BUSINESS

& POLITICS IN THE WORLD

GLOBAL

OPINION REPORT NO. 679

Week: February 22 –February 28,

2021

Presentation: March 05, 2021

679-43-23/Commentary: 55% Of American Adults

Already Vaccinated Against COVID 19: First Dose

Fukushima

Poll, 74% Say Nuclear Disaster Work Not Promising

More

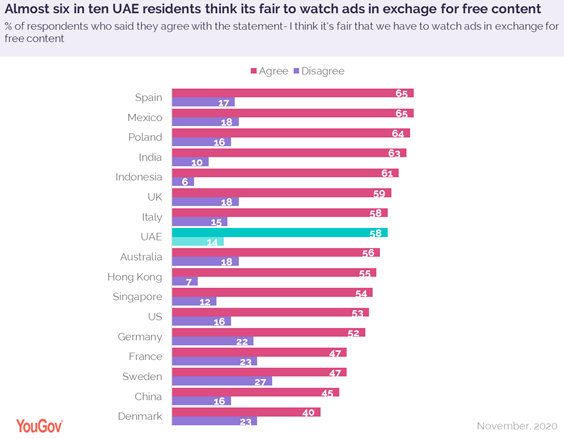

Than Six In Ten Urban Indians Do Not Mind Watching Ads In Exchange For Free

Content

One

In Five Singaporean Gen Z-Ers Willing To Exchange Personal Data For Free

Content

Iranian

Public Opinion In The Biden Era

Top

Most Important Things Nigerians Want From Their President

35%

Of British Public See a Decrease In UK And EU Relatinship

Latest

Findings From Antibody Surveillance Study Published

Support

For Scottish Independence Falls Back

The

Boom In Online Shopping And Delivery Services

Health

Barometer # 4 - Yougov X 20 Minutes X Doctissimo

Rare

Diseases: Europeans And In Particular The French Do Not Accept Fatality

Sunday

Question: 3 Percentage Points Loss At The CDU

International

Study On Anti-Covid Rules: Italians Stopped At The Bare Minimum

On

The Money: The Evolution Of The Banking And Insurance Sector In Italy

The

Financial Sector In Spain After Covid-19

Majority

of Americans Confident in Biden’s Handling of Foreign Policy as Term Begins

55%

Of American Adults Already Vaccinated Against COVID 19: First Dose

A

Quarter Of Australian Millennials Willing To Exchange Personal Data For Free

Content

Heavy

Hands And Heavy Hearts: The Perils Of Military Intervention In Mena

Covid-19

And Consumer Behavior, How Has The Pandemic Affected Personal Finances And

Consumption

More

Than Three-Quarters Of UAE Residents Plan To Cut Down Their Non-Essential

Spending In 2021

Almost

Six In Ten UAE Consumers Think Watching Ads In Exchange For Free Content Is A

Fair Deal

INTRODUCTORY NOTE

679-43-23/Commentary: 55% Of American Adults Already Vaccinated Against COVID 19: First Dose

The KFF COVID-19 Vaccine Monitor is an ongoing research project tracking the public’s attitudes and experiences with COVID-19 vaccinations. Using a combination of surveys and qualitative research, this project tracks the dynamic nature of public opinion as vaccine development and distribution unfold, including vaccine confidence and acceptance, information needs, trusted messengers and messages, as well as the public’s experiences with vaccination.

Key Findings

• As COVID-19 vaccination distribution efforts continue across the United States, the latest KFF COVID-19 Vaccine Monitor reports that a majority (55%) of U.S. adults now say they have received at least one dose of the vaccine (18%) or that they will get it as soon as they can (37%), up from 47% in January and 34% in December. The share that wants to “wait and see” how the vaccine is working for others before getting vaccinated themselves decreased from 31% in January to 22% in February, while a persistent one in five say they will get the vaccine “only if required for work, school, or other activities” (7%) or will “definitely not” get vaccinated (15%).

• While the share that is most enthusiastic to get vaccinated increased across racial and ethnic groups, Black and Hispanic adults continue to be more likely than White adults to say they will “wait and see” before getting vaccinated. Nearly four in ten Republicans and three in ten rural residents say they will either “definitely not” get vaccinated or will do so “only if required,” as do one-third (32%) of those who have been deemed essential workers in fields other than health care.

• With the potential arrival of a one-dose COVID-19 vaccine to the U.S. market, most of those who have not yet been vaccinated say the number of doses doesn’t make a difference in their own intentions, but about a quarter (26%) of those in the “wait and see” group say they’d be more likely to get a vaccine if only one dose was required.

• Having a close relationship with someone who’s been vaccinated is correlated with individuals’ own intentions to get the COVID-19 vaccine. Among those who have not yet been vaccinated, seven in ten of those with a household member who’s been vaccinated and about half of those who say a close friend or family member has been vaccinated say they want the vaccine “as soon as possible,” compared to about a third of those who don’t have a close relationship to someone who’s gotten the vaccine. Black and Hispanic adults, those with lower incomes, and those without a college degree are less likely than their counterparts to say someone close to them has gotten the vaccine, reflecting other KFF analysis showing similar disparities.

• The perceived side effects of the vaccine continue to be a top concern for the public, with eight in ten in the “wait and see” group saying they are concerned they might experience serious side effects if they get vaccinated. Large shares of those who want to “wait and see” – including majorities of Black and Hispanic adults – also say they are concerned that they might get COVID-19 from the vaccine, they might have to miss work if the side effects make them feel sick, they may have to pay an out-of-pocket cost to get vaccinated (despite the fact that the vaccine is available for free to everyone), or they won’t be able to get the vaccine from a place they trust.

• Half of Black adults and about one-third Hispanic adults (35%) say they are not confident that the COVID-19 vaccines have been adequately tested for safety and effectiveness among members of their own racial or ethnic group, and those who aren’t confident in this type of testing are much less likely to say they’ve already been vaccinated or want the vaccine as soon as they can get it.

COVID-19 Vaccine Uptake and Intentions

Trends Among Key Groups

More than half of U.S. adults (55%) now say they have already received at least one dose of the COVID-19 vaccine (18%) or they want it as soon as possible (37%). This is an increase from 47% in mid-January and up from 34% in early December before vaccine distribution began. About one in five adults (22%) say they will “wait and see” how the vaccine is working for others before getting vaccinated themselves, a share that is down from 31% in January and 39% in December. The remaining public say they will get the vaccine “only if required for work, school, or other activities” (7%) or that they will “definitely not” get

vaccinated (15%), shares that have not changed much over the past two months.

Across racial and ethnic groups, there was a steady increase from December to February in the share of adults who say they’ve already been vaccinated for COVID-19 or want the vaccine as soon as possible, and a corresponding decrease in the share who say they will “wait and see” before getting vaccinated. Despite this movement, differences in vaccine enthusiasm between members of different racial and ethnic groups persist. For example, six in ten White adults (61%) say they have already gotten the vaccine or want it as soon as possible compared to about half (52%) of Hispanic adults and four in ten Black adults (41%).

The Monitor also reports changes in vaccine enthusiasm across partisans, with large gaps in enthusiasm remaining between groups. Between December and February, there was a large increase in the share of Democrats who report being vaccinated or wanting to do so as soon as possible (from 47% to 75%) and a more modest increase among Republicans (from 28% to 41%). A substantial share of Republicans remain more resistant to getting vaccinated, with 28% saying they will “definitely not” get the shot.

Similarly, there has been an increase in COVID-19 vaccine enthusiasm across residents of urban, suburban, and rural areas since December, and now at least half of each group say they have already gotten the vaccine or want it as soon as possible (55% of urban, 56% suburban, and 53% of rural residents). Still, a larger share of rural (24%) compared to urban (13%) and suburban (14%) adults say they will “definitely not” get the vaccine.

Which Groups Are Most

Enthusiastic/Cautious/Resistant?

While there has been an overall shift towards greater enthusiasm for getting a COVID-19 vaccination, the demographic groups that are the most enthusiastic, most cautious, and most resistant remain similar to those reported in January. About three-quarters of adults ages 65 and over (77%) and a similar share of Democrats (75%) say they have either already gotten at least one dose of the vaccine or will do so as soon as they can. About two-thirds of college graduates (67%) and those who work in health care delivery settings (65%) also fall into this most enthusiastic group.

About one in five adults overall (22%) say they want to “wait and see” how the vaccine is working for other people before getting vaccinated themselves, including about a third of Black adults (34%) and those between the ages of 18-29 (33%), and about a quarter of Hispanic adults (26%), those without college degrees (25%), and essential workers in non-health fields (25%).

Four in ten Republicans (38%) say they will get a COVID-19 vaccine “only if required” or will “definitely not” get vaccinated, as do about three in ten (28%) of adults living in rural areas. Notably, about one-third of those who say they’ve been deemed “essential workers” and are required to work outside their homes during the pandemic (excluding those who work in health care settings) say they will get the vaccine “only if required” (9%) or will “definitely not” get it (24%).

Demographic Differences In

Vaccine Intentions

Looking at patterns of vaccine intentions across demographic groups, it’s notable that lower levels of enthusiasm among Black adults compared to White adults persist even after controlling for education levels. For example, among White adults without a college degree, 54% say they’ve already gotten the vaccine or will get it as soon as they can, compared to 38% of Black adults without a college degree. Similarly, among those who have graduated from college, vaccine uptake and enthusiasm is higher among White adults (72%) compared to their Black counterparts (48%).

Adults ages 65 and over are one of the target groups for early vaccination, and one of the groups most likely to say they’ve already been vaccinated or want the vaccine as soon as possible. Looking at vaccine intentions by a combination of race and age, large majorities of both Black and White adults ages 65 and over fall into the most enthusiastic categories. However, while nearly half of older White adults (46%) say they they’ve already gotten the vaccine, about one-third of Black older adults say the same (35%). Half (46%) of Black adults 65 and older say they will get it as soon as they can.

Among younger age groups, Black adults are nearly twice as likely as White adults to say they will “wait and see” before getting vaccinated (35% vs. 18% among those ages 50-64 and 41% vs. 23% among those ages 18-49).

Two-Dose Versus Single-Dose

Vaccine

With the potential arrival of a single-dose vaccine to the U.S. market, the Vaccine Monitor probed people’s willingness to get a vaccine that required only one dose as opposed to the currently available two-dose vaccines. A large majority (83%) of those who have not yet been vaccinated say that the number of doses doesn’t make a difference in their own intentions to get vaccinated. However, about a quarter of (26%) of those who want to “wait and see” before getting vaccinated say they’d be more likely to get a vaccine if only one dose was required (including 20% of Black adults, 28% of Hispanic adults, and 29% of White adults in the “wait and see” group).

Personal Experiences With

COVID-19 Vaccination

Having a close relationship with someone who’s been vaccinated is correlated with individuals’ own intentions to get the COVID-19 vaccine. Among those who have not yet gotten the vaccine but live in a household with someone who has been vaccinated, about seven in ten (69%) say they will get the vaccine as soon as they can. Similarly, about half (49%) of those who say a close friend or family member outside of their household has been vaccinated are in the “as soon as possible” group. Among those who have only a casual connection or no connection to someone who’s been vaccinated, about one-third say they want the vaccine as soon as they can get it, while larger shares (compared to those with a close personal connection to someone who’s been vaccinated) say they want to “wait and see” before getting vaccinated.

Given this association between having a close relationship to someone who has gotten the vaccine and an individual’s personal level of vaccine enthusiasm, it’s notable that Black and Hispanic adults, those with lower incomes, and those without college degrees are less likely than their counterparts to report having these connections. For example, three-quarters of White adults have a close personal connection to someone who has gotten the vaccine (including themselves) compared to 57% of Black and Hispanic adults. Similarly, 83% of those with incomes of $90,000 or more report a close personal connection to someone who has been vaccinated compared to 59% of those with incomes under $40,000, as do 86% of college graduates compared to 64% of adults without college degrees.

Personal Concerns About

COVID-19 Vaccination

The February COVID-19 Vaccine Monitor probed a variety of personal concerns people might have when it comes to receiving a vaccine. As reported previously, side effects remain a prominent concern; over half (56%) of those who have not yet been vaccinated, including 80% of those in the “wait and see” group, say they are “very concerned” or “somewhat concerned” that they might experience serious side effects from the vaccine. Other concerns cited by about a third of the unvaccinated and about half of those in the “wait and see” group” are that they might have to pay out of pocket for the vaccine (despite the fact that the vaccine is available at no cost), they might have to miss work if the vaccine’s side effects make them feel sick, or that they might get COVID-19 from the vaccine.

