BUSINESS

& POLITICS IN THE WORLD

GLOBAL

OPINION REPORT NO. 665

Week: November

16 – November 22, 2020

Presentation: November 27, 2020

Worlwide

study shows Covid-19 is a long-term threat to women's physical and mental

health

Print Remains Most Important News Source For

Indian Readers: CVoter Survey

Japan sentiment toward China worsens for 1st

time in 4 years

In

spite of scrapped plans, one in seven Singaporeans are keen on a ‘flight to

nowhere’

Google remains Hong Kong’s healthiest brand

according to YouGov Best Brands 2020

Do

urban Arabs support gender equality to a greater extent than rural Arabs do?

Italians and savings, between uncertainty and

future plans

German consumers like Adidas again

Health Barometer # 1 - YouGov x 20 Minutes x

Doctissimo

Are workers with jobs disrupted by COVID-19

willing to retrain?

Four in ten gamers say they’ve played more

during COVID-19

Two in three NHS workers say lack of COVID

tests have caused staff shortages

U.S. Support for Death Penalty Holds Above

Majority Level

62% in U.S. Say Lives Not Yet Back to Pre-COVID

Normalcy

More Americans Now Willing to Get COVID-19

Vaccine

Sharp Divisions on Vote Counts, as Biden Gets

High Marks for His Post-Election Conduct

Banks show greatest improvement in YouGov

Australia’s Best Brands list

The pandemic accelerates the decline of cash

globally

Covid-19, a long-term threat to women's

physical and mental health

Majorities in the European Union Have Favorable

Views of the Bloc

INTRODUCTORY NOTE

665-43-23/Commentary:

Worlwide study shows

Covid-19 is a long-term threat to women's physical and mental health

Worldwide, more than 50 million people have contracted Covid-19. But the health cost to women goes far beyond the virus itself. AXA and Ipsos today reveal the results of a second study conducted among women on the impact of Covid-19.

The

first study,

published in October, focused on the economic impact of the pandemic. This

second part is devoted to women's health, to the immediate impact of the health

crisis on their physical and mental well-being but also to its longer-term

effects.

Women's physical and mental

health has suffered. They have struggled to access adequate health care; women

with chronic illnesses - such as cancer or diabetes - have fallen behind in

their treatment. And it is women living alone or on low incomes who have proved

to be the most vulnerable (...), according to report produced by AXA

"Hidden costs".

Key elements:

- Overall, women's

health has deteriorated during the crisis - the biggest

deterioration has been in Europe, where the pandemic has hit hardest. All

aspects of women's health have been affected: physical, mental and social.

More than two out of three women feel anxious or worried; more than half

report sleep disturbances.

- During the crisis, many women had difficulty

accessing health care - for financial reasons, lack of

availability or fear of contracting the virus.

- Among women with chronic illnesses, 60% had to postpone

their treatment. 40% were unable to see their doctor for regular follow-up

visits. Lack of access to routine health care could have long-term

consequences on women's health.

- Women are putting the health of others ahead of

their own more than before the pandemic. Despite this, the women interviewed also

found more time to take care of themselves by making the effort, for

example, to cook healthier meals for themselves and their families.

- With the pandemic far from over, women feel more

vulnerable to threats to their health. More than half fear isolation or

deterioration of their mental health. To help them manage these risks,

women expect faster and easier access to health care for themselves and

other family members in the future.

(Ipsos)

November 20, 2020

Source: https://www.ipsos.com/en/covid-19-long-term-threat-womens-physical-and-mental-health

SUMMARY

OF POLLS

ASIA

(India)

Print Remains Most Important News

Source For Indian Readers: CVoter Survey

In the age of digital

consumption, print remains "the most credible medium" for readers in

India. That's according to the recent CVoter Media

Consumption Survey 2020. The survey, which polled 5,000 respondents about their

consumption habits, found that audiences attribute higher credibility to

stories published in print media compared to television content — which has

been perceived as "superficial." (CVoter India)

November 23, 2020

(Japan)

Japan sentiment toward China

worsens for 1st time in 4 years

Negative sentiment

among Japanese toward China marked its first deterioration in four years with

nearly 90 percent of voters polled in a survey responding that they have an

unfavorable impression of the Asian superpower. The Japan-China opinion poll,

released Nov. 17 by Japanese nonprofit think tank Genron

NPO, also found that more Chinese view the bilateral

relationship as important, reflecting the impact of heightened U.S.-China

tensions and the COVID-19 pandemic. (The Asahi Shimbun)

November 18, 2020

(Sinagpore)

In spite of scrapped plans, one

in seven Singaporeans are keen on a ‘flight to nowhere’

The pandemic has hit

the global economy hard, but no industry was hit harder than the travel

industry. With planes grounded for the foreseeable future, Singapore Airlines

launched it’s ‘Inside Singapore Airlines’ experience. Latest YouGov data

reveals what Singaporeans think about their national carrier and their latest

offering of unique experiences. (YouGov)

November 20, 2020

(Hong Kong)

Google remains Hong Kong’s

healthiest brand according to YouGov Best Brands 2020

Google has topped

YouGov Best Brands list for the second year in a row, on YouGov’s annual

ranking of the healthiest brands in the nation. The rankings are based on the

Index score from YouGov BrandIndex, which constantly

measures overall brand health. The score takes into account consumers’

perception of a brand’s overall quality, value, impression, reputation,

satisfaction and whether consumers would recommend the brand to others. (YouGov)

November 18, 2020

MENA

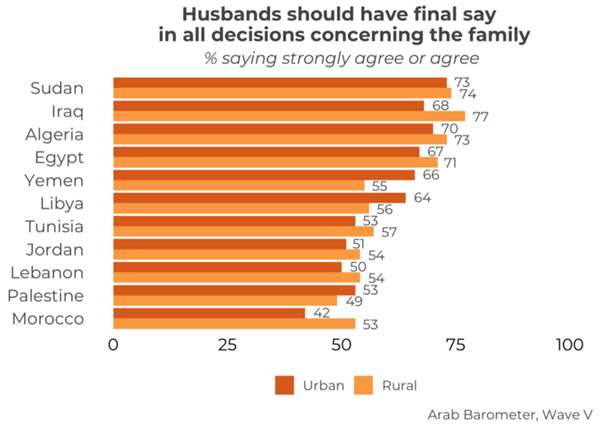

(Sudan)

Do urban Arabs support gender

equality to a greater extent than rural Arabs do?

Traditional perceptions

of gender roles continue to constrain women’s autonomy in household

decision-making. Data from the Arab Barometer’s fifth wave of surveys show that

60 percent of Arabs agree or strongly agree with the following statement, “Husbands should have final say in all decisions

concerning the family”. The proportions of citizens who agree with

husbands having final say, vary by country. Approval is highest in Sudan and

Algeria (74 and 71 percent, respectively), while somewhat lower in Lebanon and

Morocco (50 and 46 percent, respectively). (Arab

Barometer)

November 23, 2020

EUROPE

(Italy)

Italians and savings, between

uncertainty and future plans

Italians are very

prone to saving. In 2020, most people who have had any form of monetary income

(including subsidies, pensions, etc.) have set themselves the goal of saving

(76%).

The value of savings

is also felt by those who are unable to save: in fact, those who have not done

so mainly indicate the impossibility due to reduced earnings (51%) rather than

the lack of perception of its usefulness (for 3% of those who do not, saving

does not make sense). (YouGov)

November 18, 2020

(Germany)

German consumers like Adidas

again

In a YouGov ranking

of the world's best brands, several German brands make it into the top 25,

including Adidas, although the brand in Germany suffered severe damage to its

image due to the pandemic. The world's best German brand is Nivea. This is

shown by the YouGov 2020 Global Best Brand Ranking. The ranking is based on the

YouGov BrandIndex index score and considers the image

of several thousand brands in 33 markets. (YouGov)

November 23, 2020

(France)

Health Barometer # 1 - YouGov x

20 Minutes x Doctissimo

Overall, almost all

French people say they have complied with the rules related to confinement

(92%). In detail, the youngest say they have slightly less respected the rules

than their elders. Over the next two weeks, the trend will be the same

according to our survey. In fact, 9 out of 10 French people expect to respect

these rules (90%). Note, the youngest still stand out with once again a slight

dropout compared to their elders. With regard to preventive measures, almost

all French people say they respect them and even 56% apply them rigorously. (YouGov)

November 24, 2020

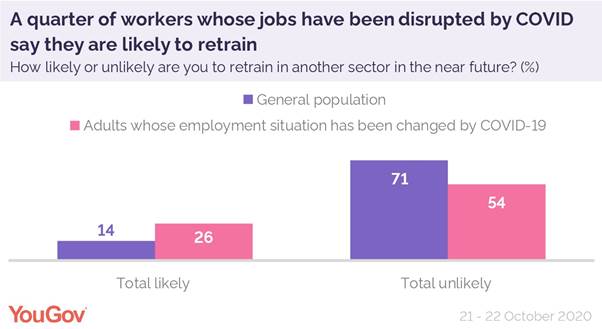

(UK)

Are workers with jobs disrupted

by COVID-19 willing to retrain?

The government has

faced criticism recently for suggesting that people in the arts sector who

cannot currently work because of coronavirus should consider finding a new

career. But how willing are people to take a new direction in their

professional lives? YouGov data reveals that coronavirus is currently impacting

one in seven (13%) workers’ employment status, either because they are

furloughed, experiencing a reduction in pay or hours, or have lost their job. (YouGov)

November 17, 2020

Four in ten gamers say they’ve

played more during COVID-19

More than four in ten

UK gamers say they’ve been gaming more during the COVID-19 outbreak (43%),

while a further four in ten have been gaming about the same (42%). Just 8% say

they’re playing less, a new YouGov white paper reveals. Additionally a quarter of gamers say that once

the pandemic is over, gaming will be “stronger and more relevant than ever

before” (24%). (YouGov)

November 18, 2020

Two in three NHS workers say lack

of COVID tests have caused staff shortages

The latest YouGov

polling of NHS workers – undertaken before the second national lockdown was

announced – finds that nearly two thirds (64%) say their workplace has been

affected by staff shortages because of lacking access to coronavirus tests. The

figures include one in nine (11%) who report being affected to a great extent,

one in three to some extent (29%) and a quarter to a small extent (24%). One in

five (19%) have not experienced any shortages. (YouGov)

November 20, 2020

NORTH AMERICA

U.S. Support for Death Penalty

Holds Above Majority Level

Americans' support for the death penalty

continues to be lower than at any point in nearly five decades. For a fourth

consecutive year, fewer than six in 10 Americans (55%) are in favor of the

death penalty for convicted murderers. Death penalty support has not been lower

since 1972, when 50% were in favor. 55% of Americans in 2020 are in favor of

and 43% opposed to the death penalty for persons convicted of murder. (Gallup

USA)

November 19, 2020

62% in U.S. Say Lives Not Yet

Back to Pre-COVID Normalcy

As COVID-19 cases were surging again across the

U.S. last month, more than six in 10 Americans said their lives had not

returned to pre-pandemic normalcy. Overall, 62% of Americans surveyed Oct.

