|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 693 Week:

May 31 –June 06, 2021 Presentation:

June 11, 2021 Only

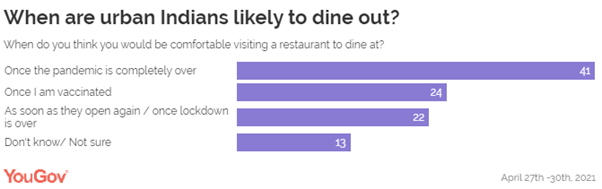

A Few (22%) Indians Are Likely To Dine Out Once Restaurants Re-Open Or The

Lockdown Is Lifted In

2020 80% Of Liberians Think That Country Is Going In Wrong Direction Ugandans

(50%) approved of COVID-19 lockdown despite difficulty complying 65%

Ugandans Are Of The View That COVID-19 Resources Are Lost Due To Corruption Environmental

Protection Is A Matter Close To The Heart For Seven Out Of Ten Germans 60%

Of U.S. Adults Favor The Death Penalty For People Convicted Of Murder Australian

Unemployment Increases To 10.3% In May – A Month After The End Of Jobkeeper Most

Of The Total Adult Population In The US (59%) And In The UK (72%) Are

Meat-Eaters Are

Consumers Moving Back To Offline Shopping? INTRODUCTORY NOTE

693-43-22/Commentary:

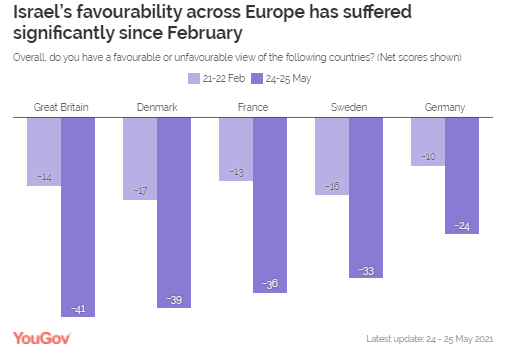

Israel

Is Least Favorable Amongst Britons, With Favorability Falling From -14 In

February To -41 In May Following Gaza Strikes

The ongoing

conflict between Israel and Palestine has recently flared

up again, with Israel executing air strikes on the

Gaza Strip, in response to rocket attacks by Hamas. With an estimated 243

lives lost – almost all civilian – both Hamas and Israel have now agreed to a ceasefire. Now new

YouGov Eurotrack data shows that Israel’s favourability across Europe has

suffered significantly since we last tested it in February, with net

favourability for the nation falling by at least 14 points in all countries

surveyed.

Of all the

countries surveyed, Israel is least favourable amongst Britons, with

favourability falling from -14 in February to -41 in May, its lowest rating

in Britain since we started asking this question in 2016. Israel’s

favourability is lowest amongst Labour voters, of whom only 13% view Israel

favourably, with 68% viewing the country unfavourably (a net score of -55).

Conservative voters view Israel more favourably, although perceptions are

still largely negative: 29% have a favourable impression of Israel while 53%

have an unfavourable impression (net -24). The next

highest fall in Israel’s favourability is seen in France, decreasing 23

points from -13 to -36, the country’s lowest favourability rating amongst the

French since May 2019. A similar fall can be seen in Denmark, experiencing a

22 point drop from -17 to -39. Sweden and Germany see the smallest falls in

favourability, at 17 and 14 points respectively. Germany stands out from the

rest of the countries surveyed with the highest net favourability rating for

Israel at-24, nine points higher than the next highest country (Sweden) at

-33. (YouGov UK) June 04,

2021 SUMMARY

OF POLLS

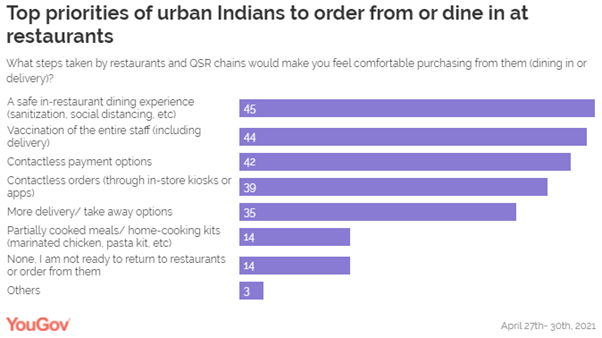

ASIA (India) Only A Few (22%) Indians Are Likely To Dine Out Once

Restaurants Re-Open Or The Lockdown Is Lifted Amid the fresh Covid19 outbreak, YouGov’s latest

survey reveals urban Indians prioritize vaccination of staff as much as a safe

dining experience when it comes to their comfort of buying food from a

restaurant or a QSR chain- either through delivery or dining-in. Many respondents said contactless

payment options and provisions for contactless orders (42% and 39%,

respectively) would make them feel relaxed buying from a restaurant in the

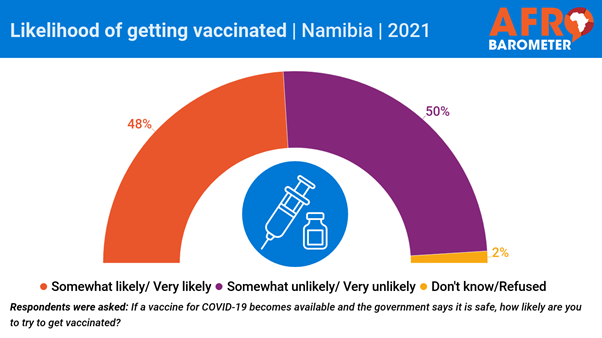

current scenario. (YouGov India) June 1, 2021 AFRICA (Namibia) 48 % Of Namibians Are Likely To Get Vaccinated If It Is

Available And Government Says Its Safe, 50% Are Unlikely Nearly all adult Namibians are worried

about the effects of the COVID-19 pandemic on their households, the country,

and the future of their children, according to a telephone survey by

Afrobarometer. But a majority of citizens have concerns about the safety of COVID-19

vaccines and believe that prayer is more effective than vaccines in

preventing COVID-19 infection. Only about half say they are likely to try to

get vaccinated. (Afrobarometer) 2 Jun 2021 (Liberia) In

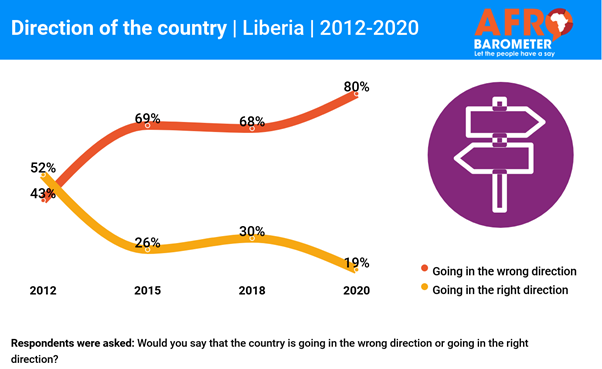

2020 80% Of Liberians Think That Country Is Going In Wrong Direction Liberians

generally hold gloomy views of the direction of the country, the country’s

economic condition, and their personal living conditions, the latest

Afrobarometer survey shows. An overwhelming majority – almost twice as many

as in 2012 – say the country is going in “the wrong direction,” and only

one-fourth of citizens assess the country’s economic condition as “fairly” or

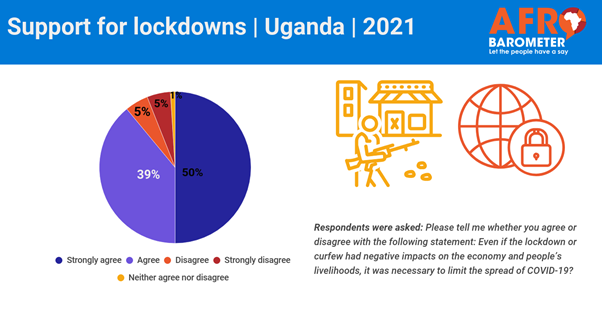

“very” good. (Afrobarometer) 3 Jun 2021 (Uganda) Ugandans (50%) approved of COVID-19 lockdown despite

difficulty complying Almost nine in 10 Ugandans say that last

year’s lockdown was necessary to limit the spread of COVID-19, in spite of

the toll it took on the economy and people’s livelihoods, the latest

Afrobarometer survey shows. Two-thirds say they found it difficult to comply

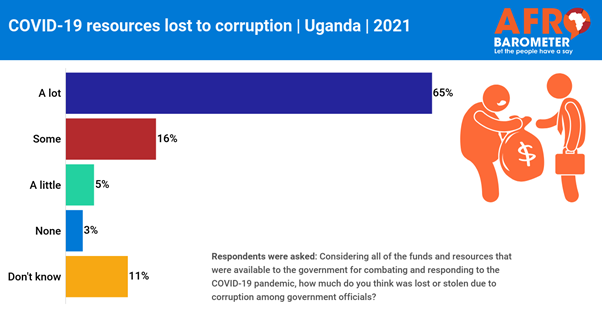

with lockdown restrictions or curfews imposed by the government. (Afrobarometer) 4 Jun 2021 65% Ugandans Are Of The View That COVID-19 Resources Are