While the possibility of experiencing serious side effects from the vaccine is a top concern across racial and ethnic groups, larger shares of Black and Hispanic adults compared to White adults in the “wait and see” category express concern that they might get COVID-19 from the vaccine, might miss work due to side effects, or have to pay out of pocket to get vaccinated (despite the fact that the vaccine is free for everyone). Among those who want to “wait and see,” about six in ten Hispanic adults (58%) and about half of Black adults (52%) are concerned that they won’t be able to get the vaccine from a place they trust, compared with about one-third of White adults (32%). In addition, about four in ten Hispanic adults in this group are concerned that they might need to take time off work to get vaccinated (43%) or they will have difficulty traveling to a vaccination site (39%).

Confidence In Vaccine

Development And Testing Among Black And Hispanic Adults

Concerns about COVID-19 vaccination among Black and Hispanic adults may be linked to perceptions of whether people of color were represented in clinical trials and other vaccine research. In fact, half of Black adults say they are “not too confident” or “not at all confident” that the COVID-19 vaccines were adequately tested for safety and effectiveness specifically among Black people, and about a third of Hispanic adults (35%) say the same thing about testing among Hispanic people.

Confidence in adequate testing among one’s own racial or ethnic group is related to vaccine intentions and enthusiasm among Black and Hispanic adults. Those who are at least somewhat confident that the vaccines have been adequately tested for safety and effectiveness among their own racial or ethnic group are about twice as likely to say they’ve already been vaccinated or want the vaccine as soon as they can get it compared to those who are not confident (58% vs. 24% among Black adults, 63% vs. 30% among Hispanic adults).

(Ssrs)

February

26, 2021

Source: https://ssrs.com/kff-covid-19-vaccine-monitor-february-2021/

679-43-24/Country Profile: United States Of America

SUMMARY

OF POLLS

Asia

(Japan)

Fukushima Poll, 74% Say Nuclear Disaster Work Not Promising

Only 19 percent of residents in Fukushima

Prefecture believe the work to decommission the crippled Fukushima No. 1

nuclear plant is showing “promise” nearly 10 years after the triple meltdown, a

survey showed. Seventy-four percent of respondents in the telephone survey said

the situation was “not promising” at Tokyo Electric Power Co.’s nuclear plant.

The survey, jointly conducted by The Asahi Shimbun and Fukushima Broadcasting

Co. on Feb. 20 and 21, is the 11th since the Great East Japan Earthquake and

tsunami caused the nuclear disaster in March 2011.

(Asahi Shimbun)

February 24, 2021

(India)

More Than Six In Ten Urban Indians Do Not Mind

Watching Ads In Exchange For Free Content

YouGov’s latest global report reveals

more than six in ten urban Indians (63%) think it is fair to watch ads in

exchange for free content. The report, titled ‘International Media Consumption Report 2021- Is there a

new normal?’ provides an analysis of the global media

landscape across 17 markets. Across the globe, a plurality of consumers in the

17 markets favour the idea of watching advertisements

in exchange for free content. Along with India, countries such as Mexico (65%),

Spain (65%) and Poland (64%) highly favour this idea.

(YouGov India)

February 25, 2021

(Singapore)

One

In Five Singaporean Gen Z-Ers Willing To Exchange

Personal Data For Free Content

YouGov’s new ‘International media consumption report 2021: Is there a new normal?’ white paper examines Singaporeans generational attitudes towards paid content. While personal data and privacy concerns have become a growing concern, one in six (16%) Singaporeans agree that they are willing to give up their personal data for free content. Men are twice as willing compared to women (21% vs. 11%). Over half (55%) are unwilling and a quarter (25%) are undecided.

(YouGov Singapore)

February 26, 2021

MENA

(Iran)

Iranian Public Opinion In The Biden Era

University of Maryland CISSM has conducted its most recent study based on two consecutive waves of nationally representative surveys that were conducted in Iran by IranPoll for the University of Maryland. University of Maryland CISSM was responsible for designing the questionnaires, getting feedback on them from relevant policy experts and practitioners, performing the analysis, and putting together the final report.

(Iran Poll)

AFRICA

(Nigeria)

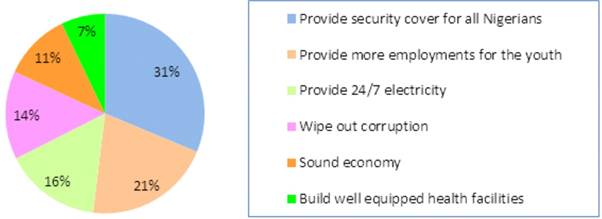

Top Most Important Things Nigerians Want From

Their President

Provision of full security cover for all Nigerians (31%) and creation of job opportunities for youths (21%) topped the list of the most important things Nigerians want from their President. Over the last decade, insecurity has been ravaging all the nocks and crannies of Nigeria.

(Market Trends International)

February 21, 2021

WEST EUROPE

(UK)

35% Of British Public See a Decrease In UK And EU Relatinship

There has been a surge in the proportion who see Coronavirus as the single biggest issue for the nation however: 61% say this, up from 47% in December last year and the highest score on this measure since July 2020. Concern about the economy is the third biggest issue for Britons this month, rising five percentage points to 32%. There have also been increases in public concern about the NHS, poverty/inequality, education and unemployment.

(Ipsos MORI)

22 February 2021

Latest

Findings From Antibody Surveillance Study Published

Of these participants, over 17,000 said they had received at least one COVID-19 vaccine dose. The data shows 87.9% of people over the age of 80 tested positive for antibodies after two doses of the Pfizer-BioNTech vaccine, rising to 95.5% for those under the age of 60 and 100% in those aged under 30.

(Ipsos MORI)

25 February 2021

Support

For Scottish Independence Falls Back

Ipsos MORI’s Scottish Political Monitor, run in partnership with STV News, finds that the SNP are still in pole position ahead of May’s Holyrood elections. 52% say they are likely to vote for the SNP in the constituency vote, while 23% will vote for the Scottish Conservatives and 15% for Scottish Labour. 52% would vote Yes in an independence referendum, slipping slightly from 56% in November - while 48% would vote No.

(Ipsos MORI)

25 February 2021

(France)

The Boom In Online Shopping And Delivery Services

9 out of 10 French people say they have bought at least one product online in the past 12 months (90%). More specifically, 41% say they made purchases in the week preceding the survey, a figure drawn on the rise by women (47%) and 25-34 year olds (51%). Among the French who say they have made purchases on the internet in the past 12 months. 37% indicate ordering more often than before the health crisis (42% of women vs. 32% of men). 39% say their average basket has increased since the start of the pandemic (42% of women vs. 35% of men)

(YouGov France)

February 25, 2021

Health

Barometer # 4 - Yougov X 20 Minutes X Doctissimo

Nearly 3 in 4 French people (73%) say they are worried about the arrival of new variants of the coronavirus (English, South African, etc.). Faced with these variants, the main source of concern observed is contagiousness (36%), followed by the effectiveness of vaccines (28%). 54% of French people say they will get vaccinated as soon as they are affected (+4 points).

(YouGov France)

February 25, 2021

Rare

Diseases: Europeans And In Particular The French Do Not Accept Fatality

Rare diseases are not that much: one in 20 people say they have them (5%) and 3 in 10 people are affected by these diseases, directly or indirectly because they have a loved one (a child, a parent, a friend : 13%) or a fair knowledge (13%) suffering from a rare disease. This is particularly the case for more than a third of French people (34%). 72% would not accept the impossibility of obtaining a diagnosis for several years (74% of French people) and 72% would also not admit to discovering that no research is being carried out to develop a treatment against this disease

(Ipsos France)

February 27, 2021

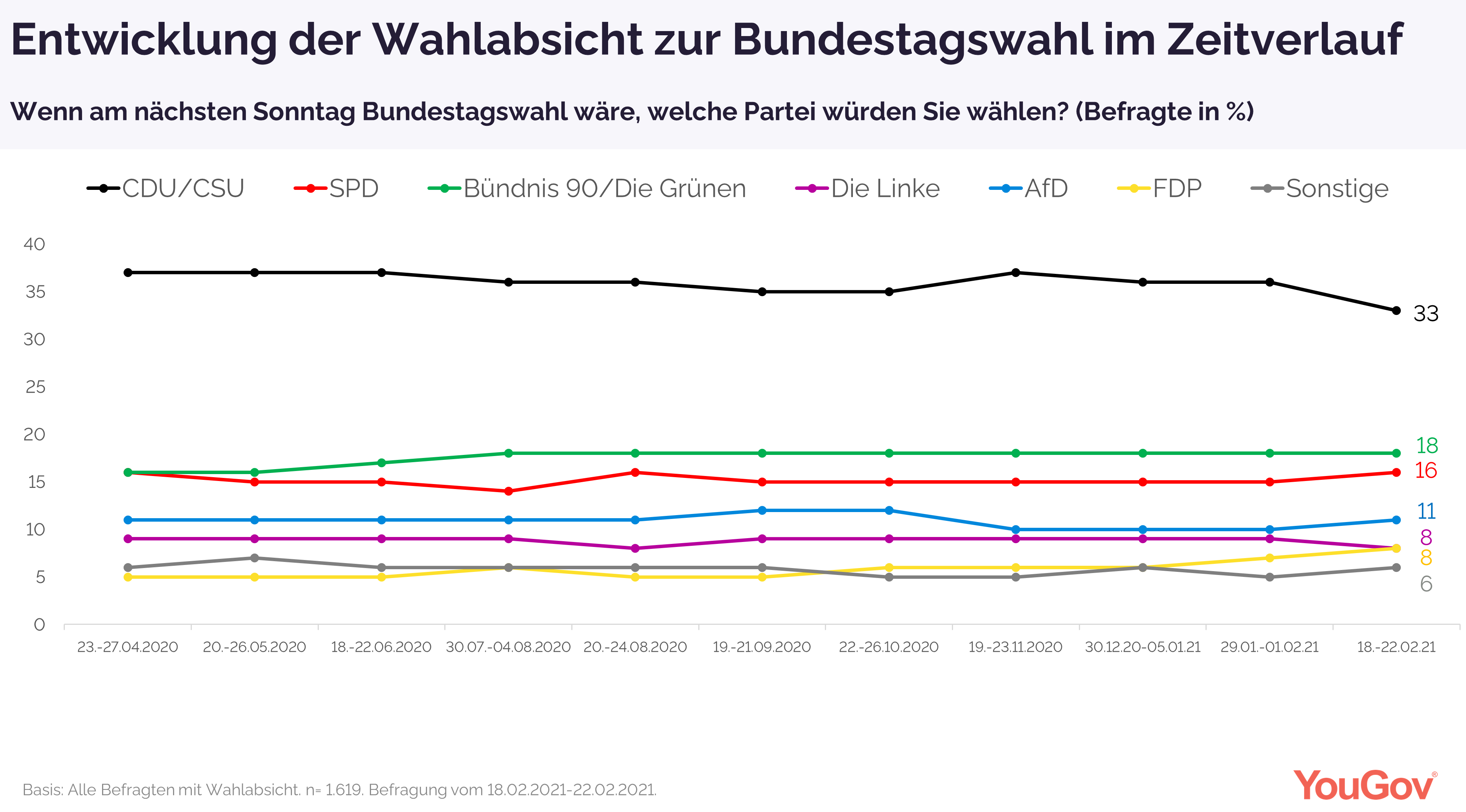

(Denmark)

Sunday Question: 3 Percentage Points Loss At The

CDU

33 percent of the German citizens entitled to vote state that they will vote for the CDU / CSU if there would be a general election next Sunday. This value is 3 percentage points lower than in January 2021, making it the worst result in voting intent for the Union since the beginning of the Corona crisis. The result of the SPD, on the other hand, can make up one point: The Social Democrats landed at 16 percent in February.

(YouGov Denmark)

February 26, 2021

(Italy)

International Study On Anti-Covid

Rules: Italians Stopped At The Bare Minimum

YouGov research has repeatedly shown that, at best, Italians stick to following the rules to the letter and rarely go any further - for example, our research on Christmas restrictions showed that 59% would have celebrated Christmas. with other people , although distancing is clear to all to be the only means to stop the infections. And sometimes they even border on violations: another research has shown that only half of Italians think that the people around them have been loyal to the anti-contagion prescriptions.