19-Nov. 1 said their life right now is "not yet back to normal,"

while 34% said theirs is "somewhat back to normal" and 3% said

"completely" so. Among a host of key demographic subgroups,

Republicans are the most likely to say their lives have somewhat (59%) or

completely (8%) gotten back to what they were before COVID-19. (Gallup USA)

November 18, 2020

More Americans Now Willing to

Get COVID-19 Vaccine

Americans' willingness to be vaccinated against

COVID-19 rebounded a bit in October, as seen in Gallup polling conducted before

Pfizer/BioNTech and Moderna

made promising announcements about the likely effectiveness of their

coronavirus vaccines. Fifty-eight percent of Americans in the latest poll say

they would get a COVID-19 vaccine, up from a low of 50% in September. (Gallup

USA)

November 17, 2020

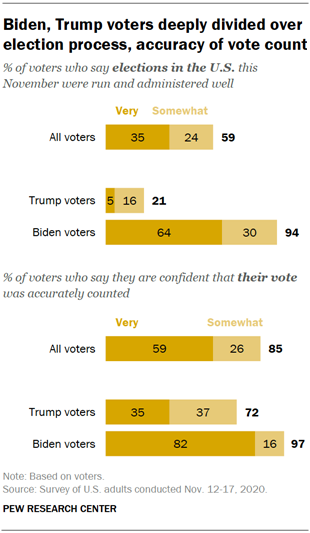

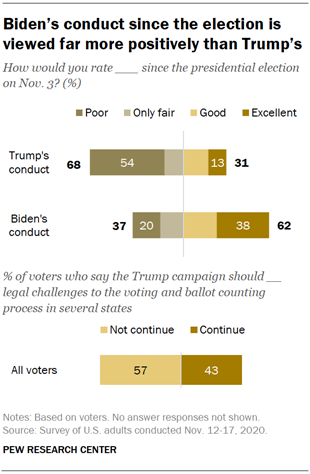

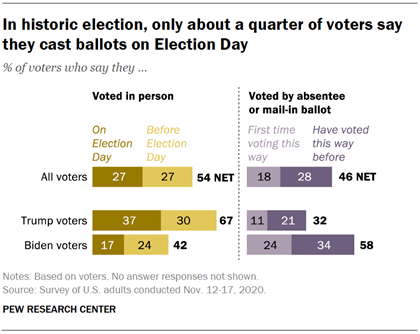

Sharp Divisions on Vote

Counts, as Biden Gets High Marks for His Post-Election Conduct

More than two weeks after the presidential

election, there are sharp divisions between voters who supported Joe Biden and

Donald Trump over nearly all aspects of the election and voting process,

including whether their own votes were counted accurately. Trump voters, who

already were skeptical of the electoral process and prospects for an accurate

vote count before the election in October, have become much more so since

Biden’s victory. (PEW)

November 20, 2020

AUSTRALIA

Banks show greatest

improvement in YouGov Australia’s Best Brands list

Google has topped YouGov Best Brands list for

the third year in a row, on YouGov’s annual ranking of the healthiest brands in

the nation. The rankings are based on the Index score from YouGov BrandIndex, which constantly measures overall brand health.

The score takes into account consumers’ perception of a brand’s overall

quality, value, impression, reputation, satisfaction and whether consumers

would recommend the brand to others. (YouGov)

November 18, 2020

MULTICOUNTRY STUDIES

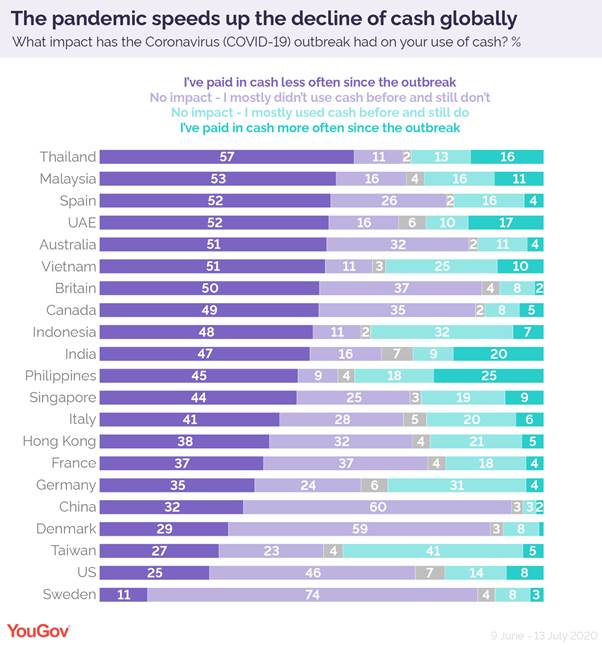

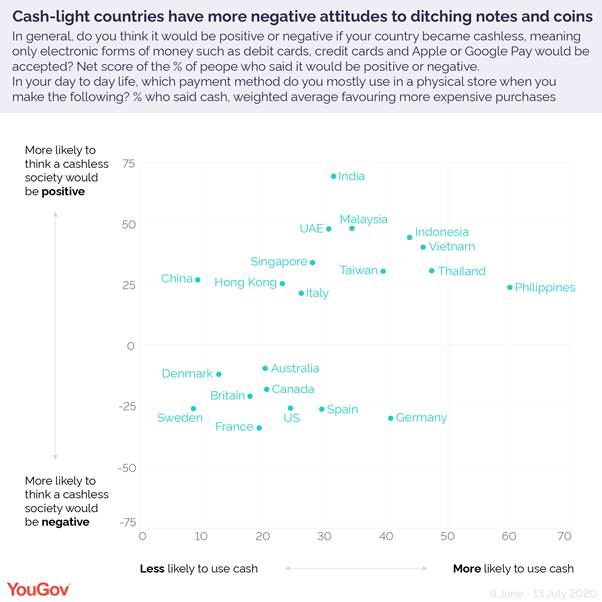

The pandemic accelerates the

decline of cash globally

A YouGov survey of 21 countries across four

continents suggests that the coronavirus pandemic has made many people limit

their use of cash in favour of electronic payments.

The data finds that Thailand has seen the largest decline in cash use. Over

half (57%) of the population has used coins and notes less often in the wake of

COVID-19, while one in six (16%) report they have used cash more frequently.

Only 11% of Thai people say they mostly didn’t use cash before the pandemic and

still don’t. (YouGov)

November 16, 2020

Covid-19, a long-term threat

to women's physical and mental health

Worldwide, more than 50 million people have

contracted Covid-19. But the health cost to women goes far beyond the virus

itself. AXA and Ipsos today reveal the results of a second study conducted

among women on the impact of Covid-19. The first study, published in October,

focused on the economic impact of the pandemic. This second part is devoted to

women's health, to the immediate impact of the health crisis on their physical

and mental well-being but also to its longer-term effects. (Ipsos)

