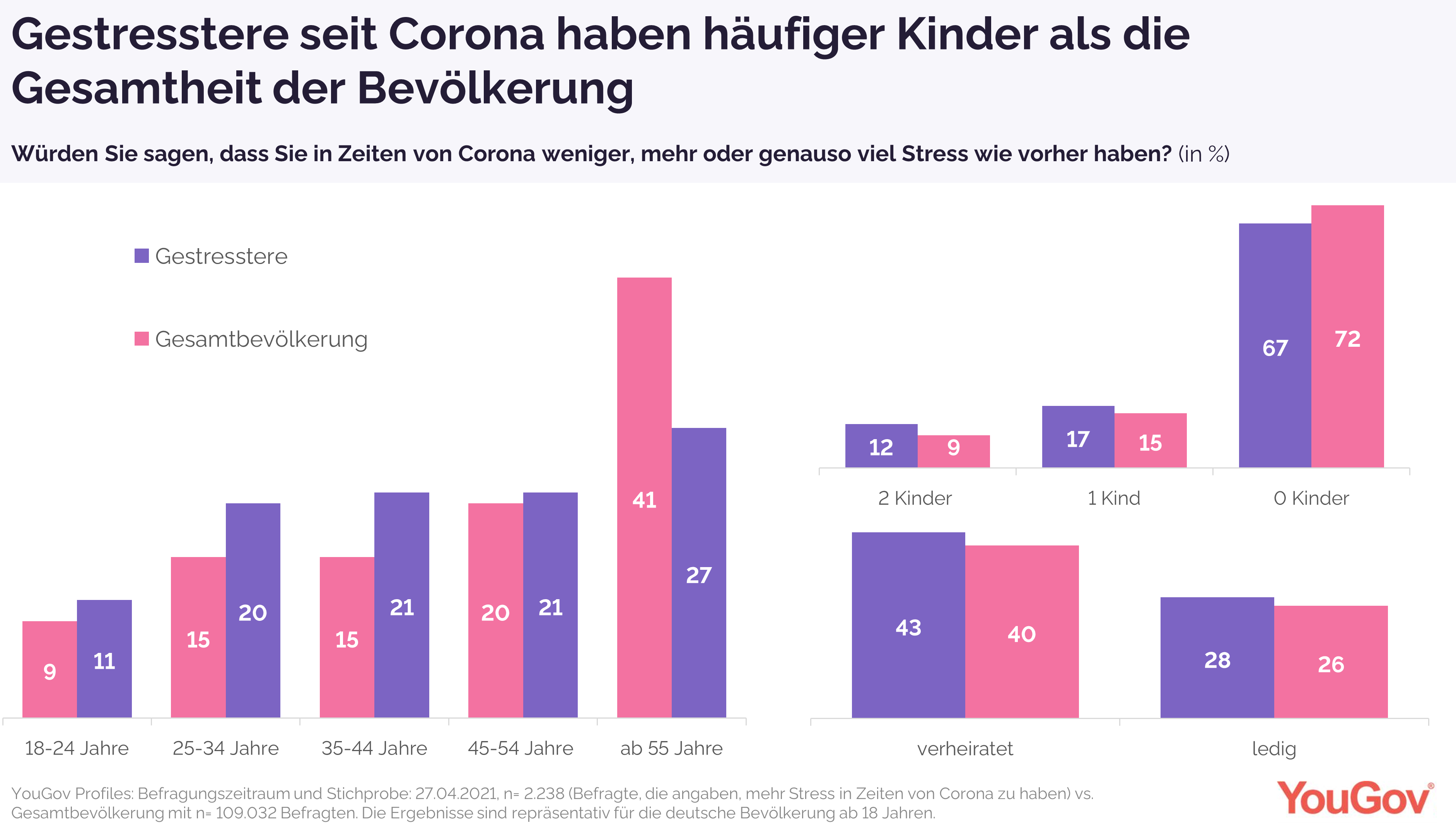

and 6%. (YouGov Denmark) (Germany) Every Third German Feels More Stressed In 2021 Than Before

Corona, People With Children Most Often A survey from the end of April 2021,

compared to April 2020, showed that people in times of Corona feel more

stressed this year than they did a year ago. At that time, 17 percent

said they felt more stressed than before, in 2021 31 percent said they were

more stressed, 14 percentage points more than a year ago. 51 percent

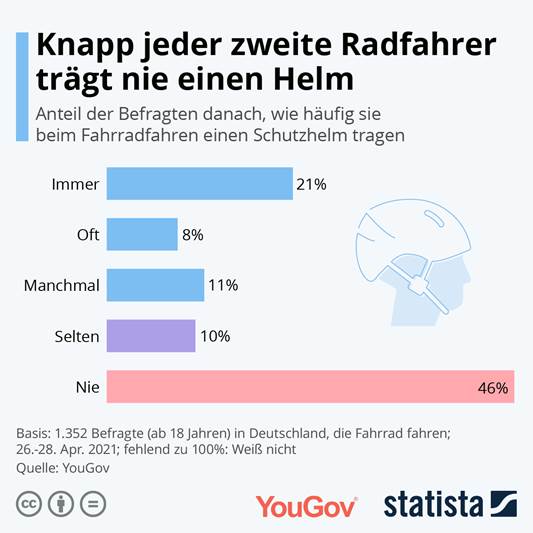

currently do not notice any change in their stress level due to Corona. (YouGov Germany) May 7, 2021 Every Second Cyclist Wears A Protective Helmet At Least Now

And Then When Cycling Spring and summer are just around the

corner - time to cycle again more often. The majority of Germans (63

percent) have their own bike, most of them a city bike (28 percent), and 14

percent own a cross bike or mountain bike. 10 percent of the German

respondents state that they own an e-bike. 36 percent of Germans do not

own a bicycle, including more women (40 percent) than men (31

percent). This was the result of a current survey in cooperation with

Statista. (YouGov Germany) May 5, 2021 26 Percent Germans Praised The Government's Handling Of The

Crisis In April 2021 At the beginning of 2021, the proportion of

those who rated the federal government's handling of the crisis negatively

was higher than the proportion of those who voted positively for the first

time: in January 2021, 49 percent had a negative and 46 percent a positive

image. According to current YouGov Corona Tracker data, a reversal of

this trend can currently be seen: After only a quarter of all respondents (26

percent) praised the government's handling of the crisis in April 2021, the

lowest value since the tracker began, attested in May 39 percent of the

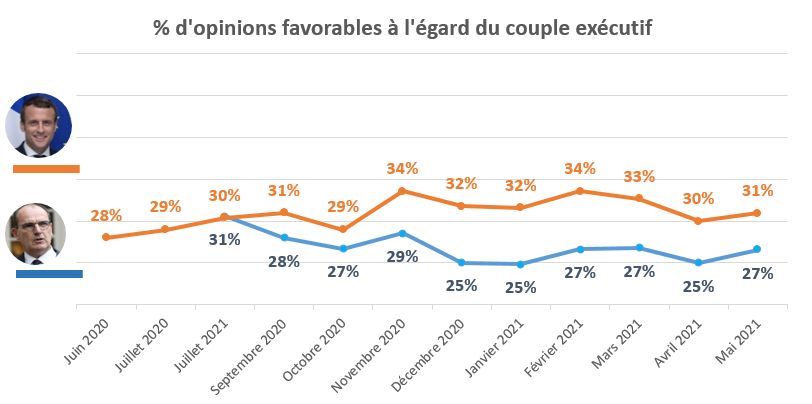

government is good practice. (YouGov Germany) (France) This Month, The President Of The France Recovers 1 Point Of

Favorable Opinions From The French (31% Of Favorable Opinions) This month, the President of the Republic

recovers 1 point of favorable opinions from the French (31% of favorable opinions) . In

detail, the Head of State is making progress with all fringes of opinion

except the moderate Left and the Far Right. Indeed, Emmanuel Macron

gains 10 points from supporters of the Far Left (18% of favorable opinions),

5 points from supporters of the Center (82% of favorable opinions) and 2

points from supporters of the moderate Right. (36% favorable

opinions). It loses, on the other hand, 2 points with sympathizers of

the moderate Left (29% of favorable opinions) and of the Far Right (8% of favorable

opinions). (YouGov France) May 7, 2021 A Quarter Of 18-25 Years Old Say They Have Had

Suicidal Thoughts Since The Start Of The Crisis (27%) This distress experienced by young people

since the start of the health crisis is all the more worrying as more than a quarter of them say they have had suicidal thoughts

since the start of the crisis (27%), a proportion that has

increased from 4 points in 9 months. Students and young people currently

looking for a job appear to be particularly concerned (31% and 35%

respectively). (Ipsos France) May 10, 2021 45% French Believe That Major Beauty Brands Do Not

Care Enough About The Diversity Of Their Consumers In terms of offer, consumers are largely

satisfied with the diversity of the

beauty sector , 77% of

them saying they easily find products that match their physical

characteristics. When it comes to communication, things are

more complicated: 51% are

not represented in brand communication ,

especially men ( 59% of

them), undoubtedly because they are targeted by far fewer products, but also

the oldest ( 62% of

55- 75 years old) 45% believe

that major beauty brands do not care enough about the diversity of their

consumers. (Ipsos France) May 18, 2021 (Italy) 9 May, Europe Day: The European Union In The Perception Of

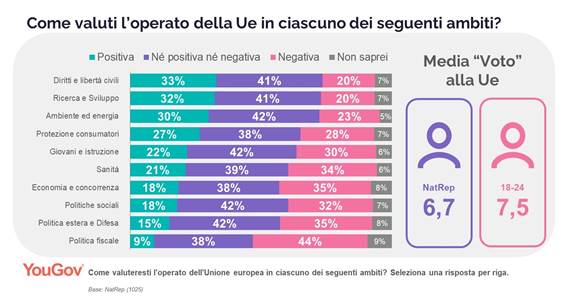

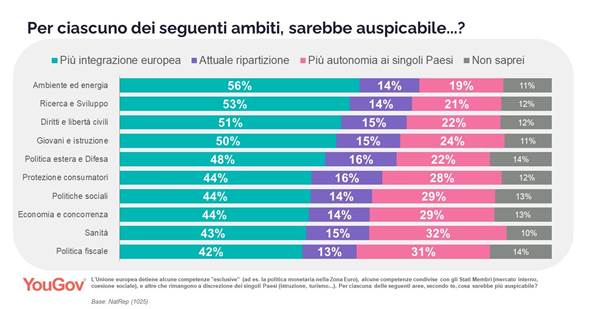

Italians On 9 May the European Union celebrates

Europe Day , in memory of the Schumann

Declaration, which set the tone for the first European Coal and Steel

Community (ECSC). More than seventy years later, this anniversary remains unrecognized in Italy: only

5% of Italians know how to place this day among the May

holidays (against over 90% who know how to place the Labor Day), a percentage

that rises however 11% among young

people aged 18-24. Only 10% say they are generally aware

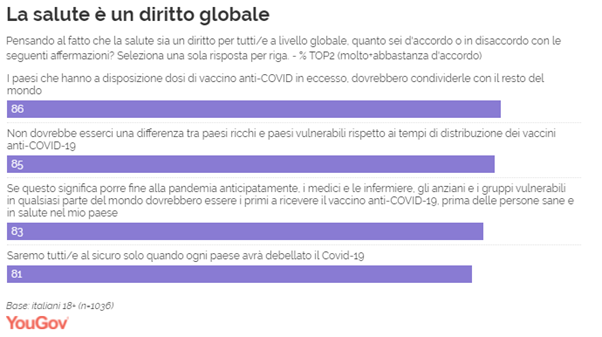

of Europe Day and its meaning, plus 25% who have heard of it. (YouGov Italy) May 7, 2021 8 Out Of 10 Italians And Italians Agree: Excess Doses Of

The Anti-Covid 19 Vaccine Must Be Shared 8 out of 10 Italians and Italians agree:

excess doses of the anti-COVID 19 vaccine must be shared, because only by

eradicating the virus everywhere will the pandemic be put to an

end. This emergency situation requires a response that goes beyond

borders and national income differences (85%), with immunization that gives

priority to the categories of people most vulnerable and at risk in the face

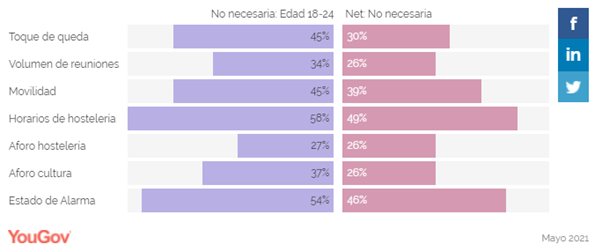

of the threat of the virus (83%). (YouGov Italy) (Spain) 40% Of Spaniards Do Not Agree With The Changes In The