Lost Due To Corruption A new Afrobarometer survey in Uganda shows

that a majority of citizens approve of the government’s management of the

response to COVID-19, although many raise concerns about corruption. More

than three-quarters of Ugandans believe that at least some of the resources

available for responding to the pandemic were lost due to corruption among

government officials. Only about half of citizens say they trust government

statistics on COVID-19 cases and deaths. (Afrobarometer) 4 Jun 2021 WEST

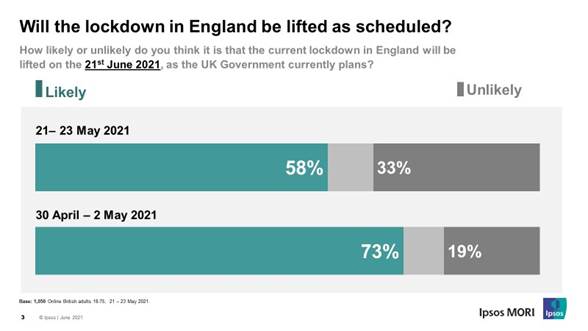

EUROPE (UK) Six In Ten Britons Still Expect Measures To Be Lifted On

21st June, But Optimism That Lockdown Will Be Lifted Has Fallen Over The

Month New polling by Ipsos MORI shows most people

are still hopeful for the lifting of current lockdown restrictions on 21st

June. Almost 6 in 10 (58%) believe it is likely that this will go ahead as

currently planned by the Government, while a third (33%) say it is unlikely,

in research carried out between 21-23 May. But while a majority remain

hopeful, there has been a significant drop over the month. When the same

question was asked at the beginning of May, almost three-quarters (73%) said

the lifting of restrictions on 21st June was likely, 15ppt more than those

who feel the same way now, while the proportion who think it is unlikely has

risen 14ppt. (Ipsos MORI) 1 June 2021 Two In Five Brits (42%) Say That Local Police Are Effective

At Providing Advice And Guidance To The Public A NEW Ipsos MORI survey shows that two in

five Brits (42%) say that local police are effective at providing advice and

guidance to the public and a similar proportion say they are effective at

responding when a member of the public calls (39%). But only around a quarter

(23%) say they are effective at protecting those online. On most measures of

effectiveness, there has been little change since 2017. (Ipsos MORI) 2 June 2021 53% Of People Think Changes To The National Curriculum

Should Be A Part Of A Hypothetical Overhaul Of The Schooling System The Education Recovery Commissioner Sir

Kevan Collins has resigned after his plans for education reform

to help students catch up following the pandemic were rejected by the government. Some

53% of people think changes to the national curriculum should be a part of a

hypothetical overhaul of the schooling system – including some 61% of parents

with children under 5. (More precise questions on how the curriculum is

handled and could be changed are covered in the next section). (YouGov UK) June 03, 2021 (Germany) Environmental Protection Is A Matter Close To The Heart For

Seven Out Of Ten Germans World Environment Day is celebrated on

Saturday, June 5th. For the majority of Germans, environmental

protection is important: 70 percent say that it is important to

them. Not surprisingly, this is what voters from the Greens are most

likely to say (91 percent). Also voters of the party "Die

Linke" (86 percent), the SPD (79 percent) and the Union (77 percent) are

more important than the general population. This was the result of a

current YouGov survey in cooperation with Statista. (YouGov Germany) June 2, 2021 (Spain) 52% Of The Spaniards Have Not Yet Planned Their Vacations

Since They Prefer To Wait To See How The Pandemic Evolves With the arrival of the month of June, many

are those who can no longer think of anything other than the summer holidays.

While last summer 24% of respondents decided not to go on vacation, this

year 100% of those interviewed affirm that they will. Despite this,

2 out of 3 admit that they have not yet booked their vacations, stating 52%

of them that they prefer to wait to see how the pandemic evolves to make sure

that everything is more controlled and calm. Added to this are the

undecided who still do not have a clear destination (16%) or those who are

waiting to be vaccinated (12%). (Ipsos France) June 3, 2021 NORTH AMERICA (USA) 51% Republicans Say United States Should Follow Its Own

National Interests Even When Allies Strongly Disagree Republicans who turn only to Fox News or

talk radio are less likely than other Republicans to say many of the problems

facing the country can be solved by working with other countries (20% vs.

36%). Democrats, however, are about equally likely to say this regardless of

their media diet: Overall, 71% of Democrats hold this view. (PEW) JUNE 2, 2021 Smartphone Ownership (85%) And Home Broadband Subscriptions (77%) Have Increased Among American

Adults Since 2019 Smartphone ownership (85%) and home broadband subscriptions (77%) have increased

among American adults since 2019 – from 81% and 73% respectively. Though

modest, both increases are statistically significant and come at a time when

a majority of Americans say the internet has been important to them personally. And 91% of adults

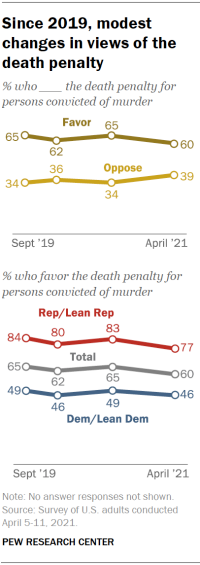

report having at least one of these technologies. (PEW) JUNE 3, 2021 60% Of U.S. Adults Favor The Death Penalty For People

Convicted Of Murder More Americans favor than oppose the death

penalty: 60% of U.S. adults favor the death penalty for people convicted of

murder, including 27% who strongly favor it. About four-in-ten (39%) oppose

the death penalty, with 15% strongly opposed, according to a new Pew Research

Center survey. The survey, conducted April 5-11 among 5,109 U.S. adults on

the Center’s American Trends Panel, finds that support for the death penalty

is 5 percentage points lower than it was in August 2020, when 65% said they

favored the death penalty for people convicted of murder. (PEW) JUNE 2, 2021 (Canada) Four In Ten (40%) Working Canadians Say They’ve Experienced

A Decline In Their Physical Health Throughout The Pandemic As vaccination rates have ramped up across

the country, and businesses are starting to prepare for a post-pandemic

future, working Canadians continue to face a number of health-related

challenges. Four in ten (40%) working Canadians say they’ve experienced a

decline in their physical health throughout the pandemic, according to a

recent Ipsos poll conducted on behalf of RBC Insurance. The inability to

socialize with family, friends or co-workers (72%) and work-related stress

(58%) were also cited as factors impacting overall health. (Ipsos Canada) 1 June 2021 AUSTRALIA Australian Formula 1 Grand Prix In Doubt For 2021 But It’s

The Ongoing V8 Supercars Series That Provides Value For Sponsors Nearly 4.6 million Australians watched

motorsports including Formula 1, V8 Supercars, the Bathurst 1000, Drag racing

and Rally car racing on TV in 2020. The leading motor sports events watched

by Australians on TV are the Bathurst 1000 watched by over 3.1 million, the

V8 Supercars watched by 2.6 million and the Formula 1 watched by nearly 2.3

million. In contrast, only around a quarter of all Australians, 28%, can name

a brand associated with V8 Supercars and just over a fifth, 22%, can name a

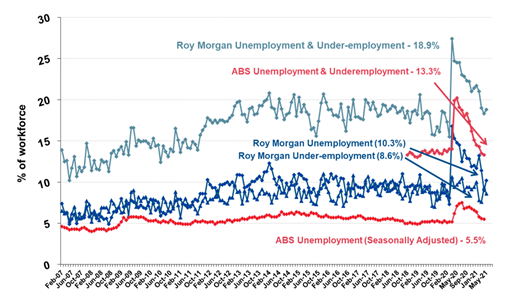

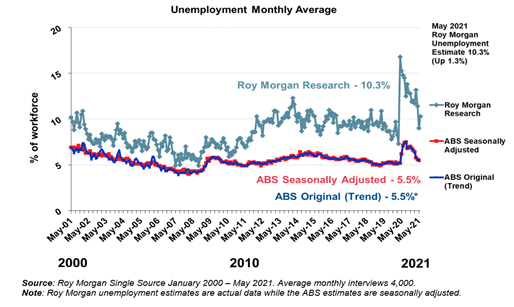

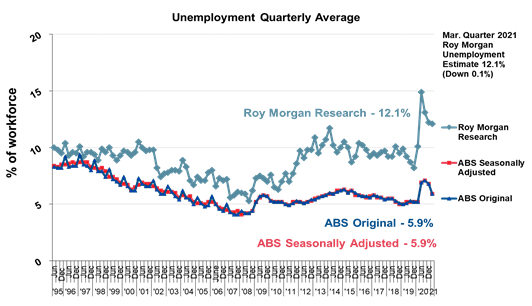

brand associated with the Australian Formula 1 Grand Prix. (Roy Morgan) June 01 2021 Australian Unemployment Increases To 10.3% In May – A Month