(YouGov Italy)

February 23, 2021

On The Money: The Evolution Of The Banking And

Insurance Sector In Italy

Compared to the national average, they are mostly men over 35

years of age (51% in the target compared to 37% of the total adult

population). 66% of them have a paid job and almost 4 out of 10 have

a monthly “surplus” of income exceeding 500 euros (39%

vs. 23% of the national average). This kind of Italian investors is not

composed, therefore, only of individuals with capital blocked in medium or

long-term investments, but also of people with much higher than average

liquidity.

(YouGov Italy)

February 25, 2021

(Spain)

The Financial Sector In Spain After Covid-19

37% of those surveyed

affirm that they do not have

savings or investment products, the rest are divided

into holders of a bank deposit that

allows you to enter or

withdraw money (33%), in second place, pension plans (16% ), fixed-term bank deposit in third place (8%) and, in fourth

place, investments in the

Stock Market (6%). On the other hand,

of those surveyed, almost three out

of 10 people (29%) admit that they do not

save at the end of each month,

compared to 40% who say they

save less than 500 euros and 13% who say they save

more than this amount, between 500 and 1000

euros per month.

(YouGov Spain)

February 22, 2021

NORTH AMERICA

(USA)

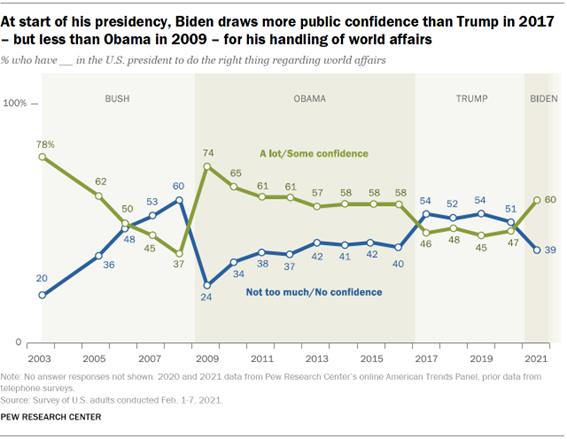

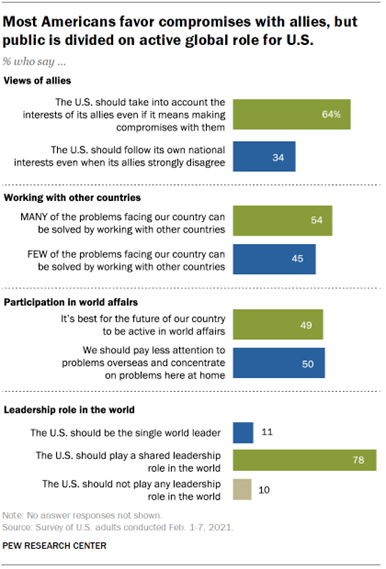

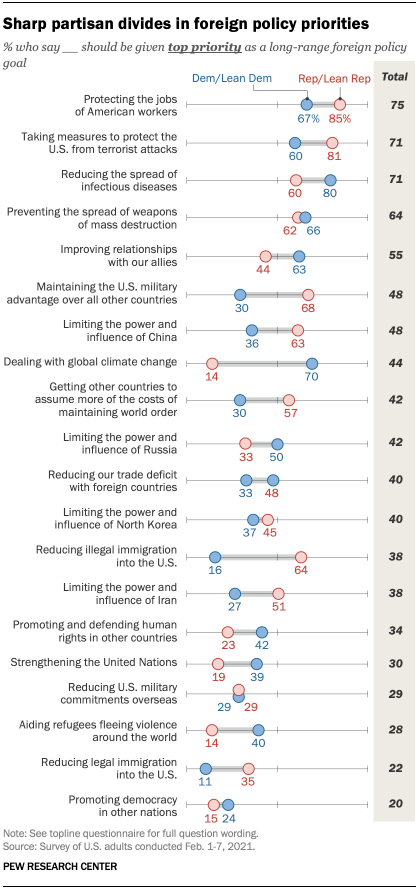

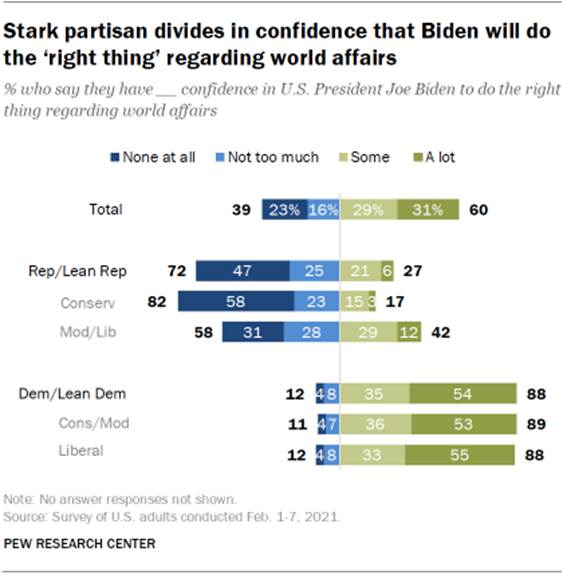

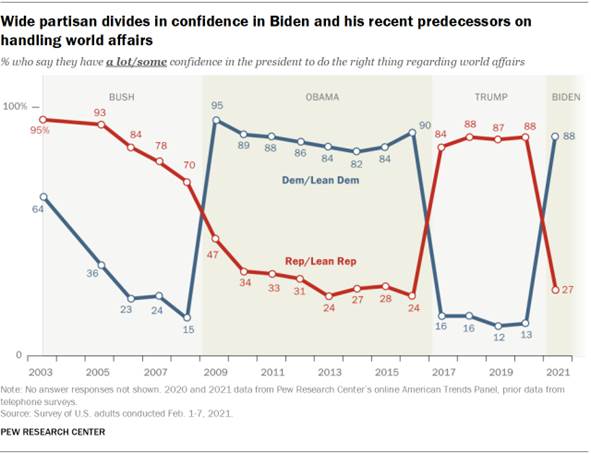

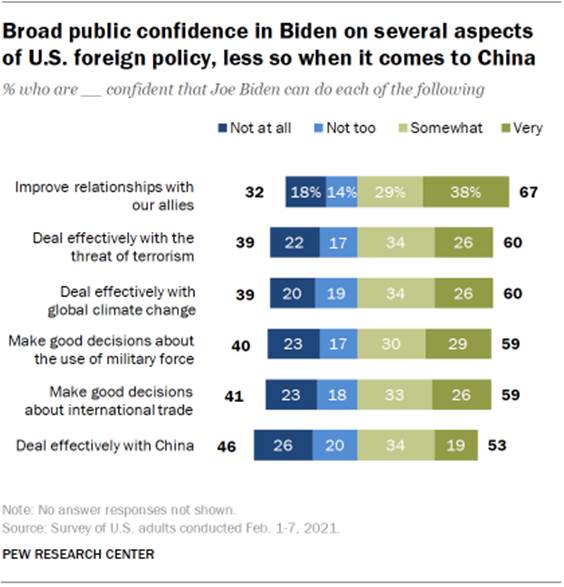

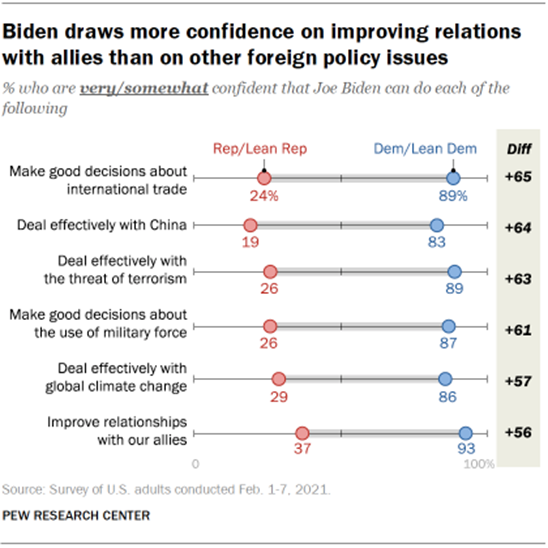

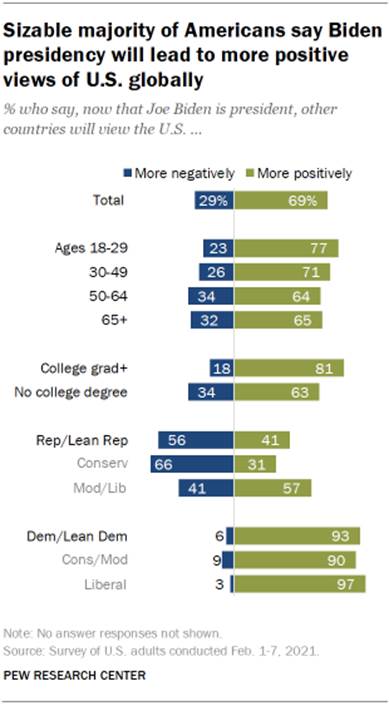

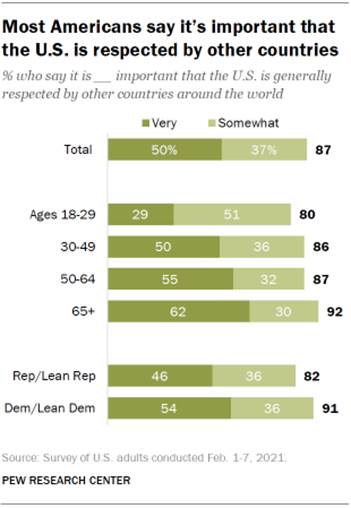

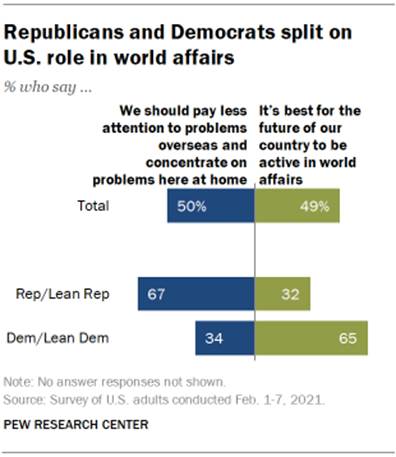

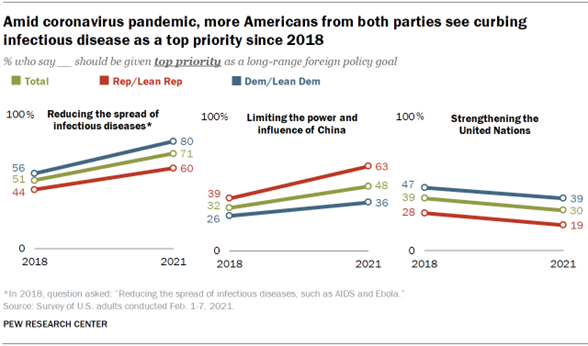

Majority of Americans Confident in Biden’s

Handling of Foreign Policy as Term Begins

President Joe Biden begins his term with a majority of Americans having confidence in his ability to handle international affairs. In a new Pew Research Center survey, 60% of U.S. adults have confidence in Biden on foreign policy – fewer than said the same of Barack Obama as his presidency began (74%) but more than for Donald Trump in his first year (46%).

(PEW)

FEBRUARY 24, 2021

55% Of American Adults Already Vaccinated Against

COVID 19: First Dose

More than half of U.S. adults (55%) now say they have already received at least one dose of the COVID-19 vaccine (18%) or they want it as soon as possible (37%). This is an increase from 47% in mid-January and up from 34% in early December before vaccine distribution began. About one in five adults (22%) say they will “wait and see” how the vaccine is working for others before getting vaccinated themselves, a share that is down from 31% in January and 39% in December.