Measures Implemented In Their City After The Fall Of The State Of

Alarm Young people between 18 and 34 years old

are the group of the population that is most in favor of the changes in the

measures (42% in both cases), compared to the rest of the population, where

the most negative age group towards the arrival of This new normal would be

between 45 and 54 years of age (46% do not agree with the new

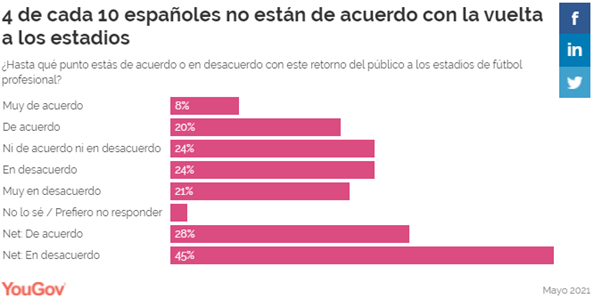

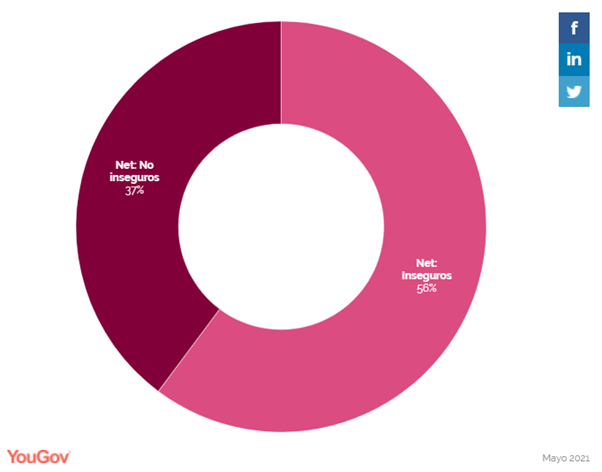

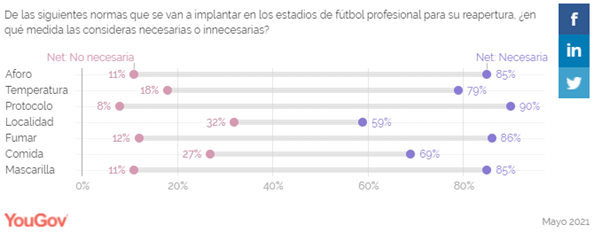

measures). (YouGov Spain) Four Out Of Every Five Spanish Respondents (45%) Rejects

The Fact That They Can Return To Stadium Fans Last Wednesday, May 12, the return of the

public to the stands of the professional football stadiums was

approved. This measure will be valid only for communities in phase 1,

with a cumulative incidence of less than 50 cases per 100,000 inhabitants in

the last 14 days. With this new measure, stadiums will be able to accommodate

30% of their capacity as long as they do not exceed 5,000 spectators, they

must wear a mask and maintain a safety distance, among other rules. (YouGov Spain) May 20, 2021 (Hungary) Only one in five Hungarians is vaccinated Thanks to improving epidemic data and

rising vaccination rates, the population is moving more freely and letting

their children into the community, interacting with others. The rate of

wearing a face mask was 87%, with a lower level most recently seen in

November. The 73% mention of frequent hand washing against infection is

the lowest in the history of the research series . The outlook for public

transport and the event market is mild, with domestic tourism improving

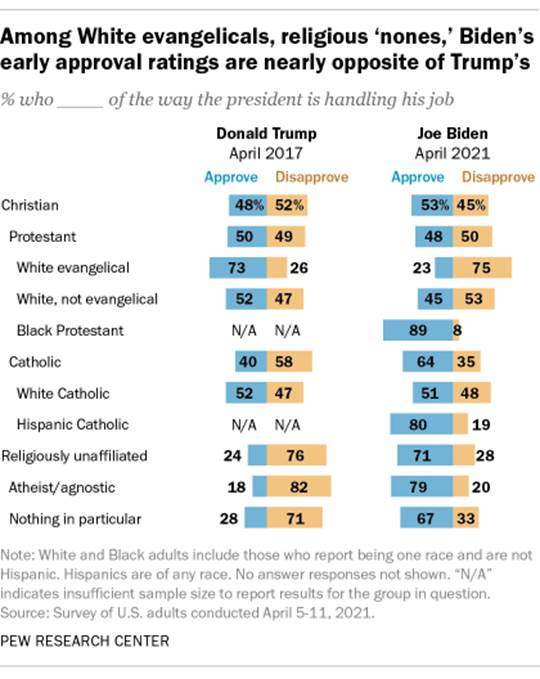

significantly over the past month. (Ipsos Hungary) May 20, 2021 NORTH AMERICA (USA) Three-Quarters Of White Evangelical Protestants (75%) Say

They Disapprove Of The New

President’s Performance So Far Seven-in-ten religiously unaffiliated

adults (71%) say they approve of how Biden is handling the job of president,

compared with three-quarters (76%) who said they disapproved of Trump’s performance in

April 2017. At the other end of the spectrum, three-quarters of White

evangelical Protestants (75%) say they disapprove

of the new president’s performance so far, which is about equal to the share

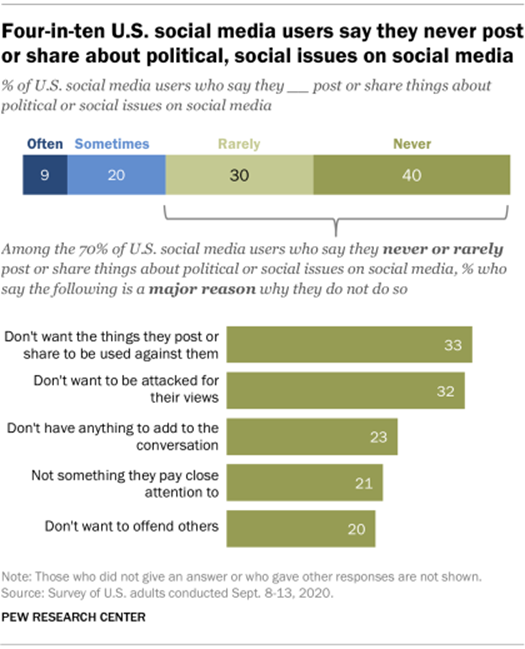

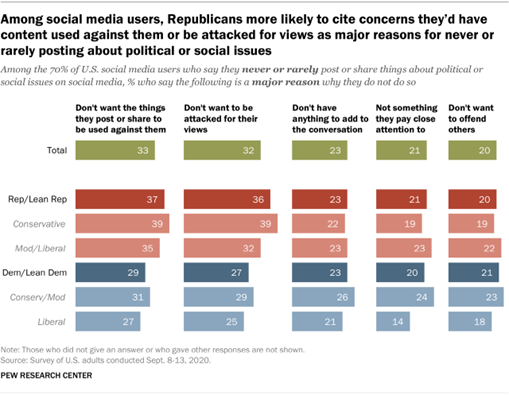

who approved of Trump’s performance four years ago (73%). (PEW) MAY 4, 2021 70% Of U.S. Social Media Users Never Or

Rarely Post Or Share About Political, Social Issues Only 9% of adult social media users say they

often post or share things about political or social issues on social media,

according to newly released results from a Pew Research Center survey of U.S.

adults conducted Sept. 8-13, 2020. Some 70% of social media users say they

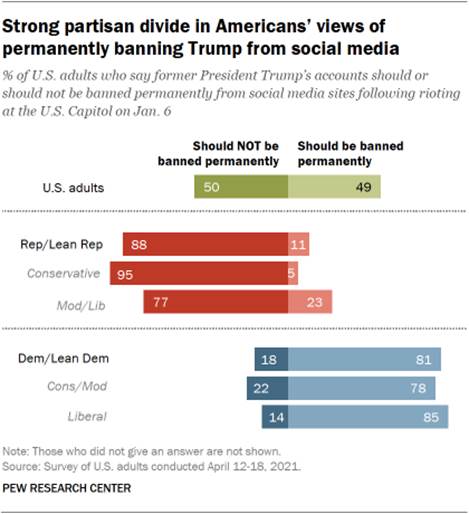

never (40%) or rarely (30%) do so. (PEW) MAY 4, 2021 Just 11% Of Republicans And

Republican-Leaning Independents Say Trump’s Accounts Should Be Permanently

Banned From Social Media Americans are split on whether former

President Donald Trump should be barred from social media. Some 49% of U.S.

adults say Trump’s accounts should be permanently banned from social media,

while half say they should not be. But views are deeply divided along

partisan lines, according to a new Pew Research Center survey. And then

– just like today – most Republicans (78%) said social media companies’

decisions to ban Trump’s accounts following the riots were the wrong thing to

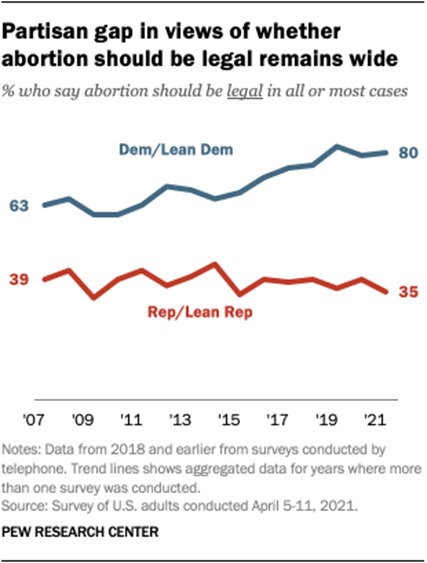

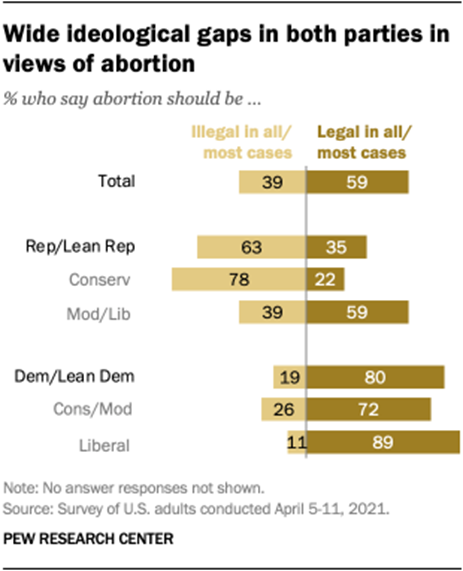

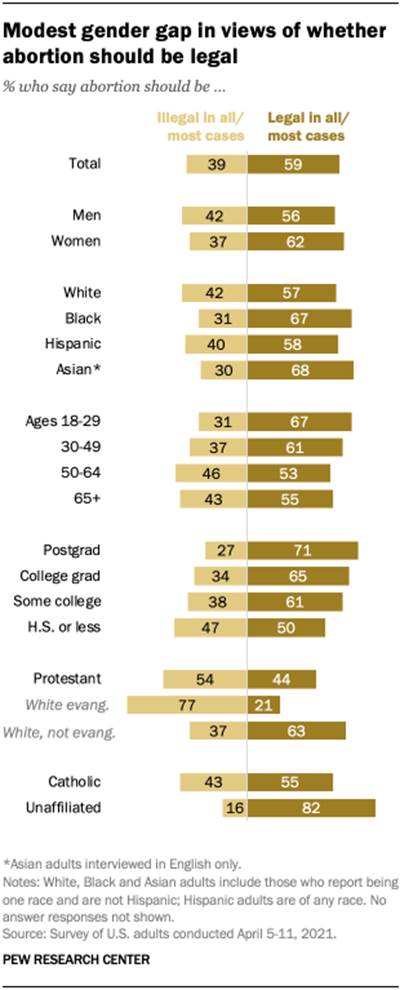

do, while a vast majority of Democrats (89%) supported these decisions. (PEW) MAY 5, 2021 About Six-In-Ten Americans Say Abortion

Should Be Legal In All Or Most Cases Today, a 59% majority of U.S. adults say

abortion should be legal in all or most cases, while 39% think abortion

should be illegal in

all or most cases. These views are relatively unchanged in the past few

years. The latest Pew Research Center survey, conducted April 5 to 11, finds

deep disagreement between – and within – the parties over abortion. In fact,

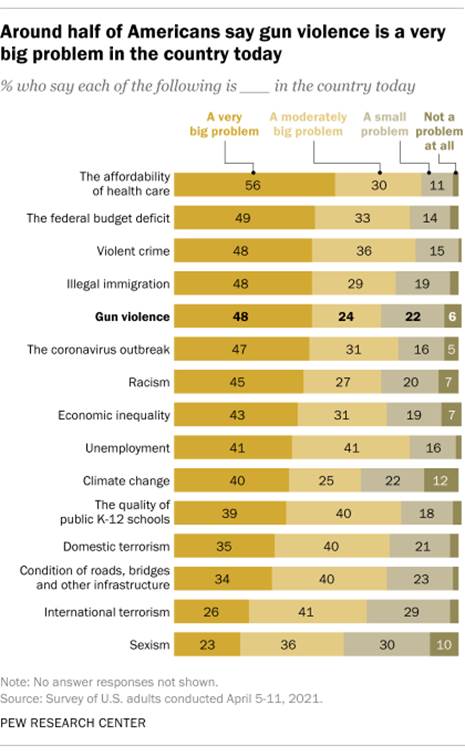

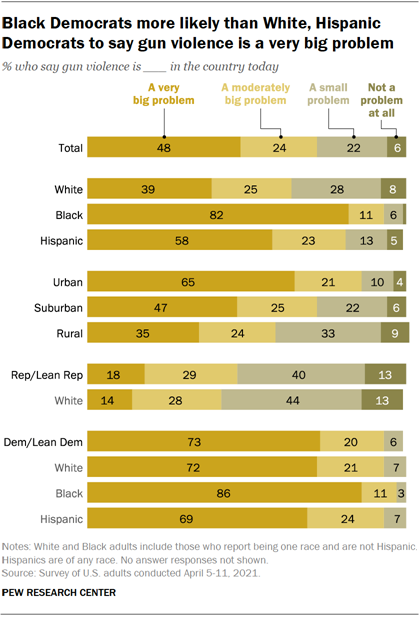

the partisan divide on abortion is far wider than it was two decades ago. (PEW) MAY 6, 2021 Around Half Of Americans (48%) See Gun

