BUSINESS &

POLITICS IN THE MUSLIM WORLD

Global Opinion

Report No. 366

Week:

February 01 – 07, 2015

Presentation:

February 11, 2015

M. Zubair Khan

INTRODUCTORY NOTE 02

SUMMARY OF POLLS 02

WEST

ASIA

·

Public

opinion divided over the possibility of war between India and Pakistan 06

SOUTHEAST ASIA

·

Philippines: 85% says gays and

lesbians should be protected against discrimination 08

·

Philippines: Adult joblessness at

27.0%; 9% lost their jobs involuntarily, 14% resigned 11

SUB-SAHARAN AFRICA

·

Tanzanians see increased

corruption, ineffective fight against it 14

EAST EUROPE

·

Paris Terrorist Attacks: Russian

Assessments 18

·

Ruble Exchange Rate: Fears And

Forecasts 20

·

Protest Actions: Manifestations Of

Democracy Or Crisis? 23

WEST EUROPE

·

Economist/Ipsos MORI January 2015

Issues Index 25

·

Captains of Industry support

Britain being in the EU 27

·

Public perceptions of climate

change in Britain following the winter 2013/14 flooding 31

·

Overwhelming public support for the

‘Gordon’s Fightback’ Campaign 32

·

UK: Voters: time to slim down the royal

family 33

·

Scotland: SNP lead at 21 34

NORTH AMERICA

·

Obama Approval Ratings Still

Historically Polarized 37

·

Majorities in Five States Approved

of Obama in 2014 40

·

Eight-Point Increase in Monthly

Economic Confidence Index 46

·

Gallup Student Poll: Job Confidence

Lower in Higher Grades 49

·

For Banks, Baby Boomers Mean

Lucrative Business 51

·

After Holidays, January U.S.

Consumer Spending Falls to $81 53

·

U.S. Flu Reports Decline in January 56

·

U.S. Small-Business Owners'

Optimism Highest Since 2008 59

·

U.S. Payroll to Population Rate

44.1% in January 61

·

U.S. Job Creation Lingers Near

Seven-Year High 66

·

Investigative Journalists and

Digital Security 69

LATIN AMERICA

·

65% of Brazilians have a positive

view of the UN 73

·

19% of Brazilians do not know better time

to buy tickets or travel package 74

MULTI-COUNTRY

SURVEYS

·

Widespread concerns about extremism

in Muslim nations, and little support for it 76

·

Consumer Mood Brightened Again

Towards End Of Year 78

CYBER WORLD

·

More Australians buying eBooks 80

ANALYSIS TANK

·

America’s ‘middle’ holds its ground

after the Great Recession 82

INTRODUCTORY

NOTE

This week report consists of twenty nine surveys.

One of these is a multi-country survey while the rest of twenty eight are

national surveys from countries across the world.

366-30

Commentary:

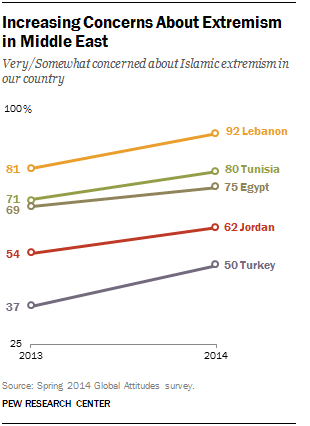

Widespread Concerns About Extremism In

Muslim Nations, And Little Support For It

February 05, 2015

Widespread Concerns About Extremism In

Muslim Nations, And Little Support For It

The horrific murder of Jordanian

pilot Moaz al-Kasasbeh has generated shock and outrage around the globe. And

if recent history is a guide, this brutal act will only deepen opposition to

ISIS, and to violent extremism more generally, in Jordan and other

predominantly Muslim nations.

The horrific murder of Jordanian

pilot Moaz al-Kasasbeh has generated shock and outrage around the globe. And

if recent history is a guide, this brutal act will only deepen opposition to

ISIS, and to violent extremism more generally, in Jordan and other

predominantly Muslim nations.

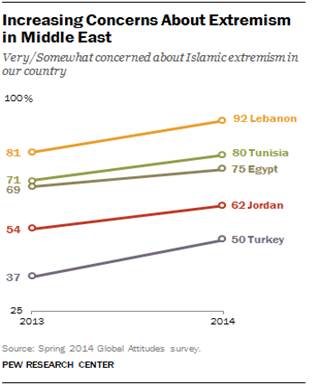

At the Pew Research Center, we’ve been asking questions related to extremism on our international surveys for over a decade, and what we’ve generally found among Muslim publics is that support for extremism is low, while concerns about it are high.

Even before ISIS’s battlefield victories and humanitarian atrocities began capturing international headlines last summer, we found growing worries about extremism in the Middle East. For instance, 62% of Jordanians said they were concerned about Islamic extremism in their country in our spring 2014 poll, up from 54% a year earlier. There were also increases in Lebanon, Tunisia, Egypt and Turkey.

The survey also found mostly negative views toward al Qaeda and other extremist groups in these and many other predominantly Muslim countries. The most positive rating for al Qaeda was in the Palestinian territories, where 25% had a favorable view of the terrorist organization.

One pattern we’ve seen in different parts of the world is that the more people are exposed to terrorist violence, the more they reject it. Jordan is a good example. Early in the last decade, Jordanians expressed relatively high levels of support for suicide bombing and confidence in Osama bin Laden, but this changed after the November 2005 suicide attacks on three hotels in Amman, Jordan’s capital. The bombings, which killed dozens and wounded more than 100, were orchestrated by an al Qaeda affiliate, led at the time by the Jordanian Abu Musab al-Zarqawi.

A few months later, a Pew Research survey found the percentage of Jordanian Muslims saying suicide attacks can often or sometimes be justified had fallen from 57% to 29%. Today, it stands at 15%. Similarly, confidence in bin Laden plummeted from 61% to 24% after the bombings, and by the time of his death just 13% of Jordanians had confidence in the terrorist leader.

Pakistan is another example. The terrible violence Pakistanis have experienced at the hands of the Taliban and other groups over the past decade has led many to reject violent extremism. In 2004, 41% of Pakistani Muslims said suicide bombing can often or sometimes be justified; by 2014 only 3% held this view.

In 2009, when the Taliban occupied Pakistan’s Swat Valley and threatened to drive even closer to the nation’s capital, Islamabad, opposition to the extremist group jumped dramatically. In 2008, just 33% of Pakistanis had an unfavorable view of the Taliban, but this rose to 70% in the 2009 survey. In Pakistan and elsewhere, once terrorist violence and extremist rule has become a reality, people have rejected it.

SUMMARY OF POLLS

WEST

ASIA

Public opinion divided over the possibility of war

between India and Pakistan

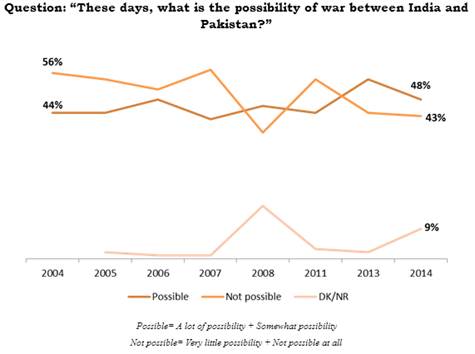

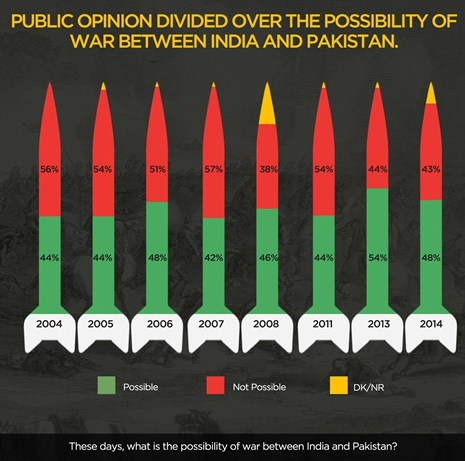

According to a Gilani Research Foundation Survey carried out by Gallup Pakistan, 48% Pakistanis believe there is possibility of war between India and Pakistan; 43% believe there is very little possibility. (Gallup Pakistan)

February 3, 2015

SOUTHEAST ASIA

Philippines:

85% says gays and lesbians should be protected against discrimination

Eighty-five

percent of adult Filipinos believe that gays and lesbians have the right to be

protected against any form of discrimination, according to the Social Weather

Survey of June 28-30, 2013. (SWS)

February 06, 2015

Philippines:

Adult joblessness at 27.0%; 9% lost their jobs involuntarily, 14% resigned

The Fourth Quarter

2014 Social Weather Survey, fielded over November 27-December 1, 2014, found

adult joblessness at 27.0% (est. 12.4 million adults). (SWS)

February 04, 2015

SUB-SAHARAN AFRICA

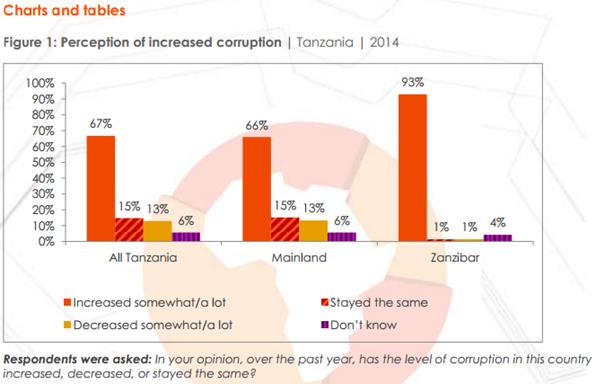

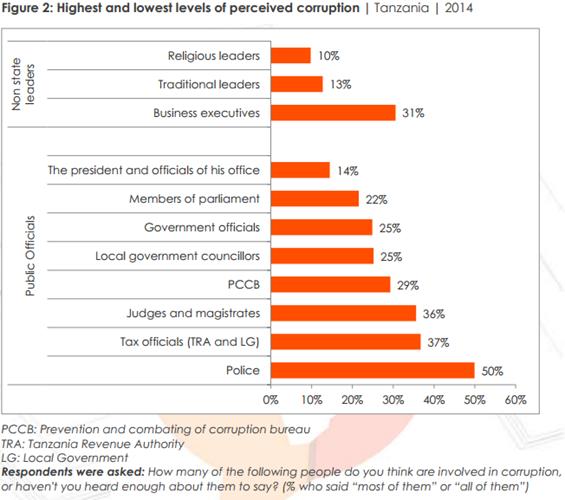

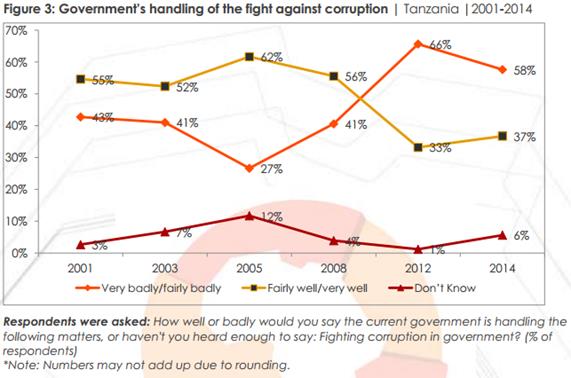

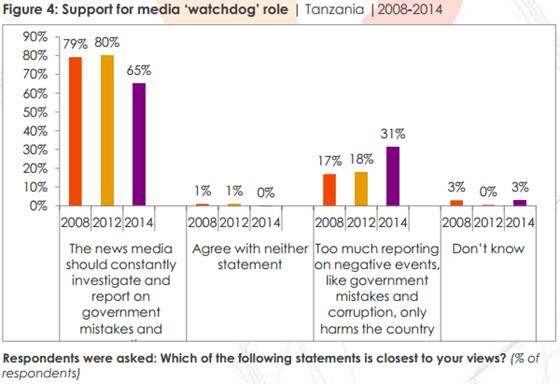

Tanzanians

see increased corruption, ineffective fight against it

A majority of

Tanzanians say that the level of corruption in the country has increased over

the past year, according to the latest Afrobarometer survey. The police, tax

officials, and judges and magistrates perceived as the most corrupt. Citizens’

rating of the government’s handling of the fight against corruption has

improved slightly since 2012 but still remains mostly negative. (Afrobarometer)

February 06, 2015

EAST EUROPE

Paris

Terrorist Attacks: Russian Assessments

Russians believe

that Paris

shootings were caused by ineffective migration policies of the French

government and improper behavior of the Charlie Hebdo journalists. (VCIOM)

January 26, 2015

Ruble

Exchange Rate: Fears And Forecasts

Most of Russians are afraid of the

further drop in the ruble`s value; at the same time, one-third of Russians

believe that in the coming months the ruble exchange rate will not change much.