(Ssrs)

February 26, 2021

AUSTRALIA

(Australia)

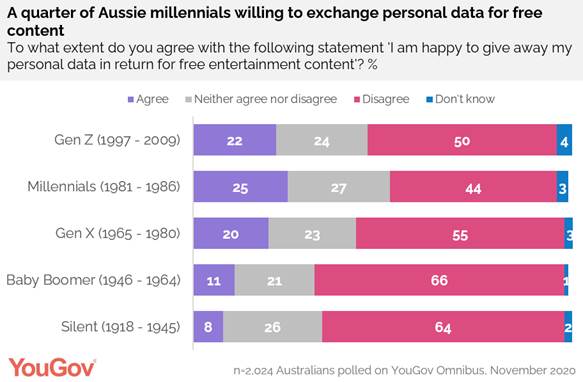

A Quarter Of Australian Millennials Willing To

Exchange Personal Data For Free Content

YouGov’s new ‘International media consumption report 2021: Is there a new normal?’ white paper examines Australians’ generational attitudes towards paid content. While personal data and privacy concerns have become a growing concern, almost one in five (19%) agree that they are willing to give up their personal data for free content. Men are more willing compared to women (22% vs. 15%). Over half (55%) are willing, and the remaining quarter (24%) are undecided.

(YouGov Australia)

February 26, 2021

MULTICOUNTRY STUDIES

Heavy Hands And Heavy Hearts: The Perils Of

Military Intervention In Mena

Amongst these four powers, support across the region is highest for Turkey, with majorities holding favorable views of the country in four of the six countries surveyed. Support is highest in Morocco (65 percent), followed by Jordan and Algeria (56 percent, respectively), and Tunisia (52 percent). However, support is not universal, with only three-in-ten holding this view in Lebanon compared with 27 percent in Libya. In Lebanon, views are linked by sect, with 45 percent of Sunnis favoring Turkey, compared with 35 percent of Christians, 11 percent of Shiites and only 7 percent of Druze.

(Arabbarometer)

February 24, 2021

Covid-19 And Consumer Behavior, How Has The

Pandemic Affected Personal Finances And Consumption

Globally, many consumers have actively limited their spending during the pandemic; most in Indonesia, with 72% of the adult population, and over half of the population in countries such as Italy (56%) and Mexico (55%). Denmark (20%), Germany (28%) and Sweden (35%) are the countries where the fewest have reduced their consumption. But even here, at least one-fifth of consumers (20%) have reduced their non-essential expenses.

(YouGov Denmark)

February 23, 2021

More Than Three-Quarters Of UAE Residents Plan To

Cut Down Their Non-Essential Spending In 2021

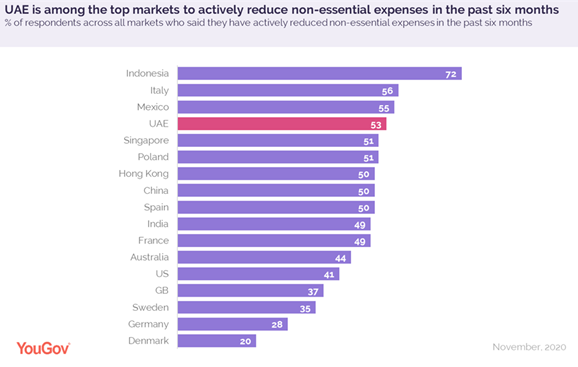

YouGov’s deep dive custom research reveals that over half (53%) of UAE residents had to cut their non-essential spending in the past six months in order to cover expenses, and more than three-fourths (77%) are likely to continue doing so in the future. In many of the surveyed markets, a majority of people have cut down their non-essential expenditure in past six months. This is the highest in Indonesia- at 72%, followed by Italy (56%) and Mexico (55%). Germany and Denmark are at the bottom of the list where less than a third claim to have done it (28% and 20% respectively).

(YouGov MENA)

February 24, 2021

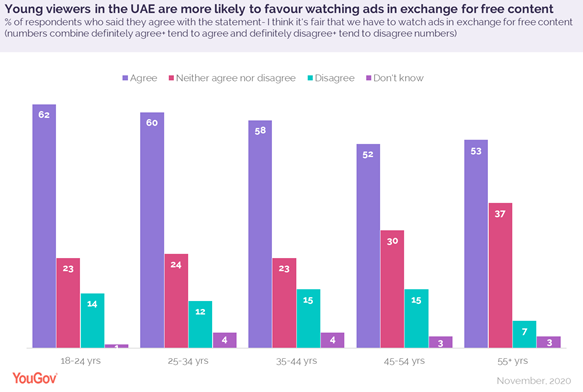

Almost Six In Ten UAE Consumers Think Watching Ads

In Exchange For Free Content Is A Fair Deal

In the UAE, all age groups show a general acceptance towards viewing ads in exchange for free content, but the younger audiences (18-24 years) favour this trend the most (62%). At a global level, Spain and Mexico are the top countries (65% each) where consumers are in support of this proposition. Whereas two Scandinavian countries, Sweden and Denmark, are most likely to dissent, but even in these markets, only around a quarter (27% Sweden; 23% Denmark) consider watching advertising in exchange for free-content to be unfair.

(YouGov MENA)

February 25, 2021

ASIA

679-43-01/Poll

Fukushima Poll, 74% Say Nuclear Disaster Work Not Promising

Only 19 percent of residents in Fukushima

Prefecture believe the work to decommission the crippled Fukushima No. 1

nuclear plant is showing “promise” nearly 10 years after the triple meltdown, a

survey showed.

Seventy-four percent of respondents in the

telephone survey said the situation was “not promising” at Tokyo Electric Power

Co.’s nuclear plant.

The survey, jointly conducted by The Asahi

Shimbun and Fukushima Broadcasting Co. on Feb. 20 and 21, is the 11th since the

Great East Japan Earthquake and tsunami caused the nuclear disaster in March

2011.

The first was conducted in September 2011,

followed by surveys on February or March every year from 2012.

The central government and TEPCO have set a

goal of completing the decommissioning work “in 30 to 40 years,” but their

efforts so far have been hit with various problems and delays.

Although evacuation orders have been lifted,

many residents who fled the disaster have not returned to their homes near the

plant. Still, the government plans to entice people to move into

municipalities around the nuclear plant.

According to the survey, 21 percent of

respondents viewed the new settlement policy as “promising” for revitalizing

the area, compared with 72 percent who said it was “not promising.”

One constant problem in the decommissioning

work is the continual stream of contaminated water that must be stored in tanks

at the site of the plant.

With space running out, the government’s policy

is to treat the water and dump it into the sea, even though the process will

not remove all radioactive substances.

Thirty-five percent of respondents approved

this policy, up from 31 percent in the 2020 survey, while 53 percent opposed

the policy, down from 57 percent.

However, 87 percent of respondents said they

were worried about damage caused by rumors over the dumping of the water into

the sea, such as over exaggerated claims about the effects. Of them, 48 percent

were “greatly” worried while 39 percent were worried “to a certain degree.”

The government continues to hold explanatory

briefings about the water-dumping policy at local sites, but the effort has not

reduced the people’s concerns.

The respondents were also asked whether the

government should be held responsible for failing to prevent the nuclear

disaster from occurring. Eighty-four percent agreed, including 33 percent who

said the state has “great responsibility” and 51 percent who cited “a certain

degree of responsibility.”

Forty-five percent of respondents in their 60s

and 44 percent aged 70 or older said the government was “greatly responsible.”

Twenty-eight percent of respondents gave high

marks to the government’s response so far to the nuclear disaster, while 50

percent had low evaluations.

As for TEPCO, 39 percent said the utility has

acted responsibly over the 10 years since the accident, compared with 43

percent who said, “It hasn’t.”

And only 32 percent of respondents said the

country has learned lessons from the nuclear accident, while 57 percent said it

has not.

All nuclear reactors in Japan were shut down

following the Fukushima disaster. Much tougher safety standards were

established, and some reactors have been brought back online.

Sixteen percent of the Fukushima residents

approved restarts of nuclear plants while 69 percent said they should remain

offline.

Nationwide, 32 percent were in favor of the

restarts and 53 percent were against, according to a phone survey conducted on

Feb. 13 and 14 that showed opposition is higher in Fukushima Prefecture.

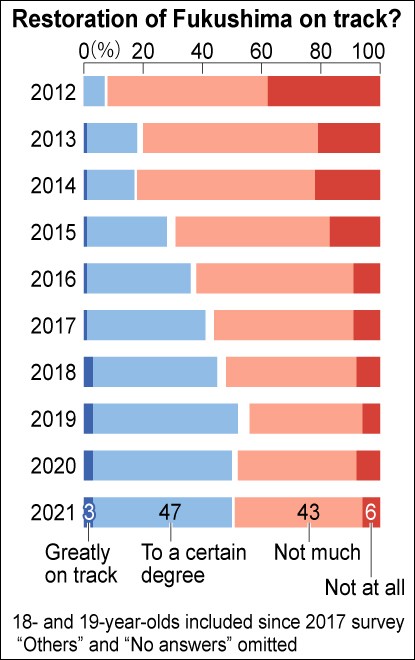

Half of the Fukushima respondents said

restoration of the prefecture was on track, including 3 percent who said

“greatly” and 47 percent who said “to a certain degree.”

In the 2012 survey, 7 percent said restoration

was on track. The ratio jumped to 36 percent in 2016.

In the 2019 survey, conducted a year after most

of the decontamination work was completed in the prefecture, the figure

increased to 52 percent, but it has since remained at around the same level.

Sixteen percent of respondents said they feel

“great” anxiety over the effects of radioactive materials released in the

accident on themselves and their families, while 48 percent felt a “certain

degree” of anxiety.

The overall ratio of 64 percent was down from

91 percent in September 2011 and 68 percent in 2016. But the latest figure was

up from 56 percent in 2020.

By sex, 69 percent of female respondents and 59

percent of males felt anxious about the radioactive fallout.

In addition, 79 percent of all respondents were

worried that the public will lose interest in the plight of the victims of the

nuclear accident. Of them, 34 percent were “greatly” worried and 45 percent

were worried “to a certain degree.” Nineteen percent were not worried very much

or not at all.

Fifty percent think the image of Fukushima

Prefecture has been restored to the pre-disaster level, but only 4 percent

“largely” believe this is the case.

The overall figure has improved from 30 percent

in the 2016 survey.

But the nationwide survey on Feb. 13 and 14

showed that only 40 percent believe that Fukushima Prefecture’s image has been

restored.

The survey used home phone numbers for voters

in Fukushima Prefecture, excluding some areas, selected at random by computer.

It received valid responses from 1,049, or 54 percent, of the 1,955 voters

contacted.

(Asahi Shimbun)

February 24, 2021

Source: http://www.asahi.com/ajw/articles/14216668

679-43-02/Poll

More Than Six In Ten Urban Indians Do Not Mind Watching Ads In Exchange For Free Content

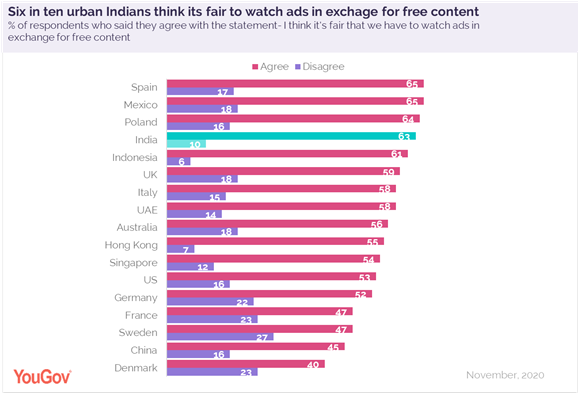

YouGov’s latest global report reveals more than six in ten urban Indians (63%) think it is fair to watch ads in exchange for free content.

The report, titled ‘International Media Consumption Report 2021- Is there a new normal?’ provides an analysis of the global media landscape across 17 markets.

Across the globe, a plurality of consumers in the 17 markets favour the idea of watching advertisements in exchange for free content. Along with India, countries such as Mexico (65%), Spain (65%) and Poland (64%) highly favour this idea.

Support is comparatively lower in France (47%), Sweden (47%) and Denmark (40%), but even in these markets, only around a quarter consider watching advertising in exchange for free-content to be unfair.