After The End Of Jobkeeper Latest Roy Morgan employment series data

shows 1.49 million Australians unemployed in May – up 186,000 on April for an

unemployment rate of 10.3% with the increase somewhat offset by a fall in

under-employment which dropped 101,000 in May to 1,256,000 (8.6%).1,493,000

Australians were unemployed (10.3% of the

workforce), up 186,000 from April. There were far more people

looking for part-time work (up 221,000 to 935,000) but fewer people looking

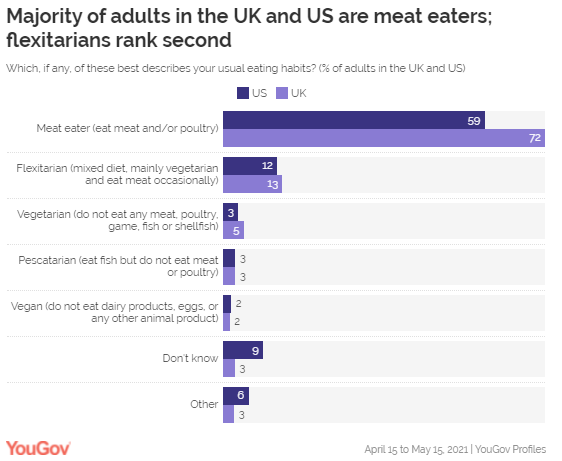

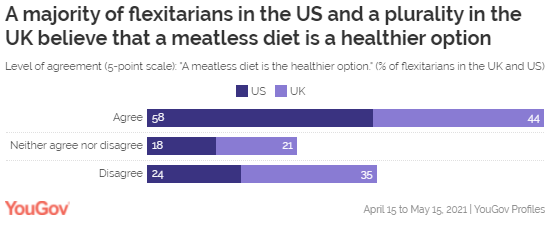

for full-time work (down 35,000 to 558,000). (Roy Morgan) June 04 2021 MULTICOUNTRY STUDIES Most Of The Total Adult Population In The US

(59%) And In The UK (72%) Are Meat-Eaters More than half (58%) of the American adults

who identify themselves as flexitarians believe that a meatless diet is

a healthier option, albeit that a quarter (25%) of them

disagree. Compared to the general population, half of Americans

(50%) agree that going meat-free is better for

you, while 32% disagree. Flexitarians, who follow

vegetarianism with the occasional inclusion of meat, form 13% of the UK’s

population and 12% in the US. (YouGov UK) May 31, 2021 Are Consumers Moving Back To Offline Shopping? The Covid effect is unmistakable: In

countries with stricter restrictions, the gap between online and offline

buyers is greater. It is one of the greatest divergences in Germany: 46

percent of those surveyed bought non-essentials in stores, 74 percent

online. In Australia, on the other hand, the number of offline shoppers

was higher than that of online shoppers. Only 29 percent of those surveyed

name social distancing as a reason to shop online. On the other hand, 47

percent say it is easier to shop online and 57 percent cite home delivery as

an important benefit. (YouGov Germany) Source: https://yougov.de/news/2021/05/31/schwenken-verbraucher-zuruck-zum-offline-einkauf/ One In Six Consumers In The US (17%) And One In Seven In

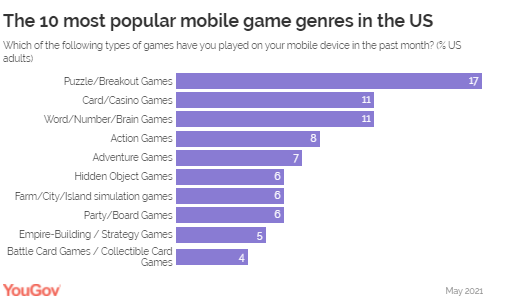

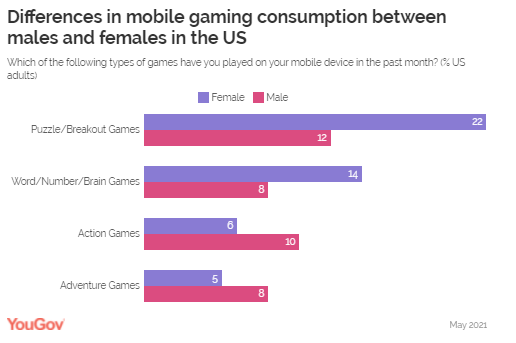

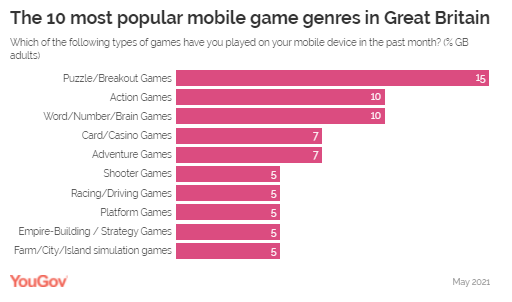

Great Britain (15%) Said They Play Games Such As Candy Crush Saga And

Bejeweled Blitz Let's explore the types of mobile games

that consumers are most drawn to in two key markets: the US and Great

Britain. Data from YouGov Profiles reveals that Puzzle and Breakout games

constitute the most popular category in both markets. About one in six consumers

in the US (17%) and one in seven in Great Britain (15%) said they play games

such as Candy Crush Saga and Bejeweled Blitz. In the US, Card/Casino and

Word/Number/Brain games were tied at the second spot with one in nine

Americans (11%) saying they played games from those genres on their cell

phones over the past month. Action games (8%) and Adventure games (7%)

featured in the top five as well. (YouGov UK) June 01, 2021 Israel Is Least Favourable Amongst Britons,

With Favourability Falling From -14 In February To -41 In May Following Gaza

Strikes Of all the countries surveyed, Israel is

least favourable amongst Britons, with favourability falling from -14 in

February to -41 in May, its lowest rating in Britain since we started asking

this question in 2016. The next highest fall in Israel’s favourability is

seen in France, decreasing 23 points from -13 to -36, the country’s lowest

favourability rating amongst the French since May 2019. A similar fall can be

seen in Denmark, experiencing a 22 point drop from -17 to -39. Sweden and

Germany see the smallest falls in favourability, at 17 and 14 points

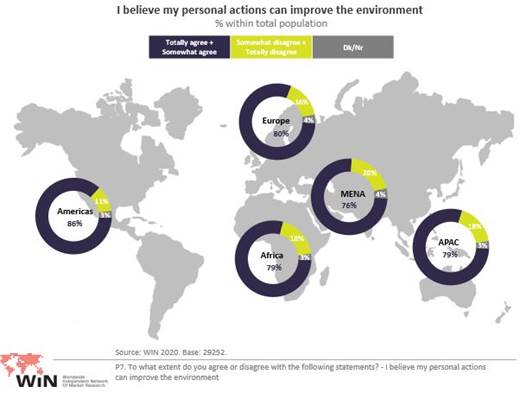

respectively. (YouGov UK) June 04, 2021 Protect The Environment And Fight Climate

Change: Individuals’ Responsibility And The Role Of Companies And Governments Climate change has already been a reality

for several years, and one of its main consequences is global warming, which

is perceived as a threat to humanity

by 85% of the global population surveyed (in APAC and

Americas the share is even higher, with 87% of the population believing

global warming is a threat). Vietnam (97%), South Korea (94%), Chile (93%),

Indonesia (92%), India, Ecuador, and China (91%) are at the top of the world

ranking when it comes to the perceived threat of global warming. (WIN) 4 Jun 2021 ASIA