November 20, 2020

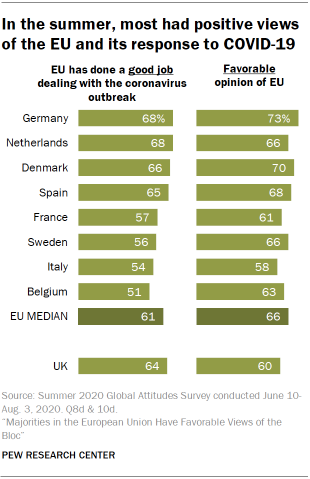

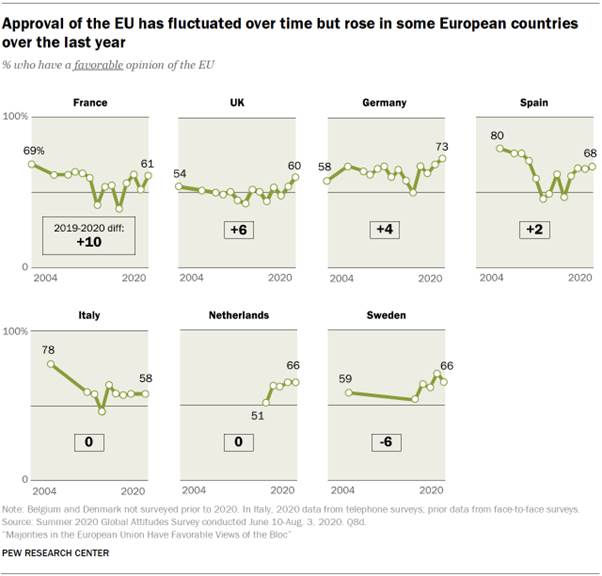

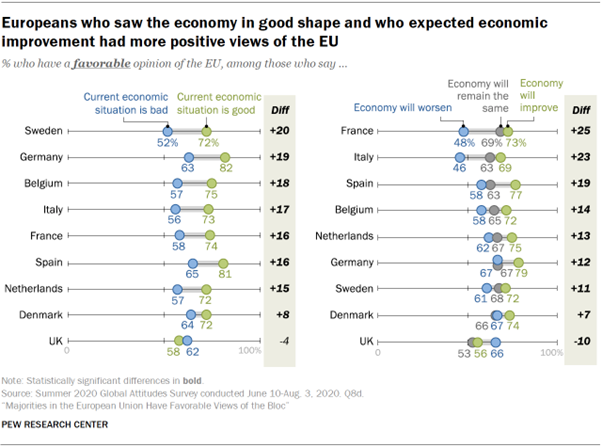

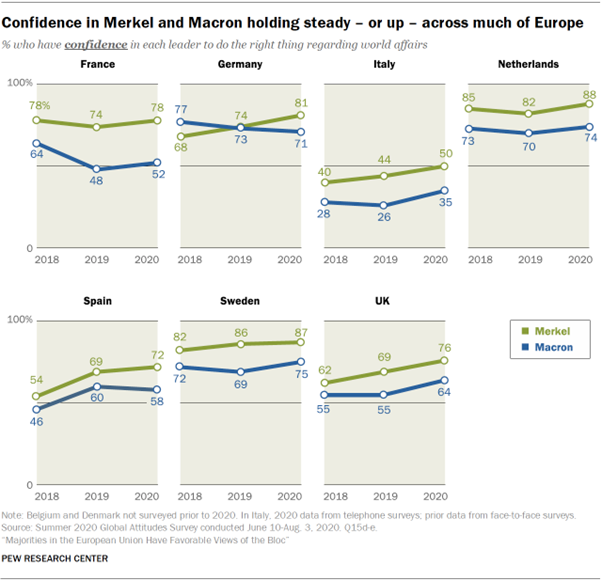

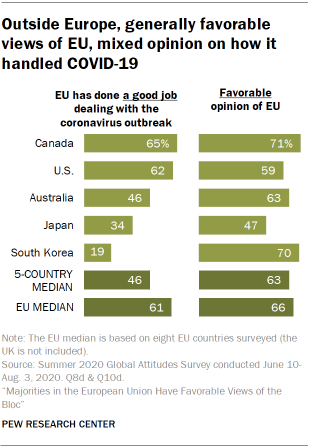

Majorities in the European

Union Have Favorable Views of the Bloc

Outside of China, Europe was home to some of

the first major coronavirus hotspots – as well as some of the most stringent

early national quarantine requirements to curb the spread. Results of a summer

survey – conducted before a second surge in cases began, in earnest, in

September – indicate that people in most European Union nations approved not

only of their national governments’ response to COVID-19, but also of how the

EU had handled the outbreak. (PEW)

November 17, 2020

ASIA

665-43-01/Poll

Print Remains Most Important News Source For Indian Readers:

CVoter Survey

In the age of digital consumption, print remains "the most credible

medium" for readers in India. That's according to the recent CVoter Media Consumption Survey 2020.

The survey, which polled 5,000 respondents about their consumption

habits, found that audiences attribute higher credibility to stories published

in print media compared to television content — which has been perceived as

"superficial."

Checking the latest updates

via print media has become a more important habit for many readers in India,

particularly now as the world grapples with the COVID-19 pandemic. The survey

found that readers fall back to what's safe and reliable; 63.2% of CVoter survey respondents said reading newspapers for

updates — including which of the COVID-19 vaccine candidates is the most

promising — have become even more important to them in the time of pandemic.

Meanwhile, over 75% of the survey respondents confirmed they prefer to check

the newspapers for news and current affairs rather than watch a "shouting

TV news debate," with 71.2% saying they have a favorite newspaper section

they read first thing every day. For many media watchers, news content on

television can be "superficial and trite" given its propensity for

sensationalism, frenzied debates, and biased reportage, according to the polls.

CVoter noted that 72.90% said newspaper reporting

"gives more information than the debate of TV news channels."

"As a content medium, TV grapples to cope with the meteoric growth of

digital entertainment. The 24-hours news cycle — that's a poor transition

between the old world of periodic bulletins and the advent of digital channels

- is to be partly blamed for TV not enjoying the preferred channel status of

Indian audiences anymore," the survey stated. Digital emerges as important

content consumption platform CVoter survey aside,

television is still poised to remain the world's favorite medium, according to

a 2019 Medium Consumption Forecast report by Zenith Media. Mobile internet,

however, will pose challenges for TV ahead — the report expects people around

the world will spend an average of 930 hours, or 39 full days.

Nationally, digital is considered an "important extension of conventional

news vehicles," CVoter survey found. Print and

digital "offer an ideal combination of reach and credibility," and

this goes beyond news reading. Particularly during the pandemic, the many

readers have been turning to technology not just to check out the news, but

also learn new skills and augment their reading materials on topics from

politics to health and lifestyle, or even learning how to play roulette and

other certain games online. A Deloitte report on "Digital media: Rise of

On-demand Content" also notes how mobile devices are driving the digital

consumption around the world — especially in India, where the internet user

base is growing at a rapid rate. It explained: "India has the largest

young population in the world which is driving the digital media consumption in

India. Internet traffic in India is being driven by mobile internet users. The

major reason for this will be the availability of cost efficient smartphones in

India, improving 3G and 4G internet coverage and fast reducing data

prices."

(CVoter India)

November 23, 2020

665-43-02/Poll

Japan sentiment toward China worsens for 1st time in 4 years

Negative sentiment among Japanese toward China marked its first

deterioration in four years with nearly 90 percent of voters polled in a survey

responding that they have an unfavorable impression of the Asian superpower.

The Japan-China opinion poll, released Nov. 17 by Japanese nonprofit

think tank Genron NPO, also found that more Chinese view the bilateral

relationship as important, reflecting the impact of heightened U.S.-China

tensions and the COVID-19 pandemic.

The annual opinion poll started in 2005. The latest survey was carried

out in September and October with valid responses received from 1,000 Japanese

and 1,571 Chinese.

Of Japanese respondents, 89.7 percent said they have an “unfavorable” or

“somewhat unfavorable” impression of China, up 5 percentage points from a year

earlier. That marks the first time Japanese sentiment toward China has worsened

since 2016.

More respondents cited China’s behavior in the international arena and

its military buildup as reasons in the latest survey. Rising tensions between

the United States and China, as well as issues affecting Hong Kong, apparently

put a damper on Japanese views toward China.

(The Asahi Shimbun)

November 18, 2020

Source:

http://www.asahi.com/ajw/articles/13941132

665-43-03/Poll

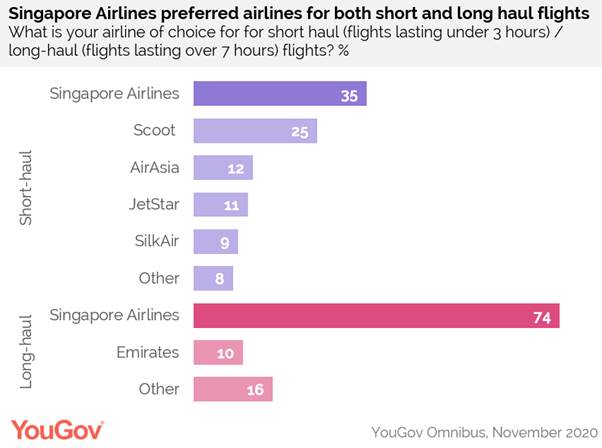

In spite of scrapped plans, one in seven Singaporeans are keen on a ‘flight to nowhere’

The pandemic has hit the

global economy hard, but no industry was hit harder than the travel industry.

With planes grounded for the foreseeable future, Singapore Airlines launched

it’s ‘Inside Singapore Airlines’ experience. Latest YouGov data reveals what

Singaporeans think about their national carrier and their latest offering of

unique experiences.

Whether short-haul or

long-haul flights, Singapore Airline is the preferred airlines amongst

Singaporeans. For short-haul flights (flights under 3 hours), over a third

(35%) picked Singapore Airlines as their preferred airline, followed by

Singapore Airlines subsidiary Scoot (25%), AirAsia (12%), and JetStar (11%). When

it comes to long-haul flights (flights over 7 hours), Singapore Airlines is the

clear winner, with three-quarters (74%) saying it is their top choice.

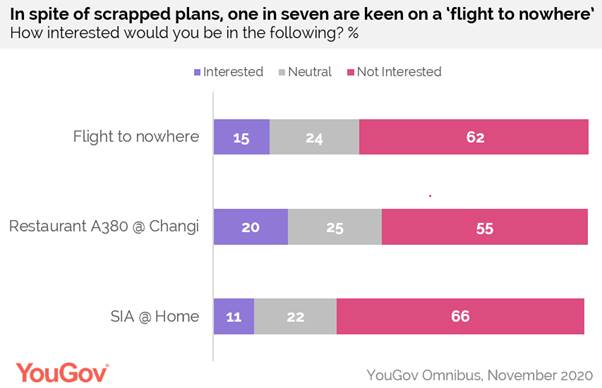

As an attempt to boost

grounded passenger business, Singapore Airline unveiled plans in September this

year to launch a ‘flight to nowhere’ with trips that start and end at the same

airport. Though the plan was eventually scrapped after criticism about the

environment impact, one in seven (15%) of Singaporeans are interested in a

‘flight to nowhere’. Frequent flyers (which we termed by those who took more

than five flights last year) are most likely to be interested in a flight to

nowhere, compared to those who took zero flights last year (21% vs. 8%).

High-income earners (household income of more than RM 8,000) are also much more

likely to be keen on a flight without a destination than low-income earners

(household income of less than RM 2,999).

In October 2020, Singapore

Airlines announced the launch of Restaurant A380 @ Changi – a dining experience

aboard a parked A380 plane at Changi Airport, with tickets selling out in

thirty minutes. Although the experience was limited to two weekends and there

has not been an announcement for a third sitting, one in five (20%)

Singaporeans remain interested in the experience. A quarter (25%) have no

opinion, and a third (33%) are uninterested.

Alongside Restaurant A380 @

Changi, Singapore Airlines also launched SIA @ Home – where business class or

first class meals are delivered to the home, alongside tableware and flight

amenities. Compared to the restaurant, less Singaporeans are keen on dining on

airplane fare at home – only one in ten (11%) are interested in this

experience. However, amongst those who profess to ‘love’ / ‘like’ airplane food

(35% of the population) interest in this experience jumps to over a quarter

(27%).

Rounding off the ‘Inside

Singapore Airlines’ experience is a behind-the-scenes tour of the training

centre, including various add-ons. Of all the add-on experience, the flight

simulator is the most popular, with half (48%) interested in it. The second

most popular experience is the training centre tour (33%), followed by the

junior pilot experience (32%), grooming workshop (22%), wine tasting and junior

cabin crew experience (both 20%). A third (33%) of Singaporeans have no

interest in any of the experiences.