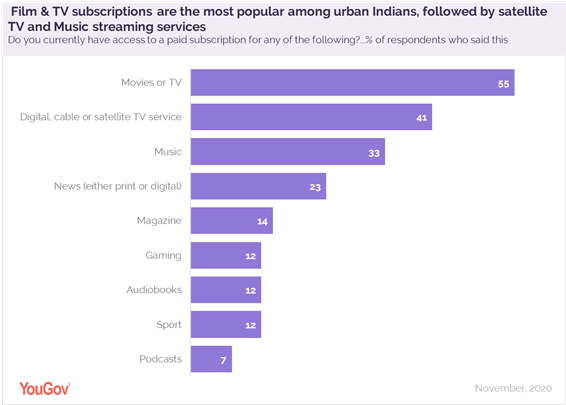

For many people, COVID-19 meant spending more time at home. That translated into more time watching content - such as live TV, on-demand and streamed video. Across the globe, film and TV subscriptions such as Netflix, AppleTV+ or HBO Max are the most popular by some distance in every market featured in the study, in most, a majority of consumers have signed up to one of these services.

Music streaming services such as Spotify and digital, cable, or satellite TV subscriptions alternate between second and third place depending on the market. For all these international comparisons, it is worth bearing in mind that in some markets our sample is nationally representative, while in others it is online or urban representative.

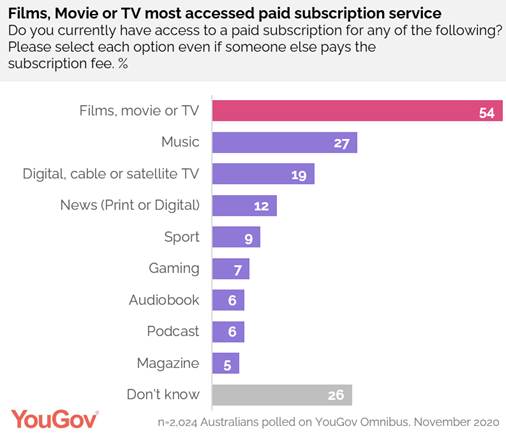

In India, 55% of urban Indians are signed up to a film or TV subscription. Digital/ satellite TV services are the next most popular- at 41%, second highest in the world after Mexico. Music subscriptions rank third- with one in three (33%) subscribing to a paid version of a music streaming platform.

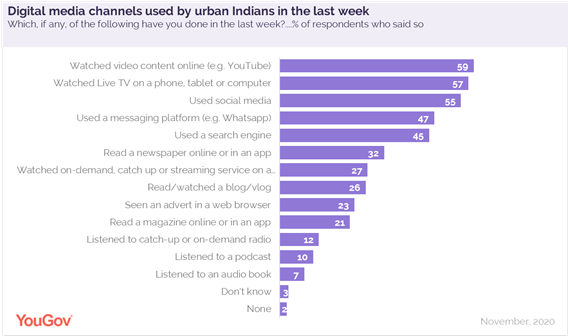

Our data shows that when global consumers were asked about the kinds of traditional media they have used in the past week, live TV came out on top. Across most of the 17 markets, over half of respondents consumed it – with the only exceptions being the UAE, Singapore, and China.

Print sits in the middle of the international pack and is particularly popular in India – where 46% of our nationally urban representative sample read a newspaper.

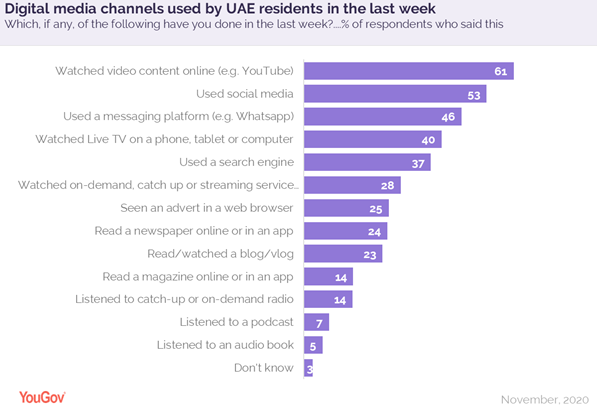

When asked about the digital media channels they used in the past week, a majority of respondents in most markets said they had used a search engine, logged on to social media, or seen video content online.

Large proportions also said they had communicated via messaging services, viewed content-streaming platforms, or watched live TV on their phone, tablet, or computer.

Urban Indians were the most likely among other markets to say they watched live TV on their phone, tablet or computer in the past week- at 57%. This trend is similar across age groups: majorities within most categories claim to have watched live TV in the last week, except for the 55+ group, where consumption is slightly lower - at 47%.

Consumption of online video content (59%) and social media (55%) was also high among urban Indians in the past week.

A third read a newspaper online or in an app (32%) but fewer read a magazine digitally (21%).

Consumption of radio, podcast and audiobooks was much lower and very few consumed these formats during that period.

Commenting on the report, Julian Newby, Sector Head of Media at YouGov, said: “Covid-19 has had a dramatic impact on consumer behaviour globally, and in turn, on media consumption habits. With a pandemic keeping more people indoors than ever before, digital media assumed greater importance as a means of keeping the public informed and entertained. Even then, certain traditional media formats remained popular among the masses. Our data shows that there are huge challenges for brands and advertisers looking to achieve ROI and effectively reach consumers in the right channels, at the right time, with the right message. Reliable, up-to-date insight can provide an early window into behaviour change to inform effective media planning and campaign development.”

(YouGov India)

February 25, 2021

Source: https://in.yougov.com/en-hi/news/2021/02/25/more-six-ten-urban-indians-do-not-mind-watching-ad/

679-43-03/Poll

One In Five Singaporean Gen Z-Ers Willing To Exchange Personal Data For Free Content

The pandemic has left most Singaporeans stranded at home and turning to their screens to keep them entertained. However, advertisers have seen their budgets cut or paused as sales continue to plunge.

YouGov’s new ‘International media consumption report 2021: Is there a new normal?’ white paper examines Singaporeans generational attitudes towards paid content.

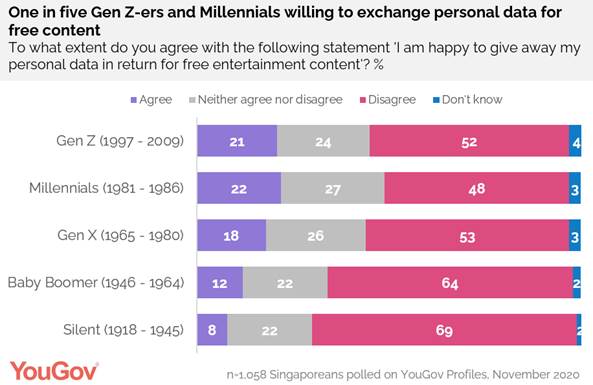

While personal data and privacy concerns have become a growing concern, one in six (16%) Singaporeans agree that they are willing to give up their personal data for free content. Men are twice as willing compared to women (21% vs. 11%). Over half (55%) are unwilling and a quarter (25%) are undecided.

The data also shows that attitudes towards exchanging personal data for free content is generational. While over two in ten Gen Z-ers (21%) and Millennials (22%) are happy to give away their data, this drops to about one in ten amongst Baby Boomers (12%) and the Silent Generation (8%).

‘International media consumption report 2021: Is there a new normal?’ provides a high-level analysis of consumers’ attitudes and behaviours around the international media landscape as the sector enters a pivotal time. The white paper is based on more than 18,000 interviews across 17 global markets and explores traditional media, digital media, advertising, subscriptions and the impact of COVID-19, with the overall aim of providing a sharp tool for media planners in an uncertain time.</yougov’s>

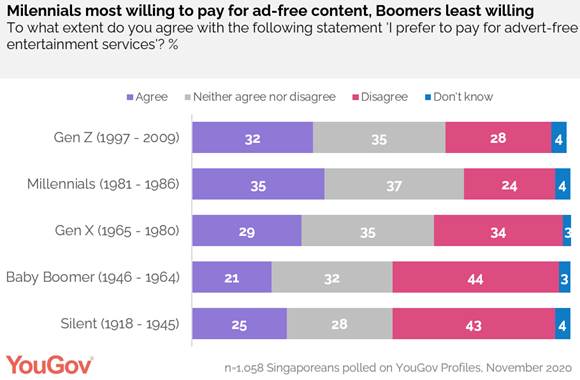

The research finds that while some are happy to give up personal data for free content, some prefer to pay for uninterrupted entertainment services, with one in five (20%) Singaporeans preferring to pay for ad-free content. Singaporean males are more likely to do so than women (24% vs. 16%). Two in five (40%) prefer not to pay for ad-free content, and over a third (37%) are on the fence.

Again, willingness for paying to be free of ads depends much on generation. Millennials are the most willing (35%), while Baby Boomers (21%) are the least willing.

As a whole, over more than half (55%) agree that it is fair to watch ads in exchange for free content. One in ten (12%) disagree and the jury is still out for a third (33%) of the population.

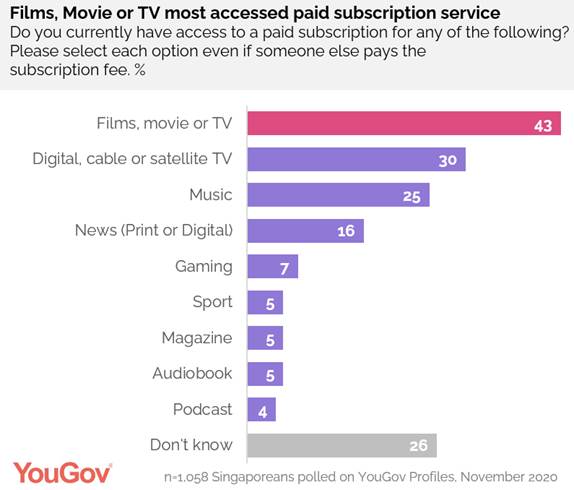

The most accessed paid subscription service amongst Singaporeans is for films, movies or TV, with two in five (43%) having access to a paid subscription. This is followed by digital, cable or satellite TV (30%) and music (25%). Millennials are the most likely to have paid access to films, movie or TV subscription (51%), and Gen Z-ers are the most likely to have paid access to music, with over half (55%) saying they do. While Baby Boomers lag behind in paid access to media subscriptions as a whole, there is one channel that has gained favour – digital, cable or satellite TV service (35%).

Commenting on the report, Julian Newby, Sector Head of Media at YouGov, said: “With most of the world spending the past year at home under lockdown, we looked at attitudes towards paid content amongst Singaporeans, and found out how this differs from generation to generation. Perhaps unsurprisingly, the TikTok generation (Gen Z-ers) are happy to give away personal data for free content, while the older generation remain more hesitant. There is also a generational gap in terms of paid media channels, with Baby Boomers dominating satellite TV and millennials for films and movies. Whatever channel it is, we hope that this data will useful for those in an increasingly competitive media landscape in making better decision for ad spend in the coming year.”

(YouGov Singapore)

February 26, 2021

Source: https://sg.yougov.com/en-sg/news/2021/02/26/one-five-singaporean-gen-z-ers-willing-exchange-pe/

MENA

679-43-04/Poll

Iranian

Public Opinion In The Biden Era

University of Maryland CISSM has conducted its most recent study based on two consecutive waves of nationally representative surveys that were conducted in Iran by IranPoll for the University of Maryland. University of Maryland CISSM was responsible for designing the questionnaires, getting feedback on them from relevant policy experts and practitioners, performing the analysis, and putting together the final report.

IranPoll partially sponsored the collection of these surveys through “IranPoll Opinion Research Support Fund in Memory of Professor Thomas Schelling”.

Survey results were released on Feb 24, 2021 at an event hosted by the Atlantic Council (Washington DC). The surveys cover a wide range of issues, including the impact of the pandemic, Iran’s regional involvements, attitudes toward the JCPOA and its future, and current political and economic state of affairs in Iran.

The study is based on two probability sample nationally representative telephone surveys. The fieldwork for first wave was conducted in October 2020 (Sept. 1 – Oct. 2, 2020) and the second wave in February 2021 (Jan. 26 – Feb. 6, 2021), among a representative sample of about 1000 Iranians per each wave. The margin of error for both surveys is about +/- 3.1%. The AAPOR2 contact rate of the October 2020 survey was 76%. The AAPOR2 cooperation rate of the survey was 81%. The overall response rate of the survey based on AAPOR2 was 60%. The AAPOR2 contact rate of the February 2021 survey was 83%. The AAPOR2 cooperation rate of the survey was 82%. The overall response rate of the survey based on AAPOR2 was 64%. Surveys were conducted using IranPoll’s standard nationally representative probabilistic sampling as detailed here.