693-43-01/Poll Only A Few

(22%) Indians Are Likely To Dine Out Once Restaurants Re-Open Or The Lockdown

Is Lifted

Amid the fresh Covid19 outbreak, YouGov’s

latest survey reveals urban Indians prioritize vaccination of staff as much

as a safe dining experience when it comes to their comfort of buying food

from a restaurant or a QSR chain- either through delivery or dining-in. Interestingly, these two factors are a

higher priority in tier-1 cities of India, some of which are worst affected

by the current wave of Covid19. Many respondents said contactless payment

options and provisions for contactless orders (42% and 39%, respectively)

would make them feel relaxed buying from a restaurant in the current scenario. Slightly over a third feel more delivery or

take away options would encourage them to buy (35%), and for few partially

cooked or semi-cooked meal kits would do the needful (14%). Only one in seven (14%) are currently not

willing to either order or dine out at a restaurant no matter what steps they

take. On being asked about their likeliness to

visit a restaurant, it seems urban Indians are in no hurry and most of them

would be comfortable going to a restaurant once the pandemic is over or once

they are vaccinated. The rising fear levels around contracting the virus

could perhaps be the reason for not wanting to step out soon. In comparison to this, only a few (22%) are

likely to dine out once restaurants re-open or the lockdown is lifted. Few

others (13%) are unsure of their decision yet. Among the different age groups, 40+ adults

were most likely to say they will dine out once the pandemic is over, but

adults between 18-39 years were more likely than them to visit a restaurant

upon vaccination. It seems home-delivery of food has assumed

importance during the current phase of lockdown and most urban Indian

respondents (58%) are ordering in food at home at least once a week. When asked about the places they usually

order from, two in five people (38%) said they order from restaurants

offering healthy menus. A quarter (25%), however, order from QSR

chains such as McDonald’s, KFC, etc). Slightly fewer (19%) order in from

fine-dine restaurants. Comparatively, very few prefer to order from home

chefs or tiffin services. When it comes to reasons for ordering in,

unsurprisingly boredom of eating home-cooked food is the biggest motivation

to order in (62%), followed by the inability to dine out during the pandemic

(53%). Some people order to celebrate special

occasions (45%), others order when they don’t have the time to cook (38%) or

when domestic help is not available (36%). Some others call for food for its

variety (31%), or to avail offers or deals available on ordering (23%). This

indicates people are ordering in to seek the taste or experience of

restaurant dining more than out of convenience. Restaurants and delivery chains may want to

consider these insights in order to provide a safe dining experience to their

customers whilst emphasizing on the safety and wellbeing of their staff and

delivery agents. (YouGov India) June 1, 2021 Source: https://in.yougov.com/en-hi/news/2021/06/01/staff-vaccination-safe-dining-experience-are-top-p/ AFRICA

693-43-02/Poll 48 % Of

Namibians Are Likely To Get Vaccinated If It Is Available And Government Says

Its Safe, 50% Are Unlikely

Nearly all adult Namibians are worried

about the effects of the COVID-19 pandemic on their households, the country,

and the future of their children, according to a telephone survey by

Afrobarometer. But a majority of citizens have concerns

about the safety of COVID-19 vaccines and believe that prayer is more

effective than vaccines in preventing COVID-19 infection. Only about half say they are

likely to try to get vaccinated. The survey, conducted last

December-February, is Afrobarometer’s first under its “AB Calling” telephone

survey label. With 54,659 COVID-19 cases and 817 deaths

as of 1 June 2021 reported by the Namibia Statistics Agency, the country is

facing its biggest health crisis since the start of the pandemic. About

76,500 vaccine doses have been administered, according to the World Health Organisation.

Slow vaccine uptake is of great concern with a third wave of infections

looming large during this winter period. (Afrobarometer) 2 Jun 2021 693-43-03/Poll In 2020 80%

Of Liberians Think That Country Is Going In Wrong Direction

Liberians

generally hold gloomy views of the direction of the country, the country’s

economic condition, and their personal living conditions, the latest

Afrobarometer survey shows. An

overwhelming majority – almost twice as many as in 2012 – say the country is

going in “the wrong direction,” and only one-fourth of citizens assess the

country’s economic condition as “fairly” or “very” good. Fewer than

half describe their personal living conditions as at least “fairly good.” The study

shows that negative assessments of the country’s overall direction and

economic condition increased with individuals’ experience of poverty. (Afrobarometer) 3 Jun 2021 693-43-04/Poll Ugandans

(50%) approved of COVID-19 lockdown despite difficulty complying

Almost nine in 10 Ugandans say that last

year’s lockdown was necessary to limit the spread of COVID-19, in spite of

the toll it took on the economy and people’s livelihoods, the latest

Afrobarometer survey shows. Two-thirds say they found it difficult to

comply with lockdown restrictions or curfews imposed by the government. Only about two in 10 citizens say their

households received special government assistance during the pandemic, and

most Ugandans believe that government assistance was not distributed fairly. Whereas the lockdown was nationwide, relief

aid was distributed only in Kampala and Wakiso, and the first phase targeted

only 1 million urban poor. These survey findings suggest a need for

transparent criteria for targeting of beneficiaries so as to ensure equitable

benefits of the program intervention. (Afrobarometer) 4 Jun 2021 693-43-05/Poll 65% Ugandans

Are Of The View That COVID-19 Resources Are Lost Due To Corruption

A new Afrobarometer survey in Uganda shows

that a majority of citizens approve of the government’s management of the

response to COVID-19, although many raise concerns about corruption. More than three-quarters of Ugandans

believe that at least some of the resources available for responding to the

pandemic were lost due to corruption among government officials. Only about half of citizens say they trust

government statistics on COVID-19 cases and deaths. A report by the Auditor General in March

revealed significant mismanagement of COVID-19 funds. As of 3rd June 2021,

Uganda has so far tested 1,125,306 samples for COVID-19, with 49,759

confirmed cases, 47,760 recoveries and 365 deaths. (Afrobarometer) 4 Jun 2021 WEST EUROPE

693-43-06/Poll Six In Ten Britons Still Expect Measures To Be Lifted On 21st June,

But Optimism That Lockdown Will Be Lifted Has Fallen Over The Month

New polling by Ipsos MORI shows most people are still hopeful for the

lifting of current lockdown restrictions on 21st June. Almost 6 in 10 (58%)

believe it is likely that this will go ahead as currently planned by the

Government, while a third (33%) say it is unlikely, in research carried out

between 21-23 May. But while a majority remain hopeful, there has been a

significant drop over the month. When the same question was asked at the

beginning of May, almost three-quarters (73%) said the lifting of

restrictions on 21st June was likely, 15ppt more than those who feel the same

way now, while the proportion who think it is unlikely has risen 14ppt.

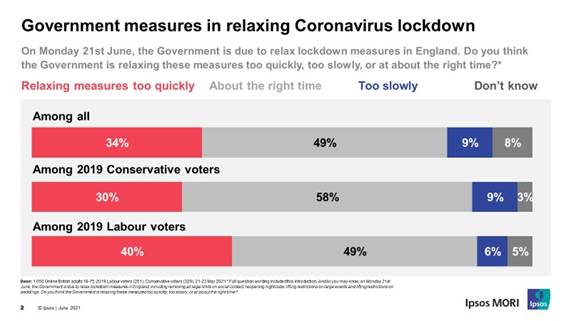

Overall, a third of Britons (34%) believe the Government is lifting

lockdown restrictions too quickly while half say the easing of rules is

coming at the right time, and only 1 in 10 (9%) believe it is happening too

slowly.

Gideon Skinner, Head of Political Research

at Ipsos MORI, said: Even before the reports this weekend, this

latest polling showed that while most Britons were still hopeful that

lockdown would end on the 21st June, they were not as optimistic as they had

been at the beginning of the month – perhaps partly in response to growing

awareness of the potential impact of the new variant. As we have seen

throughout the pandemic the public themselves remain fairly cautious and

there is little sign of much appetite to speed up the relaxation of measures

– instead, around half are broadly supportive of the government’s approach to

easing restrictions, and even a third worry it might be happening too

quickly. (Ipsos MORI) 1 June 2021 693-43-07/Poll Two In Five Brits (42%) Say That Local Police Are Effective At

Providing Advice And Guidance To The Public

A NEW Ipsos MORI survey shows that two in five Brits (42%) say that

local police are effective at providing advice and guidance to the public and

a similar proportion say they are effective at responding when a member of

the public calls (39%). But only around a quarter (23%) say they are

effective at protecting those online. On most measures of effectiveness,

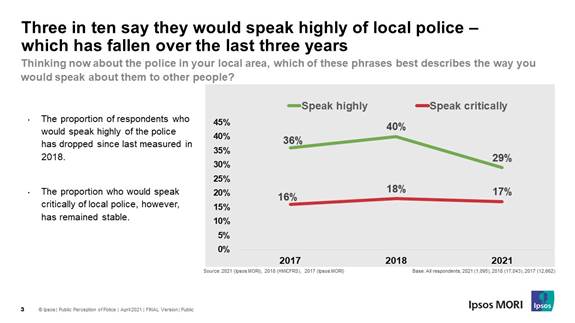

there has been little change since 2017. However, people are now significantly less likely to say they would

speak highly of the police in their local area compared with three years ago.

In 2018, four in ten 10 (40%) Britons said they would speak highly of their

local law enforcement, now only 29% feel the same way. Although, there has

been no change in the proportion of people who would be critical of local

police; 17% now compared with 18% in 2018.