Violence As A Very Big Problem In The Country Today According to a Pew Research Center survey conducted in April 2021. That’s

comparable to the share who say the same about the federal budget deficit

(49%), violent crime (48%), illegal immigration (48%) and the coronavirus

outbreak (47%). Only one issue is viewed as a very big problem by a majority

of Americans: the affordability of health care (56%). Another 24% of adults

say gun violence is a moderately big problem. About three-in-ten say it is

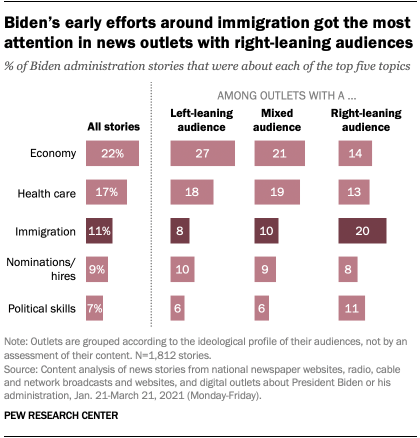

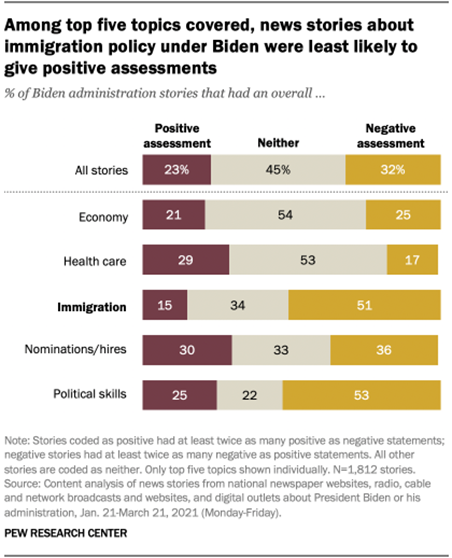

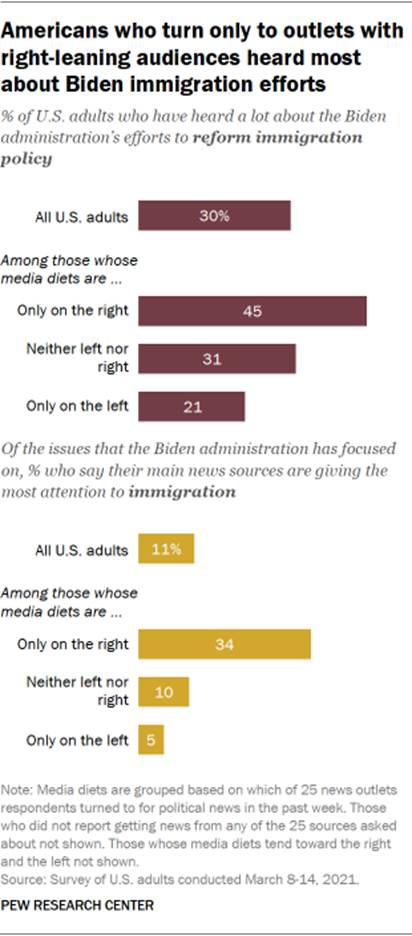

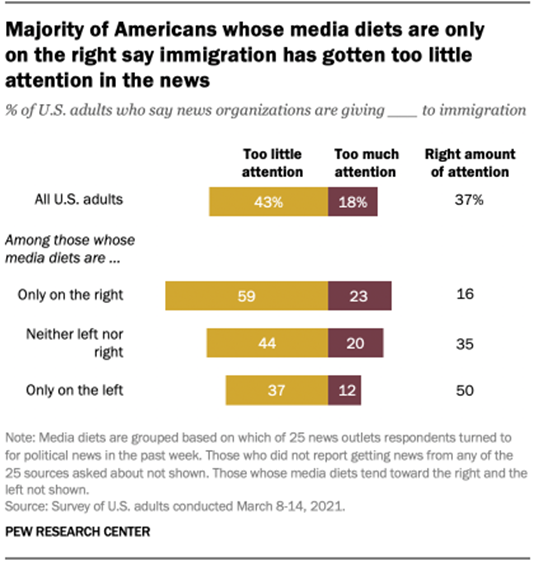

either a small problem (22%) or not a problem at all (6%). (PEW) MAY 11, 2021 Immigration Was A Top Focus Of Early Biden

Coverage, Especially Among Outlets With Right-Leaning Audiences The topic of immigration (which included

all references to immigration, including broader trends and changes in law,

as well as stories about the border with Mexico) accounted for about twice as

many stories from outlets with right-leaning audiences (20%) as from news

outlets with left-leaning audiences (8% of stories) and those with

ideologically mixed audiences (10%). (Details about how news outlets were

grouped can be found here.) Indeed, among those outlets with

right-leaning audiences, immigration was the No. 1 topic among stories

related to the new administration, well ahead of both the economy (14%) and

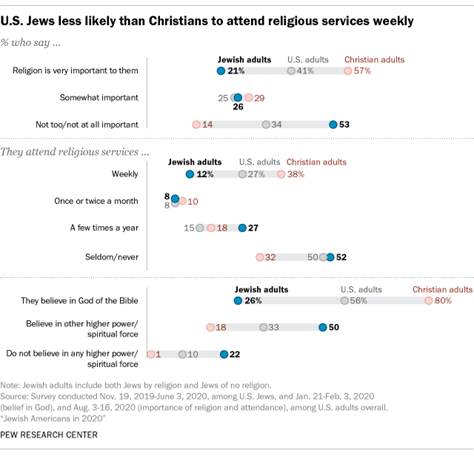

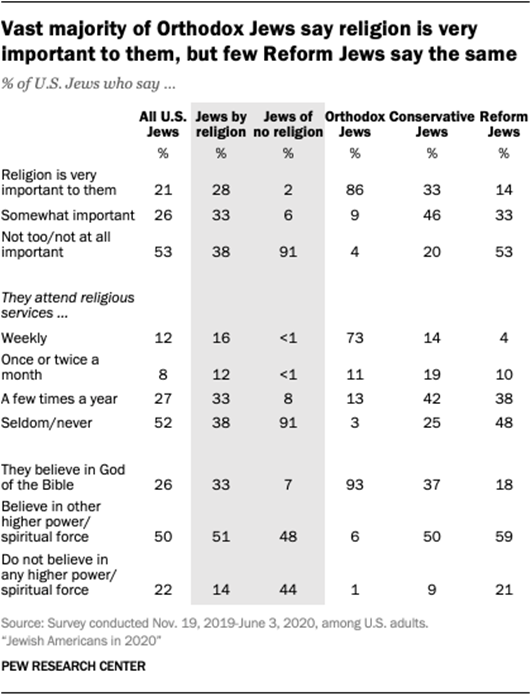

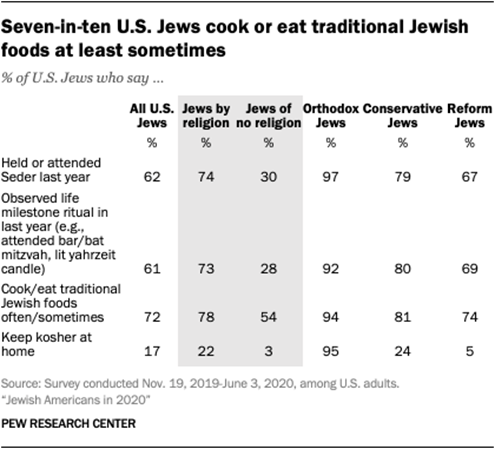

health care (13%). (PEW) MAY 12, 2021 12% Of Us Jewish Adults Say They Attend

Religious Services Weekly Or More Often, Compared With 27% Of The General

Public And 38% Of Us Christians 12% of U.S. Jewish adults say they attend

religious services weekly or more often, compared with 27% of the general

public and 38% of U.S. Christians. And 21% of Jewish adults say religion is

very important in their lives, compared with 41% of U.S. adults overall and

57% of Christians. Orthodox Jews – who make up 9% of all U.S. Jews – are a

notable exception. They are among the most highly religious groups in U.S.

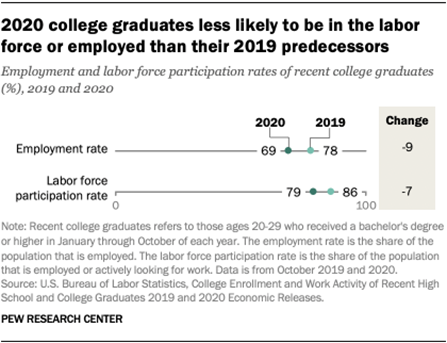

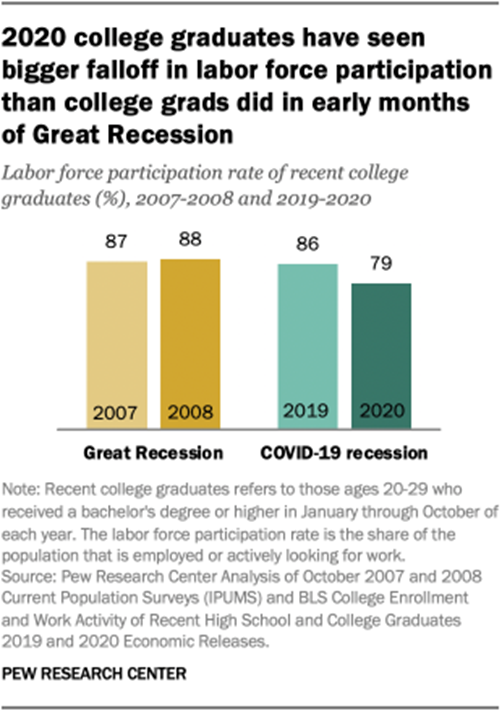

society by these measures. (PEW) MAY 13, 2021 69% Of Adults Ages 20 To 29 Who Had Graduated

From College During The Previous Spring Were Employed, Lower Than The Share

Of 2019 Graduates Who Were Employed In October Of That Year (78%) The labor force participation rate for

recent college graduates – or the share of people employed or actively

looking for a job – also dropped from 86% to 79% during this one-year period.

As has been widely documented, the broader labor market took a

significant hit during the pandemic. Among all Americans ages 16 and older,

the employment rate declined from 61% in October 2019 to 58% in October 2020,

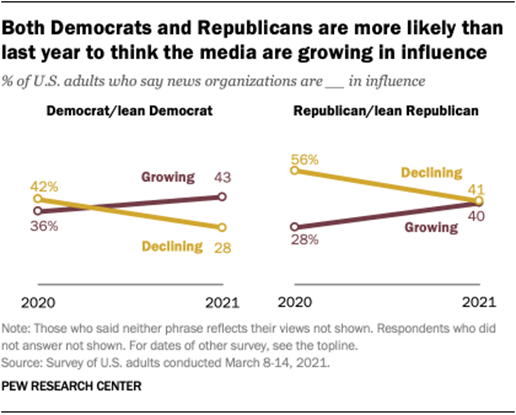

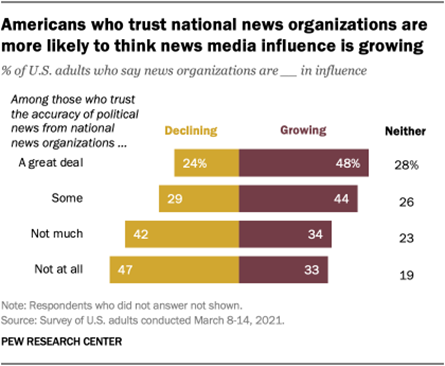

and the labor force participation rate declined from 63% to 62%. (PEW) MAY 14, 2021 About Four-In-Ten (41%) Americans Say News