(VCIOM)

January 20, 2015

Protest

Actions: Manifestations Of Democracy Or Crisis?

The level of protest potential of

Russians is still low. Rallies and demonstrations are mainly perceived as

crisis symptoms rather than instruments to solve problems. (VCIOM)

January 23, 2015

WEST EUROPE

Economist/Ipsos

MORI January 2015 Issues Index

The first

Economist/Ipsos MORI Issues Index of 2015 shows that concern about the NHS has

increased by 12 percentage points since December of last year, and it is now

seen as the most important issue facing Britain – mentioned by almost half

(45%) of the public. (Ipsos MORI)

February 06, 2015

Captains

of Industry support Britain being in the EU

Could British business leaders be

the biggest block to UKIP’s campaign for parliament? The new Ipsos MORI

Captains of Industry survey shows that although 45% of Captains want to return

to being part of an economic community, without political links, just 1% would

be happy to leave it all together. Just under half (45%) want to continue our

relationship with the EU as it stands. (Ipsos MORI)

February 04, 2015

Public

perceptions of climate change in Britain following the winter 2013/14 flooding

A recent Ipsos

MORI survey for Cardiff University updates trend data on public attitudes to

climate change as well as providing new data on how the British public

responded to the flooding last winter. The study tested whether the

public, but particularly those affected by flooding, link the winter 2014

flooding to climate change. (Ipsos MORI)

February 02, 2015

Overwhelming

public support for the ‘Gordon’s Fightback’ Campaign

An Ipsos MORI

Scotland poll for the Gordon’s Fightback campaign shows overwhelming support

for their key objectives. Almost all of those polled (97%) would support the UK

government introducing a new system of fast tracking benefits for those with a

terminal illness, such as motor neurone disease. Support for such a measure is

overwhelming across all groups in the population. (Ipsos MORI)

February 02, 2015

UK: Voters:

time to slim down the royal family

Most British

people say that apart from the core royal family of the Queen, Charles and his

descendants, the rest should no longer receive money from the taxpayer and

royal estates. (YouGov)

February 2015

Scotland:

SNP lead at 21

The Scottish National

Party has retained its lead in Scotland – and on the question of Scottish

independence, Yes leads No by 4 points. (Ipsos Mori)

February 03, 2015

NORTH AMERICA

Obama

Approval Ratings Still Historically Polarized

Throughout

President Barack Obama's sixth full year in office, an average of 79% of

Democrats, compared with 9% of Republicans, approved of the job he was doing.

That 70-percentage-point party gap in approval ratings ties for the

fifth-most-polarized year for a president in Gallup records dating back to

1953. (Gallup USA)

February 06, 2015

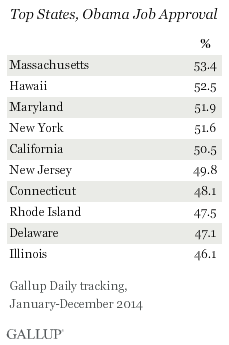

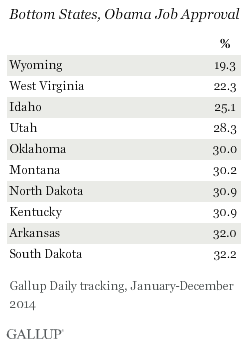

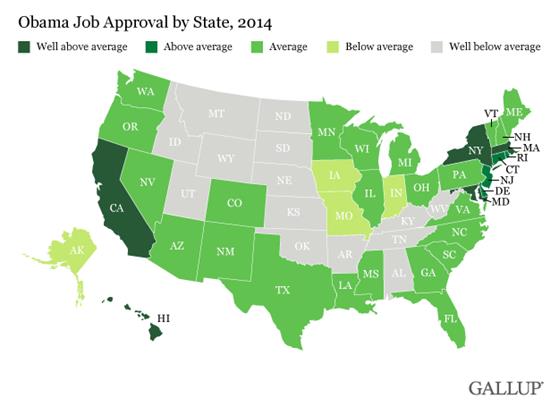

Majorities

in Five States Approved of Obama in 2014

Residents of five

states gave President Barack Obama 50% or better job approval ratings in 2014,

with Massachusetts and Hawaii leading the list at roughly 53%. Wyoming

residents were the least approving, at 19.3%. (Gallup USA)

February 02, 2015

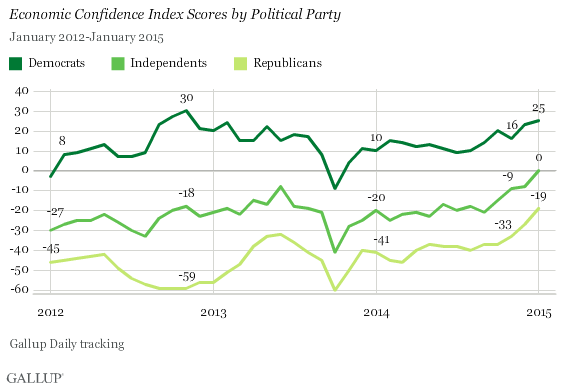

Eight-Point

Increase in Monthly Economic Confidence Index

Gallup's U.S.

Economic Confidence Index, which has been positive for each of the past six weeks, finished January

with an average score of +3 -- the first time a monthly average has been in

positive territory since the recession. The monthly index score is up eight

points from December -- the highest

month-to-month increase in more than a year. (Gallup USA)

February 03, 2015

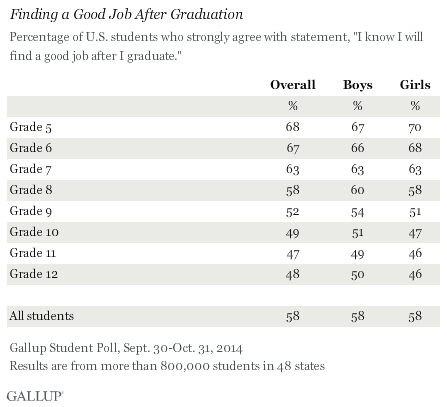

Gallup

Student Poll: Job Confidence Lower in Higher Grades

Gallup Student

Poll students in elementary and middle school are much more optimistic about

their ability to find a good job than are students in high school. The

percentage of students in grades 5 through 12 who strongly agree with the

statement, "I know I will find a good job after I graduate" declines

from 68% in grade 5 to 49% in grade 10, and remains at about that level through

grade 12. (Gallup USA)

February 03, 2015

For

Banks, Baby Boomers Mean Lucrative Business

For banks, baby

boomers stand out among generations as highly attractive and lucrative

customers. (Gallup USA)

February 02, 2015

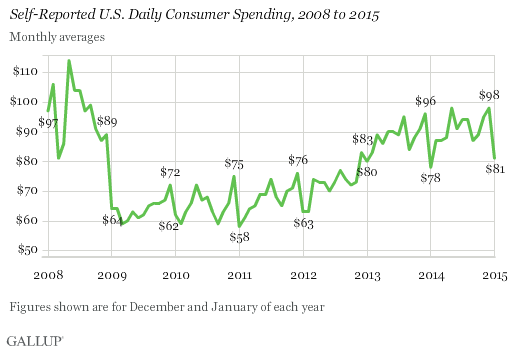

After

Holidays, January U.S. Consumer Spending Falls to $81

U.S. consumers'

daily self-reports of spending fell to an average of $81 in January, down from

$98 in December. Spending usually drops after the holiday season, falling an

average of $15 each January since 2008. Despite this year's $17 drop, $81 is

one of the highest self-reported averages in any January since 2008. (Gallup

USA)

February 02, 2015

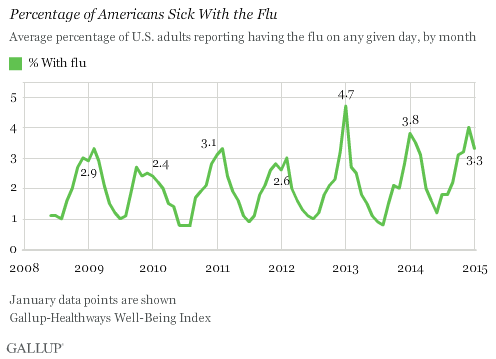

U.S.

Flu Reports Decline in January

The 2014-2015 U.S.

flu season may have peaked early. In January 2015, an average of 3.3% of

Americans reported they "were sick with the flu yesterday." This is

down from 4.0% in December, the highest rate

in any December since Gallup began tracking the flu daily in 2008. Average flu

reports in January are also lower than in January 2013 and January 2014.

(Gallup USA)

February 05, 2015

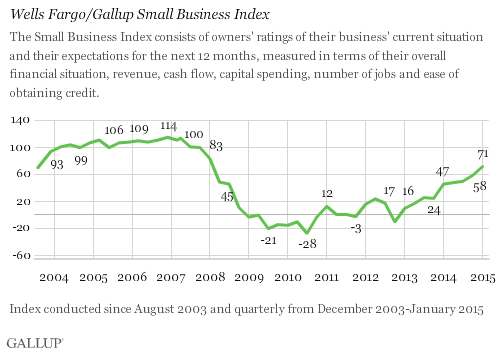

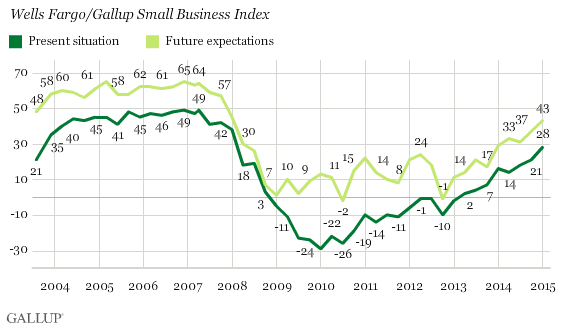

U.S.