(YouGov)

November 20, 2020

Source: https://sg.yougov.com/en-sg/news/2020/11/20/spite-scrapped-plans-one-seven-singaporeans-are-ke/

665-43-04/Poll

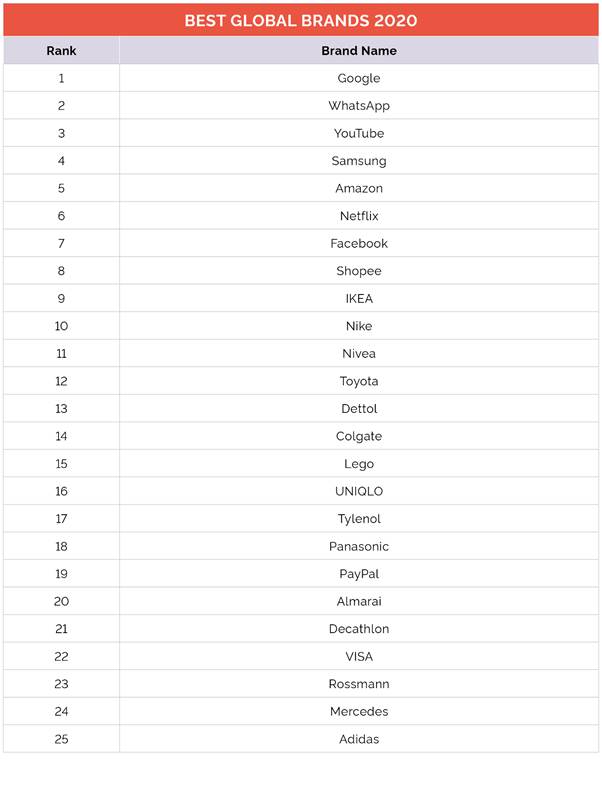

Google remains Hong Kong’s healthiest

brand according to YouGov Best Brands 2020

Google has topped YouGov

Best Brands list for the second year in a row, on YouGov’s annual ranking of

the healthiest brands in the nation. The rankings are based on the Index score

from YouGov BrandIndex, which constantly measures overall brand

health. The score takes into account consumers’ perception of a

brand’s overall quality, value, impression, reputation, satisfaction and

whether consumers would recommend the brand to others.

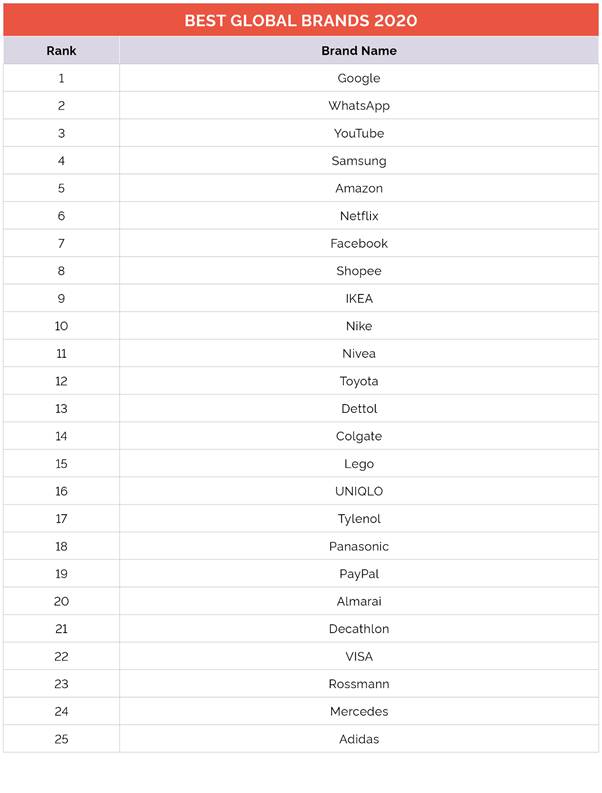

Google is not only the

healthiest brand in Hong Kong (+36.1), it is also the brand with the highest

Index score globally. Instant messaging platform WhatsApp hold its position in

second place (+35.7). Other brands familiar to the top ten are multinational

financial services provider VISA in fifth (+32.2), and Japanese clothing

retailer Uniqlo in sixth (+31.1) – both falling two spots from last year. Video

sharing platform YouTube and luxury watchmaker Rolex hold their positions in

seventh (+29.1) and eighth (+27.7) respectively.

This year’s rankings sees a

number of new entrants from various industries. Public transport provider KMB

comes in strong in third (+33.1), local e-commerce platform HKTVmall in fourth

(+32.5), sports apparel retailer Nike in eighth (+26.9) and tech conglomerate

Apple in tenth (+26.1).

YouGov BrandIndex also

reveals the brands that have noted the greatest improvement to their

Index score over the past 12 months in Hong Kong. Subscription

video-on-demand service Netflix comes up on top with an increase in score of

+7.1. Skincare brand Sebamed comes in second (up +5.6) and supermarket chain

PARKnSHOP in third (up +4.8).

The improvers list is

populated with brands from various industries. Healthcare chain Watsons is in

fourth (up +4.5), local fast-food chain Fairwood in fifth (up +3.9), Apple in

sixth (up +3.6), telecommunications provider i-CABLE in seventh (up +3.0) and

insurance provider Manulife in ninth (up +2.7).

Luxury brands have also

shown great improvement in this year’s list. Louis Vuitton in eighth (up +2.9)

and Hermès in tenth (up +2.4).

Cindy Chan, General Manager

at YouGov Greater China commented: “With businesses hit hard by the pandemic,

consumers have looked to big corporations and organisation to respond

accordingly. Google has done just that, committing $100 million and technical

expertise to the global COVID-19 response. The brand’s efforts sees it holding

its spot as Hong Kong’s healthiest brand.”

Global

Rankings

Google takes the top spot in

YouGov’s annual global best brands ranking. Tech brands dominate the top of the

list with the search and advertising giant followed by WhatsApp, YouTube,

Samsung and Amazon.

With Netflix and Facebook in

sixth and seventh respectively, the only non-tech-related brands in the top ten

are Singaporean ecommerce platform Shopee (eighth), Swedish retailer IKEA

(ninth) and US sportswear titan Nike (tenth).

(YouGov)

November 18, 2020

Source: https://hk.yougov.com/en-hk/news/2020/11/18/google-remains-hong-kongs-healthiest-brand-accordi/

MENA

665-43-05/Poll

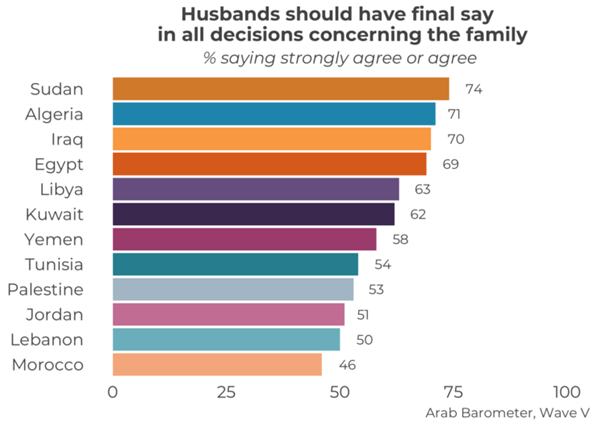

Do urban Arabs support gender equality to a greater extent than rural Arabs do?

Traditional perceptions of gender roles continue to constrain women’s

autonomy in household decision-making. Data from the Arab Barometer’s fifth

wave of surveys show that 60 percent of Arabs agree or strongly agree with the

following statement, “Husbands should

have final say in all decisions concerning the family”. The

proportions of citizens who agree with husbands having final say, vary by

country. Approval is highest in Sudan and Algeria (74 and 71 percent,

respectively), while somewhat lower in Lebanon and Morocco (50 and 46 percent,

respectively). Beyond such country-level differences, are there

individual-level predictors that can account for some of the variance seen in

citizens’ support for gender equality across the Arab world?

Previously, I

have argued that socioeconomic development and attitudes towards gender

equality are positively correlated. As the economy grows, living conditions

improve and education levels rise. People also experience a greater sense of

human autonomy that brings demands for gender equality. However, value shifts

do not occur evenly distributed in the entire society. Rather, different social

groups have different values. In liberal democracies, for example, highly

educated urban women have been at the forefront of the women’s rights movement.

Hence, settlement type has often been used to explain variations in support for

gender equality. This raises the question as to whether there is a similar

rural-urban divide in the Arab World.

The evidence from the Arab world does not support this hypothesis.

Instead, findings from eleven Arab countries suggest that urban Arabs do not

support gender equality to a greater extent than their rural counterparts do.

Only in Morocco and Iraq does a rural-urban divide exist in support on gender

equality, in which urban citizens are more liberal on gender equality. In

Yemen, in contrast, the urban population is even more conservative on gender

equality than the rural population.

Urbanization and gender equality

Socioeconomic development has historically had important implications on

patterns of human settlement. Industrialization led to large-scale migration to

urban centers, creating new social classes, such as the bourgeoisie and the

working-class, whose values were different to those of traditional classes,

represented by landowners and peasants. Changes in the social structure were

accompanied by a shift from traditional religious values to rational-secular

values. As the old social hierarchy deteriorated, people were no longer subject

to traditional social roles and ties, bringing demands for greater autonomy.

Simple proportions show that a slightly higher share of rural citizens

agree with the husband’s privileged role in household decision-making, compared

to their urban counterparts (63 versus 59 percent, respectively). Though these

simple proportions show a correlation between respondents’ settlement type and

support for gender equality, this analysis suggests that such a trend could be

due to the effects of confounding variables like education. The uncontrolled

model with settlement type as a single variable shows statistically significant

coefficients for six countries. However, when controlling for education, only

three countries remain statistically significant.

Two countries show a rural-urban divide similar to the one in liberal

democracies. Urban Iraqis and Moroccans are – respectively 30% and 21% – less

likely to agree with traditional household decision-making, compared to their

rural counterparts. In Yemen, in contrast, the relationship goes into the

opposite direction. Urban Yemenites are 40% more likely to agree with the

husband’s privileged role. Given these results, urban centers in some Arab

countries are more liberal on gender equality due to the higher concentration

of highly educated people in those areas.