Organizations Are Growing In Their Influence When Americans were asked to evaluate the

media’s standing in the nation, about four-in-ten (41%) say news

organizations are growing in their influence, somewhat higher than the

one-third (33%) who say their influence is declining, according to a Pew

Research Center survey conducted March 8-14, 2021. The remaining one-quarter

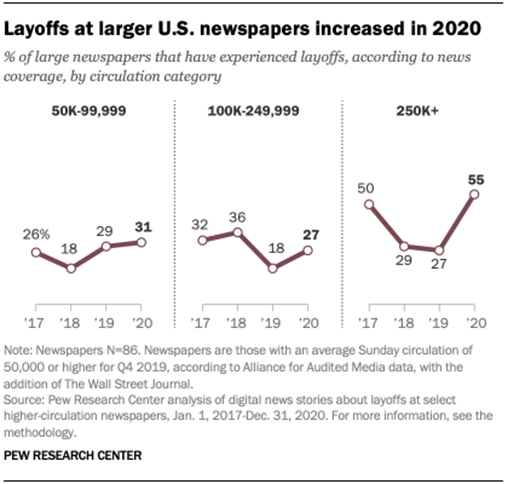

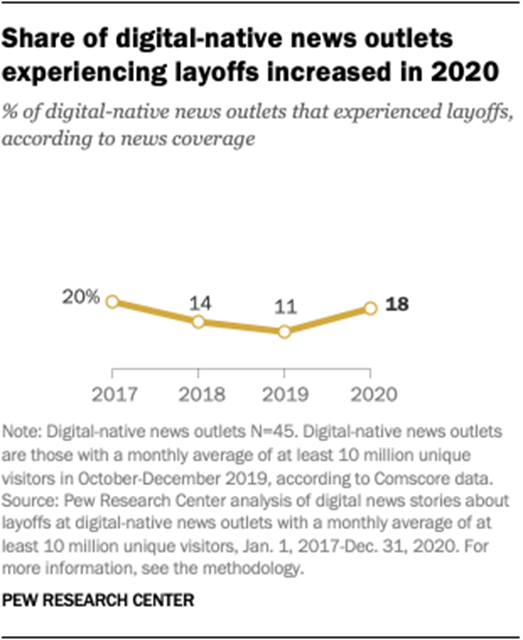

of U.S. adults say they are neither growing nor declining in influence. (PEW) MAY 17, 2021 A Third Of Large US Newspapers Experienced

Layoffs In 2020, More Than In 2019 Large-market newspapers – those with a

Sunday circulation of 250,000 or more – were the most likely to suffer

layoffs in 2020, with more than half of them experiencing staff cuts. That is

unlike 2019, when cuts were roughly similar across the different tiers of

circulation groups studied. Meanwhile, digital-native news outlets saw a slight uptick in

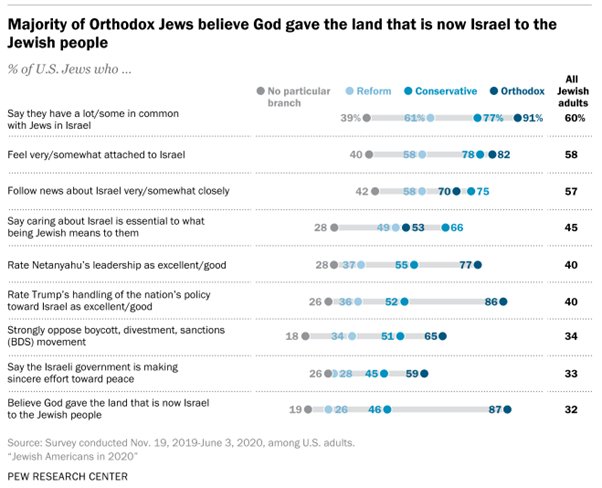

layoffs in 2020 compared with 2019. (PEW) MAY 21, 2021 45% Of US Jewish Adults, And An Additional

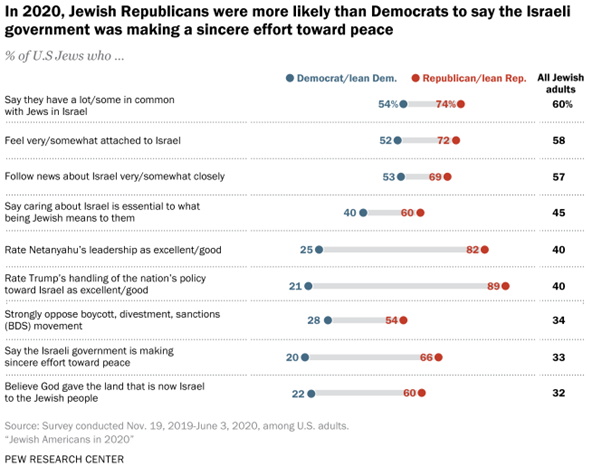

37% Say Caring About Israel Is Important, But Not Essential Israel, the world’s only Jewish-majority

country, is a subject of special concern to many Jews in the United States.

Caring about Israel is “essential” to what being Jewish means to 45% of U.S.

Jewish adults, and an additional 37% say it is “important, but not

essential,” according to a new Pew Research Center survey that was fielded from Nov. 19, 2019,

to June 3, 2020 – well before the latest surge of violence in the region. Just 16% of U.S. Jewish adults say that

caring about Israel is “not important” to their Jewish identity. (PEW) MAY 21, 2021 (Canada) Liberals (38%) in the Driver’s Seat over

Conservatives (29%) as Vaccination Rollout Hits its Stride If the election were held tomorrow, 38% of

decided voters would vote for the Liberal Party led by Justin Trudeau,

unchanged since Ipsos/Global News post-budget survey last month. Three in ten

(29%) would vote for Erin O’Toole’s Conservative Party, up 2 points since

last month. Two in ten (21%) decided voters would cast their ballot for their

local NDP candidate, led by Jagmeet Singh, also up 2 points. Yves-Francois

Blanchet and the Bloc would receive 6% of the vote nationally, down 1 point

(or 30% of the popular vote within in Quebec). (Ipsos Canada) 18 May 2021 Seven In Ten (70%) Canadians Believe Summer

2021 Will Be A Disappointment Given The Ongoing Covid Restrictions Given the ongoing COVID-19 restrictions

that have been implemented throughout the country, a strong majority (70%) of

Canadians agree (21% strongly/49% somewhat) that this summer will be a

disappointment, according to a new Ipsos poll conducted on behalf of Global

News. Those residing in Ontario and Atlantic provinces are the most likely to

agree that summer 2021 will be a disappointment, while those in Quebec are

least likely to agree (75%, 75% vs 62%). Perhaps not surprising, those who

have not been

vaccinated are more likely to agree that this summer will be a disappointment

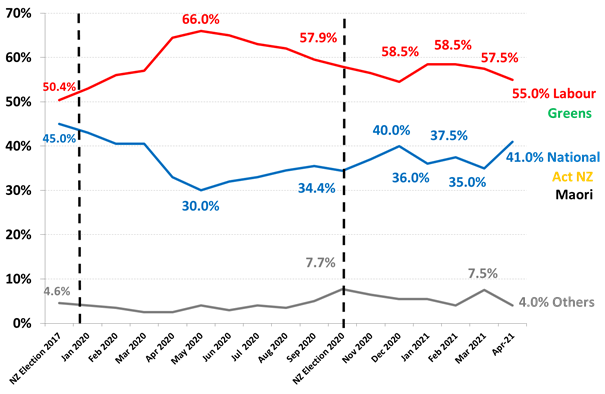

compared to those who have been vaccinated (74% vs 67%). (Ipsos Canada) 20 May 2021 AUSTRALIA (New Zealand) New Zealand Government Lead Over Opposition Down To 14% In

April – Smallest Lead Since January 2020 The governing parties are now 14% points

ahead of the Parliamentary opposition National/Act NZ/Maori Party on 41%, up

6% points since March. Support for National has now recovered to its highest

since last year’s election, up 6.5% points to 29.5%, and is the highest for

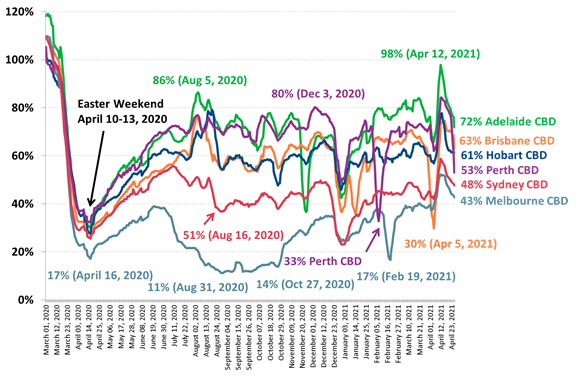

exactly a year since April 2020 at the start of the COVID-19 pandemic. (Roy Morgan) May 03 2021 (Australia) Movement In The Sydney, Melbourne And Adelaide Cbds Drops

In Late April After Hitting Covid-19 Highs Over The Easter Holidays Since school holidays ended average 7-day

movement levels have declined across all Capital City CBDs including the

Melbourne CBD (down 9% points to 43%), Sydney CBD (down 11% points to 48%),

Brisbane CBD (down 12% points 63%) and Hobart CBD (down 16% points to 61%).

The largest declines in average movement were seen in the Adelaide CBD

(26%-point decline to 72%) and the Perth CBD which experienced a sharp 31%-point

decline to 53% average movement as the city entered a snap three-day lockdown

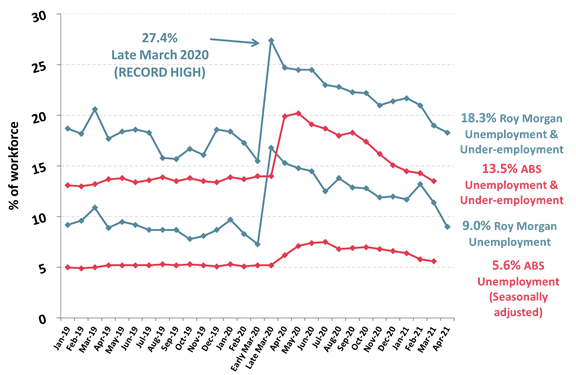

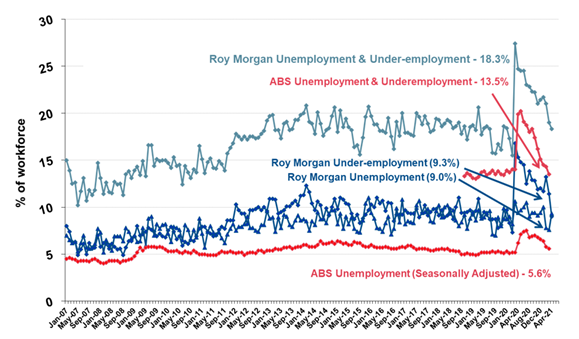

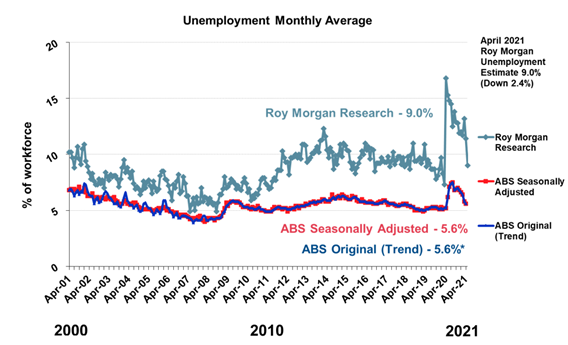

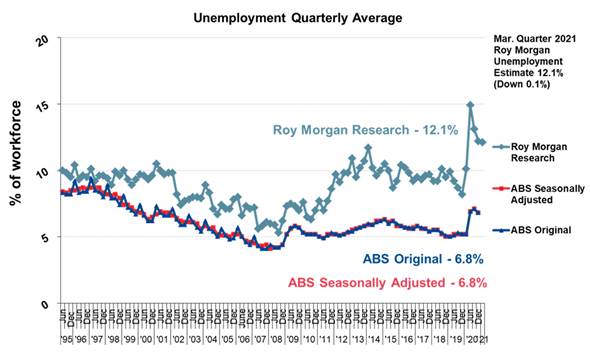

over the three-day ANZAC Day weekend. (Roy Morgan) May 03 2021 Australian Employment Hits A Record High

Above 13 Million In April – Unemployment Down, But Offset By Rising

Under-Employment 13,291,000 Australians were employed, up

542,000 from March driven by an increase in part-time employment, up 413,000

to a record high 4,757,000. Full-time employment was up 129,000 to 8,534,000. Unemployment dropped in April to its lowest since

early March 2020 (pre-pandemic): 1,307,000 Australians were

unemployed (9.0% of the workforce),

down 332,000 from March. There were fewer people looking for both full-time

work (down 75,000 to 593,000), or part-time work (down 257,000 to 714,000). (Roy Morgan) May 06 2021 A Huge Majority Of 93% Of Australians Said