Small-Business Owners' Optimism Highest Since 2008

U.S.

small-business owners are the most optimistic they have been in seven years,

according to the latest Wells Fargo/Gallup Small Business

Index.

The index, at +71, has increased significantly for two consecutive quarters,

and reflects optimism in small-business owners' views of both their current

situation and their expectations for the future. (Gallup USA)

February 05, 2015

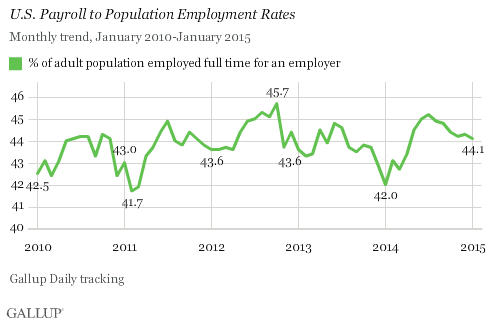

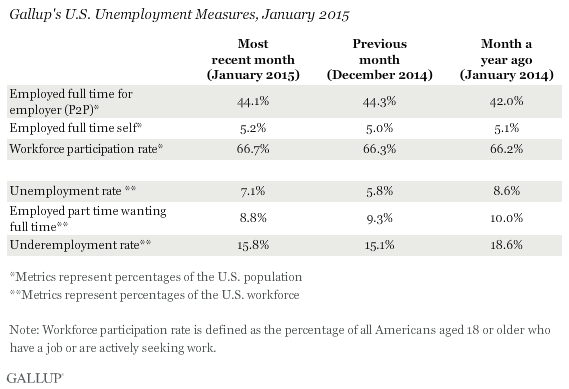

U.S.

Payroll to Population Rate 44.1% in January

The U.S. Payroll

to Population employment rate (P2P), as measured by Gallup, was 44.1% in

January. This is statistically similar to the 44.3% measured in December, but

it is the highest measurement of P2P for any January since Gallup began

tracking the metric in 2010. January is typically one of the lowest months for

P2P in any year. (Gallup USA)

February 05, 2015

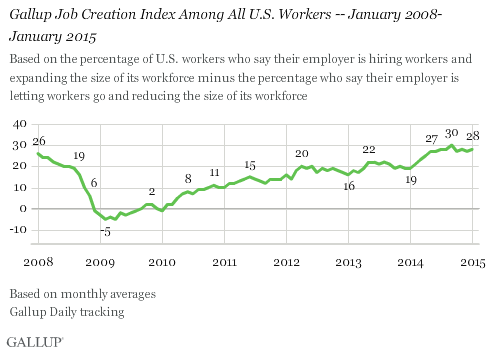

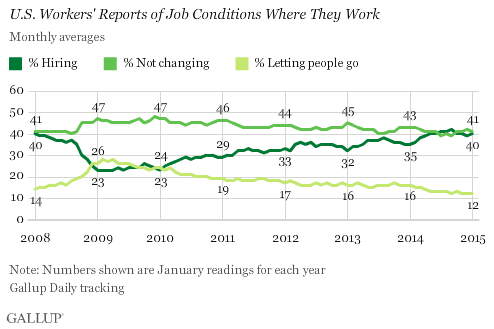

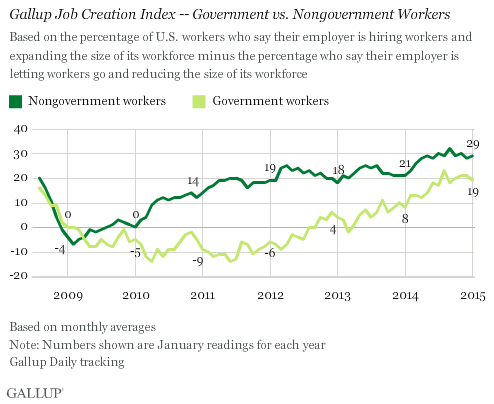

U.S.

Job Creation Lingers Near Seven-Year High

The hiring climate

at the start of 2015 is similar to where it stood in the second half of 2014,

with Gallup's U.S. Job Creation Index coming in at +28 for the month of

January. This is nearly identical to the +27 found in December, and just below

the seven-year high of +30 reached in September. (Gallup USA)

February 04, 2015

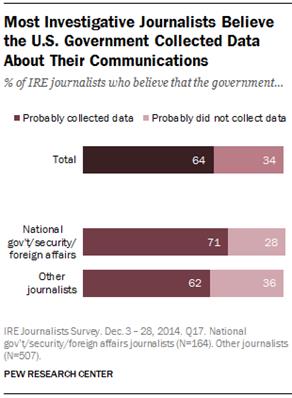

Investigative

Journalists and Digital Security

About two-thirds

of investigative journalists surveyed (64%) believe that the U.S. government

has probably collected data about their phone calls, emails or online

communications, and eight-in-ten believe that being a journalist increases the

likelihood that their data will be collected. (Pew Research Center)

February 05, 2015

LATIN AMERICA

65%

of Brazilians have a positive view of the UN

A survey conducted

by IBOPE Inteligência in Brazil to measure what Brazil´s population knows about

the United Nations (UN) shows that 74% of Brazilians know or have heard of the

UN, and 65% consider the work of the international organization as positive

(22%) or very positive (43%). (Ibope)

February 02, 2015

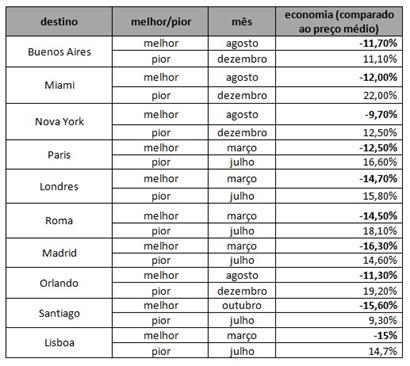

19% of

Brazilians do not know better time to buy tickets or travel package

To travel economically it is

necessary to plan. The trip planning is essential to ensure the best and

know the best dates for the holidays. According to a survey * of CONECTAí

to Skyscanner, 19% of Brazilians still do not know the best time to purchase

tickets or travel package and 14% still have doubts became the most economical

choice.

(Ibope)

February 06, 2015

MULTI-COUNTRY

SURVEYS

Widespread

concerns about extremism in Muslim nations, and little support for it

The horrific murder of Jordanian pilot Moaz

al-Kasasbeh

has generated shock and outrage around the globe. And if recent history is a

guide, this brutal act will only deepen opposition to ISIS, and to violent

extremism more generally, in Jordan and other predominantly Muslim nations.

(Pew Research Center)

February 05, 2015

Consumer

Mood Brightened Again Towards End Of Year

The mood of

consumers throughout Europe improved again over the fourth quarter of the year.

The indicators for economic and income expectations, as well as willingness to

buy, rose towards the end of the year in almost all countries of the European

Union (EU). The consumer climate for the EU 28 also improved by 1.3 points in

the final quarter, closing the year at 5.5 points. These are the findings of

the GfK Consumer Climate Europe study in 14 European countries. (GFK)

February 04, 2015

CYBER WORLD

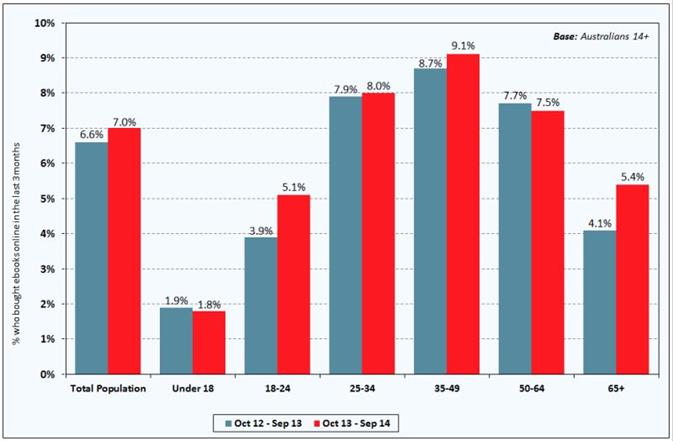

More

Australians buying eBooks

Amid recent reports in the UK that the eBook may have had its day, Roy

Morgan Research’s latest figures reveal that this might not be the case in

Australia. In fact, over the past two years, online sales of eBooks have

increased across most age groups — along with the proportion of Aussies reading

novels or non-fiction titles in an average three-month period. (Roy Morgan)

February 02, 2015

ANALYSIS TANK

America’s

‘middle’ holds its ground after the Great Recession

WEST ASIA

366-43-1. Public

opinion divided over the possibility of war between India and Pakistan

GILANI RESEARCH FOUNDATION (GRF POLL)

February 3, 2015

According to a Gilani Research Foundation Survey carried out by Gallup Pakistan, 48% Pakistanis believe there is possibility of war between India and Pakistan; 43% believe there is very little possibility.

A nationally representative sample of adult men and women, from across the four provinces was asked, “These days, what is the possibility of war between India and Pakistan?” In response to this question, 15% respondents said there is a lot of possibility, 33% said there is somewhat possibility, while 43% believe there is very little possibility and 9% did not respond.

This question was also asked previously over the last decade. In 2004, 6% respondents said there was a lot of possibility of war between India and Pakistan, while 38% said there was somewhat possibility and 56% said there was no possibility at all. There were minor fluctuations in public opinion between 2004 and 2007. In 2008 however, there was a sharp decline in the percentage of respondents who thought war was not possible (57% to 38%), corresponding with an increase in individuals refusing to respond to the question (1% to 15%). After 2008, the percentage of those who think war was not possible rose once again (54% in 2011) but sharply declined to 44% in 2013. This was complimented by an increase in those who think war is possible between 2011 and 2013 (44% to 54%) before this percentage also declined slightly to 48% in 2014.

The study was released by Gilani Research Foundation and

carried out by Gallup Pakistan, the Pakistani affiliate of Gallup

International. The recent survey was carried out among a sample of 2442 men and

women in rural and urban areas of all four provinces of the country, during

December 29, 2014 – January 05, 2015. Error margin is estimated to be

approximately ± 2-3 per cent at 95% confidence level.

SOUTHEAST ASIA

366-43-2.

Philippines: 85% says gays and lesbians should be protected against

discrimination

SWS Special Report:

February 06, 2015

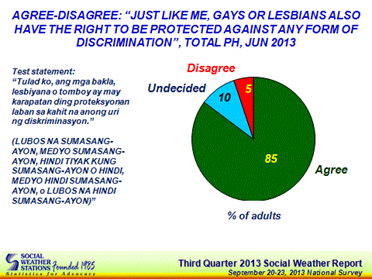

Eighty-five percent of adult Filipinos believe that gays and lesbians have the right to be protected against any form of discrimination, according to the Social Weather Survey of June 28-30, 2013.

To the statement, “Just like me, gays and lesbians also have the right to be protected against any form of discrimination [Tulad ko, ang mga bakla, lesbiyana o tomboy ay may karapatan ding proteksyonan laban sa kahit na anong uri ng diskriminasyon]”, 85% agree, 5% disagree, and 10% are undecided [Chart 1].