MAIN

FINDINGS:

Below please find the results of this survey in greater detail:

- The frequency tables of survey results.

- The presentation of the results by University of Maryland CISSM at the Atlantic Council could be watched here.

- The report written based on the survey results by University of Maryland CISSM.

- Charts showing some of the results created by University of Maryland CISSM are available below.

(Iran Poll)

Source: https://www.iranpoll.com/publications/biden

AFRICA

679-43-05/Poll

Top Most Important Things Nigerians Want From Their President

Market Trends International International

(MTI), conducted a study across the six geo-political regions covering

urban and rural areas. A total of 10,000 interviews were conducted.

The sample distribution was proportionate to the population of each State and

respondents were randomly selected.

Provision of full security cover for all Nigerians (31%) and creation of job opportunities for youths (21%) topped the list of the most important things Nigerians want from their President. Over the last decade, insecurity has been ravaging all the nocks and crannies of Nigeria. This takes different diverse – insurgency, kidnapping, armed robbery, cultism, Fulani’s herdsmen attack on farmers, ritual killing and activities of militant groups.

Notably, unemployment rate is on the increase as more youths graduate from schools every year to add to the millions of youths that are seeking for gainful employment. This has direct correlation with the high insecurity in the country because ‘an idle mind is the devil workshop’.

Other key issues unveiled from the study were: provision of 24/7 electricity (16%), wipe out corruption (14%), sound economy (11%) and build well equipped health facilities (7%).

Findings from the study also revealed that over half of adult population (62%) have permanent voter card (PVC). There could be some people that have registered, but are yet to collect theirs.

(Market Trends International)

February 21, 2021

Source: http://www.markettrends-int.com/top-most-important-things-nigerians-want-from-their-president/

WEST EUROPE

679-43-06/Poll

35% Of British Public See a Decrease In UK And EU Relatinship

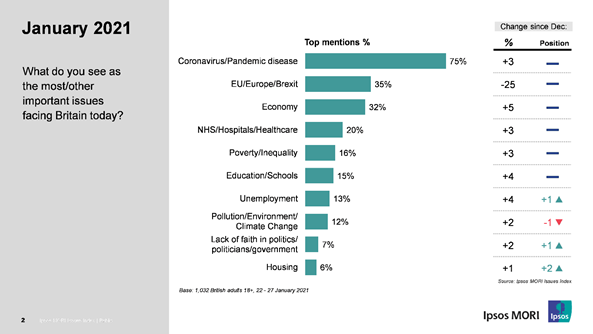

The January 2021 Ipsos MORI Issues Index shows a sharp slump in concern about Brexit, although it remains the second biggest issue for the nation. Thirty-five per cent of the British public see the UK's relationship with the EU as a significant concern, a decrease of 25 percentage points since December 2020.

In the first wave of the index conducted during the third national lockdown in England, the proportion of Britons who cite covid-19 as a big issue facing the country remains unchanged from previous months. Three-quarters mention the pandemic as one of their biggest worries – the same level of concern that has been recorded in every month since June 2020.

There has been a surge in the proportion who see Coronavirus as the single biggest issue for the nation however: 61% say this, up from 47% in December last year and the highest score on this measure since July 2020.

Concern about the economy is the third biggest issue for Britons this month, rising five percentage points to 32%. There have also been increases in public concern about the NHS, poverty/inequality, education and unemployment.

In the first month outside of the

European Union, the proportion of the public who see relations with Europe as a

big issue for Britain has fallen sharply.

In the first month outside of the

European Union, the proportion of the public who see relations with Europe as a

big issue for Britain has fallen sharply.

The drop between December and January has been especially notable for some groups. For instance, although the youngest show the lowest absolute level of concern in January (20% of 18-24 year olds mention Brexit, down from 42% in December), the largest drop has been among the oldest. The proportion of over 65s mentioning Brexit has fallen from 64% in December to 29% in January

Mike Clemence, a researcher at Ipsos MORI, said:

After the last-minute

agreement of an EU-UK trade deal last month it is no surprise to see that the

public’s level of concern about Brexit has fallen. However, many are still

worried and it remains the second-biggest issue for Britons.

The public also continue to sustain a high level of worry about the COVID-19 pandemic.

While the overall level of concern remains at the same level we’ve seen since

June 2020 in this first survey wave during the third national lockdown in

England we record a big jump in the proportion of the public who see the

pandemic as the single biggest issue facing the country, recovering from a drop

off in concern over December.

Technical note

- Since May 2020 the Issues Index has been conducted over the phone; lockdown conditions mean face-to-face fieldwork is currently not an option for public opinion polling. Mode effects should be kept in mind when comparing the new data points with previous months.

- Ipsos MORI's Issues Index is conducted monthly and provides an overview of the key issues concerning the country. Ipsos MORI interviewed a representative sample of 1,032 adults aged 18+ across Great Britain. The answers are spontaneous responses, and participants are not prompted with any answers.

- Ipsos MORI's telephone omnibus was used for this survey. Interviews were conducted between 22 and 27 January 2021 across Great Britain. Data are weighted to match the profile of the population.

(Ipsos MORI)

22 February 2021

Source: https://www.ipsos.com/ipsos-mori/en-uk/ipsos-mori-issues-index-january-2021

679-43-07/Poll

Latest Findings From Antibody Surveillance Study Published

- Over 154,000 participants took part in a home surveillance study for COVID-19 antibodies between 26 January and 8 February

- Findings published by Imperial College London and Ipsos MORI show 13.9% of the population in England had antibodies against COVID-19

- 17,000 participants had received at least one dose of a COVID-19 vaccine, with 91% of people across all ages testing positive for antibodies after two doses of the Pfizer vaccine

- Overall vaccine confidence is high with 92% having accepted or planning to accept a vaccine offer

Imperial College London and Ipsos MORI have today published their latest antibody surveillance report tracking COVID-19 infection across England.

For the first time, the study captures participants who have received a COVID-19 vaccine, and also gathers insight into how different groups feel about vaccines.

Over 154,000 participants tested themselves at home using a finger prick test between 26 January and 8 February, showing 13.9% of the population had antibodies either from infection or vaccination.

Of these participants, over 17,000 said they had received at least one COVID-19 vaccine dose. The data shows 87.9% of people over the age of 80 tested positive for antibodies after two doses of the Pfizer-BioNTech vaccine, rising to 95.5% for those under the age of 60 and 100% in those aged under 30.

The findings show high confidence levels in the vaccine. Over 90% of those surveyed reported that they would be willing to accept, or had already had a vaccination for COVID-19.

Today’s report provides insight on antibody responses following infection, or for some participants, vaccination. It does not provide insight on other elements of immune responses following vaccination – such as the presence of T-cells - nor does it assess vaccine effectiveness, including whether a vaccine prevents severe disease, hospitalisation or death.

Health and Social Care Secretary Matt Hancock said:

These findings shed more

light on rates of antibodies across the UK and among different groups, as we

continue to strengthen our understanding of COVID-19.

It is fantastic to see over

90% of people surveyed would accept or had already accepted a vaccine, as we

continue to expand the roll-out.

I urge anyone who has been

invited for a vaccine to book an appointment. And while we are seeing rates of

the virus gradually decline it is important we all hold our resolve and follow

the rules as we deliver on our cautious but irreversible approach to easing

lockdown.

Key findings:

- Over 154,000 participants took the antibody test, with 13.9% testing positive for antibodies among vaccinated and unvaccinated people;

- Antibody prevalence in unvaccinated people remains highest in London (16.9%), and in people of black (22.1%) and Asian (20%) ethnicities, and those aged 18-24 years (14.5%);

- Over 17,000 participants said they had received one or more vaccine doses, with the majority receiving the Pfizer-BioNTech vaccine;

- After two doses of the Pfizer-BioNTech vaccine, the proportion of participants who tested positive for antibodies was high across all age groups (100% in those under 30, and 87.9% in those 80 and over);

- For individuals who received a single dose of the Pfizer-BioNTech vaccine after 21 days, the proportion testing positive for antibodies was 94.7% in those under 30; the proportion testing positive was lower at older ages ranging from 73.7% at 60 to 64 years to 34.7% in those aged 80 and over;

- Overall vaccine confidence is high, with 92% having accepted or planning to accept a vaccine offer; and

- Vaccine confidence varied by age, sex and also by ethnicity, highest in those of white (92.6%) and lowest of Black (72.5%) ethnicity.

The findings on antibody response following a single dose align with existing research that suggests those aged over 80 take longer to develop an antibody response to infection and the immune response is not as strong.

Antibodies are just one component of the body’s immune response produced by COVID-19 infection or vaccination. Vaccines also induce T-cell related protection, independent of antibody production. T-cell responses may vary significantly between vaccines and may be particularly important in influencing duration of protection.

The Joint Committee on Vaccination and Immunisation (JCVI) noted that in Pfizer’s clinical trial, protection against coronavirus was very high (89%) between 14 and 21 days after vaccination, despite very low levels of antibodies measured at the same time. This suggests that early antibody response does not correlate with clinical protection.

There is still insufficient information to say how protected a person may be from COVID-19 based on a positive antibody test result, and it does not mean they are immune. It is vital everyone continues to follow the rules in order to keep themselves and those around them safe.

Data from a Public Health Scotland study published this week has found that hospital admissions four weeks after the first dose were reduced by 85% and 94% for the Pfizer and AstraZeneca jabs respectively. Public Health England’s SIREN study also shows good evidence that the Pfizer-BioNTech vaccine helps to interrupt virus transmission, and that one dose is effective against the virus from three to four weeks after the first dose.

PHE’s analysis of routine testing data also shows that one dose is 57% effective against symptomatic COVID-19 disease in those aged over 80. This effect occurs from about 3 to 4 weeks after the first dose. Early data suggests the second dose in over 80s improves protection against symptomatic disease by a further 30%, to more than 85%.

Professor Helen Ward, lead author for the REACT study of population prevalence, said:

It is very encouraging to

see that uptake and confidence in the vaccination programme

is so high, and that most people develop a detectable antibody response after

one dose. Our findings suggest that it is very important for people to take up

the second dose when it is offered. We know that some groups have concerns

about the vaccine, including some people at increased risk from COVID-19, so it

is really important that they have opportunities to discuss these and find out

more.

Kelly Beaver, Managing Director – Public Affairs, Ipsos MORI said:

It’s deeply encouraging to

see such high levels of positivity towards receiving a COVID-19 vaccine among

the population in our latest REACT study. That combined with our findings on

the antibody response in those vaccinated show a cause for cautious optimism.

The study uses a finger prick device to use at home and can tell someone if they tested positive for antibodies in under 15 minutes. Some studies, including the PHE antibody surveillance studies, take a larger sample of blood to analyse in the lab.

The REACT antibody data follows preliminary data from PHE on vaccine effectiveness showing clear protection from the first vaccine dose, particularly against severe disease. It supports the decision to maximise the number of people vaccinated with a single dose and delay a second dose.

The government and the NHS are working hard to encourage people in all communities to come forward and accept the offer of a jab. This includes working closely with the NHS and faith and community groups, to support and reach people who are eligible for a vaccine, by providing advice and information in over thirteen languages. Over £23 million funding has already been allocated through the Community Champions scheme to 60 councils and voluntary groups across England to expand work to support those most at risk from COVID-19 and boost vaccine take up.

(Ipsos MORI)

25 February 2021

Source: https://www.ipsos.com/ipsos-mori/en-uk/latest-findings-antibody-surveillance-study-published

679-43-08/Poll

Support For Scottish Independence Falls Back

Ipsos MORI’s Scottish Political Monitor, run in partnership with STV News, finds that the SNP are still in pole position ahead of May’s Holyrood elections. However, support for Scottish independence has fallen since last November - by four percentage points. The First Minister’s satisfaction ratings have also dropped since last October, although they remain the highest of any of the party leaders.