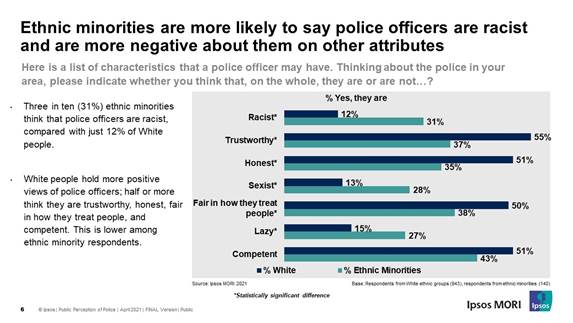

On some aspects of local policing, ethnic minorities are more

positive than White people; around half of ethnic minorities (53%) say that

police in their local area are effective at providing advice to the public

and responding when a member of the public calls (49%), compared with 40% and

37% of White people respectively. Ethnic minorities are also more likely than

White people to see local police as being effective at preventing and

investigating offending, as well as protecting those who are online. Overall, the public is fairly positive about the characteristics of

local police – around half say they are trustworthy (52%), competent (50%),

fair in how they treat people (49%) and honest (49%). Around one in six think

they are lazy (16%), sexist (15%) or racist (14%). However, ethnic minorities are significantly more likely to view

police officers in their area as being racist than White people; three in ten

(31%) ethnic minority people say that the police in their area are, on the

whole, racist, compared to only one in 10 (12%) White people.

Kully Kaur-Ballagan, Research Director at

Ipsos MORI said On the whole people are positive about the

police and how effective they are at policing although there is clearly less

confidence in their ability to protect people online. (Ipsos MORI) 2 June 2021 693-43-08/Poll 53% Of People Think Changes To The National Curriculum Should Be A

Part Of A Hypothetical Overhaul Of The Schooling System

The Education Recovery Commissioner Sir Kevan Collins has resigned after

his plans for education reform to help students catch up following the

pandemic were rejected by the government. In our last

article on the English school system, YouGov looked at what parents

thought of the current schooling system, how it handled the pandemic, and

whether it prepared their children well for adult life. Now, further YouGov

polling for The

Times reveals how parents think the schooling system should change,

from the focus of curriculums and key subjects, to the nature of private schools

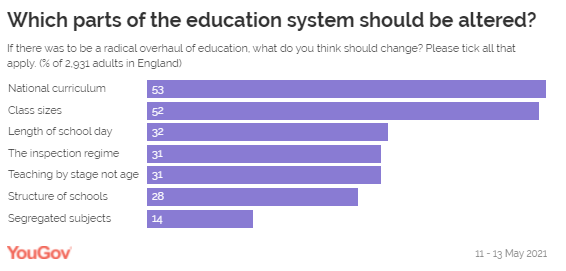

and whether homework is really needed for younger learners. How should schools be reformed? Some 53% of people think changes to the national curriculum should be

a part of a hypothetical overhaul of the schooling system – including some

61% of parents with children under 5. (More precise questions on how the

curriculum is handled and could be changed are covered in the next section). Elsewhere, however, another 52% of the public think that changes need

to be made to class sizes. Parents who have children at secondary age are

more likely to back changes to class sizes (56%) versus just under half of

those with children under 5 (46%) – possibly unsurprising given secondary

classes at their largest size in nearly

twenty years,

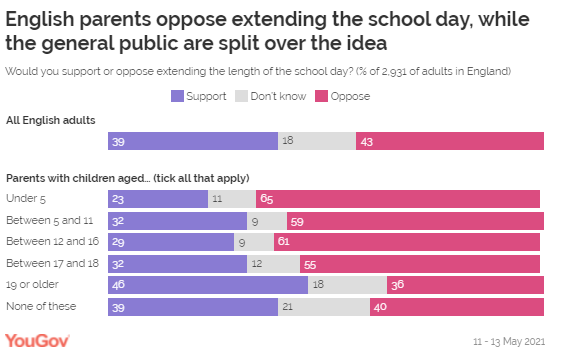

Further to this, Sir Kevan Collins had highlighted increasing

the length of the school

day as a solution to help students catch up on teaching after COVID.

YouGov’s Teacher Track survey previously showed

that the overwhelming majority of teaching staff (91%) across Great Britain

were opposed to such measures. Now this survey finds a similar opinion with

parents, who are also opposed to an extension of the school day, although not

quite as strongly. Opposition is highest among parents of children under 5

(65%) and lower among parents of children aged 17 to 18 (55%). The general public, however, are split over the idea of an extended

school day, with 39% in favour and 43% opposed. Of other potential changes to the system, three in ten people (31%)

would change the current inspection regime, and the same proportion of people

would back teaching by stage, rather than age of child, and 28% think school

structures need to change. Curriculum: do schools focus too much on

certain subjects like science or art? As we saw above, 53% of the general public would back changes to the

curriculum if there was an overhaul of the education system – so how they do

think schools are currently balancing their topics?

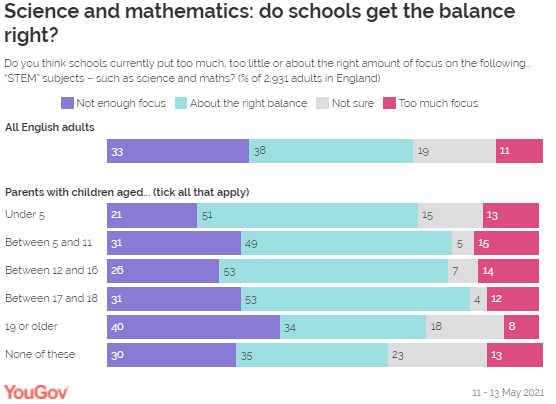

The general public is split on whether arts and STEM (science,

technology, engineering and maths) get either too little or about the right amount

of focus, and among those with children there is disagreement between parents

of the youngest and oldest. Parents with children older than 19 tend to think that the STEM

subjects are not focused on enough in schools (40%), compared to only 21% of

those with the youngest children (under 5) who think the same. This group of

parents is instead most likely to think STEM subjects already get about the

right amount of focus in class time (51%).

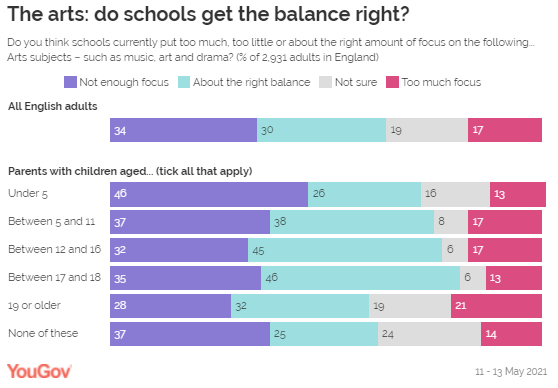

This feeling is reversed when asking about arts subjects. Those with

children under the age of 5 are more likely to think that the arts do not get

enough focus in schools (46%) compared to parents of children aged 19 or

older (28%).

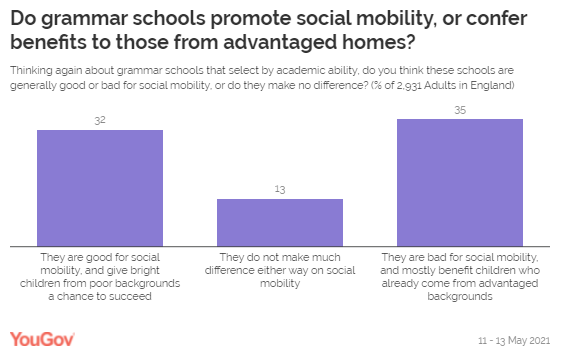

Are grammar schools good for social

mobility, and should private schools be banned? One topic that is always at the forefront of discussion around the

education system is that of private and grammar schools. What do parents and

adults make of elite education: does it benefit all or just a privileged few? The public is split on how grammar schools effect social mobility.

Some 32% of people think they give poor children a chance to succeed and are

good for social mobility, while 35% say they are bad, and limit advantages to

a select few. Another 13% think they make little difference either way.

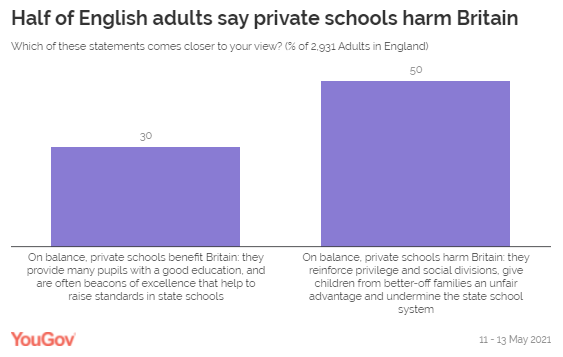

Moving on to private schools, half of people think they harm Britain

and that on balance they “reinforce privilege and social divisions” (50%) –

an opinion consistent among the parental groups. Three in ten people (30%) take the opposing view, instead feeling

more that private schools are “beacons of excellence that help to raise

standards in state schools”.