Out of the six specific statements about gays and lesbians tested in June and September 2013, results showed sympathetic attitude on 5 issues, and unsympathetic on one issue.

The strongest sympathetic attitude was (a) the importance of non-discrimination, followed by (b) the belief that gays and lesbians are just as trustworthy as any other Filipino, (c) the big contribution of gays and lesbians to societal progress, (d) the belief that being gay or lesbian is NOT a form of mental illness, and (e) the belief that being gay or lesbian is NOT contagious.

The only statement where opinions are more on the unsympathetic side was (f) the belief that Acquired Immunodeficiency Syndrome, or AIDS, can be considered as a sickness of gays and lesbians.

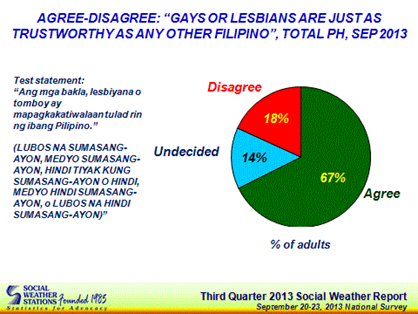

Gays and lesbians are trustworthy? 67% agree, 18% disagree

In the September 20-23, 2013 Social Weather Survey, 67% agree and 18% disagree that “Gays or lesbians are just as trustworthy as any other Filipino [Ang mga bakla, lesbiyana o tomboy ay mapagkakatiwalaan tulad rin ng ibang Pilipino]”. The remaining 14% are undecided about this matter [Chart 2].

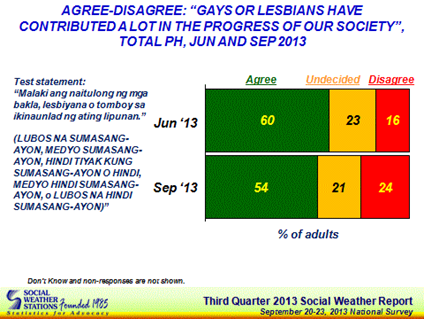

Gays and lesbians have contributed a lot to societal progress? 54% agree, 24% disagree

The September 2013 survey found that 54% agree with the statement, “Gays or lesbians have contributed a lot in the progress of our society [Malaki ang naitulong ng mga bakla, lesbiyana o tomboy sa ikinaunlad ng ating lipunan]”, slightly less than the 60% in June 2013 [Chart 3].

Compared to June 2013, the proportion of those who disagree rose from 16% to 24%, while those who areundecided hardly moved from 23% to 21%.

Is being gay or lesbian a form of mental illness? 54% disagree, 25% agree

In June 2013, 54% disagree and 25% agree that “Being gay or lesbian is a form of mental illness [Ang pagiging bakla, lesbiyana o tomboy ay isang uri ng sakit sa pag-iisip]”. Twenty percent are undecided, and 1% did not give an answer [Chart 4].

Is being gay or lesbian contagious? 45% disagree, 38% agree

To the statement, “Being gay or lesbian is contagious [Nakakahawa ang pagiging bakla, lesbiyana o tomboy]”, the September 2013 survey found that a plurality 45% disagree and 38% agree. Sixteen percent areundecided, and 1% did not give an answer [Chart 5].

Can AIDS be considered a sickness of gays or lesbians? 45% agree, 33% disagree

The September 2013 survey found that a plurality 45% agree and 33% disagree with the statement,“Acquired Immuno Deficiency Syndrome or AIDS can be considered as a sickness of gays and lesbians [Ang Acquired Immuno Deficiency Syndrome o AIDS ay maituturing na sakit ng mga bakla, lesbiyana o tomboy]”. One out of five (21%) are undecided, and 1% did not give an answer [Chart 6].

Survey Background

The Social Weather Surveys of Second and Third Quarters 2013 were conducted on June 28-30, 2013 and September 20-23, 2013, respectively. Both surveys used face-to-face interviews of 1,200 adults nationwide, 300 each in Metro Manila, the Balance of Luzon, Visayas, and Mindanao (sampling error margins of ±3% for national percentages, and ±6% for Metro Manila, Balance Luzon, Visayas, and Mindanao).

The area estimates were weighted by National Statistics Office medium-population projections for 2013 to obtain the national estimates.

In both surveys, the introduction used for each test statement was, “I have here some statements which may reflect how people feel or think about gays or lesbians. Please tell me if you agree or disagree with these statements. You may indicate your answers by placing the card with the statement in the appropriate place in this rating board. (STRONGLY AGREE, SOMEWHAT AGREE, UNDECIDED IF AGREE OR NOT, SOMEWHAT DISAGREE, or STRONGLY DISAGREE)[Mayroon ako ritong mga statements o pangungusap na maaaring maglarawan sa nararamdaman o naiisip ng mga tao ngayon tungkol sa mga bakla, lesbiyana o tomboy. Pakisabi po kung kayo ay sumasang-ayon o hindi sumasang-ayon sa mga statements o pangungusap na ito. Pakilagay lang po ang kard na may pangungusap sa naaangkop na lugar sa rating board na ito. (LUBOS NA SUMASANG-AYON, MEDYO SUMASANG-AYON, HINDI TIYAK KUNG SUMASANG-AYON O HINDI, MEDYO HINDI SUMASANG-AYON, o LUBOS NA HINDI SUMASANG-AYON)]

The Social Weather Survey items on agreement-disagreement with specific positive and negative statements about gays and lesbians were not commissioned, and were done on SWS's own initiative.

The findings in this report were presented in the paper, “Measuring Homophobia in the Philippines”, by Vladymir Joseph Licudine <vlad.licudine@sws.org.ph> and Ma. Leah Czarina Aldave <leah.aldave@sws.org.ph> at the XVII World Congress of Sociology, held in Yokohama, Japan, last July 13-19, 2014. Please contact the authors for inquiries on the paper presented.

SWS employs its own staff for questionnaire design, sampling, fieldwork, data-processing, and analysis, and does not outsource any of its survey operations.

#

Chart 1

Chart 2

Chart 3

Source: http://www.sws.org.ph/

366-43-3. Adult

joblessness at 27.0%; 9% lost their jobs involuntarily, 14% resigned

February

04, 2015

Fourth Quarter 2014 Social Weather Survey:

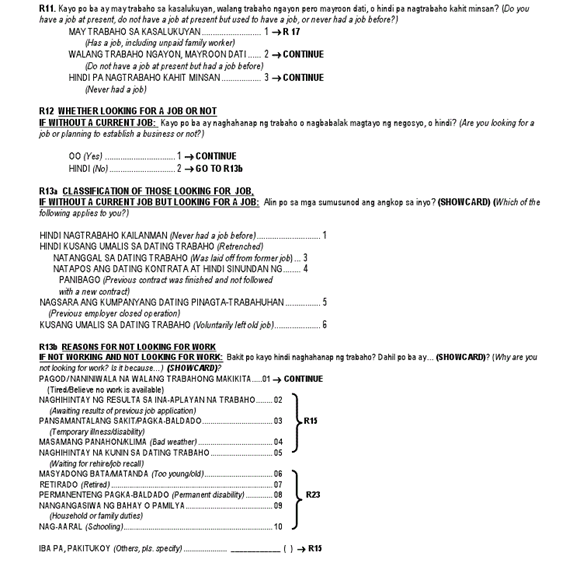

The Fourth Quarter 2014 Social Weather Survey, fielded over November 27-December 1, 2014, found adult joblessness at 27.0% (est. 12.4 million adults).

This is 4.1 points above the 22.9% (est. 10.4 million

adults) in September 2014. This brings the 2014 annual average to 25.4%, or

close to the 2013 annual average of 25.2%.

Joblessness was at a record-high 34.4% in March 2012. It has since then been

between 21.7% and 29.4% [Chart 1, Table 1].

The December 2014 adult joblessness rate consisted of 14% (est. 6.5 million adults) who voluntarily left their old jobs, 9% (est. 4.3 million adults) who involuntarily lost their jobs, and 3% (est. 1.5 million adults) who were first-time job seekers [Chart 2].

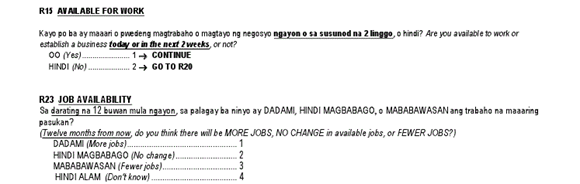

The survey also found that 36% of adults say the number of available jobs in the next 12 months will increase, 32% say it will not change, and 20% say it will decrease.

This gave a Net Optimism on job availability score of +16 (% more jobs minus % fewer jobs), classified by SWS as fair. This is 4 points above the fair +12 in September 2014 [Chart 3].

The SWS terminology for Net Optimism on job availability: +30 and above - "very high"; +20 to +29 - "high"; +10 to +19 - "fair"; +1 to +9 - "mediocre"; -9 to zero - "low"; -10 and down - "very low".

Profiles of the jobless

Adult joblessness consists of (a) those who voluntarily

left their old jobs, (b) those who lost their jobs due to economic

circumstances beyond their control, termed as the retrenched, and (c) those

seeking jobs for the first time.

The proportion of those who resigned or left their old jobs voluntarily rose by

2 points from 12% in September to 14% in December.

Those who were retrenched rose by 2 points, from 7% in September to 9% in December.

The 9% (correctly rounded) who were retrenched consisted of 6% whose previous contracts were not renewed, 2% whose employers closed operations, and 2% who were laid off.

First-time job seekers stayed at 3%.

Joblessness rose among women, and among 25 up

Compared to the previous quarter, adult joblessness rose sharply among women, from 33.2% in September to 41.7% in December, the highest since 42.5% in August 2012 [Chart 4, Table 2].

It barely moved among men, rising from 14.9% to 15.6%.

By age group, adult joblessness rose among those aged 25-34, from 30% in September to 32% in December [Chart 5, Table 3].

It rose among those aged 35-44, from 18% to 22%.

It also rose among those aged 45 and above, from 15% to 19%.

On the other hand, it fell among 18-24 (youth), from 50% to 48%.

Job availability prospect rose to "fair" +16

On the survey question, "Sa darating na 12 buwan mula ngayon, sa palagay ba ninyo ay DADAMI, HINDI MAGBABAGO, o MABABAWASAN ang trabaho na maaaring pasukan?" ["Twelve months from now, do you think there will be MORE JOBS, NO CHANGE in available jobs, or FEWER JOBS?"], optimism that there will be more jobs rose from 33% in September to 36% in December, while pessimism that there will be fewer jobs fell from 22% to 20%.

The proportion of those who say there will be no change in

job availability hardly changed from 33% to 32%.

This brought the Net Optimism on job availability score (% more jobs minus %

fewer jobs) up by 4 points, from "fair" +12 to "fair" +16.

SWS Joblessness versus Labor Force Survey (LFS) Unemployment

The SWS data on joblessness refer to the population of adults in the labor force. This is because respondents in the standard SWS surveys are those at least 18 years old. On the other hand, the official lower boundary of the labor force has always been 15 years of age.