- 52% say they are likely to vote for the SNP in the constituency vote, while 23% will vote for the Scottish Conservatives and 15% for Scottish Labour;

- 52% would vote Yes in an independence referendum, slipping slightly from 56% in November - while 48% would vote No;

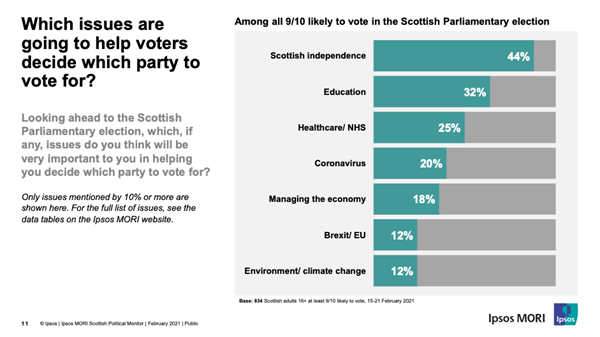

- Scottish independence is seen as the most important issue in helping people decide which party to vote for (44%), followed by education (32%), healthcare/ NHS (25%) and coronavirus (20%).

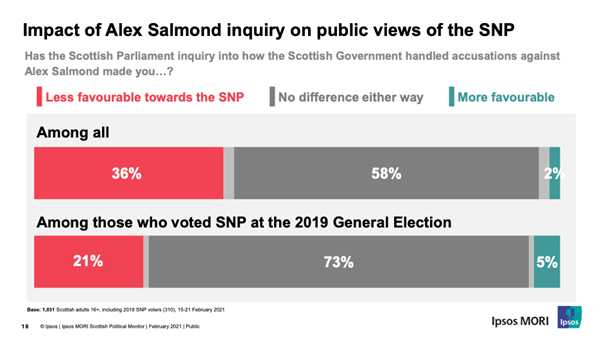

- Over a third of Scots (36%) say the Holyrood inquiry into the Scottish Government’s handling of the accusations against Alex Salmond has made them less favourable towards the SNP, although most (58%) say it has made no difference to their view of the party.

Scottish Parliament voting

intention

The SNP retains a very comfortable lead in voting intention for both constituency and list votes in next May’s Scottish Parliament elections, with the Conservatives in second place and Labour in third.

Headline Scottish Parliament voting intention figures for the constituency vote are:

- SNP: 52% (-3 compared with 20-26 November)

- Scottish Conservatives: 23% (+1)

- Scottish Labour: 15% (+1)

- Scottish Liberal Democrats: 5% (-1)

- Scottish Green Party: 3% (+2)

- Other: 2% (unchanged)

Headline Scottish Parliament voting intention figures for the regional vote are:

- SNP: 47% (unchanged)

- Scottish Conservatives: 22% (unchanged)

- Scottish Labour: 14% (-2)

- Scottish Green Party: 8% (+1)

- Scottish Liberal Democrats: 6% (unchanged)

- Other: 3% (+1)

Three in ten (31%) say they may change their mind about which party they’ll cast their constituency vote for:

- Those who say they’ll vote SNP or Conservative are surer of their vote than those voting Labour. Labour voters who may change their mind are most likely to consider the SNP, while SNP voters who may change their mind are most likely to consider Labour.

Top issues for voters

- Independence is seen as the top issue helping voters decide which party they’ll vote for, with 44% mentioning it (note these are spontaneous, top-of-mind responses, not prompted).

- Independence is followed by education (mentioned by 32% of voters), the NHS (25%), coronavirus (20%) and the economy (18%).

Salmond inquiry

There are signs that the Holyrood inquiry into the Scottish Government’s handling of the accusations against Alex Salmond is starting to impact on voters’ perceptions of the SNP.

- Over a third of Scots (36%) say the inquiry has made them less favourable towards the SNP, although most (58%) say it has made no difference to their view of the party.

- Among those who voted SNP at the last General Election, one in five (21%) say it has made them less favourable towards the SNP.

Scottish independence

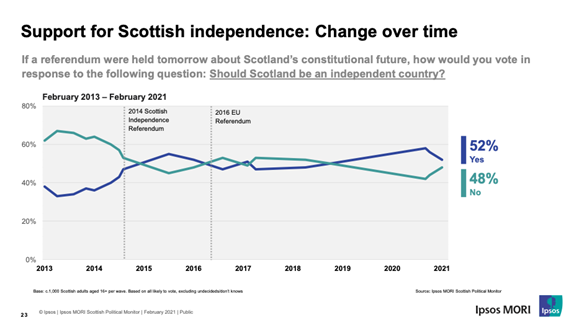

- Support for independence has slipped, although Yes retains a narrow lead. Among those who would be likely to vote in an independence referendum, 52% say they would vote Yes while 48% would vote No. This is lower than in November 2020, when Ipsos MORI/STV polling showed a larger Yes lead (56% Yes/ 44% No).

- Over half (56%) of Scots say that the UK Government should allow another independence referendum to be held within the next five years if the SNP wins a majority of seats in the 2021 Scottish Parliament elections – while 41% say that the UK Government should not allow this. Support for this has fallen by eight percentage points since October 2020.

- In the event that the SNP wins a majority of seats but the UK Government refuses to allow another independence referendum, two in five Scots (42%) say that the Scottish Government should accept that a referendum cannot be held in the next five years unless the UK Government changes its mind. A third (34%) think the Scottish Government should take the UK Government to court to try and establish a legal basis for holding a referendum, while 18% say the Scottish Government should hold another referendum anyway without the UK Government’s consent.

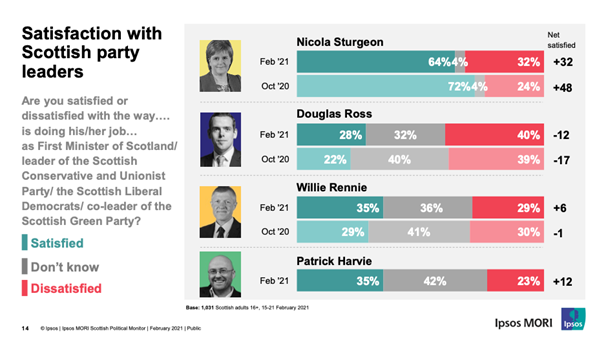

Party leaders

- Nicola Sturgeon remains the highest rated party leader among the Scottish public, with a ‘net’ satisfaction rating of +32 – although this is 16 points lower than when Ipsos MORI and STV last polled on this in October 2020.

- Scots are split on whether Anas Sarwar or Monica Lennon would make the best leader for Scottish Labour - 28% say Sarwar would be the best leader and 25% favour Lennon, while 44% don’t know.

- Among those who say they would vote Labour in May, Sarwar enjoys a narrow lead, with 40% saying he would be the best leader compared with 35% who say the same of Lennon.

Emily Gray, Managing Director of Ipsos MORI Scotland, commented:

This latest poll from Ipsos

MORI and STV News shows a fall in support for

independence, and a corresponding increase in support for staying in the Union

– though Yes still has a four-point lead over No. That’s important for

Scotland’s political parties, since independence is the top issue voters say

will help them make up their minds about which party to vote for in May’s

Holyrood elections. At this point the SNP look on course to win a majority of

seats, but the next few weeks are set to be challenging for the party, with the

Salmond inquiry ongoing – and our poll shows that this issue has started to cut

through with Scottish voters.

(Ipsos MORI)

25 February 2021

Source: https://www.ipsos.com/ipsos-mori/en-uk/support-scottish-independence-falls-back

679-43-09/Poll

The Boom In Online Shopping And Delivery Services

Since the beginning of 2020, the health crisis has profoundly changed the consumption patterns of the French. Boom in online shopping and delivery services, changes in purchasing criteria… discover below a study devoted to French people who say they have made online purchases during the last 12 months.

An increase in online shopping

9 out of 10 French people say they have bought at least one product online in the past 12 months (90%). More specifically, 41% say they made purchases in the week preceding the survey, a figure drawn on the rise by women (47%) and 25-34 year olds (51%).

Among the French who say they have made purchases on the internet in the past 12 months:

- 37% indicate ordering more often than before the health crisis (42% of women vs. 32% of men)

- 39% say their average basket has increased since the start of the pandemic (42% of women vs. 35% of men)

The boom in delivery services

In view of COVID-19, 40% of respondents use home delivery more often, 28% use relay point delivery, and 23% use the click & collect service.

The most popular product categories

When polling consumers to find out the types of products purchased online in the past 12 months, clothing, footwear and accessories come out on top at 58% , followed by cultural products (47%) and high-tech products & household appliances (39%).

In detail, there are significant differences between men and women . Indeed, the latter are significantly more likely to have ordered clothes, shoes and accessories (66% vs. 49% of men), cultural products (52% vs. 40% of men) or even cosmetics (45% vs. . 25% of men). Conversely, men have turned more to high-tech products & household appliances (46% vs. 33% of women) and the DIY and gardening category (26% vs. 17% of women).

What are the main criteria for buying online?

In view of the current health context, delivery conditions are particularly important in the eyes of consumers. After the product price (59%), the cost of delivery (44%) and delivery times (37%) are the two most cited purchase criteria.

Have these online shopping criteria grown in importance due to the pandemic?

- Among those who cite Made in France , 73% consider that this criterion has been more important since the start of the health crisis

- Among those who cite promotions , 61% indicate that this criterion has been more important since the start of the health crisis

- Among those who cite the price of delivery , 48% say that this criterion has been more important since the start of the health crisis

- Among those who cite the price of the product , 40% say that this criterion has been more important since the start of the health crisis

Methodology :

Omnibus study carried out from January 19 to 21, 2021 among 1,017 people representative of the national population aged 18 and over, according to the quota method.

(YouGov France)

February 25, 2021

Source: https://fr.yougov.com/news/2021/02/25/boom-achats-en-ligne-et-services-de-livraison/

679-43-10/Poll

Health Barometer # 4 - Yougov X 20 Minutes X Doctissimo

Nearly 3 in 4 French people (73%) say they are worried about the arrival of new variants of the coronavirus (English, South African, etc.). Faced with these variants, the main source of concern observed is contagiousness (36%), followed by the effectiveness of vaccines (28%) .

Strong increase in the desire of the French to be vaccinated

Up again this month, 54% of French people say they will get vaccinated as soon as they are affected (+4 points). The French not wishing to be vaccinated evoke the lack of perspective on the effectiveness of the vaccine (71%), the fear of side effects (50%) and the fact of being against vaccines in general (15%).

The habits of the French during this period

Nearly one in 2 French people say they pay more attention to their diet and lifestyle in order to protect themselves from possible contamination (48%, -3 points) . However, only 44% of French people say they have practiced regular physical activity over the past two weeks (+4 points). In decline this month, the morale of the French is still impacted by the current context linked to COVID-19 (51%, -3 points).

Nearly 1 in 5 French people say they have canceled or postponed at least one medical appointment for fear of contracting the COVID-19 virus (21%, +1 point).

The “Tous Anti-Covid” application

To date, nearly 4 in 10 French people say they have downloaded the “Tous Anti-Covid” application.

* Any total or partial publication must imperatively use the following complete statement: "YouGov Barometer for 20 Minutes and Doctissimo".

The detailed results of the 4th edition of the barometer are available here

Access the analysis note of the 3rd edition of the barometer here

Methodology :

Omnibus study carried out from February 15 to 16, 2021 among 1,000 people representative of the French national population aged 18 and over, using the quota method.

(YouGov France)

February 25, 2021

Source: https://fr.yougov.com/news/2021/02/25/barometre-de-la-sante-4-yougov-x-20-minutes-x-doct/

679-43-11/Poll

Rare Diseases: Europeans And In Particular The French Do Not Accept Fatality

Rare diseases are not that much: one in 20 people say they have them (5%) and 3 in 10 people are affected by these diseases, directly or indirectly because they have a loved one (a child, a parent, a friend : 13%) or a fair knowledge (13%) suffering from a rare disease. This is particularly the case for more than a third of French people (34%).

Faced with what constitutes the reality of the painful journey of many parents of children suffering from rare diseases, many Europeans imagine that they would not agree to accept fatalism: if one of their relatives were suffering from a rare disease, 72% would not accept the impossibility of obtaining a diagnosis for several years (74% of French people) and 72% would also not admit to discovering that no research is being carried out to develop a treatment against this disease (75% of French people), considering in both cases that it is possible to act if all the actors concerned are mobilized.

They applaud the measures that could be put in place today to improve the care of patients with rare diseases and the support of their relatives: they consider it important or even essential to train health professionals when the announcement of the diagnosis (94% of Europeans, 95% of French people), to develop a “culture of doubt” by encouraging health professionals to take more account of the symptoms that parents describe to them, in order to reduce error or diagnostic error in children (91% of Europeans, 94% of French people) or to systematically screen at birth for rare diseases for which there is an effective treatment (90% of Europeans, 92% of French people).