Further explanations

These findings suggest that there is no rural-urban divide on gender

equality in most Arab countries. One explanation for these findings may have to

do with the different

types of urbanization. In most western

countries, urbanization was the byproduct of industrialization. In the Middle

East, in contrast, urbanization started before the advent of industrialization,

when society was still predominantly agrarian. As a result, cities were rather

administrative, cultural and commercial centers. Without the social

transformation triggered by industrialization, people kept their interwoven

network and social ties from traditional society.

However, Arab economies have grown dramatically in the recent decades, so

one should see a rural-urban divide on gender equality in the next decades if

the underlying mechanism is valid outside a Western context. For example,

different levels of socioeconomic development might explain why the

relationship goes into the diametrically opposed direction in Yemen, being

one of the poorest countries in the world.

Further research is required to analyze the relationship between socioeconomic

development, different types of urbanization, and their impact on gender

values.

(Arab Barometer)

November 23, 2020

EUROPE

665-43-06/Poll

Italians and savings,

between uncertainty and future plans

Italians are very prone to saving. In 2020, most people who have had any form of

monetary income (including subsidies, pensions, etc.) have set themselves the goal of saving (76%).

The value of savings is also felt by those who are

unable to save: in fact, those who have not done so mainly indicate the

impossibility due to reduced

earnings (51%) rather than the lack of perception of its

usefulness (for 3% of those who do not, saving does not make sense).

While nearly a quarter of savers don't have a

strategy, putting aside what's left of

what they earn after making all the necessary expenses (23%), most people have

a personal way to save.

Almost half (48%) regularly check their balance and keep track of expenses . Others,

on the other hand, impose more concrete limitations, such as monthly budgets to be followed (35%),

or the transfer of the sums to be saved

to a different account .

The trend for 2021 is even more upward due to the uncertain period

In fact, if a third of those who have already saved

this year (33%) intend to continue next

year , more than half (56%) want to save even more .

Even among those who did not want to or could not in

2020, over a third (35%) plan to start

saving next year .

Having an emergency

fund is the number one reason to save next year (45%), and the

pandemic plays a big part in that. More than one in three people (34%)

feel they have to save to be ready for the eventuality of changes in their employment status (such

as job loss, but also reduced hours, or layoffs) or in general for lockdowns and due closures at

Covid-19.

Those just mentioned are the first three most cited

reasons in order of importance; but the uncertainty of the current period

is not the only incentive for saving. In addition to the more traditional

reasons, such as children (30%)

or large expenses (eg

for the home, 26%, or car - 13%), one in five, despite the restrictions of

current movements, plan on saving for

view of the possibility of starting to travel again in the

future (19%).

Almost a

quarter of Italians save without a specific reason (24%).

What do Italians do to save? The first strategy

is to limit food waste ,

mentioned by 58%, along with the renunciation

of take-away food / eating out indicated by 41%. On a par

with the balances ,

expected by many before buying the

products they need (57%). Not a few, on the other

hand, completely renounce and reduce the frequency of purchase of certain

products (45%) or services (31%).

(YouGov)

November 18, 2020

Source: https://it.yougov.com/news/2020/11/18/risparmio/

665-43-07/Poll

German consumers like Adidas

again

In a YouGov

ranking of the world's best brands, several German brands make it into the top

25, including Adidas, although the brand in Germany suffered severe damage to

its image due to the pandemic.

The world's best German brand is Nivea . This is shown by the

YouGov 2020 Global Best Brand Ranking. The ranking is based on the YouGov BrandIndex index

score and considers the image of several thousand brands in 33

markets. In around eight million online interviews, consumers answered

questions about quality, customer satisfaction, value for money and other

image-relevant dimensions. At the top: global digital brands such as Google , WhatsApp, Youtube and Samsung , followed by Amazon , Netflix and Facebook . In addition to Nivea, there are also German brandsRossmann , Mercedes and Adidas represented in the top 25.

NIKE AND DECATHLON STRONGER

INTERNATIONALLY

While the online and e-commerce companies at the top

were strengthened by the pandemic, Adidas lost points due to the corona. We collected the data from

October 2019 to September 2020 and in the middle of this period Adidas caused

negative headlines because the company decided during the uncertainty at the

beginning of the crisis not to pay rents for forcibly closed shops or to want

to pay hours. We analyzed the loss of

image measured in

our brand monitor BrandIndex

in more detail in mid-April. A few days later, our score for Adidas hit its low point: 24 points (on

a scale from 100 to -100) below the value on April 24th. At the beginning of March

the value was 39.

For several months, the reputation of Adidas from the

perspective of German consumers was comparable to that of Nike . The

gap to Puma was now only a few points. Usually

Adidas is many points ahead of the competition in Germany , although the Global Best Brand Ranking clearly shows how much

the Nike brand is internationally stronger: The US sporting goods manufacturer

is in 10th place, Adidas in 25th place. Decathlon is in between (21st place).

BUYING INTEREST

SUFFERED TOO

Most of the Adidas customers do not feel bound to the

brand. A target group analysis with YouGov Profiles shows that Puma is an option for

almost a third of Adidas customers . Almost half can imagine buying

Nike products. On the other hand, Profiles data also suggests that Adidas

customers are picky. 61 percent of them say they prefer to buy certain

brands - compared to just 42 percent of the general population. Whoever

wears Adidas says they are asked more often for advice when it comes to

clothing.

This is likely to have contributed to the fact that,

in parallel to the general impression of the brand, the willingness to

recommend, measured in the BrandIndex, fell sharply in March and

April. Recently, however, this score has also returned to a normal

level. Adidas can therefore hope to gain a few points in the next Global

Best Brand Ranking.

(YouGov)

November 23, 2020

Source: https://yougov.de/news/2020/11/23/die-deutschen-verbraucher-mogen-adidas-wieder/

665-43-08/Poll

Health Barometer # 1 -

YouGov x 20 Minutes x Doctissimo

Overall, almost

all French people say they have complied with the rules related to confinement

(92%). In detail,

the youngest say they have slightly less respected the rules than their

elders. Over the next two weeks, the

trend will be the same according to our survey. In fact, 9 out

of 10 French people expect to respect these rules (90%). Note, the

youngest still stand out with once again a slight dropout compared to their

elders. With regard to preventive

measures, almost all French people say they respect them and even 56% apply

them rigorously.In detail, the French say they respect in mind the

fact of banning festive gatherings (95%), the fact of washing hands (94%) or

the fact of greeting without shaking hands and stopping hugs. (93%). Once

again, compliance with these measures seems more difficult for the youngest.

The level of

knowledge of the French with regard to COVID-19

A little more

than 6 out of 10 French people still consider a "good" level of

knowledge regarding the COVID-19 virus (61% vs. 5% finding it on the

contrary "bad"). It should be noted that 34% believe they have a

level of knowledge "neither good nor bad". In addition, the level of knowledge relating to the means to

protect oneself is significantly higher (82%). We always note a

slight dropout of the youngest. Despite everything, more than half of

French people are looking for information about the virus and how to protect

themselves from it (52%).

The habits of

the French during this period

One in two

French people say they pay more attention to their diet in order to protect

themselves from possible contamination (50%) but less than half of French people say

they have practiced regular physical activity over the past two

weeks. Finally, more than half of French people say that the current

context has a negative impact on their morale (52%).

Note that nearly

one in five French people say they avoid or have even canceled one or more

medical appointments for fear of contracting the COVID-19 virus (19%).

The “Tous

Anti-Covid” application, a modest success

Less than one in three French people say they have

downloaded the “Tous Anti-Covid” application (30%). We note that a little

more than half of them only use it to generate a certificate. In detail,

8% of these users reported a contact case and 6% say they have been reported a

contact case.

The French and

the arrival of a vaccine against COVID-19

Only 34% of

French people say they would get vaccinated as soon as possible if

a vaccine were to be put on the market soon. Of those who do not want to do it as soon as

possible, 36% still consider doing it after several months. Note all the

same that a quarter of the French population says it is refractory to this

vaccine. In fact, less than half of French people believe that it should

be made compulsory (47%).

(YouGov)

November 24, 2020

Source: https://fr.yougov.com/news/2020/11/24/barometre-de-la-sante-20-minutes-doctissimo/

665-43-09/Poll

Are workers with jobs

disrupted by COVID-19 willing to retrain?

Britons tend to

think the government should focus on supporting struggling industries rather

than encouraging workers to find new careers

The government has faced criticism recently for

suggesting that people in the arts sector who cannot currently work because of

coronavirus should consider finding a new career.

But how willing are people to take a new direction in

their professional lives? YouGov data reveals that coronavirus is currently

impacting one in seven (13%) workers’ employment status, either because they

are furloughed, experiencing a reduction in pay or hours, or have lost their

job.

Of these workers, a quarter (26%) say they are likely

to retrain in another sector in the near future.

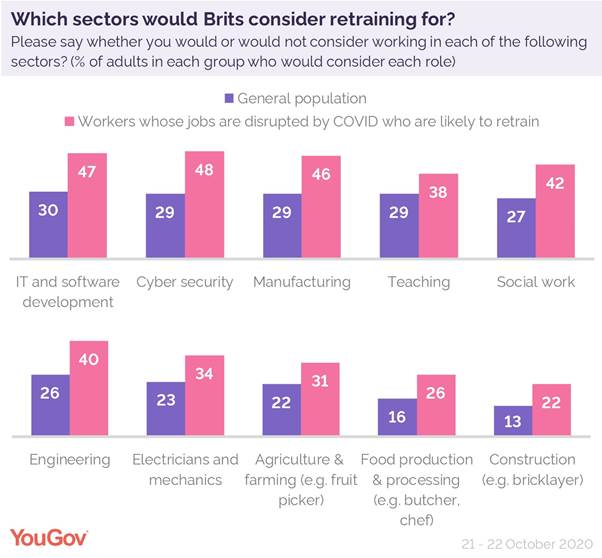

As part of their attempt to help people into new

careers, the government launched a new retraining quiz to allow workers to see what kinds of work they might enjoy. We

asked Britons about 11 lines of work that have been reported as experiencing

shortages, as well as some of those which appear in the Shortage Occupation

List 2020, and asked whether they would consider working in each.