In the SWS surveys, persons with jobs are those who have a job at present ("may trabaho sa kasalukuyan"), including unpaid family workers. The question does not use any past reference period. The SWS joblessness figures are consistently based on the traditional definition of joblessness as fulfilling two requirements: without a job at present and looking for a job. Those without a job without looking for one, such as housewives, retirees, differently abled, and students, are excluded from the labor force.

On the other hand, the official Labor Force Survey (LFS) definition of employed include all those who, during the week before the interview date, are 15 years and over as of their last birthday and are reported to be either:

a. At work. Those who do any work for at least one hour during the reference week for pay or profit, or work without pay on the farm or business enterprise operated by a member of the same household related by blood, marriage, or adoption; or

b. With a job but not at work. Those who have a job or a business but are not at work because of temporary illness/injury, vacation, or other reasons. Also, persons who expect to report for work or to start operation of a farm or business enterprise within two weeks from the date of the enumerator's visit are considered employed.

Before April 2005, the official definition of the unemployed was those who did not work during the reference week and looking for work. However, from April 2005 onwards, the official definition was refined as follows:not working, looking for work, and available for work. It subtracts those who are looking but not available for work and adds those available but not looking for work for the following reasons: tired/believe no work is available, awaiting results of a job application, temporarily ill/disabled, bad weather, and waiting for rehire/job recall.

This means that if the availability requirement is included, adult joblessness in December 2014 was 17.9% (est. 7.3 million adults). That is, 17.6% (est. 7.2 million adults) who were not working, looking for work, and available for work and 0.2% (est. 90900 adults) who were not working, not looking for work due to the reasons mentioned above, but available for work.

Therefore, among the 12.4 million adults who were jobless and were looking for work, 41% (est. 5.1 million adults) were not available for work at present or in the next two weeks.

Survey Background

The December 2014 Social Weather Survey was conducted from November 27-December 1, 2014 using face-to-face interviews of 1,800 adults nationwide, 300 each in Metro Manila, the Balance of Luzon and Mindanao, and 900 in the Visayas (sampling error margins of ±2% for national percentages, ±6% each for Metro Manila, Balance Luzon and Mindanao, and ±3% for Visayas).

The area estimates were weighted by National Statistics Office medium-population projections for 2014 to obtain the national estimates.

The quarterly Social Weather Surveys on joblessness and job availability are not commissioned, but are done on SWS's own initiative and released as a public service, with first printing rights assigned to BusinessWorld.

SWS employs its own staff for questionnaire design, sampling, fieldwork, data processing, and analysis, and does not outsource any of its survey operations.

The exact SWS questionnaire items on joblessness are as follows:

Source: http://www.sws.org.ph/

SUB-SAHARAN AFRICA

366-43-4. Tanzanians see increased

corruption, ineffective fight against it

February

06, 2015

A

majority of Tanzanians say that the level of corruption in the country has

increased over the past year, according to the latest Afrobarometer survey. The

police, tax officials, and judges and magistrates perceived as the most

corrupt. Citizens’ rating of the government’s handling of the fight against

corruption has improved slightly since 2012 but still remains mostly negative –

and far more negative than a decade ago. Tanzanians laud news media’s

effectiveness and show considerable support for the role played by the media in

exposing corruption. These results come at a time when the Tanzanian public is

eagerly monitoring how the government is responding to the latest grand

corruption scandal. Early last year, the media reported that hundreds of

billions of shillings were siphoned from the Tegeta Escrow account at the Bank

of Tanzania, leading to public outcry and suspension of donor assistance to the

Tanzanian government. A parliamentary probe implicated key figures in the

government, and Parliament passed a resolution calling for immediate actions

against them. Key findings Two-thirds

(67%) of Tanzanians say that corruption increased during the past year.

Sub-groups

§

that hold this view the most include people in Zanzibar (93%) (Figure 1) and

urbanites (72%). The more educated a person is, the more likely he or she is to

say corruption increased. Half of

Tanzanians (50%) believe that most or all police are corrupt. More than

one-third say

§

most or all tax officials and judges and magistrates are corrupt. Slightly more Tanzanians than in 2012 say the

government is handling the fight against

§

corruption well or very well (37% vs. 33%). But a majority (58%) rates the government’s

performance as bad or very bad. Amidst

persistent reports of malfeasance in the public sector, 65% of Tanzanians say

that the media should constantly investigate and report on government

corruption and mistakes (Figure 4).

Afrobarometer

Afrobarometer

is an African-led, non-partisan research network that conducts public attitude

surveys on democracy, governance, economic conditions, and related issues

across more than 30 countries in Africa. Five rounds of surveys were conducted

between 1999 and 2013, and Round 6 surveys are currently under way (2014-2015).

Afrobarometer conducts face-to-face interviews in the language of the

respondent’s choice with nationally representative samples of between 1,200 and

2,400 respondents.

The

Afrobarometer team in Tanzania, led by REPOA, interviewed 2,386 adult

Tanzanians between August 26th and September 29th 20141. A sample of this size

yields results with a margin of error of +/- 2% at a 95% confidence level.

Previous surveys have been conducted in Tanzania in 2001, 2003, 2005, 2008. and

2012..

EAST EUROPE

366-43-5. Paris Terrorist Attacks:

Russian Assessments

Paris shootings were caused by

ineffective migration policies of the French government and improper behavior

of the Charlie Hebdo journalists.

MOSCOW, January 26, 2015. Russian Public Opinion Research Center (VCIOM)

presents the results of the survey describing how many Russians are aware of

the terrorist attack on the French weekly newspaper Charlie Hebdo as well as

what they think was the reason behind the shootings.

Seventy-four percent of Russians are

aware of what happened in the offices of the Charlie Hebdo weekly newspaper on

January 7th. Twenty-three percent of Rusians have

seen the Prophet Muhammad cartoons that were published before

the shooting; 51% of Russians heard about the terrorist attack but did not see

any cartoons. Ninety percent of residents of Moscow and St.Petersburg are

informed about the tragedy.

The major reasons behind the Charlie

Hebdo attack are insulting Muslim religious feelings

(30%) and soft mass media policies of the French authorities that allow them

insulting the believers (25%). Eleven percent of Russians oppose them stating

that the main cause is that the French authorities allow immigrants to enter

the country and this creates a huge flow of immigrants. Eight percent believe

that the tragedy happened because of the cruelty of the Muslim extremists; 6%

mention poor work of the French police and security services.

An overwhelming majority of

respondents (87%) condemn the armed attack on the editorial and the killings of

the journalists; at the same

time, 39% say that they can understand why this happened; 48% fail to explain

the reason behind the tragedy.

The VCIOM opinion poll was

conducted on January 17-18, 2015. 1600 respondents were interviewed

in 132 communities in 46 regions of Russia. The margin of error does not exceed 3,5%.

|

Last week the French weekly

newspaper published the cartoons of the Prophet Mohammed that provoked the

attacks on the offices of the newspaper; several journalists were killed.

Have you heard about it/have you seen the cartoons? (close-ended question,

one answer) |

|||||||

|

|

Total respondents |

Moscow and St.Petersburg |

Million cities |

More than 500 ths |

100–500 ths |

Less than 100 ths |

Rural area |

|

Yes, I heard about it and I

have seen the cartoons |

23 |

21 |

21 |

22 |

25 |

18 |

27 |

|

Yes, I know what happened but I

have not seen the cartoons |

51 |

69 |

43 |

36 |

48 |

54 |

50 |

|

I know nothing about it |

22 |

5 |

35 |

38 |

23 |

23 |

19 |

|

Don`t know |

4 |

5 |

1 |

4 |

3 |

4 |

4 |

|

In your opinion, what is the basic

reason behind the shooting? (close-ended question, one answer, % of those who

know what happened) |

|||||||

|

|

Total respondents |

A Just Russia party |

Supporters of LDPR |

Supporters of CPRF |

Supporters of United Russia party |

Supporters of non-parliament

parties |

I would not take part in elections |

|

French journalists who insulted

Muslim religious values |

30 |

23 |

22 |

33 |

33 |

24 |

29 |

|

Policies of the French government

that allows journalists insulting religious values |

25 |

35 |

16 |

19 |

27 |

20 |

24 |

|

Policies of the French government

that allows Muslims entering the country |

11 |

10 |

25 |

13 |

9 |

12 |

11 |

|

Several extremist Muslims whose

response to these cartoons was violence |

8 |

6 |

8 |

8 |

7 |

8 |

9 |

|

Poor work of French police and

security services |

6 |

13 |

6 |

7 |

6 |

4 |

7 |

|

Politics of the self-proclaimed

Islamic State; hatred of the Islamic extremists towards secular society and

freedom of speech |

5 |

3 |

12 |

2 |

5 |

12 |

6 |

|

Other |

3 |

<1 |

2 |

6 |

2 |

8 |

3 |

|

Don`t know |

12 |

10 |

10 |

11 |

12 |

12 |

11 |

|

What are your attitudes towards

people who attacked the French weekly newspaper`s office? (close-ended

question, one answer, % of those who know what happened) |

||||||

|

|

Total respondents |

Aged 18-24 |

Aged 25-34 |

Aged 35-44 |

Aged 45-59 |

60 and over |

|

I do not understand and do not

appreciate such actions |

48 |

43 |

47 |

45 |

49 |

54 |

|

I do not approve of them but

I understand the reasons behind it |

39 |

38 |

41 |

42 |

40 |

35 |

|

I understand and approve of the

actions of such people |

5 |

10 |

5 |

5 |

3 |

3 |

|

Don`t know |

8 |

9 |

7 |

8 |

8 |

8 |

Note: Using materials from the site www.wciom.ru or wciom.com,

as well as distributed by VCIOM, the reference to the source (or hyperlink for

the electronic media) is obligatory!

366-43-6. Ruble Exchange Rate: Fears

And Forecasts

Most of Russians are afraid of the further

drop in the ruble`s value; at the same time, one-third of Russians believe that

in the coming months the ruble exchange rate will not change much.

MOSCOW, January 20, 2015. Russian Public Opinion Research Center (VCIOM)

presents the information describing what currency Russians use to save money;

how much they are concerned about the ruble decline; what they expect to happen

with the ruble in the months to come.

Half of Russians (52%) do not have

savings. An overwhelming majority of those who make savings still

prefer rubles (46%); 4% prefer dollar, 2% choose euro; and less than

1% opt for other foreign currencies.

Russians show high levels of

interest towards foreign currencies:

66% report that they keep an eye on the situation in the currency markets (27%

regularly; 39% - from time to time). Those who keep an eye on the situation

constantly are respondents with high education diplomas (35%) and high

financial income (35%).

Sixty-three percent of Russians are

concerned about the current dollar exchange rate 63% (57% in November 2014). Those who are most concerned are

residents of Moscow and St. Petersburg (73%), respondents with high income

(72%) and students (71%). Thirty-three percent of Russians are not bothered

with the problem.

The reasons behind the drop of ruble

are the policies of western countries and anti-Russian sanctions (18%) and a

decrease in oil prices (17%). Rarely

respondents mention the general economic situation in the country (7%) or the

policies of the Russian authorities (6%). Five percent say that the situation

is artificial, and certain people benefit from that.