Europeans are convinced that funding research projects on innovative treatments against rare diseases makes it possible to advance research for other diseases: 90% think so, and even 94% of French people.

They are also extremely in favor of accelerating the procedures for making innovative treatments available when there is a vital emergency (90% of Europeans and 93% of French people) and this is even for the majority of them. them essential.

(Ipsos France)

February 27, 2021

679-43-12/Poll

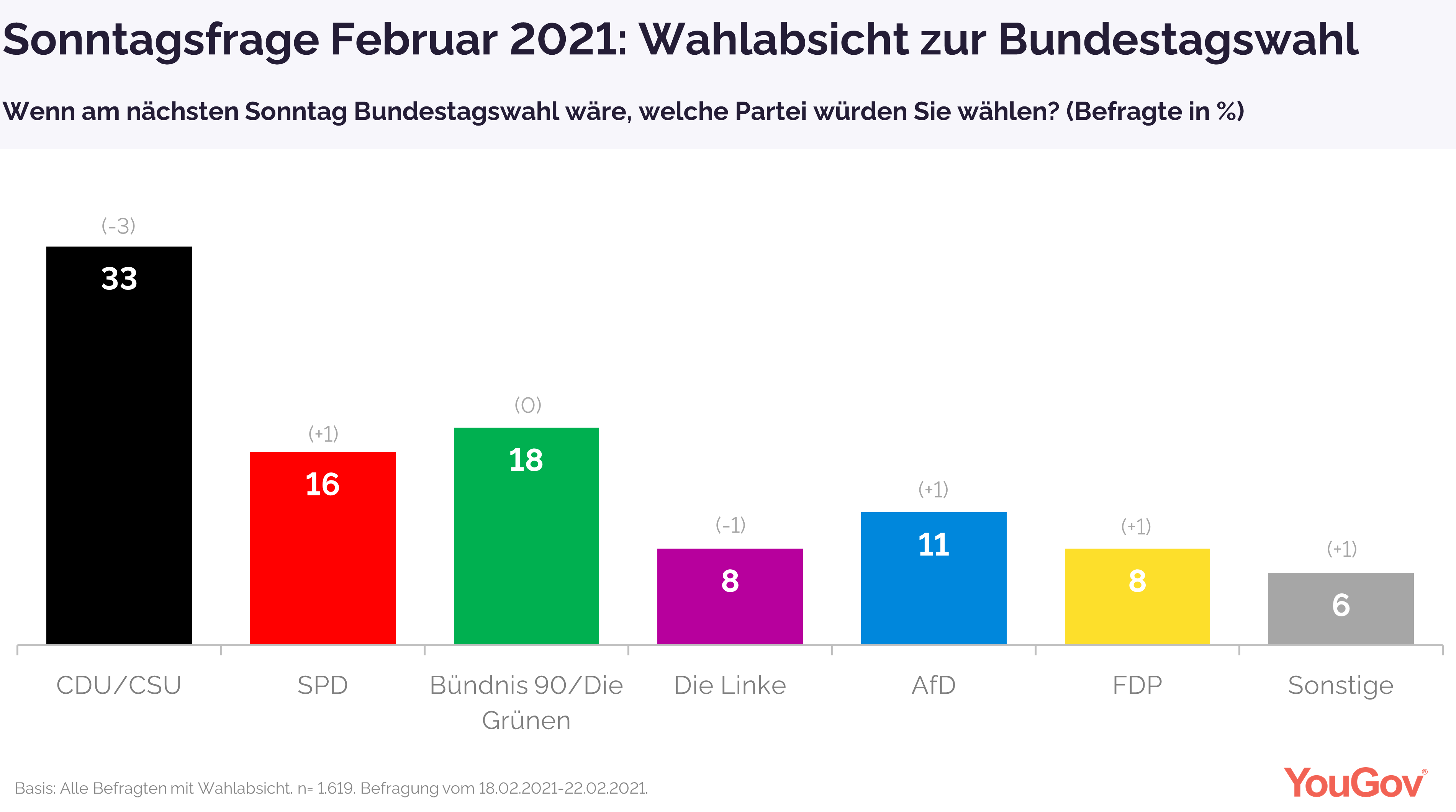

Sunday Question: 3 Percentage Points Loss At The CDU

Movement in voting intent -

losses in the Union and the Left, gains in the SPD, FDP and AfD

33 percent of the German citizens entitled to vote state that they will vote for the CDU / CSU if there would be a general election next Sunday. This value is 3 percentage points lower than in January 2021, making it the worst result in voting intent for the Union since the beginning of the Corona crisis. The result of the SPD, on the other hand, can make up one point: The Social Democrats landed at 16 percent in February.

The FDP was also able to gain another percentage point in February and landed at 8 percent. The AfD wins a point with a total of 11 percent. In addition to the CDU, the left is also losing and falling by one percentage point to 8 percent. Only the Greens remain unchanged in February at 18 percent. The other parties get 6 percent of the vote.

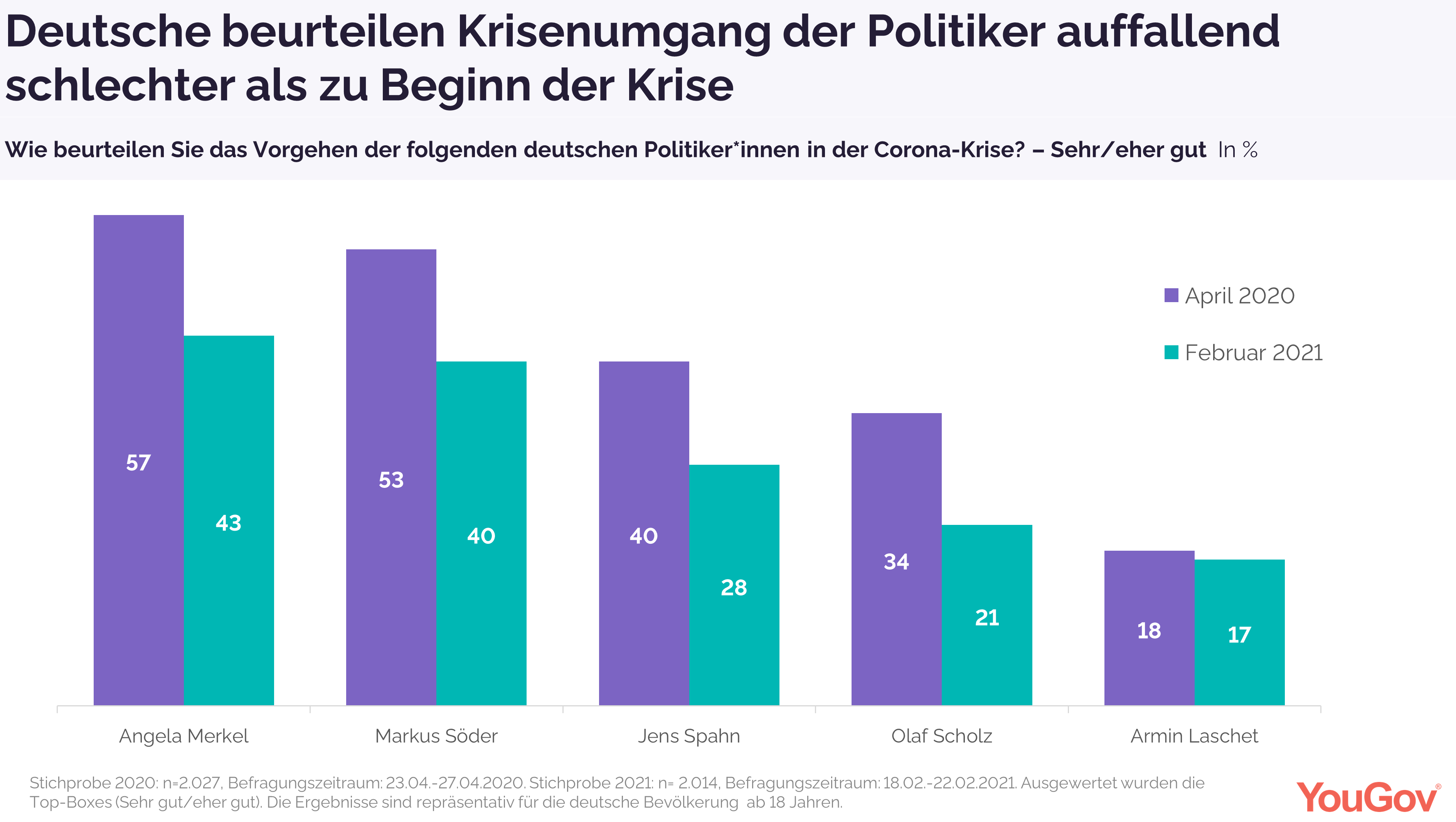

Germans judge politicians to deal with the crisis noticeably worse than at the beginning of the crisis

The assessment by the German that Chancellor Angela Merkel is handling the Corona crisis well is 43 percent in February 2021, 14 percentage points less than in April 2020, when 57 percent of those surveyed expressed their confidence in her. The assessment is not much different for Markus Söder, who in February only 40 percent attest to a good procedure (cf. 53 percent in April 2020). Olaf Scholz achieved 21 percent vs. 34 percent ten months ago, and trust in Jens Spahn also fell from 40 percent to 28 percent. Only Armin Laschet's values remain constant, but at a low level. In April 2020, 18 percent certified that the NRW Prime Minister had a good approach to the crisis, while 17 percent currently say so.

This is the result of the current Sunday question, for which 1,619 people out of 2,014 survey participants who are eligible to vote submitted their voting intention between February 18, 2021 and February 22, 2021.

(YouGov Denmark)

February 26, 2021

Source: https://yougov.de/news/2021/02/26/sonntagsfrage-3-prozentpunkte-verlust-bei-der-cdu/

679-43-13/Poll

International Study On Anti-Covid Rules: Italians Stopped At The Bare Minimum

A YouGov survey of nearly 19,000 people in 17 countries and regions shows us where people have worked hard to protect themselves from the spread of the virus.

Periodically in Italy, the transitions from orange to yellow areas see the pouring of many people into city centers, who "take advantage" of the newfound freedom causing crowds that generate controversy, but in fact do not violate the rules.

YouGov research has repeatedly shown that, at best, Italians stick to following the rules to the letter and rarely go any further - for example, our research on Christmas restrictions showed that 59% would have celebrated Christmas. with other people , although distancing is clear to all to be the only means to stop the infections. And sometimes they even border on violations: another research has shown that only half of Italians think that the people around them have been loyal to the anti-contagion prescriptions.

Today a new international YouGov survey, conducted in 17 countries, shows that 56% of Italians describe their approach to the coronavirus rules saying "I followed the rules when and in the way they were introduced, but I did not act in advance or done more than required by the government. ”This makes Italians the most likely to adopt the“ bare minimum ”approach in the practice of security measures , to the same extent as Singapore and Denmark.

The people of Hong Kong are more likely to go further when it comes to protecting yourself and others from illness. Six out of ten people (61%) said: " I took protective measures before the government said so and I went beyond what the government prescribed ."

Mexicans are the second to say they have gone beyond what the government demands, at 54%. This could be a legacy of the government's slow response in the early stages of the outbreak of the pandemic, as well as an indication of Mexicans overzealous - albeit in the recent study mentioned earlier, while 84% of Mexicans say they following the rules, only 30% say the same about people in their neighborhood - the biggest discrepancy observed.

Just over a third of Italians (36%) say they have done more than the government requested, while Poles and Americans are the most likely to say they have not heeded the rules. One in six people in each of these countries (17%) confessed that "they have only followed the rules I wanted to follow or that I think make sense, but otherwise I did what I wanted ".

(YouGov Italy)

February 23, 2021

Source: https://it.yougov.com/news/2021/02/23/covid-compliance/

679-43-14/Poll

On The Money: The Evolution Of The Banking And Insurance Sector In Italy

COVID-19 has impacted the financial sector globally, causing disruption in several markets, as well as between employees and consumers.

On the occasion of the publication of the new global Banking & Insurance 2021 study, in YouGov we investigated the impact of COVID-19 on the perception of Italian consumers of banks and insurance companies.

The accentuated gap in

advertising recollection