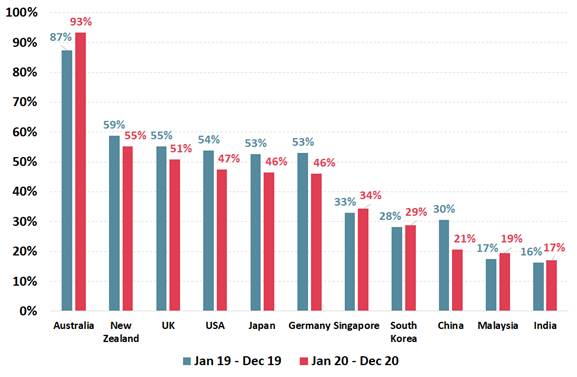

They Are More Likely To Buy Products Made In Australia A huge majority of 93% of Australians said

they are more likely to buy products made in Australia – up from 87% a year

earlier. The big ‘loser’ during 2020 was Chinese-made goods with only 21% of

Australians saying they’d be more likely to buy products made in China, a 9%

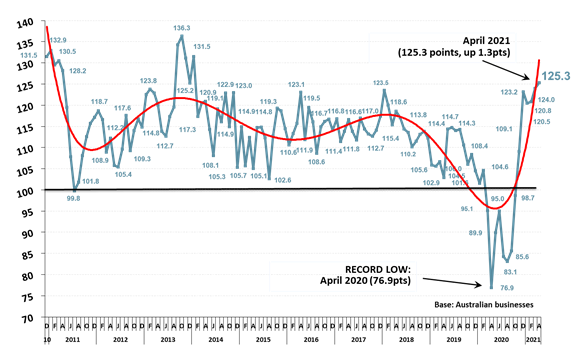

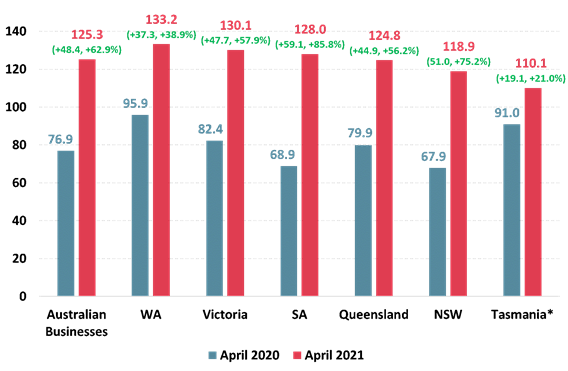

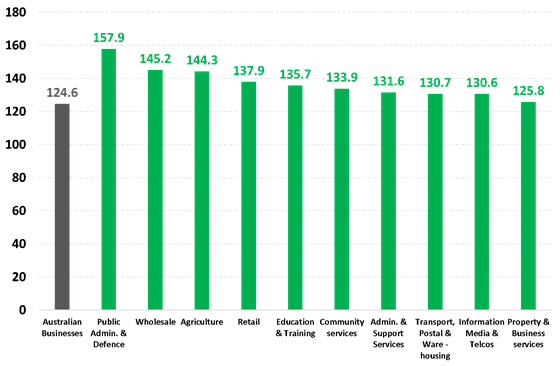

points drop from 2019. (Roy Morgan) May 10 2021 Roy Morgan Business Confidence Hits 7-Year

High Of 125.3 In April – Up 48.4 Pts (+62.9%) On A Year Ago Business Confidence is now 11.6pts above

the long-term average of 113.7 and nearly two-thirds, 65%, expect ‘good

times’ for the Australian economy over the next 12 months and an increasing

majority of 59.5% of businesses said the next 12 months is a ‘good time to

invest in growing the business’. Business Confidence has now averaged 122.7

during the first four months of 2021, the best start to a year for the Index

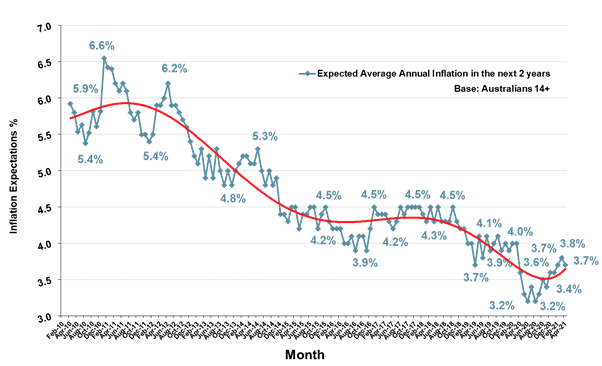

for a decade since 2011 – during the middle of the ‘Mining Boom’. (Roy Morgan) May 11 2021 Inflation Expectations Virtually Unchanged

At 3.7% In April – Far Higher For Unemployed (4.5%) Than Full-Time Employees

(3.4%) Inflation Expectations are now 1% point

below their long-term average of 4.7% but have increased by 0.5% points since

reaching a record low of only 3.2% in August 2020. This is far higher than

Australians employed either part-time on 3.9% (up 0.5% points) or full-time

on 3.4% (up 0.8% points). Interestingly, Australians who are employed

part-time but want more work, the under-employed, have Inflation Expectations

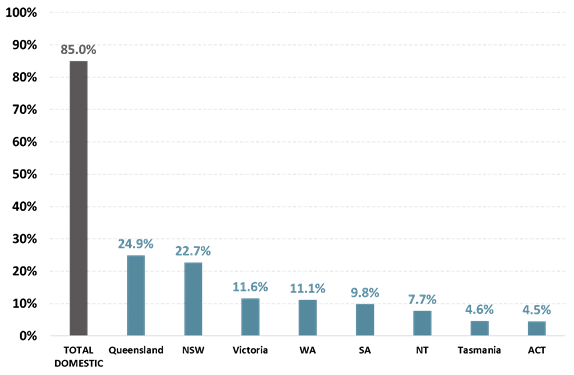

of 4.4% (up 0.8% points) – almost as high as the unemployed. (Roy Morgan) May 11 2021 5.68 Million Australians (26.9% Of Those

Aged 14+) In The March Quarter 2021, Intend To Take A Holiday During The Next

12 Months Of these travellers there were 5.24 million

set on taking a domestic holiday and a further 340,000 planning an overseas

holiday – although according to this week’s Federal Budget the international

borders are set to remain closed for holidaymakers until early next year.

There were a small number of prospective travellers who couldn’t decide

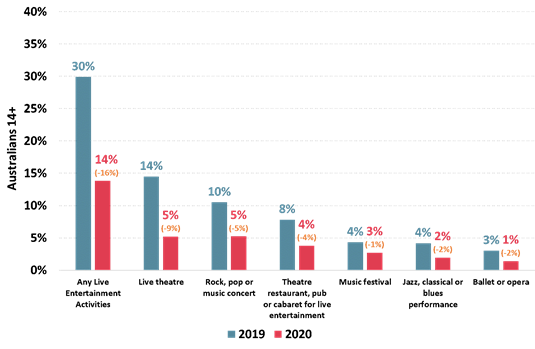

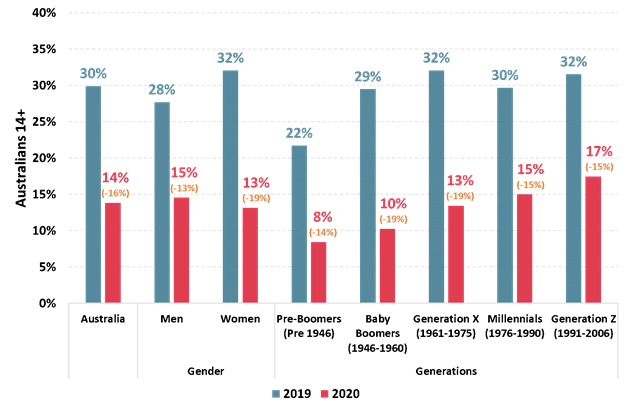

whether their holidays would be domestic or international. (Roy Morgan) May 14 2021 In 2020 Just 14% Of Australians Aged 14+ Attended Live Entertainment

Activities Such As Theatre, Rock, Pop Or Music Concerts Only 5% of Australians attended live

theatre in an average three months in 2020, down from 14% in 2019, and just

5% went to rock, pop or music concerts, compared to 10% in 2019. Attendance

at other activities including theatre restaurants, music festivals, jazz,

classical, blues, ballet or opera performances also plunged during 2020. The

re-opening of Australia that has occurred in 2021 and the rollout of the

COVID-19 vaccines this year should lead to a boost in attendance at live

entertainment activities although the threat of outbreaks means it is

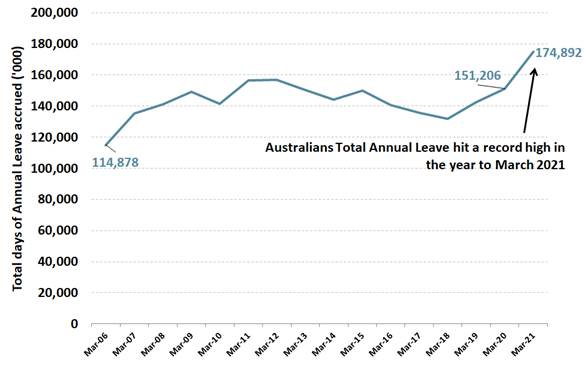

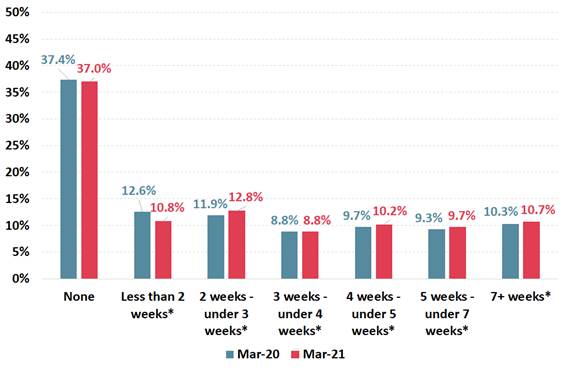

unlikely to approach the levels of 2019 just yet. (Roy Morgan) May 18 2021 Australians Have Nearly 175 Million Days Of

Annual Leave Due – Up Over 23 Million Days From Early 2020 The accrued annual leave of nearly 175

million days is a record high total of accrued annual leave and represents an

increase of 23.7 million (+15.7%) on the 151.2 million days of accrued annual

leave Australians had available prior to the COVID-19 pandemic. Now over 6.69

million Australians (52.2% of paid workers) have at least 2 weeks of annual

leave due, up from 6.14 million prior to the pandemic, while fewer than 1.38

million (10.8%) have less than 2 weeks due compared to over 1.54 million

(12.6%) pre-pandemic. (Roy Morgan) May 18 2021 In 2020 Only 24% Of Australians Said They’d

Be More Likely To Buy Clothes If They Knew The Clothes Were ‘Made In China’,

Down 7% Points From 2019 In 2020 only 24% of Australians said they’d

be more likely to buy clothes if they knew the clothes were ‘Made in China’,

down 7% points from 2019. The same trend was evident for Chinese-made

electrical goods with 23% (down 5% points from 2019) of Australians saying

they’d be more likely to buy the product if they knew it was ‘Made in China’,

mobile phones on 22% (down 4%), footwear on 17% (down 6%) and sporting goods

on 14% (down 3%). (Roy Morgan) May 18 2021 MULTICOUNTRY STUDIES A Closer Look At The European Criteria For Grocery Purchases

Shows That The Main Criteria Are Product Quality (88%) And Good Prices (82%) A closer look at the European criteria for

grocery purchases shows that the main criteria are product quality (88%) and

good prices (82%). Sustainable development is less important (53%), but

there are differences between countries. Italians (72%), Turks (72%) and

Spaniards (70%) consider the sustainability of products more important, while

Norwegians (29%), Danes (39%) and Finns (41%) consider it less important. (YouGov Finland) May 4, 2021 Source: https://yougov.fi/news/2021/05/04/eurooppalaiset-kuluttajat-ovat-muuttaneet-ostotott/ Ideological Divisions Over Cultural Issues

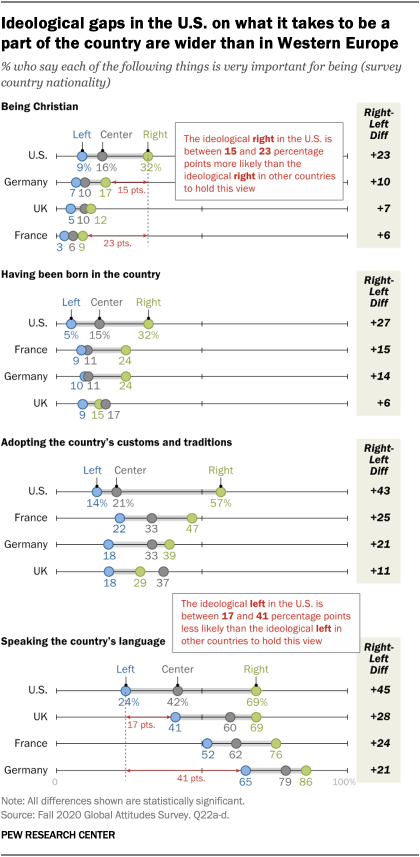

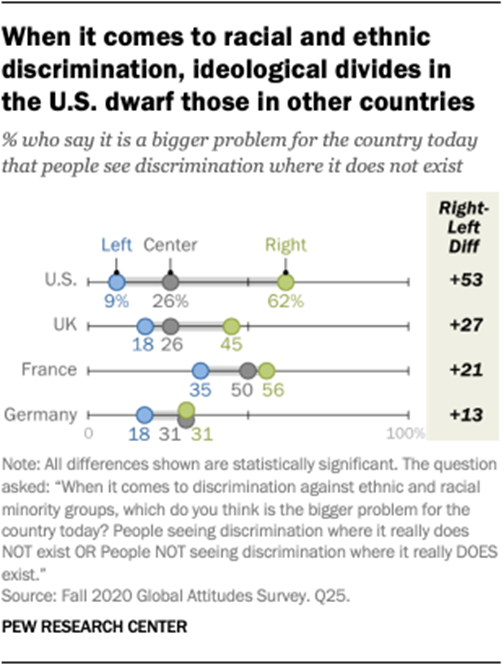

Are Far Wider In The U.S. Than In The UK, France And Germany When it comes to the importance of

being born in the

country, around a third on the U.S. right (32%) think it is very important

for being American, compared with no more than 24% of those on the right in

any other country. Similarly, those on America’s ideological right (57%) are

more likely than their counterparts in France (47%), Germany (39%) and the UK

(29%) to say that sharing national customs and traditions is very important

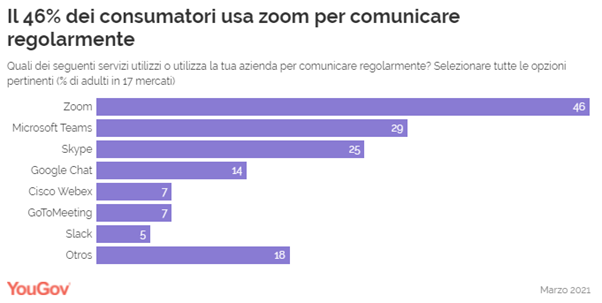

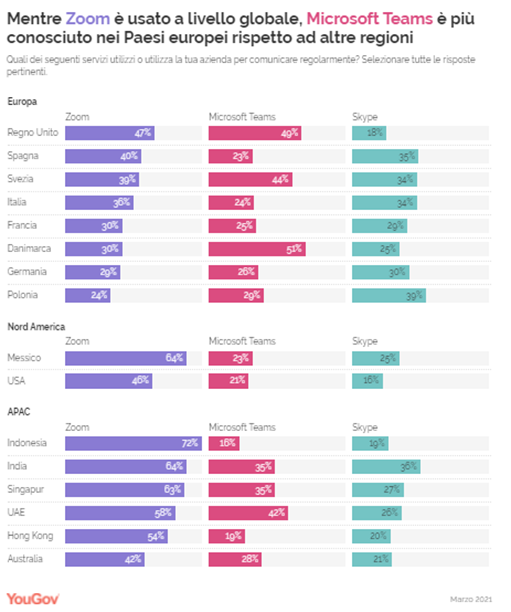

to national identity. (PEW) MAY 5, 2021 Nearly Half (46%) Of Consumers In 17 Global