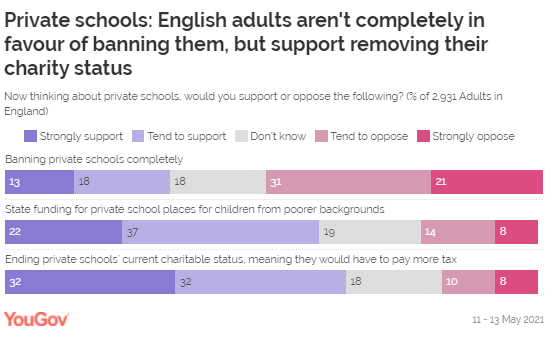

While people are opposed to banning private schools, they do support

ending their charitable status so they would have to pay more tax (64%), with

only 18% opposed to doing so. Most (59%) would also support state funding for

poorer children to attend private institutions. Is homework a good tool for learning, or is

there too much emphasis on it? Homework is another contentious subject, with some arguing it has a “limited

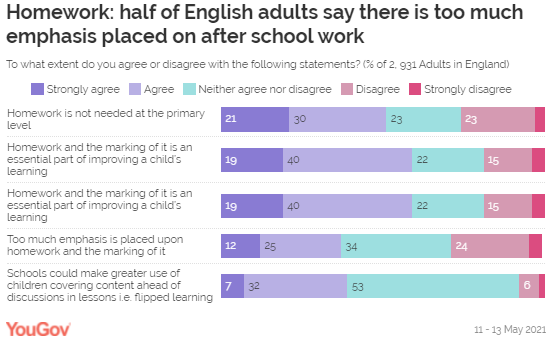

purpose” in teaching - but what do parents think? Among the public, some 59% agree that homework is an “essential part

of improving a child’s learning”. This opinion is most strongly held by those

with older children, including 65% of those with children over the age of 19,

and less reflected in those with children under 5 (47%). Another 51% of the public think that homework is not needed for

students at primary level – a sentiment shared by half of parents with

children at this stage of their education (50%), but is higher among those

with children under 5 (64%).

These parents of the youngest children are also the most likely to

think that too much emphasis is placed on the marking of homework (55%),

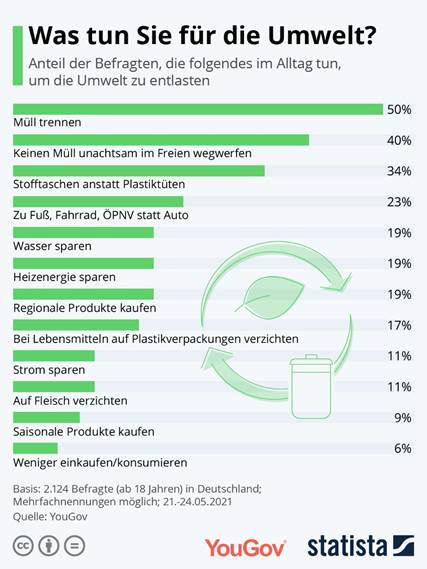

compared to three in ten of those with children aged over 19 (30%). (YouGov UK) June 03, 2021 693-43-09/Poll Environmental Protection Is A Matter Close To The Heart For Seven Out

Of Ten Germans

World Environment Day is celebrated on Saturday, June 5th. For

the majority of Germans, environmental protection is important: 70 percent

say that it is important to them. Not surprisingly, this is what voters

from the Greens are most likely to say (91 percent). Also voters of the

party "Die Linke" (86 percent), the SPD (79 percent) and the Union

(77 percent) are more important than the general population. This was

the result of a current YouGov survey in cooperation with Statista.

A THIRD OF GERMANS FIND CLIMATE CHANGE TO

BE EXAGGERATED IN THE MEDIA With their fight for environmental and climate protection, Greta

Thunberg and Fridays for Future have attracted a lot of media attention since

2018. Every third respondent in Germany (33 percent) thinks the media

coverage of climate change is excessive. More men (38 percent) say that

than women (28 percent). Differences are also apparent when looking at the voters of the

various parties. AfD voters in particular think that the topic of

climate change is being exaggerated in the media (66 percent). This is

what 40 percent of the voters of the FDP say. Green voters are the least

likely to give this figure (10 percent).

WASTE SEPARATION, CLOTH BAGS AND NO PLASTIC

PACKAGING - THAT IS WHAT GERMANS DO TO PROTECT THE ENVIRONMENT In order to consciously relieve the environment in everyday life,

every second German separates their garbage (50 percent). 40 percent say

they don't carelessly throw away rubbish outdoors or in nature, and 34

percent use cloth bags instead of plastic bags. Almost a quarter (23

percent) walk, ride a bike or use public transport instead of

driving. Every fifth person (19 percent) saves water and heating energy

or buys regional products. Only 11 percent of the Germans surveyed say they save electricity,

also when it comes to video streaming and video games, and 18-24 year-olds

least of all (4 percent).

Based on the YouGov

Omnibus , 2,124 people were surveyed from May 21 to 24, 2021 using

standardized online interviews. The results are weighted and

representative for the German population aged 18 and over. (YouGov Germany) June 2, 2021 Source: https://yougov.de/news/2021/06/02/umweltschutz-fur-sieben-von-zehn-deutschen-ein-her/ 693-43-10/Poll 52% Of The Spaniards Have Not Yet Planned Their Vacations Since They

Prefer To Wait To See How The Pandemic Evolves

With the arrival of the month of June, many are those who can no

longer think of anything other than the summer holidays. In addition,

this year the desire is greater than ever since with the increasingly high

vaccination rate, the coming months draw a much more hopeful horizon and

without so many restrictions that allow us to enjoy a summer more similar to

what we knew before. Faced with this scenario, Ipsos

wanted to know how the members of its What & Why Community approach their summer vacations , and thus be able to shed light

on the forecasts that the tourism sector can make regarding this campaign. While last summer 24% of respondents decided not to go on vacation,

this year 100% of those interviewed

affirm that they will. Despite this, 2 out of 3 admit that they have not

yet booked their vacations, stating 52% of them that they prefer to wait to

see how the pandemic evolves to make sure that everything is more controlled

and calm. Added to this are the undecided who still do not

have a clear destination (16%) or those who are waiting to be vaccinated

(12%). Where and how will the holidays be this

year? This year the summer holidays will be enjoyed within the national

territory, 81% of those interviewed

affirm that they will only travel within Spain . 18%

will combine the national with a trip abroad, and 2% who will spend their

vacations exclusively abroad. Within these destinations, as is customary at this time of

year, the majority (73%) will opt for

beach tourism seeking rest and disconnection from everyday life (57% ). On

the other hand, 33% will opt for city tourism, since there are also those

whose main motivation is to know new places (29%). Regarding where to stay, a change is observed compared to 2020,

since the percentage of those who will

choose to stay in a hotel or tourist complex increases by 10 points (38%

in 2020 compared to 48% in 2021); an option that is gaining followers

this summer compared to second homes,

which drops by 7 points compared to 2020, and homes of family

or friends that goes from 22% to 18%. In addition, since it is mostly a national tourism, almost the total

of those surveyed (86%) will choose the car as a means of transport to get to

their holiday destination, while 21% will use the plane and 8% the train. The Covid-19 will also be present on the

holidays Although this summer arises with important differences from the past,

Covid-19 continues to be a key factor when planning summer vacations and that

makes them different for 56% of those surveyed, and of these, 54% state that they will spend more time outdoors,

followed by 51% who will avoid crowded destinations or 44% who will travel to

nearby places. In addition, among those who have the option of telecommuting, almost

half of those surveyed, one in three (34%) affirm that they will extend their

stay at their holiday destination thanks to this job possibility. (Ipsos France) June 3, 2021 Source: https://www.ipsos.com/es-es/vacaciones-de-verano-si-pero-condicionadas-por-la-pandemia NORTH

AMERICA

693-43-11/Poll 51% Republicans Say United States Should Follow Its Own National

Interests Even When Allies Strongly Disagree

Americans’ views about key

international priorities – and China

specifically – differ widely by party, as recent Pew Research Center

surveys have found. But further differences emerge within party based on where people

turn for political news. Republicans and Republican-leaning independents who say their major

sources of political news are only sources

with right-leaning audiences (Fox News or talk radio) tend to be less open to

international cooperation and to have different foreign policy priorities

than other Republicans. Similarly, Democrats and Democratic-leaning

independents who only rely

on sources with left-leaning audiences (CNN, MSNBC, NPR, The New York Times

and/or The Washington Post) for political news stand apart from other

Democrats in some areas, including by placing a higher priority on

multilateralism and addressing global climate change. And when it comes to

China, partisans in these so-called “news bubbles” on both sides of the aisle

tend to hold more negative views than others in their respective parties. Below is a closer look at these dynamics. All findings are based on

an analysis of what outlets U.S. adults said they used as major sources for

political and election news in a September

2020 survey. The survey asked about eight different sources of news;

outlets are grouped according to the self-reported ideological leaning of

their audiences. You can read

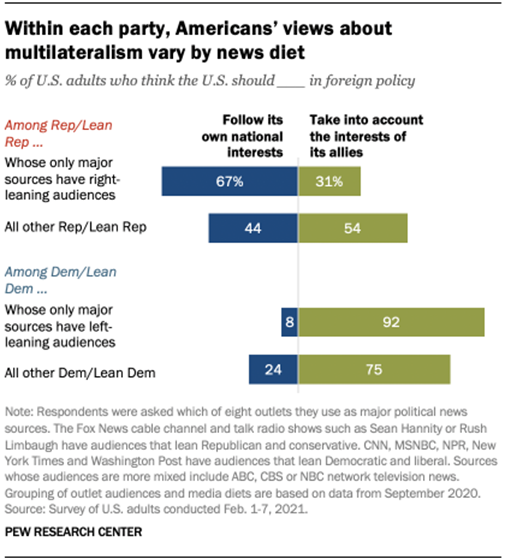

more about the methodology here. Views of international cooperation Public attitudes about the importance of international cooperation

vary widely within party based on Americans’ news diets.