Overall the most popular jobs are IT and software

development (30% would consider this), cyber security, manufacturing and

teaching (each with 29%).

The least popular jobs are in construction, which only

13% would consider, and food production (16%).

This is replicated when looking specifically at those

who would be likely to retrain in the near future. IT and software

development and cyber security are again most popular (48% and 47%

respectively), whilst potential retrainees would be least likely to consider a

job in construction (22%) and food production (26%).

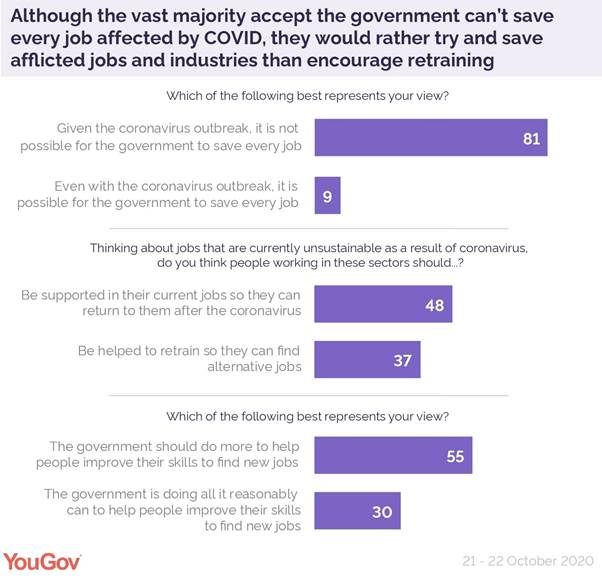

Despite the criticism in some quarters about the

government’s stance that workers should retrain, a clear majority (81%)

acknowledge that it is not possible for the government to save every job during

the coronavirus crisis.

That being said, half of Britons (48%) tend to think

that people working in sectors impacted by coronavirus should be supported in

their present jobs so that they can return to them when things go back to

normal. Just over a third (37%) think they should instead be helped with

retraining to find alternative jobs.

When it comes to actually supporting people to

retrain, however, most Britons (55%) think the government is not doing as much

as it should be to help people improve their skills or find new jobs.

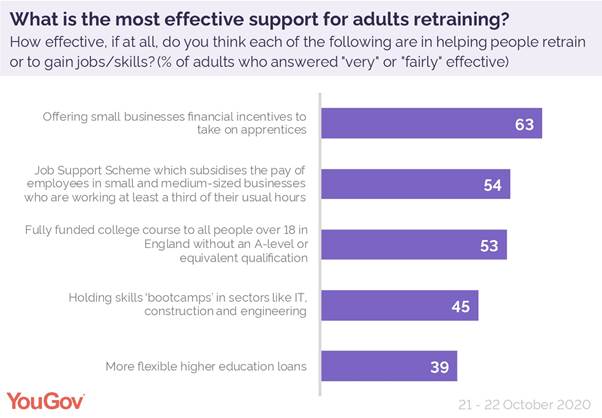

In terms of what they think the government could do on

retraining that would help most, almost two thirds (63%) think offering small

businesses financial incentives to take on apprentices would be effective,

whilst just over half (54%) think the same of the postponed Job Support. A

similar proportion (53%) think government proposals to offer English adults

without A-levels a fully funded college course would be effective in boosting

retraining.

(YouGov)

November 17, 2020

Source: https://yougov.co.uk/topics/politics/articles-reports/2020/11/17/workers-retrain-covid

665-43-10/Poll

Four in ten gamers say

they’ve played more during COVID-19

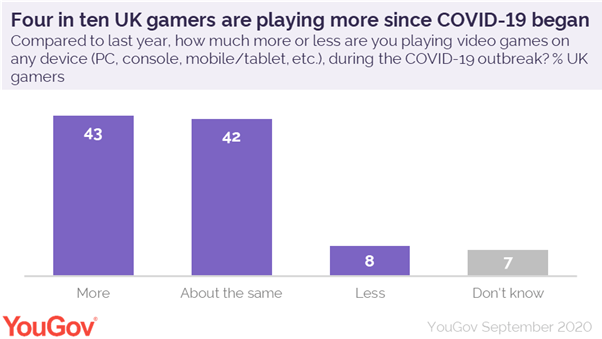

More than four in ten UK gamers say they’ve been

gaming more during the COVID-19 outbreak (43%), while a further four in ten

have been gaming about the same (42%). Just 8% say they’re playing less, a new YouGov white paper reveals.

Additionally a quarter of gamers say that once the

pandemic is over, gaming will be “stronger and more relevant than ever before”

(24%).

The data comes from YouGov’s Gaming and esports: The Next

Generation white

paper, which provides an analysis of the global video games and esports

landscape across 24 markets.

UK gamers make up over two thirds of the population

(67%); six in ten of this group say they play mobile games (52%); a quarter PC

games (25%); and three in ten console games (28%).

Mobile gamers are the most significant consumer group

worldwide, outnumbering console and PC gamers in every market, particularly in

South and South East Asia. In Thailand, just 12% play on consoles compared to

78% who use a smartphone or tablet; in India, the proportion is 12% vs.

67%.

In contrast, the leading markets for console gamers as

a proportion of the population are Hong Kong (32%), Spain (29%), the US (28%),

the UK (28%), and Australia (27%). When it comes to new consoles, a fifth

of gamers say they’re likely to buy Sony’s PlayStation 5 in the 12 months after

its launch (19%) while one in ten are likely to buy Microsoft’s Xbox Series X

(11%).

In the last decade game streaming has developed its

own subculture online and has grown a following among British gamers. Twitch

awareness among UK gamers is at 37%, while a quarter are aware of YouTube

Gaming (25%) and one in six are aware of Facebook Gaming (16%).

When it comes to esports, although four in ten Brits

(37%) are familiar with the industry engagement is relatively low. Just 6% of

Brits are engaged with these competitions in some way. The majority of those

who engage with esports are casual fans (61%) with just 5% saying they are passionately

interested.

(YouGov)

November 18, 2020

Source: https://yougov.co.uk/topics/technology/articles-reports/2020/11/18/gamers-play-more-during-covid

665-43-11/Poll

Two in three NHS workers say

lack of COVID tests have caused staff shortages

Nearly nine out

of ten also report normal services being disrupted and an even higher

proportion are anxious about the impact on non-COVID patients

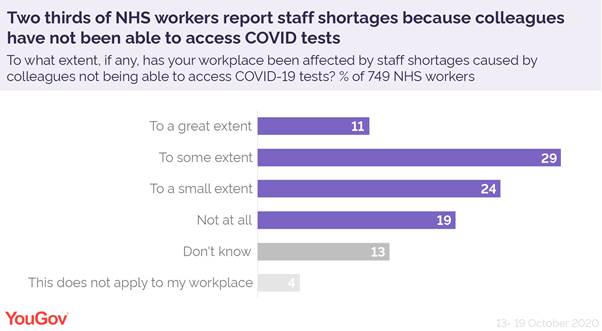

The latest YouGov polling of NHS workers – undertaken

before the second national lockdown was announced – finds that nearly two

thirds (64%) say their workplace has been affected by staff shortages because

of lacking access to coronavirus tests.

The figures include one in nine (11%) who report being

affected to a great extent, one in three to some extent (29%) and a quarter to

a small extent (24%). One in five (19%) have not experienced any shortages.

Nearly half (47%) of NHS employees who work with

admitted patients also say that access to COVID tests has delayed the discharge

of patients. This comprises 7% who report it impacting to a great extent, a

quarter (26%) to some and one in seven (14%) to a small extent. Just under a

quarter (23%) say there’s not been any delay to discharges, while three in ten

are unsure (30%).

The data also shows that about a quarter of NHS

workers (23%) have requested a coronavirus test. Of these, most say it was

either very (43%) or fairly (36%) easy to get one but about a fifth said it was

either very (8%) or fairly (11%) hard to access a test.

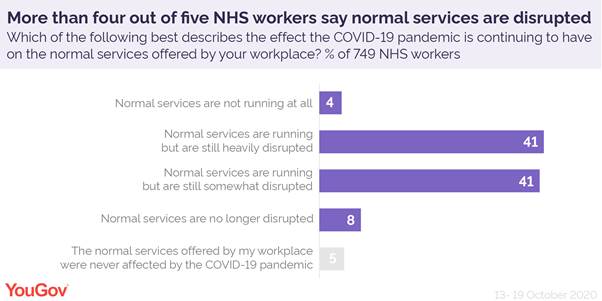

More than four

out of five report disruption to normal services

Most NHS workers (86%) say the normal services their

workplace offers are currently disrupted. Four out of five say they’re either

somewhat (41%) or heavily hampered (41%), while another 4% say they’re not

running at all.

Only a small proportion of NHS workers say the

services their workplace offers haven’t been affected (5%) or are no longer

disrupted (8%) by the pandemic.

The ongoing coronavirus outbreak also contributes to

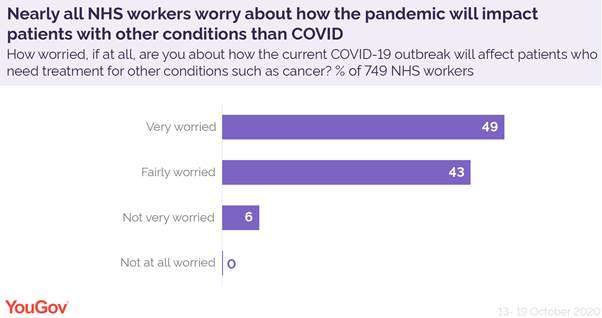

heightened anxiety about patients with other conditions such as cancer. Half of

NHS workers (49%) say they’re very worried

about how the current COVID outbreak will impact these patients, while another

two in five (43%) are fairly worried.

Only 6% say they’re not very worried while the NHS

workers who are not at all worried make up less than 1%.