Markets Use Zoom To Communicate Regularly Since the advent of COVID-19, Zoom has

become more than just a workmate, becoming in some markets even a verb

(“Let's Zoom!”) Or a real synonym for “video call”. Now, as parts of the

world slowly emerge from restrictions and more people return to the office,

YouGov data shows just how popular Zoom is and how it compares to other

competing services. Nearly half (46%) of consumers in 17 global markets

use Zoom to communicate regularly, while about three in ten (29%) use

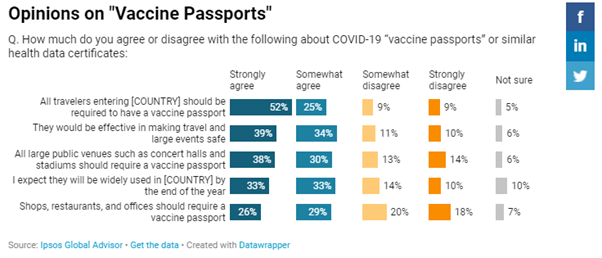

Microsoft Teams and a quarter (25%) use Skype. (YouGov Italy) May 10, 2021 Source: https://it.yougov.com/news/2021/05/10/global-data-la-popolarita-di-zoom-rispetto-ad-altr/ About Three Out Of Four Adults Globally

Agree That In Order To Enter Their Country, Travelers Are Required To Have

Covid-19 Vaccine Passports 78% agree that travelers must have a

vaccine passport in order to travel into their country. The countries

that agree most are Malaysia (92%) and Peru (92%).73% agree that vaccine

passes would be effective in making travel and major events safe; a

majority in each country agrees - from 84% in China and Argentina to 52% in

Hungary. 55% agree that vaccine passports should be required in shops,

restaurants and offices in all countries. Those who support this most

are India, where 78% agree, and those who support it least are in Poland

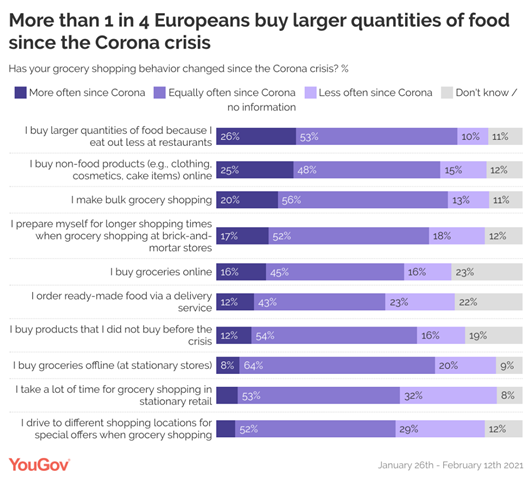

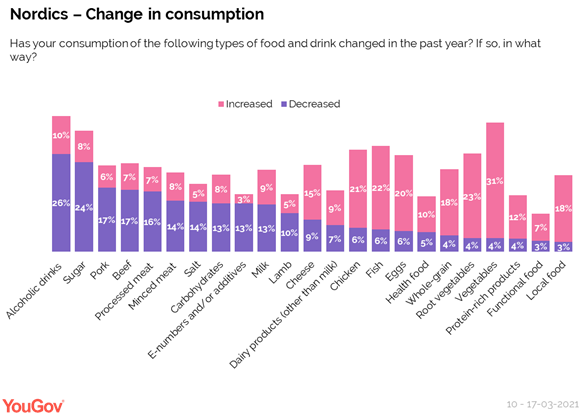

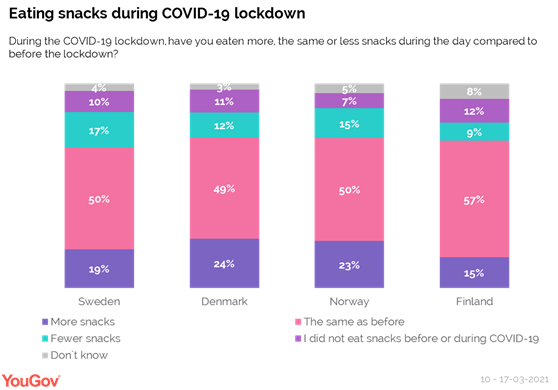

(55%), the United States (52%) and Belgium (52%). (Ipsos Denmark) 11 May 2021 Source: https://www.ipsos.com/da-dk/den-globale-befolkning-stotter-op-om-coronapas-til-internationale-rejser The Majority Of Nordic Countries State That

They Eat Healthier In The Form Of More Vegetables (31%) And Less Alcohol

(26%) And Sugar (24%) Across the Nordic countries, the majority

state that they eat healthier, eg in the form of more vegetables (31%) and

less alcohol (26%) and sugar (24%), Many have also cut back on meat -

primarily beef (17%), pork (17%) and processed meat (16%). In all four

countries, the intake of snacks has increased - but mostly in Denmark and

Norway, where a quarter (24% and 23% respectively) state that they have eaten

more snacks during lockdown. It is especially women, the younger part of

the population and households with children who have increased their snack

intake. (YouGov Denmark) May 16, 2021 Source: https://yougov.dk/news/2021/05/16/hvordan-har-et-ar-med-corona-pavirket-vores-madvan/ In UAE And Saudi, The Intent To Travel

Domestically Or Within The MENA Region Increased Slightly Data from the study shows six in ten

surveyed respondents (59%) in the UAE and Saudi Arabia said they took a

leisure trip (domestic or international) in 2020. In 2021, an appetite for

travel has improved, and more than seven in ten (72%) residents said they

have already or intend to travel this year. This is one of the highest rates

in the world. (YouGov MENA) Source: https://mena.yougov.com/en/news/2021/05/17/appetite-travel-recovers-middle-east-majority-resi/ 45% Of The Global Population Is Concerned

About Sharing Their Personal Information Digitally More than half of people in the American

continent (54%) feel concerned about sharing their information digitally. The

share of concerned people in other areas of the world remains significant: in

the APAC region, 45% are concerned about sharing personal information

digitally, and in Europe 43%. Interestingly, the Africa region experienced a

very significant drop of 22 points compared to last year (from 50% to 28%). (WIN) Globally, About Three In Four

Adults (78%) Are In Favor Of Requiring A Vaccination

Passport For Travelers Globally, about three in four adults (78%) are in

favor of requiring a vaccination

passport for travelers wishing

to enter their country. They are slightly less numerous in France: seven

out of ten are in favor (including 40%

'very favorable') , a similar proportion with the United

States and the Germans. A majority is in any case convinced of its

effectiveness in making travel and major events more secure in terms of

health (73% worldwide - France is a

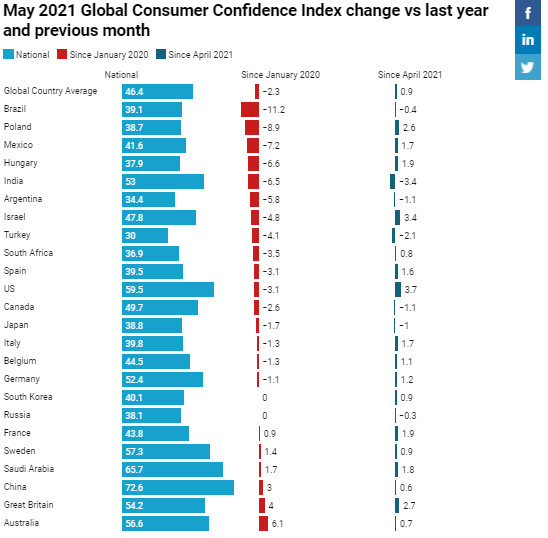

little below 65%) . (Ipsos France) May 17, 2021 Ipsos’s Global Consumer Confidence Index

Shows A Month-To-Month Gain Of Nine-Tenths Of A Point, Sitting Just 2.3

Points Below Its Pre-Pandemic Level Of January 2020 Eight countries have a National Index above

50: China (72.6), Saudi Arabia (65.7), the U.S. (59.5), Sweden (57.3),

Australia (56.6), Great Britain (54.2), India (53.0) and Germany (52.4). Only

two countries have a National Index below 35: Turkey (30.0) and Argentina

(34.4). Once again, the three countries in the survey showing the highest

levels of month-over-month growth (the U.S., Israel, and Great Britain) are

also those leading in vaccination rollout as per Oxford University data. (Ipsos Egypt) 19 May 2021 Source: https://www.ipsos.com/en-eg/global-consumer-confidence-eighth-month-row About Six-In-Ten American Adults (62%),

Including Majorities In Nearly Every Demographic Group, Support Increasing

The Minimum Wage To $15 An Hour Most Americans favor raising the federal

minimum wage, which has been $7.25 an hour since 2009. About six-in-ten

adults (62%), including majorities in nearly every demographic group, support

increasing the minimum wage to $15 an hour. Even among the 38% of Americans

who oppose a $15 minimum, most say they’d support a smaller increase,

according to an April Pew Research Center survey. (PEW) MAY 20, 2021 ASIA

689-691-43-01/Poll The

Population Of China Increased By 5.38 Percent To 1.41 Billion In 2020 Census Compared

With An Increase Of 5.84 Percent To 1.34 Billion In The 2010 Census

BEIJING--China’s population growth in the

decade to 2020 slumped to the least in official records dating back to the

1950s, fueling pressure on Beijing to ramp up incentives to couples to have

more children and avert an irreversible decline. With growth having slowed ever since a

one-child policy was introduced in the late 1970s, the 2020 results of the

country’s once-a-decade census, published on Tuesday, showed the population

of mainland China increased 5.38 percent to 1.41 billion. That compared with an increase of 5.84

percent to 1.34 billion in the 2010 census, and double-digit percentage rises

in all of China’s previous six official population surveys dating back to

1953. The number meant China narrowly missed a

target it set in 2016 to boost its population to about 1.42 billion by 2020.