Today much less Russians are

negative about the future of the ruble in the near two or three months compared

to November 2014: 27% say that ruble will keep

falling (46% in late 2014). On the contrary, more Russians believe that the

ruble exchange rate will stay at the same level as today (from 24% to 36%).

Only 16% are confident that ruble will strengthen; this share is higher than it

was before.

If the dollar` value keeps

increasing, 77% of Russians will make no moves. Those who will try to do something will invest money

in real property and expensive items (6%). Certain respondents would buy

dollars in exchange for rubles (3%) or euro or other currency (1%). Three percent

of Russians will start spending their savings.

The VCIOM opinion poll was

conducted on January 10-11, 2014. 1600 respondents were interviewed

in 132 communities in 46 regions of Russia. The margin of error does not exceed 3,5%.

|

What

currency do you use for your savings? (close-ended question, not more than 3

answers) |

|||||||||||||||||

|

|

I qrt 08 |

IV qrt 08 |

I qrt 09 |

II qrt 09 |

III qrt 09 |

IV qrt 09 |

I qrt 10 |

II qrt 10 |

III qrt 10 |

IV v qrt 10 |

IV qrt 11 |

II qrt 13 |

III qrt 13 |

IV qrt 13 |

I qrt 14 |

IV qrt 14 |

I qrt 15 |

|

Ruble |

33 |

37 |

33 |

28 |

27 |

30 |

21 |

26 |

25 |

24 |

38 |

55 |

49 |

40 |

40 |

47 |

46 |

|

Dollar |

1 |

1 |

2 |

2 |

3 |

3 |

2 |

3 |

3 |

3 |

5 |

5 |

4 |

5 |

4 |

3 |

4 |

|

Euro |

2 |

1 |

2 |

2 |

2 |

3 |

2 |

2 |

3 |

2 |

4 |

2 |

1 |

3 |

2 |

2 |

2 |

|

Other currency |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

<1 |

1 |

<1 |

<1 |

<1 |

<1 |

<1 |

|

No savings |

57 |

58 |

61 |

66 |

65 |

64 |

70 |

69 |

70 |

66 |

55 |

38 |

46 |

53 |

54 |

49 |

52 |

|

Don`t know |

7 |

2 |

3 |

2 |

4 |

3 |

7 |

3 |

3 |

8 |

3 |

5 |

2 |

2 |

2 |

2 |

1 |

|

Do you

follow the dollar to ruble exchange rate? (close-ended question, one answer) |

|||||||||||

|

|

IV v 2008 |

IV qrt 2009 |

IV qrt 2010 |

IV qrt 2011 |

IV qrt 2012 |

IV qrt 2013 |

I qrt 2014 |

II qrt 2014 |

III qrt 2014 |

IV qrt 2014 |

I qrt 2015 |

|

Yes, regularly |

17 |

13 |

13 |

13 |

11 |

14 |

16 |

14 |

19 |

27 |

27 |

|

Yes, sometimes |

37 |

37 |

33 |

30 |

31 |

35 |

37 |

37 |

36 |

38 |

39 |

|

No |

43 |

48 |

52 |

55 |

57 |

50 |

46 |

47 |

44 |

34 |

33 |

|

Don`t know |

3 |

1 |

2 |

2 |

1 |

2 |

1 |

1 |

2 |

1 |

1 |

|

Are you

concerned about the dollar exchange rate? (close-ended question, one answer) |

|||||

|

|

February 2002 |

July 2013 |

February 2014 |

November 2014 |

January 2015 |

|

Rather yes |

62 |

29 |

42 |

57 |

63 |

|

Rather no |

34 |

68 |

53 |

39 |

33 |

|

Don`t know |

4 |

4 |

5 |

4 |

4 |

|

The

ruble`s exchange rate against the U.S. is decreasing. What is the reason

behind that? (open-ended question, any number of answers) |

|

|

|

Total respondents |

|

American/western policies,

sanctions |

18 |

|

Drop in oil prices |

17 |

|

Economic situation in the country |

7 |

|

Politics of Russian authorities |

6 |

|

Artificial situation; someone

benefits from that |

5 |

|

Situation in Ukraine |

3 |

|

Central Bank of Russia`s policies

(not supporting ruble) |

2 |

|

Increase of prices |

1 |

|

No domestic production |

1 |

|

Sochi Olympics |

<1 |

|

Russia is losing its positions in

the world |

<1 |

|

Corruption |

<1 |

|

It is seasonal |

<1 |

|

Other |

2 |

|

I do not mention that |

10 |

|

Don`t know |

35 |

|

In your

opinion, how will the ruble`s positions change in recent two or three months?

(close-ended question, one answer) |

||||

|

|

July 2013 |

February 2014 |

November 2014 |

January 2015 |

|

Ruble will be cheaper |

34 |

41 |

46 |

27 |

|

Ruble will stay at the same level |

38 |

33 |

24 |

36 |

|

Ruble will get more expensive |

8 |

5 |

12 |

16 |

|

Don`t know |

19 |

21 |

17 |

21 |

|

If the

dollar exchange rate keeps growing, what will you do? (close-ended question,

not more than two answers) |

|||||

|

|

October 2011 |

July 2013 |

February 2014 |

November 2014 |

January 2015 |

|

Nothing special |

74 |

77 |

75 |

81 |

77 |

|

I will invest money in real

property and other expensive items |

9 |

6 |

8 |

4 |

6 |

|

I will exchange rubles for dollars |

5 |

9 |

7 |

5 |

3 |

|

I will start spending money and

savings* |

- |

- |

3 |

2 |

3 |

|

I will exchange euro (other

currency) for dollars |

2 |

2 |

2 |

1 |

1 |

|

Other |

1 |

2 |

1 |

2 |

3 |

|

Don`t know |

10 |

6 |

6 |

6 |

8 |

*In 2011 and 2013 this answer choice

was not used

Note: Using materials from the site www.wciom.ru or wciom.com,

as well as distributed by VCIOM, the reference to the source (or hyperlink for

the electronic media) is obligatory!

366-43-7. Protest Actions:

Manifestations Of Democracy Or Crisis?

The level of protest potential of

Russians is still low. Rallies and demonstrations are mainly perceived as

crisis symptoms rather than instruments to solve problems.

MOSCOW, January 23, 2015. Russian Public Opinion Research Center (VCIOM)

presents the results of the survey concerning the public and personal protest

potential in Russia.

The protest potential growth that

started in the first quarter of 2014 was mentioned in the first decade of

January 2015: protest potential index* exceeded the previous monthly average and

reached 34 points. Twenty-seven

percent of Russians believe that protests are possible in their community.

However, a relative majority of Russians (66%) still think that the protests

are hardly possible in their cities/rural area.

The index measuring Russians`

readiness to take part in mass rallies has been fluctuating between 23 and 25

points over the recent half a year. In

January the personal protest potential index** made up 25 points. Three quarter

of Russians (77%) report that they will never hold a mass meeting. Only 16% say

they would (the shares of those have low level of education and low income is

23% in each group).

Russians have no desire to take to

the streets to protest against social injustice because they think that rallies

are useless (37%), however today the number of

those who have such a stance is smaller than in was in 2013 (47%). Others are

afraid that the law enforcement officers will use force (28%); that they will

have problems at work (26%), or they will be arrested (25%). Every fifth

respondent (19%) thinks that people worry about their only problems, and they

do not want to deal with social problems. Sixteen percent cite the lack of

information about protest actions (16%); 12% do not like mass gatherings in

general.

For the time being, Russians are

much more negative about rallies than they were three years ago: in 2012, 22%

said that protests were unacceptable and would lead to the collapse; today the

share of such people is 30%. Those

who think so are mainly residents of Moscow and St.Petersburg (42%), rather

than rural area residents (27%). More than one-third of respondents

(38%) say that rallies are manifestations of the systemic crisis (28% in 2012).

At the same time, the share of those who believe that rallies, picketing etc.

are manifestations of democracy and general means to solve problems has

decreased (from 36% to 23%).

*Public protest potential index shows how possible Russians think the mass protests

are. The index is based on the question “In your opinion, are mass protests

against fall in living standards possible in your city/rural area?” If the

answer is “rather possible”, the coefficient is 0,9; “hardly possible” -– 0,1;

“undecided” – 0,5. The index is measured in percentage points and can vary

between 10 and 90. The higher the value of index is, the more confident

Russians are that the protests may happen in their community.

**Personal protest potential index shows the readiness of Russians to take part in mass

protests. The index is based on the question “If mass protests against fall in

living standards happen in our city/rural area will you personally take part or

not?” If the answer is “rather yes”, the coefficient is 0,9; “rather no”

– 0,1; “undecided” – 0,5. The index is measured in percentage points and

can vary between 10 and 90. The higher the value of index is, the more

respondents are ready to take part in the protests.

The VCIOM opinion poll was

conducted on January 10-11, 2015. 1600 respondents were interviewed

in 132 communities in 46 regions of Russia. The margin of error does not exceed 3,5%.

|

In your opinion, are mass protests

against fall in living standards and unfair policies possible to happen in

your city/rural area to protect human rights and freedoms? (close-ended

question, one answer) |

||||||||||||||||

|

|

I.11 |

I.12 |

I.13 |

I.14 |

II.14 |

III.14 |

IV.14 |

V.14 |

VI.14 |

VII.14 |

VIII.14 |

IX.14 |

X.14 |

XI.14 |

XII.14 |

10-11 .I.15 |

|

Rather possible |

30 |

30 |

26 |

24 |

25 |

21 |

19 |

18 |

17 |

19 |

14 |

14 |

18 |

22 |

23 |

27 |

|

Hardly possible |

62 |

64 |

70 |

71 |

70 |

75 |

77 |

78 |

81 |

77 |

81 |

82 |

77 |

73 |

72 |

66 |

|

Don`t know |

8 |

6 |

4 |

5 |

5 |

4 |

4 |

3 |

3 |

4 |

5 |

4 |

5 |

5 |

5 |

7 |

|

Public protest potential* |

37 |

36 |

32 |

31 |

32 |

28 |

27 |

26 |

25 |

27 |

23 |

23 |

26 |

30 |

30 |

34 |

|

If such protests take place, will

you personally take part in them? (close-ended question, one answer) |

||||||||||||||||

|

|

I.11 |

I.12 |

I.13 |

I.14 |

II.14 |

III.14 |

IV.14 |

V.14 |

VI.14 |

VII.14 |

VIII.14 |

IX.14 |

X.14 |

XI.14 |

XII.14 |

10-11 .I.15 |

|

Rather yes |

25 |

21 |

17 |

18 |

19 |

18 |

16 |

16 |

17 |

16 |

14 |

14 |

15 |

18 |

16 |

16 |

|

Rather no |

68 |

74 |

78 |

76 |

76 |

77 |

78 |

79 |

79 |

79 |

82 |

81 |

80 |

77 |

79 |

77 |

|

Don`t know |

7 |

5 |

4 |

6 |

5 |

5 |

5 |

5 |

4 |

5 |

5 |

5 |

5 |

5 |

5 |

7 |

|

Personal protest potential index** |

33 |

29 |

25 |

27 |

27 |

26 |

25 |

25 |

25 |

25 |

23 |

23 |

24 |

26 |

25 |

25 |

|

In your opinion, why do most of

Russians refrain from taking part in protest actions and demonstrations

today? (close-ended question, not more than 5 answers) |

|||||

|

|

III.2011 |

XII.2011 |

I.2012 |

I.2013 |

I.2015 |

|

They are confident that rallies

and demonstrations are useless |

57 |

42 |

39 |

47 |

37 |

|

They are afraid that the

representatives of the law enforcement bodies may use force |

35 |

30 |

26 |

29 |

28 |

|

They are afraid that they may have

problems at work |

36 |

27 |

28 |

29 |

26 |

|

They are afraid of being

imprisoned |

26 |

25 |

23 |

28 |

25 |

|

They are busy with their personal

life; they are not interested in the problems of the country |

25 |

21 |

23 |

21 |

19 |

|

Lack of information about protest

actions |

22 |

22 |

18 |

23 |

16 |

|

Dislike for public gatherings |

8 |

12 |

12 |

16 |

12 |

|

Only loafers and stupid persons

take part in rallies |

8 |

8 |

11 |

9 |

11 |

|

Dislike for the organizers of such

actions |

6 |

7 |

8 |

10 |

8 |

|

They are not satisfied with everything;