(YouGov)

November 20, 2020

NORTH AMERICA

665-43-12/Poll

U.S. Support for Death

Penalty Holds Above Majority Level

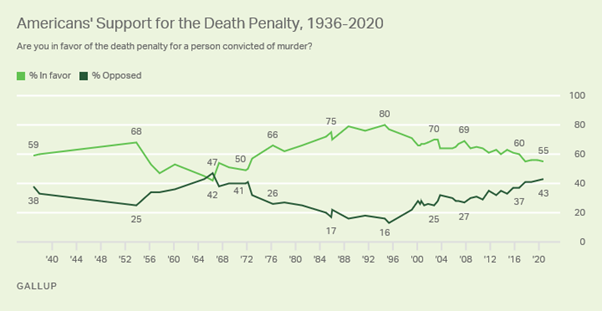

Americans' support for the death penalty continues to

be lower than at any point in nearly five decades. For a fourth consecutive

year, fewer than six in 10 Americans (55%) are in favor of the death penalty

for convicted murderers. Death penalty support has not been lower since 1972,

when 50% were in favor.

Line graph. 55% of Americans in 2020 are in favor of

and 43% opposed to the death penalty for persons convicted of murder.

Gallup has asked Americans whether they are "in

favor of the death penalty for a person convicted of murder" since 1936,

when 58% said they were. In all but one survey -- in 1966 -- more Americans

have been in favor than opposed. The 1960s and early 1970s brought many legal

challenges to the death penalty, culminating in a 1972 U.S. Supreme Court

ruling that invalidated state death penalty statutes. After the high court

upheld revised state death penalty laws in 1976, support for capital punishment

grew, peaking at 80% in 1994, a time of heightened public concern about crime.

This year's results are based on a Sept. 30-Oct. 15

survey. Gallup occasionally asks another question to gauge death penalty

support, with respondents indicating whether they believe the better punishment

for murder is the death penalty or life imprisonment with no possibility of

parole. In the most recent update, from 2019, Americans favored life imprisonment over the

death penalty by

60% to 36%, a dramatic shift from prior years.

Many Americans are thus conflicted on the death

penalty. The two Gallup trend questions indicate that about one in five

Americans express theoretical support for use of the death penalty but believe

life imprisonment is a better way to punish convicted murderers.

Republican

Support for Death Penalty Remains High

Gallup began asking its historical death penalty trend

question in its annual Crime survey beginning in 2000. During this time, there

have been two notable shifts in death penalty attitudes. Between 2011 and 2016,

the percentage expressing support showed a drop to 61% from 66% in the

preceding decade. In the past four years, support has fallen further to an

average 56%.

Both Democrats and independents show declines in their

support for the death penalty, including similar drops (eight and seven

percentage points, respectively) since 2016. Between the 2000-2010 and

2011-2016 time periods, Democratic support dropped more (eight points) than

independent support did (three points).

Now, 39% of Democrats and 54% of independents are in

favor of the death penalty.

Meanwhile, Republicans' support for the death penalty

has held steady, with 79% currently supporting it, unchanged since 2016 and

barely lower than the 80% registered between 2000 and 2010.

Changes in Support for the Death Penalty, by Political

Party

Figures are the percentage who say they are in favor

of the death penalty for a person convicted of murder

|

2000-2010 |

2011-2016 |

2017-2020 |

Change since 2011-2016 |

|

|

% |

% |

% |

pct. pts. |

|

|

U.S. adults |

66 |

61 |

56 |

-5 |

|

Republicans |

80 |

79 |

79 |

0 |

|

Independents |

64 |

61 |

54 |

-7 |

|

Democrats |

55 |

47 |

39 |

-8 |

|

GALLUP |

||||

Demographic

Trends May Lead to Further Erosion in Death Penalty Support

Changes in the U.S. population appear to be a factor

in declining death penalty support in recent years. Groups that are

constituting a greater share of the U.S. adult population over time --

including millennials and Generation Z, non-White adults and college graduates

-- all show below-average support for the death penalty.

- Over the past four years, an average of 45% of those in

Generation Z (those born after 1996) have favored the death penalty, as

have 51% of millennials (those born between 1980 and 1996). That compares

with 57% of those in Generation X, 59% of baby boomers and 62% of those

born before 1946.

- Forty-six percent of non-White Americans, versus 61% of

Non-Hispanic White Americans, support the death penalty.

- Among college graduates, 46% favor the death penalty,

compared with 60% of those without a college degree.

To be sure, demographic change does not account for

all of the attitudinal shift toward the death penalty, as older generations,

White adults and college nongraduates are all less supportive of the death

penalty now than they were in 2016.

Changes in Support for the Death Penalty, by

Generation, Race and Educational Attainment

Figures are the percentage who say they are in favor

of the death penalty for a person convicted of murder

|

2000-2010 |

2011-2016 |

2017-2020 |

Change since 2011-2016 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

% |

pct. pts. |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Generation |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Generation Z (born

1997-2002) |

n/a |

n/a |

45 |

n/a |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Millennials (born 1980-1996) |

61 |

55 |

51 |

-4 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Generation X (born

1965-1979) |

66 |

63 |

57 |

-6 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Baby boomers (born 1946-1964) |

67 |

64 |

59 |

-5 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Traditionalists (born

before 1946) |

67 |

65 |

62 |

-3 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Race/Ethnicity |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Non-Hispanic White adults |

70 |

67 |

61 |

-6 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Non-White adults |

52 |

46 |

46 |

0 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Education |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

College graduates |

60 |

53 |

46 |

-7 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

College nongraduates |

69 |

65 |

60 |

-5 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Bottom Line

Attitudes toward the death penalty have varied greatly

since Gallup first polled Americans on the topic more than 80 years ago. The

percentage favoring it has been as low as 42% and as high as 80%. The most

recent readings are toward the lower end of the range, driven by demographic

changes in the U.S. population and attitudinal evolution. If these trends

continue, the percentage of U.S. adults who favor the death penalty will drop

below 50% in the near future.

As public opinion has trended away from favoring the

death penalty, state laws have also changed. Twenty-two states do not allow the

death penalty by law, with nearly half of those having enacted their current

laws in the past two decades. Three additional states -- California, Oregon and

Pennsylvania -- have laws permitting the death penalty, but their governors

have issued moratoriums on its use.

Consistent with partisans' preferences on the issue,

most of the states that allow the death penalty are Republican-leaning, and

most of those that prohibit its use are Democratic-leaning.

(Gallup USA)

November 19, 2020

Source: https://news.gallup.com/poll/325568/support-death-penalty-holds-above-majority-level.aspx

665-43-13/Poll

62% in U.S. Say Lives Not

Yet Back to Pre-COVID Normalcy

As COVID-19 cases were surging again across the U.S.

last month, more than six in 10 Americans said their lives had not returned to

pre-pandemic normalcy. Overall, 62% of Americans surveyed Oct. 19-Nov. 1 said

their life right now is "not yet back to normal," while 34% said

theirs is "somewhat back to normal" and 3% said

"completely" so.

Among a host of key demographic subgroups, Republicans

are the most likely to say their lives have somewhat (59%) or completely (8%)

gotten back to what they were before COVID-19. The combined 67% of Republicans

feeling like life is back to normal is more than three times the rate among

Democrats (21%) and more than double that among independents (32%).

Most Americans Have Yet to Return to Pre-Pandemic Normalcy

Thinking about your life before the start of the

coronavirus, would you say your life right now is completely back to normal,

somewhat back to normal but not completely normal, or not yet back to normal?

|

U.S. adults |

Republicans |

Independents |

Democrats |

|

|

% |

% |

% |

% |

|

|

Completely back to normal |

3 |

8 |

2 |

1 |

|

Somewhat back to normal

but not completely |

34 |

59 |

30 |

20 |

|

Not yet back to normal |

62 |

33 |

68 |

79 |

|

GALLUP PANEL, OCT. 19-NOV. 1, 2020 |

||||

Indeed, Gallup's probability-based panel survey

tracking Americans' attitudes and behaviors related to the coronavirus

situation has found discrepancies in partisans' practices during

the pandemic, which may

explain why more Republicans say their lives have returned to normal.

The latest data find 48% of Democrats, 41% of

independents and 20% of Republicans saying they have isolated themselves from

people outside their household -- either "completely" or

"mostly" -- in the past 24 hours. At the same time, 50% of

Republicans say they have made little or no attempt to isolate themselves,

compared with 23% of Democrats and 38% of independents who say the same.

Partisans Differ in Their Contact With Non-Household

Members

Next, thinking about everything you've done in the

past 24 hours, which of the following comes closest to describing your

in-person contact with people outside your household?

|

Republicans |

Independents |

Democrats |

|

|

% |

% |

% |

|

|

Completely isolated |

3 |

7 |

13 |

|

Mostly isolated |

17 |

34 |

35 |

|

Partially isolated |

29 |

21 |

30 |

|

Isolated a little |

18 |

19 |

16 |

|

Made no attempt to isolate |

32 |

19 |

7 |

|

GALLUP PANEL, OCT. 19-NOV 1, 2020 |

|||

Democrats are twice as likely as Republicans to say

they "always" practiced social distancing the previous day (53% vs.

26%, respectively). Fully one-quarter of Republicans say they

"rarely" or "never" did so.

Differences in Partisans' Social Distancing Practices

Over the past 24 hours, how often have you been

practicing social distancing?

|

Republicans |

Independents |

Democrats |

|

|

% |

% |

% |

|

|

Always |

26 |

36 |

53 |

|

Very often |

26 |

35 |

35 |

|

Sometimes |

23 |

14 |

10 |

|

Rarely |

11 |

7 |

1 |

|

Never |

14 |

7 |

1 |

|

GALLUP PANEL, OCT. 19-NOV. 1, 2020 |

|||

Similarly, 73% of Republicans think the better advice

for people who do not have symptoms of the coronavirus and are otherwise

healthy is to lead their normal lives as much as possible. However, majorities

of Democrats (93%) and independents (60%) believe it is better to stay home as

much as possible to avoid contracting or spreading the coronavirus.

Americans'

Activities Differ Based on Degree of Normalcy They Feel

The degree of normalcy Americans feel they have in

their life is directly linked to the daily activities they are participating

in. That is, those who say their lives are at least somewhat back to normal are

more likely than those who say their lives are not yet back to normal to have

visited a grocery store, their workplace, someone else's home, their place of

worship and, to a lesser extent, the gym in the past 24 hours. Those who feel

life has returned to some normalcy are also twice as likely as those who do not

to say they have dined at a restaurant within the past day.