In 2016, China replaced its one-child policy--initially imposed to halt a

population explosion at the time--with a two-child limit. In recent months, China’s state media has

been increasingly bleak on the outlook, saying the population may start to

shrink in the next few years. The United Nations predicts the number of

people living in mainland China will peak in 2030 before declining. But in late April, the Financial Times

newspaper said the population actually fell in 2020 from a year earlier,

citing unidentified people familiar with the matter. The 2020 number was actually slightly

higher than the 1.4005 billion in 2019 estimated in a smaller official survey

released in February last year. China has long worried about its population

growth as it seeks to bolster its economic rise and boost prosperity. One bright spot in the census data was an

unexpected increase in the proportion of young people--17.95 percent of the

population was 14 or younger in 2020, compared with 16.6 percent in 2010. FALLING BIRTH RATE From 2016 to 2019, the annual birth rate

mostly declined with the exception of 2016. China has yet to disclose the

birth rate for 2020. “A sharp decline in the number of births is

a sure thing, and all kinds of evidence support this claim,” said Huang

Wenzheng, a demography expert at the Center for China and Globalization, a

Beijing-based think-tank. “It doesn’t take published census data to

determine that China is facing a massive drop in births,” Huang said. Even if

China’s population didn’t decline in 2020, the expert said, “it will in 2021

or 2022, or very soon.” Urban couples, particularly those born

after 1990, value their independence and careers more than raising a family

despite parental pressure to have children. Surging living costs in China’s big cities,

a huge source of babies due to their large populations, have also deterred

couples from having children. According to a 2005 report by a state

think-tank, it cost 490,000 yuan ($74,838) for an ordinary family in China to

raise a kid. By 2020, local media reported that the cost had risen to as high

as 1.99 million yuan--four times the 2005 number. “Having a kid is a devastating blow to

career development for women at my age,” said Annie Zhang, a 26-year-old

insurance professional in Shanghai who got married in April last year. “Secondly, the cost of raising a kid is

outrageous (in Shanghai),” she said, in comments made before the 2020 census

was published. “You bid goodbye to freedom immediately after giving birth.” (Asahi Shimbun) May 11, 2021 Source: http://www.asahi.com/ajw/articles/14346249

689-691-43-02/Poll Japan’s

Population Of Children Under 15 Shrank By 190,000 From A Year Earlier

Children in

that age group account for 11.9 percent of the entire population, the lowest

level in the world, according to the ministry. The figure was 0.1 percentage

point down from the previous year. The

percentage has now dropped for 47 straight years. On the other

hand, people 65 or older account for 28.9 percent of the population, up 0.3

percentage point from the previous year. Although the

government has long vowed to battle the demographic change, the numbers show

that Japan’s declining birthrate and the graying of society have progressed further. The ministry

released the numbers to mark Children’s Day, a national holiday, on May 5. Among those

under 15 years old, 7.65 million are boys and 7.28 million are girls. Japan has

3.24 million children between 12 and 14, and 2.65 million who are 2 years old

or younger, the data showed. The younger

the age, the smaller the ratio of the overall population. In 1950,

children under 15 accounted for 35.4 percent of the population because of the

first baby boom. But the

ratio started declining. In 1997, people

65 or older made up 15.7 percent of the population, exceeding the 15.3

percent for those under 15. The ministry

compared Japan’s ratio of children with those in other countries with

populations of 40 million or more. Japan’s

percentage was the lowest, although the ministry said it was difficult to do

a strict comparison because the timing of the countries’ population surveys

was different. South

Korea’s ratio was the second lowest, at 12.2 percent as of July 1, 2020,

followed by Italy, at 13.3 percent as of July 1, 2018, and Germany, at 13.6

percent as of Jan. 1, 2019. (Asahi

Shimbun) May 5, 2021 Source: http://www.asahi.com/ajw/articles/14342995 689-691-43-03/Poll 44 Percent Of Japanese People Are In Favor

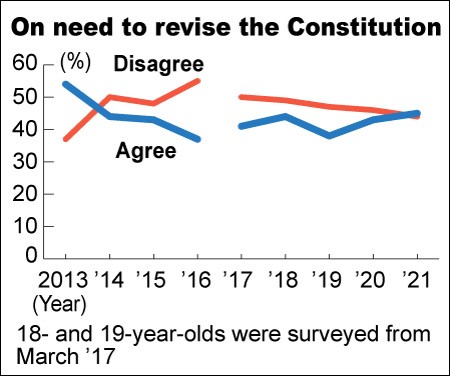

Of Revisions In Constitution

Voters were

nearly equally divided on whether the Constitution should be revised,

according to a survey by The Asahi Shimbun. The survey,

conducted ahead of Constitution Day on May 3, showed 45 percent backed

constitutional revisions, up from 43 percent in last year’s survey, while 44

percent said changes were unnecessary, down from 46 percent. The gap

between the two camps was the narrowest since the 2013 survey. The Asahi

Shimbun began the annual survey on how the public views proposals for

amending the Constitution, a key agenda pushed by Shinzo Abe, who was prime

minister from December 2012 to September 2020. The ruling Liberal Democratic

Party, led by Prime Minister Yoshihide Suga, is also seeking revisions. The

Constitution, drafted during the U.S.-led postwar occupation of Japan, has

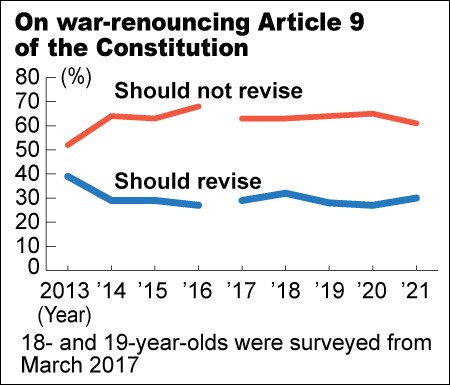

never been revised since it went into force in 1947. War-renouncing

Article 9 of the Constitution has long been a target of those who want

changes, including Abe. According to

the survey, 61 percent supported the article as it is, more than double the

30 percent who were in favor of revising it. In the 2020

survey, 65 percent were opposed to revising Article 9, while 27 percent

backed an amendment. Fifty-five

percent of voters in their 30s were in favor of constitutional revisions, the

largest group by age. Voters in their 70s or older were the least

enthusiastic about amendments, with only 35 percent backing revisions. In the

survey, respondents were asked to choose up to three reasons from among eight

provided. Among

pro-revision voters, the most common reason selected for their stance

was “a lack of sufficient provisions concerning defense,” at 58 percent,

followed by the Constitution is “getting old,” at 46 percent, and “it does

not reflect the national characteristic because it was imposed by the United

States,” at 35 percent. The three

most common answers chosen by respondents against revisions were: “the

Constitution brought peace to Japan,” at 71 percent; “there is no major

problem with the Constitution that needs to be revised,” at 41 percent; and

“the Constitution has taken root among the public,” at 40 percent. Asked if

they thought about the supreme law in their daily life, 68 percent of all respondents

chose “not at all” or “not so much,” while 30 percent chose “often” or

“sometimes,” the survey showed. It also

found that 61 percent of respondents in favor of revisions do not give much

thought or pay close attention to the Constitution, while 39 percent said

they do. The survey

also showed the text of Article 9 and asked the voters for their views. In the 2013

survey, 52 percent were opposed to revising Article 9, while 39 supported

changes. But in the

following surveys, including the latest one, more than 60 percent of

respondents rejected amendments to the article. Asked to

choose from among four answers to the question of whether momentum is

building for revisions, 19 percent chose “significantly” or “to some extent.” In

comparison, 76 percent picked the remaining two answers: “not at all” or “not

so much.” The ratio of

respondents who think momentum is gathering for constitutional revisions was

22 percent in 2019, 21 percent in 2020 and 19 percent in 2021. The

comparable figures for those who feel otherwise was 72 percent in 2019, 76

percent in 2020 and 76 percent in 2021. The LDP

is pushing to add an article to the Constitution that allows the Cabinet to

issue a directive under a state of emergency and temporarily restrict

people’s rights during contingencies, rather than waiting for the Diet to

enact a law. When voters

were asked about the emergency article for the first time in the 2019 survey,

and given three answers to choose from, 55 percent picked Japan should

“respond to emergencies without revising the Constitution.” The figure

in the latest survey was 54 percent. Thirty-three

percent chose “the Constitution should be revised to deal with emergencies,”

up from 28 percent in 2019. Six percent

in the latest survey selected “there is no need to revise the Constitution in

the first place” in relation to emergencies. The survey

was conducted between early March and mid-April by sending questionnaires to

3,000 eligible voters selected randomly across the nation. Valid answers were

received from 2,175 respondents, or 73 percent of the total. (Asahi

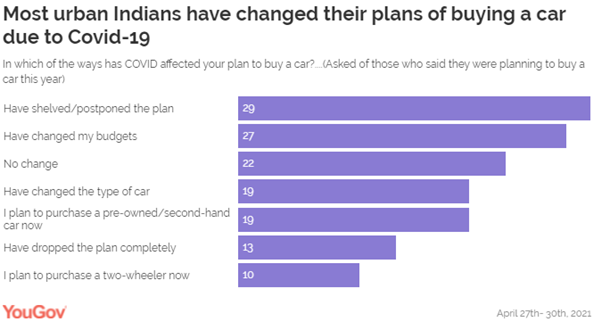

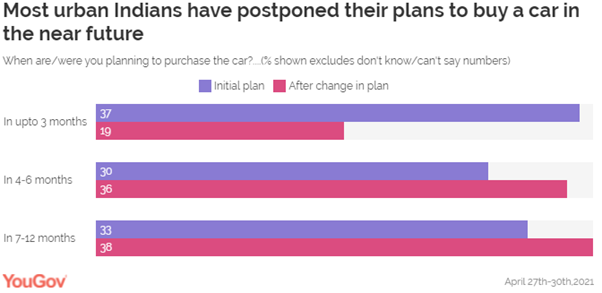

Shimbun) May 3, 2021 Source: http://www.asahi.com/ajw/articles/14342228 689-691-43-04/Poll Two In Five (19%) Indians Have Shown

Willingness To Buy Pre-Owned/Second-Hand Cars

The

coronavirus-induced economic slowdown impacted many industries and

businesses, including the automotive sector. India's second COVID

wave might derail the country’s economic recovery, adding to the worries

of carmakers. YouGov’s latest study looks into the impact of the pandemic on

the auto industry and reveals how car purchase plans have changed post the

second wave. As the

vaccination drive began in India and Covid was believed to be under control

early this year, three in ten (29%) urban Indians said they were planning to

buy a car, the data reveals. However, the second wave of the pandemic has

disrupted their planning and only one in five (22%) out of them are likely to

go ahead with their plan of buying a car, while some (13%) have completely

given up their plan or have switched the category of the vehicle; to a

two-wheeler now instead of a car (10). Others

experienced changes in the form of postponement of their plan to buy a car

(29%), change in their budget (27%) or change in the car type that they

planned to buy (19%). Interestingly, two in five (19%) respondents have shown

willingness to buy pre-owned/second-hand cars, which is a positive sign for

pre-owned car dealers.

Not only

plans, but the second wave of the pandemic has also even disrupted the

timelines to buy a car. Initially, almost two in five (37%) consumers were

planning to make a purchase within three months. However, with the second

wave hitting the country, this number has fallen to 19%. Most people

seem to have pushed their car buying decisions to a later period and are

looking to purchase a car somewhere between 4-6 or 7-12 months from now.

Likewise,

there have been changes in the car types that people want to purchase now,

with many turning towards more value-conscious options. Before the second

wave, hatchbacks were the most popular cars people wanted to buy, followed by

premium hatch cars. Preferences

have changed post the second wave of the pandemic and entry-level sedans

(Dzire, Amaze, Tigor, Altroz, etc) have seen the greatest shift in demand

between the two periods. From 13% who were planning to buy this model earlier

this year to 21% looking to buy this type of car now. On the other hand,

premium sedans have seen a decline (from 11% to 5%). Premium

hatchbacks and MUVs have also seen a growth in preference by 3% each.

Within the

SUV segment, the demand for compact (11%) mid (7% vs 6%) & premium SUVs

(6%) remained static. Although

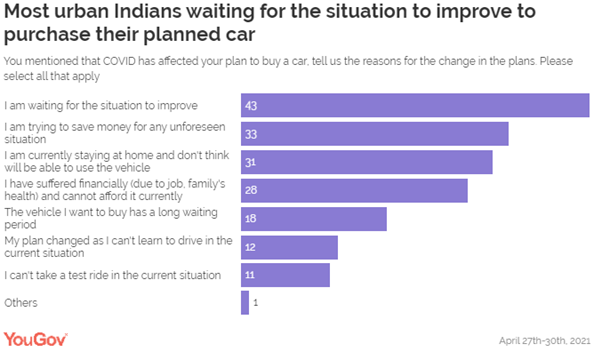

people admit to their plans getting affected by the pandemic, their reasons

to change their plans vary. A large majority of people are waiting for the

situation to improve (43%), hence, delaying their plans to buy a car by few

months. 28% have

suffered financially (job/health) to stick with their planned purchase while

a third are holding back as they want to save money for unforeseen situations Some (31%)

have voiced their inability to use a vehicle because of staying home for an

extended period as the reason to change their plan.