no reason to take part in protest actions |

6 |

9 |

8 |

6 |

8 |

|

Fear that no one will come to take

part in the protest action |

9 |

6 |

4 |

5 |

8 |

|

Other |

3 |

2 |

2 |

2 |

5 |

|

Don`t know |

4 |

9 |

12 |

3 |

4 |

|

Which of the following statements

about the rallies and protest actions is closer to yours? (close-ended

question, one answer) |

||

|

|

I.2012 |

I.2015 |

|

Actions and rallies are general

means to solve problems; they are manifestations of democracy |

36 |

23 |

|

Actions and rallies are

manifestation of democracy during systemic crisis; they are extreme measures

that can be used only in exceptional cases |

28 |

38 |

|

Actions and rallies lead to the

collapse; they do not help solving problems; they destabilize the situation

in the country and should be avoided |

22 |

30 |

|

Don`t know |

14 |

9 |

WEST EUROPE

366-43-8. Economist/Ipsos

MORI January 2015 Issues Index

Published:6 February 2015

Fieldwork:23 January - 2 February

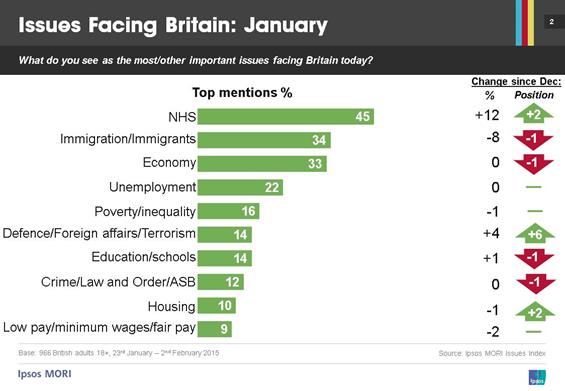

Economist/ Ipsos MORI January 2015 Issues index – the NHS replaces immigration as the most important issue facing Britain

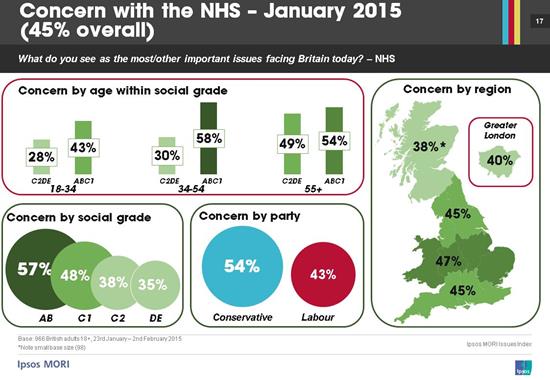

The first Economist/Ipsos MORI Issues Index of 2015 shows that concern about the NHS has increased by 12 percentage points since December of last year, and it is now seen as the most important issue facing Britain – mentioned by almost half (45%) of the public. This is the highest level of concern since April 2006, following an increased political emphasis being placed on healthcare in the runup to the 2015 election, and reports of a winter A&E ‘crisis’.

Looking at different population subgroups, it is clear that older people, and the more affluent are more likely to be concerned about the NHS. Concern rises from a third (35%) of DEs to nearly six in ten (57%) of ABs. Similarly, 35% of those aged 18-34 are concerned compared with three fifths (59%) of those aged 55-64. Over half (54%) of Conservative voters are concerned, a sharp increase of 22 percentage points since December.

Though concern about NHS has increased sharply, and is high, it is worth remembering that historically concern has been much higher in the past – indeed, it peaked at 72% in February 2002. For much of Tony Blair’s tenure in Downing Street it was the most important issue facing Britain, and it will be interesting to see if levels of concern are maintained throughout the year.

A third (34%) mention immigration, the issue which was of most concern to the public between June to December last year, and concern has fallen by 8 percentage points. However, for some, including 18-34 year old C2DEs, it remains the most important issue facing Britain. A similar percentage (33%) mention the economy, and a fifth (22%) mention unemployment, though levels of concern about these issues are unchanged since December.

Elsewhere, just 5% are concerned about inflation/prices, the lowest level of concern in eight years.

366-43-9. Captains

of Industry support Britain being in the EU

Ipsos

MORI's Captains of Industry Survey 2014

Published:4 February 2015

Fieldwork:September - December 2014

Could British business leaders be

the biggest block to UKIP’s campaign for parliament? The new Ipsos MORI

Captains of Industry survey shows that although 45% of Captains want to return

to being part of an economic community, without political links, just 1% would

be happy to leave it all together. Just under half (45%) want to continue our

relationship with the EU as it stands.

Captains like the ease of access to

markets and people that EU membership gives them, but not the accompanying

regulations. The leading business advantages they see are the ease of

cross-border trading (46%), ease of access to EU customers (41%) and being part

of the single market (40%). Recruitment is made easier too for one in three

Captains (34%) with no need for visas for EU workers.

The disadvantages of EU membership

cited by Captains include: the volume of regulations (52%) and the changes to

regulations (55%), which top the table of disadvantages. However, the EU’s

economic outlook also makes it into the top three with just under half (46%) of

Captain’s citing this as a concern.

It isn’t just EU regulation that

concerns industry leaders, 79% consider the level of regulation harmful to the

UK economy. However, the strength of agreement on this point has declined over

the last five years from 44% strongly agreeing in 2010, to 28% at the end of

2014. This may suggest that businesses are either becoming accustomed to

increasing regulation, or that the burden has improved a little in recent

years.

The most requested improvement in

regards to the regulatory burden is for employment legislation to be simplified

(24%). Other suggestions include more harmonisation between UK and EU

regulations (11%), reducing general levels of regulation (8%) and reducing tax

regulation (7%).

Technical note

·

These

are the findings of the 2014 study of Captains of Industry, widely acknowledged

as the authoritative source of opinion on Britain's business elite.

·

Respondents

are executive board-level directors and chairmen

·

Companies

are from:

o top 500 industrials by turnover;

o top 100 financial companies by

capital employed

·

A

total of 108 respondents took part, details of which are provided below

·

Fieldwork

was conducted September – December 2014

·

104

interviews were conducted face-to-face and four by telephone

366-43-10. Public

perceptions of climate change in Britain following the winter 2013/14 flooding

Findings

from research for Cardiff University

Published:2 February 2015

Fieldwork:28 August - 31 October 2014

A recent Ipsos MORI survey for Cardiff University updates trend data on public attitudes to climate change as well as providing new data on how the British public responded to the flooding last winter. The study tested whether the public, but particularly those affected by flooding, link the winter 2014 flooding to climate change.

It shows that the British public’s belief in climate change, and its human causes, rose significantly last year and is now at its highest level since 2005. Most people say they have noticed signs of climate change in their lifetime, particularly changing weather patterns or extreme weather and heavy rainfall or flooding.

Various factors were felt to have contributed to the flooding in winter 2013/14, including climate change, and a majority agreed that "The floods showed us what we can expect in the future from climate change". The survey found that those who lived in flood affected areas and whose property had been directly affected by flood waters were even more convinced that climate change is happening and concerned by it. They were also more likely to see climate change as a key issue facing the UK

Technical Details

·

Two samples were used in this

research:

o A

nationally representative survey of adults aged 16+ in the UK (n=1,002)

o A

boost of approximately 200 interviews in each of five areas that had been

affected by the floods in some way, in order to provide a sample of respondents

with more direct experience of the flooding: Aberystwyth (n=200), Dawlish (n=198),

Gloucester to Tewkesbury (n=198), Hull (n=200) and Sunbury to Windsor (n=199)

o These

five areas combined provide a flooded area sample with n=995. Of these, those

whose property had been directly affected formed the ‘directly affected’ sample

referred to in the report (n=135)

·

All respondents were interviewed

face to face in their home using Computer

Assisted Personal Interviewing (CAPI) between 28

August and 31 October 2014. Quotas were set on age, gender and working status

to ensure the final achieved samples were representative of the GB population

in the case of the national sample and each of the five areas for the flooded

area sample. The data were then weighted after fieldwork to the known

population profiles.

·

The findings from previous years

were from nationally representative in-home quota surveys conducted by Ipsos

MORI in Great Britain. Respondents were aged 15+ and weighted to the profile of

the known population.

o 2013:

Survey took place between 8 and 26 March 2013 (n=961)

o 2010:

Survey took place between 6 January and 26 March 2010 (n=1,822).

o 2005:

Survey took place between 1 October and 6 November 2005 (n=1,491).

366-43-11. Overwhelming

public support for the ‘Gordon’s

Fightback’ Campaign

Published:2 February 2015

Fieldwork:12 - 19 January 2015

An Ipsos MORI Scotland poll for the Gordon’s Fightback campaign shows overwhelming support for their key objectives. Almost all of those polled (97%) would support the UK government introducing a new system of fast tracking benefits for those with a terminal illness, such as motor neurone disease. Support for such a measure is overwhelming across all groups in the population.

Similarly, there is a very high level of support for the UK government increasing the amount of public money spent on research into motor neurone disease. Over three quarters of those interviewed (78%) would support doubling the funding from around £5 million a year to £10 million.

The poll also highlights low public awareness of Motor Neurone Disease compared to other illnesses. A third (32%) of participants know a great deal or a fair amount about Motor Neurone Disease, significantly lower than cancer (79%), diabetes (73%), heart disease (69%) and Alzheimer’s disease (61%).

Mark Diffley, Research director at Ipsos MORI Scotland said:

“In

recent months many of us have been moved by ‘Gordon’s Fightback’, the campaign

dedicated to changing the lives of those with Motor Neurone Disease. This poll

shoes overwhelming public support for the campaign’s objectives of increasing

funding to find a cure for MND and fast-tracking state benefits to those with a

terminal illness. The campaign will now be focussed on ensuring that progress

can be made to achieving these objectives.’