Americans' Participation in Activities Based on Degree

of Normalcy They Feel

Percentage who say they have visited the following

places in the past 24 hours

|

Completely/Somewhat back to normal |

Not yet back to normal |

|

|

% |

% |

|

|

Grocery store |

64 |

47 |

|

Place of work |

44 |

32 |

|

Restaurant (dined in) |

27 |

13 |

|

Someone else's home |

26 |

18 |

|

Place of worship |

21 |

5 |

|

Gym |

8 |

4 |

|

GALLUP PANEL, OCT. 19-NOV. 1, 2020 |

||

While it is clear that there are differences between these two groups, it

is not possible to tell how close the current readings are to actual pre-COVID

behaviors.

Americans' Views

of How Much COVID-19 Has Disrupted Their Lives Are Stable

Americans' assessment of their own return to normal,

pre-pandemic life is in line with their evaluation of how much the coronavirus

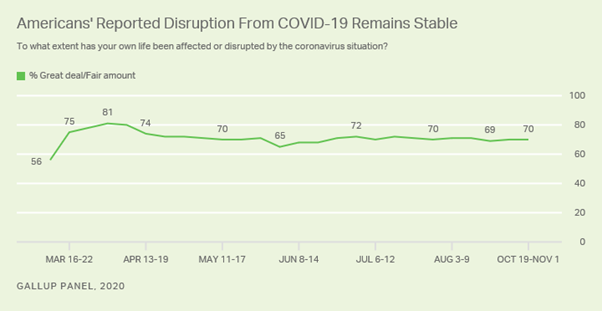

situation has affected their life. In all, seven in 10 U.S. adults say it has

disrupted their life "a great deal" (24%) or "a fair

amount" (46%). Readings on this measure have been largely stable since

April 20 after hitting highs between 74% and 81% earlier in the pandemic.

Line graph. Percentages of Americans who say their own

life has been affected or disrupted a great deal or a fair amount by the

coronavirus situation since March 16. The latest 70% reading is similar to

readings since April.

Just as Republicans are more likely than Democrats and

independents to say their life is at least somewhat back to normal, so too are

they more likely to say the coronavirus situation has not significantly

disrupted their life. Fifty-one percent of Republicans, 81% of Democrats and

74% of independents say the pandemic has affected their life at least a fair

amount.

Bottom Line

New coronavirus cases are trending sharply upward in

the U.S., and a majority of Americans continue to say the situation is

disrupting their lives. Few U.S. adults say life has completely returned to

normal -- yet there are sizable differences across key subgroups in those experiencing

a partial return to normalcy. Partisanship remains the most significant driver

of the public's perceptions of the disease and their behaviors in response to

it.

(Gallup USA)

November 18, 2020

Source: https://news.gallup.com/poll/325487/say-lives-not-yet-back-pre-covid-normalcy.aspx

665-43-14/Poll

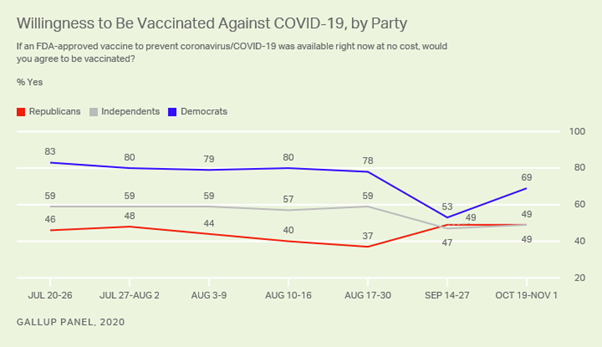

More Americans Now Willing

to Get COVID-19 Vaccine

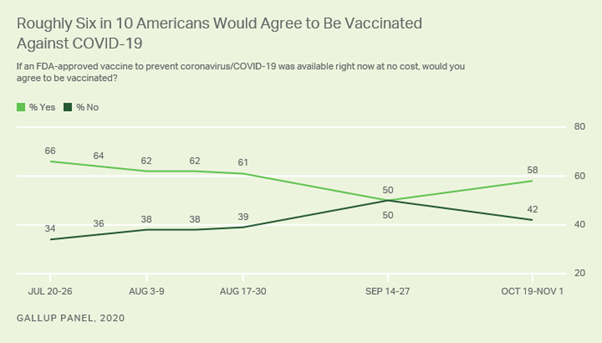

Americans' willingness to be vaccinated against COVID-19

rebounded a bit in October, as seen in Gallup polling conducted before

Pfizer/BioNTech and Moderna made promising announcements about the likely

effectiveness of their coronavirus vaccines. Fifty-eight percent of Americans

in the latest poll say they would get a COVID-19 vaccine, up from a low of 50%

in September.

Line graph. Americans' willingness to take a vaccine

against COVID-19. 58% of Americans say the would take such a vaccine, while 42%

say they would not.

These latest data come from a Gallup Panel survey

conducted Oct. 19-Nov. 1, as COVID-19 infections continued to increase across

the U.S. A vaccine for the disease is seen as key to returning Americans' lives

to normal and allowing the lifting of restrictions that would permit a full

economic recovery for the country.

The 42% of U.S. adults saying they would not get a vaccine is down from 50% in

September, but still indicative of significant challenges ahead for public

health and government officials in achieving mass public compliance with vaccine

recommendations.

COVID-19 Vaccine

Willingness Among Key Groups

Democrats currently show the largest increase in

willingness to get a COVID-19 vaccine, with 69% saying they would get a

vaccine, compared with 53% in September. Democrats have been consistently more

likely than Republicans and independents to say they would get a vaccine since

Gallup first asked about the issue in July. In September, the gap between

Democrats and Republicans on this issue narrowed to four percentage points, the

smallest margin measured to date. This was mostly due to decreased willingness

on the part of Democrats -- perhaps because of worries that a vaccine would be

rushed out prior to the presidential election, without adequate clinical

testing to ensure its safety.

Line graph. Americans' willingness to take a vaccine

against COVID-19, by political affiliation. 69% of Democrats, 49% of

Republicans and 49% of independents say they would be willing to take a vaccine

protecting against the disease.

Another significant increase in willingness to get a

vaccine is seen in Americans aged 45 to 64, with 49% of this group now willing

to do so, up from 36% in September. However, this age group remains the least

likely to say they would get a vaccine.

The latest results also show 10-point increases in

willingness among women and those without a college degree.

Willingness to Be Vaccinated Against COVID-19, by

Subgroup

If an FDA-approved vaccine to prevent

coronavirus/COVID-19 was available right now at no cost, would you agree to be

vaccinated? (% Yes)

|

Sep 14-27 |

Oct 19-Nov 1 |

Change |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

pct. pts. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Gender |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Men |

56 |

61 |

+5 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Women |

44 |

54 |

+10 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Age |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

18-44 |

60 |

62 |

+2 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

45-64 |

36 |

49 |

+13 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

65+ |

54 |

63 |

+9 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Education |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

No college degree |

45 |

55 |

+10 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

College degree |

60 |

63 |

+3 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Party |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Democrats |

53 |

69 |

+16 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Independents |

47 |

49 |

+2 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Republicans |

49 |

49 |

0 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Race/Ethnicity |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

White adults |

54 |

61 |

+7 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Non-White adults |

40 |

48 |

+8 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Region |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Northeast |

59 |

66 |

+7 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Midwest |

46 |

55 |

+9 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

South |

43 |

52 |

+9 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

West |

58 |

62 |

+4 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP PANEL, 2020 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Americans'

Reasons to Not Get a COVID-19 Vaccine

In a follow-up question, 37% of Americans who would

not get a vaccine say the rushed timeline for the development of the vaccine is

the main reason they would not be vaccinated. Another 26% say they want to wait

to confirm the vaccine is safe. Rounding out the reasons for some Americans'

hesitancy are 12% saying they don't trust vaccines in general and 10% who want

to wait to see how effective the vaccine will be. An additional 15% cite other

reasons for not getting a COVID-19 vaccine. Included among these reasons are the

politicization of the vaccine potentially comprising its safety and the view

that the vaccine is not necessary.

The majority of Democrats who say they would not get a

vaccine, 54%, reference concerns about rushed development. This compares with

26% of Republicans and 32% of independents who say the same.

One in five Republicans who do not plan to get a

COVID-19 vaccine mention distrust of vaccines in general, a view shared by 14%

of independents and 2% of Democrats.

Reasons for Choosing to Not Be Vaccinated Against

COVID-19

What is the main reason that you would not agree to

receive a coronavirus/COVID-19 vaccine, if one was available now?

|

Concerns |

Want to wait |

Don't trust |

Want to wait |

Other reason |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

% |

% |

% |

% |

% |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Overall |

37 |

26 |

12 |

10 |

15 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Gender |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Men |

35 |

22 |

12 |

12 |

19 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Women |

38 |

29 |

12 |

8 |

12 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Age |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

18-44 |

46 |

33 |

5 |

2 |

15 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

45-64 |

37 |

25 |

14 |

8 |

16 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

65+ |

32 |

23 |

14 |

17 |

14 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Education |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

No college degree |

35 |

22 |

15 |

12 |

17 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

College degree |

41 |

36 |

7 |

7 |

10 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Party |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Democrats |

54 |

30 |

2 |

4 |

10 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Independents |

32 |

30 |

14 |

12 |

11 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Republicans |

26 |

19 |

20 |

14 |

22 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Race/Ethnicity |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

White adults |

37 |

24 |

13 |

10 |

17 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Non-White adults |

37 |

30 |

11 |

11 |

12 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Region |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Northeast |

19 |

25 |

18 |

17 |

22 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

Midwest |

43 |

27 |

11 |

8 |

11 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

South |

36 |

29 |

12 |

10 |

13 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

West |

44 |

17 |

11 |

7 |

20 |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

*Among those who say they would not be vaccinated |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

GALLUP PANEL, OCT. 19-NOV. 1, 2020 |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Bottom Line

Even before the announcements made by Pfizer and

BioNTech on Nov. 9 and by Moderna on Nov. 16 about the development of highly

effective vaccines for COVID-19, Americans were already more willing to get a