Commenting

on this, Sanjeev Jha of YouGov India,

said, “The pandemic has brought about marked changes in consumers’ car

buying plans in India. The outbreak has affected customers’ finances, driving

a conservative outlook in them and diverting them to more immediate needs. As

consumers wait for the situation to improve, auto manufacturers will have to

understand changing consumer preferences and devise innovative strategies to

offer cost-effective or better financing options to them. Regular

understanding of the changing plans of customers will help the automakers

efficiently plan their production and inventory management at the dealers’

end. The players in the pre-owned car market should reach out to the

prospective customers aggressively and offer the safety of a car at a

pocket-friendly price.” (YouGov

India) May 11, 2021 Source: https://in.yougov.com/en-hi/news/2021/05/11/most-urban-indians-wanting-buy-car-have-delayed-th/ 689-691-43-05/Poll New Prime Minister Of South Korea Kim

Bu-Gyeom "Conformity" 38% Vs "Nonconformity" 26%

As a result

of a survey of 1,000 adults on the 11th to 13th days before the appointment

of Prime Minister Kim, by Gallup Korea (±3.1%

points in the 95% confidence level of the sample error), 38% of respondents

said that Prime Minister Kim is suitable for the post of Prime Minister. More

than 26% of respondents said they didn't. 36% declined to comment. The response

that it was appropriate both before and after the personnel hearing was more

than the response that it was inappropriate. In the April 20-22 survey

immediately after the Prime Minister's nomination, 34% of'conformity' and 18%

of'nonconformity'. In this survey, after the personnel hearing, opinion

reservations decreased, and both conformity and nonconformity consensus

increased. It is also

peculiar that the opinion of'conformity' is predominant in the

characteristics of most respondents. The response that it is suitable

for all regions and age groups predominated. In particular, Gallup

pointed out that "public opinion in Gwangju, Jeolla, Daegu, and

Gyeongbuk is often opposed, but for candidate Kim Bu-gyeom, it is remarkable

that 40% of candidates are suitable for both regions." The

characteristics of the respondents with the predominance of nonconformity

were the support of the people (45%), ideological conservative tendencies

(37%), and negative evaluators for the performance of the presidential duties

(38%). At 29%, it was not a pattern that was largely focused on inadequacy. 76% of

"personnel hearings need to be publicly verified not only of abilities

but also of morality" Together

with Democratic Party representative Song Young-gil, speaking at the Supreme

Council Meeting held at the National Assembly in Yeouido, Seoul on the

14th. Representative Song insisted that the personnel hearing should be

a two-track verification of competence and morality, but the public opinion

surveyed that 71% opposed it. News 1 Responding

to the proposal that "a two-track personnel hearing should be conducted

to verify the candidate's ability to be public and morality to be privately

verified," 76% of the survey respondents indicated that "the

candidate's morality and policy ability should both be publicly

verified." 19% of respondents said, "Let's keep the morality

verification private and the policy capability verification public." The

two-track proposal for a personnel hearing was discussed with the opposition

parties at the end of last year, and President Moon Jae-in also expressed

similar opinions in the recent 4th anniversary special speech. However,

unlike the political world, this proposal is far from the sentiment of the

people. In the same

questionnaire,'morality' and'policy ability' were tied at 47%, respectively,

to the question of whether morality and policy ability should be prioritized

when verifying candidates at a personnel hearing. However,

even if only those who answered that competency verification should be

prioritized over morality in this question, 69% of the respondents said that

"morality should also be publicly verified" for the personnel

hearing method was found to be far more dominant. (Gallup

Korea) 2021.05.14 Source: https://www.hankookilbo.com/News/Read/A2021051412010000940 689-691-43-06/Poll Public Verification Of Personnel Hearings, 'Morality'

76 Percent Vs 'Policy Ability Only' 19 Percent

When Gallup

Korea asked 1,000 men and women over the age of 18 on the 11th to 13th of the

year, 76% of respondents chose'open verification of both morality and policy

capabilities'. Only 19% of

respondents chose'private verification for morality and public verification

for policy capabilities'.5% reserved their opinion. In the same

survey in November of last year, 71% of'open verification of all policies'

and 23% of'public verification of policy capabilities only' yielded similar

results. When asked

whether morality and policy ability should be prioritized when verifying

candidates at the personnel hearing,'morality' and'policy ability' were tied

at 47% each. In

particular, those in their 20s and 30s who gave priority to'policy ability'

were 65% and 62%, respectively, higher than those of other age groups. New Prime Minister Kim Bu-gyeom goes to work (Seoul = Yonhap

News) Reporter Seung-Doo Kim = New Prime Minister Kim Bu-gyeom is on the

morning of the 14th to work at the Sejong-ro Government Complex in

Seoul.President Moon Jae-in approved the appointment of Prime Minister Kim at

7 am on the same day.2021.5.14 kimsdoo@yna.co.kr When asked

about the suitability for the appointment of the new Prime Minister Kim

Bu-gyeom, 38% of the voters answered that it is'suitable' and 26% answered

that it is'not suitable'.36% declined to comment. The margin

of error for this survey is ±3.1%

with a 95% confidence level. (Gallup

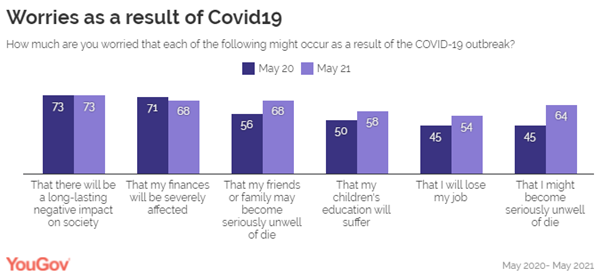

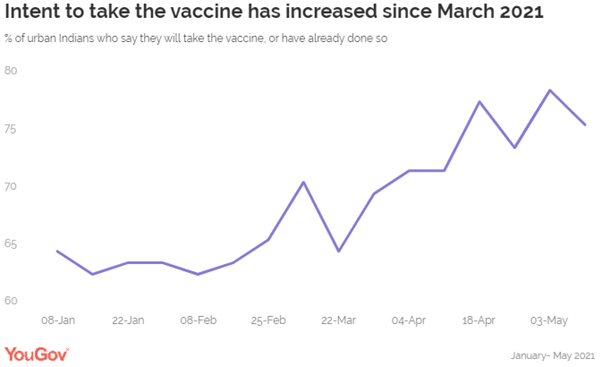

Korea) 2021-05-14 Source: https://www.yna.co.kr/view/AKR20210514062000001?input=1195m 689-691-43-07/Poll Nearly Two-Thirds Of Urban Indians (64%)

Are Worried They May Become Seriously Unwell Or Die Due To COVID

Nearly

two-thirds of urban Indians (64%) are worried they may become seriously

unwell or die due to Covid, YouGov’s latest data reveals. YouGov’s

Covid19 Public Monitor has been tracking the public sentiment around the

virus since last year when the pandemic first broke out in the world.

In May 2020, at the outset of the pandemic, only 45% of urban Indians were

worried about their personal health getting affected due to covid. A year

later as India faces a much deadlier wave of the virus with limited

healthcare facilities; this number has gone up to 64%.

With more

people contracting the virus this year, concerns over personal health have

intensified over the year; with a 19-percentage point increase between the

two periods (from 45% in May’20 to 68% in May 21). Similarly, fear about

losing a loved one has also increased by 12- percentage points during this

time. Given the current situation, it seems there is a greater focus on

worries surrounding one’s family and personal health than concerns over one’s

finances or job. This

increase in worry corresponds with the public’s failing confidence in the

government and health system.

Desperate to

battle the crisis, citizens have turned towards vaccines. Data from YouGov’s

Public Monitor shows 67% felt comfortable taking the vaccine in January when

it was first rolled out. After the second wave hit the country in February,

there has been an increase in the number of people who either have already or

are willing to take the vaccine- at 76% as of May 2021.

(YouGov

India) Source: https://in.yougov.com/en-hi/news/2021/05/21/concerns-about-personal-health-soar-india-battles-/ 689-691-43-08/Poll 3 In 10 Pakistanis Concerned About

Digitally Sharing Their Personal Information

According to

a Gallup Pakistan Survey in Pakistan (and similar surveys done by WIN

International across the world), 30% Pakistanis agreed that they are concerned

about sharing their personal information. When asked about the necessity of

sharing personal information, 24% Pakistanis think that sharing personal

information is necessary nowadays. 43% Pakistanis (27% globally) are not fine

with the privacy practices of most data collectors asking for their personal

information. As far as awareness about digital rights and personal data

privacy is concerned, 46% Pakistanis are not aware of what happens with their

personal information after they share it with a data collector. WIN

International, the world’s leading association in market research and

polling, has published the Annual WIN World Survey (WWS – 2020) exploring the

views and beliefs of 26,433 individuals among citizens from 34 countries

across the globe about the privacy of digital information. The survey

for Pakistan was conducted by Gallup Pakistan during 5th to

15th November 2020. The sample size was 1103 respondents and

CATI methodology was used. (Gallup

Pakistan) May 18, 2021 Source: https://gallup.com.pk/post/31737 MENA

689-691-43-09/Poll MENA

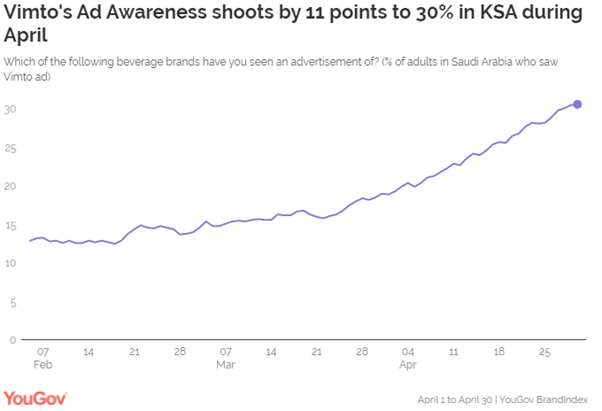

Advertiser Of The Month (April): Vimto

Vimto is a drink that has been dear

to many Arab hearts for years, especially during Ramadan. It is the

choice for many who prefer Vimto for breaking their fasts

at Iftar. Vimto is also known for its innovations in flavours, including

dates-flavoured drink, and ads - sharing videos of

celebrating Ramadan virtually with family during the

lockdown. This Ramadan, Vimto came up with a campaign

that helped the brand win YouGov's Advertiser of the Month. Data from

YouGov BrandIndex shows the percentage of adults in KSA who saw

Vimto’s ad during the month of April shot up by 11 points from 19%

(April 1) to 30% (April 30).

The campaign attracted participation from

across KSA which helped the Ad Awareness score of the

brand to shoot up from 19% on April 1 to 30% on

April 29. As Vimto's marketing brains would

wish, the campaign appeared to also have a positive

impact on the brand’s Impression and Recommendation scores

too. At the start of the month, 16% of adults in KSA indicated they had

a positive impression of Vimto – that figure shot up to 24% by April

30. Vimto’s recommendation score, which tracks the percentage of people

who would recommend a brand to others, rose to 22% (April 30) from 14% (April 1). (YouGov MENA) Source: https://mena.yougov.com/en/news/2021/05/10/mena-advertiser-month-april-vimto/ 689-691-43-10/Poll Global

Village Has Emerged As The Top Mover This Year, With A Change In Score Of

+14.2 Compared To Ramadan 2020 In UAE

Ramadan 2020, the first Ramadan in the

midst of the ongoing global pandemic saw reduced marketing activity from many

brands as budgets were slashed. By comparing Ad Awareness scores for the

Ramadan period this year vs the previous year, YouGov have identified some

interesting trends in terms of whose communications are reaching more of the

adult population in the country. The top 10 list has been compiled using the

Ad Awareness score- which measures whether a respondent has seen any

advertising for the brand in the past 2 weeks. YouGov BrandIndex data shows Global Village

has emerged as the top mover this year, with a change in score of +14.2

compared to Ramadan 2020. Despite ongoing Covid19 operating

procedures in place, Global Village decided to extend its open season into

Ramadan this year. This extension, coupled with it being the silver jubilee

(25th year) season, saw it promote its 25th world

record-breaking event, which clearly reached a wide audience in Ramadan. The Ramadan campaign had a positive impact

on the brand’s Ad Awareness, raising its score from 20.6 during Ramadan 2020

to 34.8 during Ramadan 2021. Notably, the list of top movers is

dominated by destinations and leisure & entertainment venues all vying to

attract customers back to their properties after a challenging year. Given

Ramadan typically sees families spending more time together, it’s not

surprising that these family destinations have been pushing their message to

visit out strongly during this period. Additionally, online retailer, Noon.com was the second-best improver, with a

change in score of +11.1. Aligning with the spirit of Ramadan, the e-retail

giant extended daily deals and discounts, giving up to 75% off on groceries

and household items, especially useful for households hard hit by the

pandemic. It seems UAE residents have responded to

the communications as the brand noted a significant improvement in its Ad

Awareness this festive season vs the previous year. Talabat.com is the third-best improver, with an

Ad Awareness bump of +7.9. The leading food-delivery platform partnered with

the Dubai Culture and Arts Authority (Dubai Culture) to launch ‘Ramadan

Heroes’ campaign with the aim of providing iftar meals to those in need. The

virtual charity endeavor struck a chord with people and helped the brand

enhance its Ad Awareness this Ramadan. Similarly, Starbucks joined the festivities

by introducing Ramadan cups as a seasonal edition. The holiday cups seem to

have attracted customers’ attention, raising the brand’s Ad Awareness by +6.7

compared to last Ramadan. Swedish retail giant IKEA and ADNOC also

made the top ten list- at sixth (6.6) and seventh (6.4), respectively. (YouGov MENA) Source: https://mena.yougov.com/en/news/2021/05/20/yougov-brandindex-data-reveal-top-ten-year-year-mo/ AFRICA

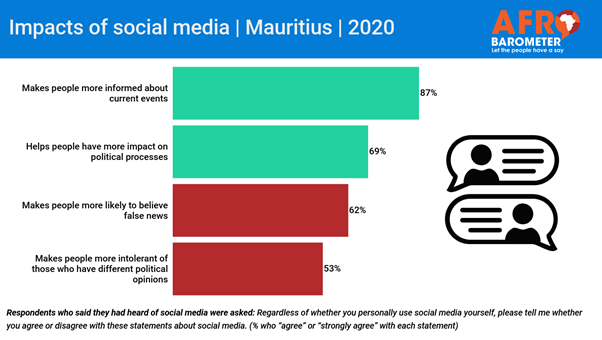

689-691-43-11/Poll 87 Percent

Mauritians Think Social Media Makes People More Informed About Current

Affairs

A majority of Mauritians want unrestricted

access to the Internet and social media, Afrobarometer’s recent national

survey finds. While a small share of citizens believe

that the use of social media such as Facebook, Twitter, and WhatsApp makes

people more susceptible to fake news and intolerance, a large majority say

social media informs them about current events and helps them have an impact

on political processes. The share of Mauritians who use social

media every day has more than doubled over the past six year, from 32% in

2014 to 69% in 2020. Overall, citizens believe the effect of social media on

society is positive. (Afrobarometer) 5 May 2021 689-691-43-12/Poll 63 Percent