Technical details:

·

Results are based on a survey of

1,001 respondents (adults aged 18+) conducted by telephone

·

Fieldwork dates: 12th January to

19th January 2015

·

Data are weighted by: age, sex and

working status using census data; tenure using Scottish Household Survey data;

and public-private sector employment using Scottish Government Quarterly Public

Sector Employment series data

·

Where results do not sum to 100%,

this may be due to computer rounding, multiple responses, or the exclusion of

“don’t know” categories

·

Results are based on all

respondents (1,001) unless otherwise stated

366-43-12.

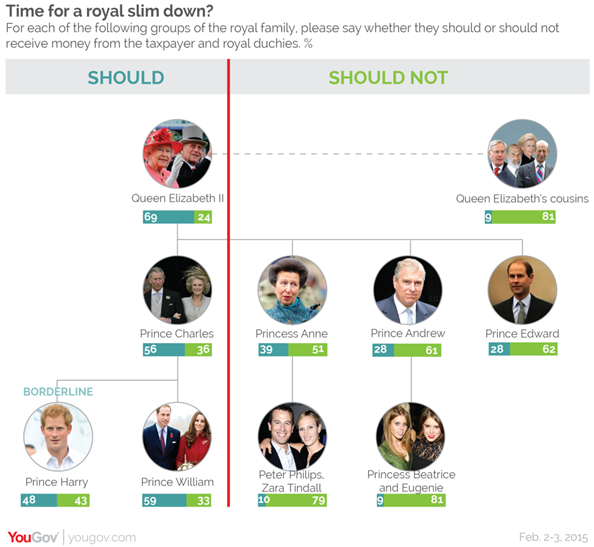

UK: Voters: time to slim down the royal family

Most British people say

that apart from the core royal family of the Queen, Charles and his

descendants, the rest should no longer receive money from the taxpayer and

royal estates

In terms of public opinion, the British royal family is enjoying something of a heydey. The Queen has long since recovered from the dark days after Princess Diana's death, Willsand Kate are very popular, and even Prince Charles has enjoyed a turnaround in the past five years. However, new research from YouGov reveals that the extent of the British public's enthusiasm for the royal family is very strictly limited to the 'core' royals in the direct line of succession. The minor royals are not thought to warrant any support from the taxpayer or even the Royal Duchies.

The research asks British people which of the major adult groupings of the royal family should continue to receive public money and revenue from the royal estates. Apart from the core family (the Queen and Prince Philip, Charles and Camilla and Prince William and Catherine; all supported in their current funding setup by a majority), the public think it’s time to cut the others off.

Thought least deserving of preferential funding are the Queen’s cousins, descended from King George V (the Duke and Duchess of Gloucester, Duke and Duchess of Kent, Princess Alexandra and Prince and Princess Michael of Kent), as well as the Queen’s grandchildren (Princess Beatrice and Eugenie, and Peter Phillips and Zara Tindall). Fewer than 10% think these groups should continue with their current financial arrangements.

Only 28% think that Prince Andrew and Prince Edward, two of the Queen’s sons, should be allowed to receive public money and revenue from the royal duchies, while slightly more (39%) think Princess Anne should qualify.

Even Prince Harry, fourth in line to the throne, only narrowly avoids the financial chop. 48% say he should be allowed to receive money by his current means, 43% say he should not.

For 250 years Parliament paid the Queen a fixed amount of money, through the Civil List, insensitive to the rate of inflation. But the Coalition’s spending review of 2010 changed all that, and as of 2013 the Queen has received an inflation-proof 15% cut of revenue from the Crown Estate – a property portfolio with soaring value – through the Sovereign Support Grant.

The cost to the taxpayer of the royal family is around 58p per head per year, or around 0.005% of total public spending. Still, republicans can argue that money raised from the Crown Estate (or in Charles’s case, the Duchy of Cornwall) is strictly hereditary, and benefits from generous tax exemptions.

366-43-13.

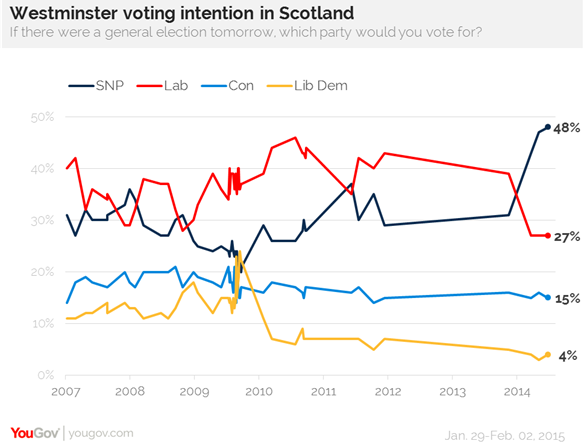

Scotland: SNP lead at 21

February

03, 2015

The Scottish National

Party has retained its lead in Scotland – and on the question of Scottish independence,

Yes leads No by 4 points

The recently appointed leader of Scottish Labour, Jim Murphy, made a joint proposal with Gordon Brown yesterday to devolve further powers to Scotland. The powers would go beyond those suggested by the Smith Commission – the report formalising promises made by Westminster leaders shortly before September’s referendum – to give Scotland the final word on the ‘bedroom tax’, and the ability to set benefits in other, non-devolved areas of welfare.

Jim Murphy has been handed the task of restoring Labour’s fortunes in Scotland, but the first YouGov/Times poll of Scottish people conducted wholly after his appointment on December 13 reveals the challenge ahead.

SNP has retained its lead, on 48% in February (up 1% from December). Labour remains at 27%, the same as December and October, but down considerably from its pre-referendum lead in June of 8 (39% to the SNP’s 31%). The results mean Labour could lose up to 30 seats in Scotland in May.

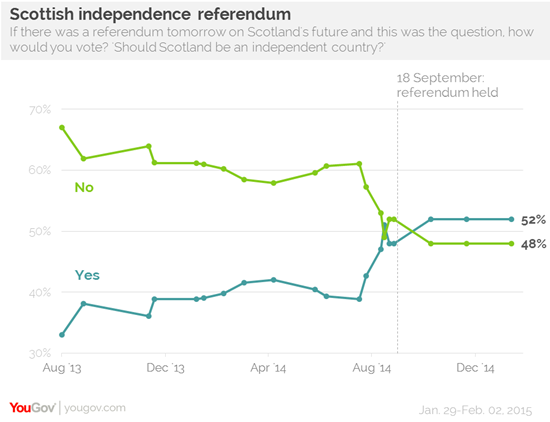

SNP's lead comes in conjunction with renewed support for Scottish independence. The final result on September 18 was Yes 45%, No 55%, however since then the Yes lead has sustained at an all-time high of 52% to the No camp's 48%.

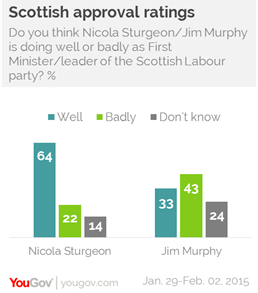

Nicola Sturgeon, Scotland’s first minister and leader of the SNP since November, enjoys the highest approval rating of any of the main party leaders. At net +42 among Scottish people (64% say she is doing well, 22% badly), she outperforms Nigel Farage in Britain-wide surveys (in October, 61% said he was doing well, 26% badly).

Jim Murphy fares around as well in Scotland as David Cameron does in national polls, at -10 (David Cameron's average so far in 2015). However, his approval among Scottish Labour voters (+55) is considerably higher than Ed Miliband’s approval among British Labour voters (+22).

NORTH AMERICA

366-43-14. Obama Approval Ratings Still

Historically Polarized

February

06, 2015

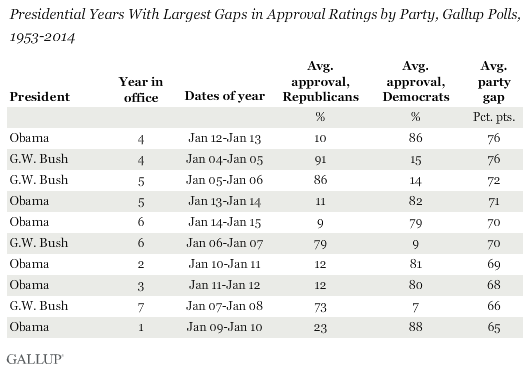

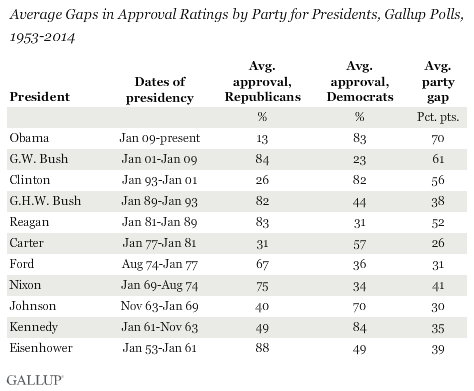

PRINCETON, N.J. -- Throughout President Barack Obama's sixth full year in office, an average of 79% of Democrats, compared with 9% of Republicans, approved of the job he was doing. That 70-percentage-point party gap in approval ratings ties for the fifth-most-polarized year for a president in Gallup records dating back to 1953.

Each of Obama's six years in office rank among the 10 most polarized in the last 60 years, with George W. Bush holding the other four spots. Bush's most polarized years were his fourth through seventh years in office, after the rally in support for him following the 9/11 terror attacks had faded. Clearly, political polarization has reached new heights in recent years, under a Republican and a Democratic president.

Bush's and Obama's approval ratings were most polarized along party lines in their fourth years in office -- which has been the case for most presidents because that is the year they seek re-election. Both Bush and Obama saw their polarization scores ease slightly in their fifth year, and go down a bit more in year six. Bush's polarization score dropped even further in his seventh year, as his overall job approval ratings continued to decline.

No Other Presidents' Sixth-Year Polarization Close to Bush's, Obama's

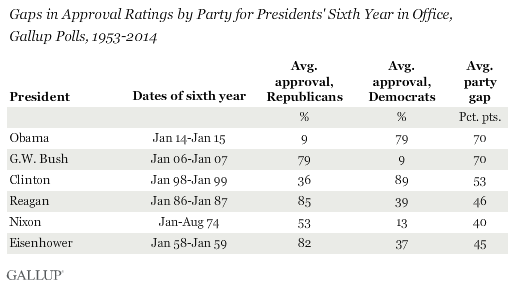

The structure of job approval in Obama's and Bush's sixth years in office was remarkably similar -- with 79% approval among supporters of the president's party, and 9% from supporters of the opposition party. Not surprisingly, Bush and Obama had by far the most polarized sixth years for presidents who served into a sixth year. In Bill Clinton's sixth year, there was an average 53-point gap in his approval ratings, 17 points lower than those of his immediate successors. Clinton's polarization score was a bit lower because his overall approval rating in year six, 64%, was much higher than Bush's (37%) or Obama's (43%). The other presidents serving into a sixth year had polarization scores below 50 points -- including Dwight Eisenhower and Ronald Reagan, who were popular at the time, and Richard Nixon, who had historically low approval ratings. Nixon resigned in August 1974, in the middle of his sixth year in office.

Obama on Pace to Have Most Polarized Approval Ratings