Overall, Republicans

are split over whether the United States should follow its own

national interests even when allies strongly disagree (51%) or whether the

U.S. should take into account the interests of its allies even if it means

making compromises with them (47%). But Republicans who only consume sources

with right-leaning audiences are much more likely than other Republicans to

say the U.S. should follow its own interests (67% vs. 44%). Democrats, for their part, are largely united in the view that the

U.S. should take into account the interests of its allies even if it means

making compromises with them (80% say this). But Democrats who only rely on

outlets with left-leaning audiences are somewhat more likely than other

Democrats to say the interests of allies should be taken into account (92%

vs. 75%). On a related question, Republicans who turn only to Fox News or talk

radio are less likely than other Republicans to say many of the problems

facing the country can be solved by working with other countries (20% vs.

36%). Democrats, however, are about equally likely to say this regardless of

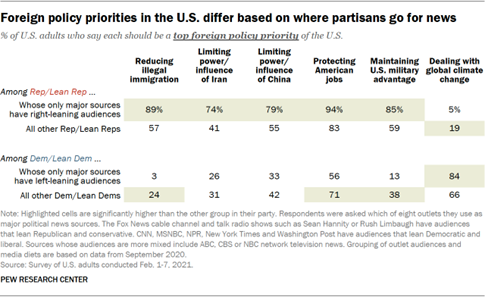

their media diet: Overall, 71% of Democrats hold this view. Foreign policy priorities When asked about foreign policy priorities, Republicans overall

prioritize traditional security goals and limiting immigration, while

Democrats are focused more on reducing the spread of infectious disease and

global climate change. Still, within each party, there are sharp divides in

some foreign policy priorities that relate to people’s media diets. Republicans who only use outlets with right-leaning audiences stand

out from other Republicans for the priority they place on protecting the jobs

of American workers, maintaining the U.S. military advantage over all other

countries, reducing illegal immigration into the U.S., limiting the power and

influence of Iran, and limiting the power and influence of China. This group,

for example, is 32 percentage points more likely than other Republicans to

say reducing illegal immigration into the U.S. should be a top foreign policy

priority. They are also much less likely

than other Republicans to prioritize dealing with global climate change (5%

vs. 19%).

Democrats who turn only to major news sources with left-leaning

audiences are much more likely than other Democrats to say dealing with

global climate change should be a top priority (84% vs. 66%). They are also

significantly less likely

than other Democrats to say reducing illegal immigration into the U.S. should

be a top foreign policy priority (3% vs. 24%). Views of China When asked about a series of foreign countries and organizations –

including Germany, the European Union, NATO and the UN – Republicans whose major

news sources are only Fox News or talk radio tend to be about as negative, or

more so, than other Republicans. Democrats who use only outlets with

left-leaning audiences, in turn, are about as positive, or more so, than

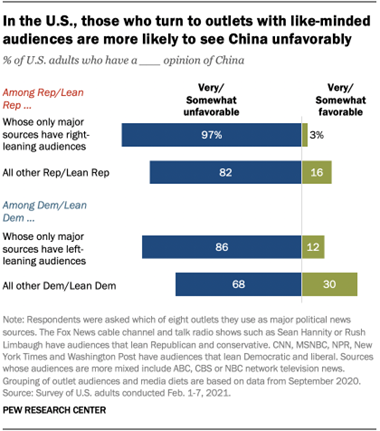

other Democrats. The pattern differs when it comes to China, however. In both partisan

coalitions, those who turn only to news outlets with audiences on the

ideological right or left are more likely than others in their party to have

an unfavorable opinion of China.

Republicans who only turn to Fox News or talk radio have an almost

universally unfavorable view of China (97%), while this is less the case for

other Republicans (82%). Similarly, Democrats who only turn to CNN, MSNBC,

NPR, The New York Times and/or The Washington Post are more likely than other

Democrats to have an unfavorable view of China (86% vs. 68%). It’s important

to note that while more conservative Americans – especially conservative

Republicans – tend to have more negative views of China, these media-related

patterns persist even after accounting for political ideology. The same pattern appears again when looking at views of Chinese

President Xi Jinping. Republicans who turn only to Fox News or talk radio are

more likely than other Republicans to say they have no confidence at all in

Xi (70% vs. 53%). On the Democratic side, those who turn only to outlets with

left-leaning audiences are slightly more likely than other Democrats to say

they have no confidence at all in Xi (37% vs. 32%). Republicans who turn only to news outlets with right-leaning

audiences and Democrats who turn only to outlets with left-leaning audiences

are also more likely than others in their respective parties to say the U.S.

should try to promote human rights in China, even if it harms economic

relations, and that China is doing a very bad job dealing with climate

change.

One area where Republicans who turn only to Fox News and talk radio

stand out strongly from other groups in both parties is on the question of

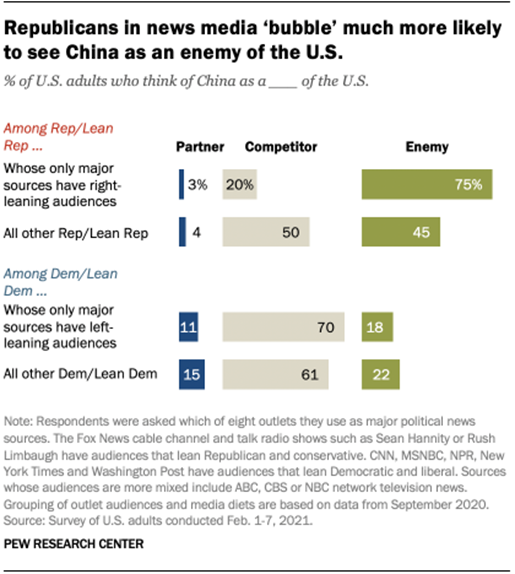

whether China is a partner, competitor or enemy of the U.S. Three-quarters of

these Republicans think of China as an enemy of the U.S., as opposed to a

competitor or partner. That compares with only 45% of Republicans with other

media diets and only about one-in-five Democrats, regardless of media diet. (PEW) JUNE 2, 2021 693-43-12/Poll Smartphone

Ownership (85%) And Home Broadband Subscriptions

(77%) Have Increased Among American Adults Since 2019

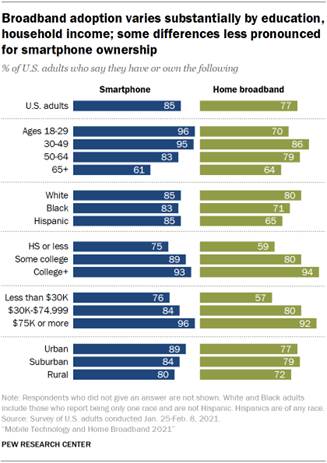

Smartphone ownership (85%) and home broadband subscriptions

(77%) have increased among American adults since 2019 – from 81% and 73%

respectively. Though modest, both increases are statistically significant and

come at a time when a majority of Americans say the internet

has been important to them personally. And 91% of adults report

having at least one of these technologies. A Pew Research Center survey of U.S. adults conducted from Jan. 25 to

Feb. 8, 2021, also finds that some Americans have difficulties when trying to

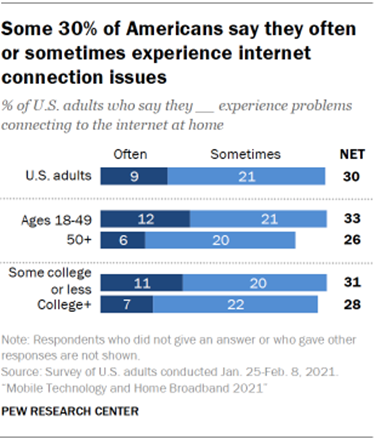

go online. Some 30% of adults say they often or sometimes experience problems

connecting to the internet at home, including 9% who say such problems happen

often. Still, a majority of Americans say these connection troubles occur

rarely (41%) or never (21%). While there has been slight growth in the share who say they

subscribe to high-speed internet, about a quarter of the population still

does not have a broadband internet connection at home. And broadband

non-adopters continue to cite financial constraints as one of the most

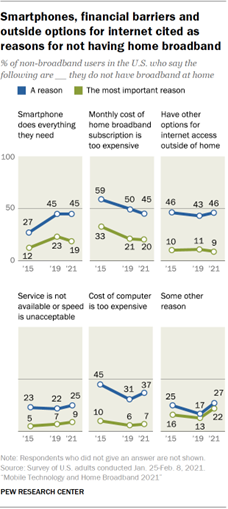

important reasons why they forgo these services. Among non-broadband users,

45% say a reason why they do not have broadband at home is that the monthly

cost of a home broadband subscription is too expensive, while about

four-in-ten (37%) say the same about the cost of a computer. Beyond cost

barriers, a little fewer than half of non-users cite having other options for

internet access or the fact that their smartphone does everything online they

need as a reason why they do not have a high-speed internet connection at

home. Other major findings in this new survey:

These findings come from a nationally representative survey of 1,502

U.S. adults conducted via telephone Jan. 25-Feb. 8, 2021. The following

sections elaborate on those findings. Adults 65 and older are less likely to own

a smartphone; Americans with lower incomes or with less formal education are

less likely to own a smartphone or have home broadband Fully 85% of adults now say they own a smartphone, up from 81% in

2019, when Pew Research Center last measured smartphone ownership. Some

long-running patterns in Center technology adoption studies are evident in

the new survey. Smartphone ownership is relatively common across major

demographic groups, but some substantial gaps in adoption remain, including

by age. While the share of adults ages 65 and older who have a smartphone has

increased from 53% to 61% in the past two years, this age cohort remains far

less likely than younger groups to report having this type of mobile device. As was the case in 2019, ownership rates also vary among the oldest

adults: 71% of adults ages 65 to 74 say they are smartphone owners, but that

share falls to 43% among those 75 and older. Additionally, those living in households earning less than $30,000

and those with a high school diploma or less are less likely than those in

higher-income households and those with higher levels of education to say

they have this type of device.

The share of Americans with home broadband subscriptions has similarly

grown since 2019 – from 73% of adults saying they have one in the previous

survey to 77% today. There are more pronounced variations across some

demographic groups, particularly in differences by annual household income

and educational attainment. For example, 92% of adults in households earning

$75,000 or more per year say they have broadband internet at home. But that

share falls to 57% among those whose annual household income is below

$30,000. The 35 percentage point gap between these two income groups is

nearly twice as large as the comparable gap for smartphone ownership – there

is a 20-point gap between those in households earning less than $30,000 per

year and those in households earning $75,000 or more who say they own a

smartphone. Educational differences follow a similar pattern. There remains a statistically significant gap between rural residents

who have home broadband and suburban residents, but while the gap was 16

percentage points in 2019, it is 7 points today. As has been true in other

Center surveys, there are still significant gaps in home broadband

adoption by race and ethnicity. White adults (80%) are more likely than Black

(71%) and Hispanic adults (65%) to have home broadband.1 Roughly one-in-ten Americans say they often

have problems connecting to the internet at home

While a majority of Americans say they rarely or never have issues

getting online at home, 30% say they experience such problems at least

sometimes, including 9% of adults who say this happens often. Relatively few Americans across major demographic groups report they

often have problems, but some groups are slightly more likely than others to

have that level of trouble connecting to the internet. For example, adults ages 18 to 49 are more likely than those 50 and

older to say they often experience problems connecting to the internet at

home (12% vs. 6%). And adults who have some college education or less formal

education are slightly more likely than college graduates to say they often

have these troubles (11% vs. 7%). There are no statistical differences among

other major demographic groups. About three-in-ten adults under 30 are

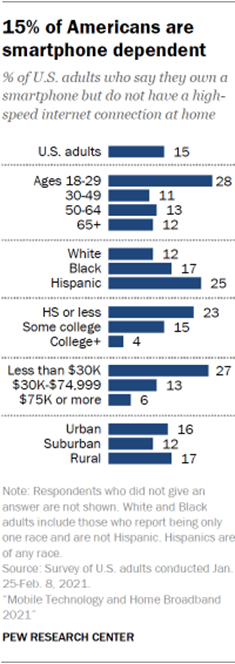

smartphone dependent

Some 15% of Americans say they have a smartphone, but not a home

broadband connection. Pew Research Center has been studying these

“smartphone-only” internet users since 2013.

Smartphone dependence is more common among younger rather than older adults:

28% of adults ages 18 to 29 are in this “smartphone-only” category, compared

with 12% of those 30 and older. Some 27% of adults who live in a household earning less than $30,000

annually are smartphone-only. By comparison, 13% of those with household

incomes of $30,000 to $74,999 and 6% of those in households earning $75,000

or more fall into this category. A similar pattern is evident when it comes

to education: Those with a high school diploma or less are much more likely

to be smartphone dependent than those who have a bachelor’s or advanced

degree. There is also a gap between Hispanic and White adults: A quarter of

Hispanic adults are smartphone-only internet users, compared with about

one-in-ten White adults. And 17% of Black adults are smartphone dependent –

but this share is not statistically different from their White or Hispanic

counterparts. Similar shares of non-broadband users cite

their smartphones, cost and alternate internet access options as reasons for

not having broadband

While a growing share of Americans say they have a high-speed

internet subscription at home, 23% do not. Financial barriers are among the more common reasons why Americans do

not subscribe to high-speed internet at home: 45% of non-broadband users say

a reason is that the monthly cost of a subscription is too expensive, while

about four-in-ten cite the cost of a computer as too expensive. Similar shares of non-broadband users say a reason is they have other

options for internet access outside of home (46%) or their smartphone lets them

do everything online that they need to do (45%). A smaller share of Americans

(25%) say they do not have a home subscription because broadband service is

not available where they live or not available at an acceptable speed. Some 27% of adults – up from 17% in 2019 – say they do not have

broadband at home for some other reason, including 11% who say it is because

they are not interested, do not care for it or do not need it. Broadband non-adopters were asked which, among the reasons they

mentioned, was the most important

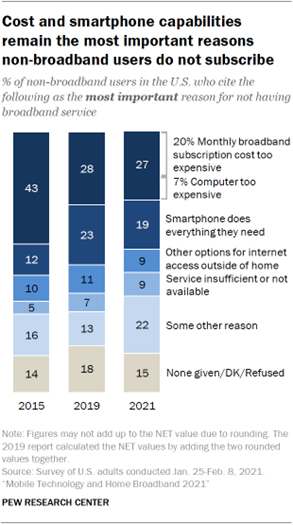

reason they did not have a broadband subscription at home.2 Some

27% of non-broadband users say the most important reason for not having

broadband at home is cost – including 20% who say a monthly broadband

subscription is too expensive and 7% who say a computer is too expensive.

About one-in-five adults (19%) say their most important reason for

not having broadband at home is that their smartphone does everything they

need to do online. Looking specifically at smartphone-dependent Americans,

three-in-ten say their smartphone doing everything they need to do online is

their most important reason for not having broadband at home. That share did

not meaningfully change from 2019. Smaller shares (9% each) say their most important reason for not

having high-speed internet at home is that they have other options for

internet access outside of home or that broadband service is not available,

or not available at an acceptable speed, where they live. Some 22% of non-broadband users cite some other reason as most

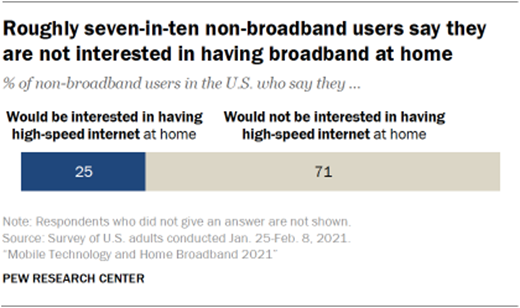

important for not having broadband at home, up from 13% in 2019. A majority of those without home broadband

are not interested in having it in the future

Roughly seven-in-ten non-broadband users (71%) say they would not be interested in having

broadband at home, while 25% think a home broadband subscription is something

that interests them. This is not a statistically significant increase from

the 2019 survey, when 18% said they would be interested in having broadband

at home. In previous Center surveys, Americans have indicated they think that

not having broadband could be tied to a number

of disadvantages – including difficulties finding job opportunities

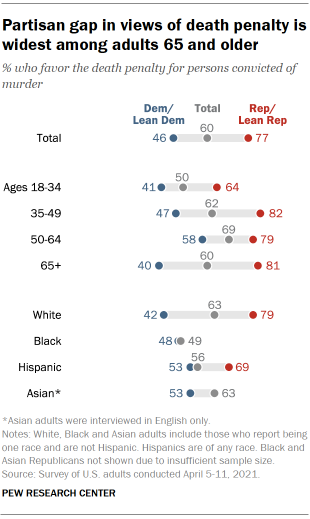

or being disadvantaged in getting access to government services. (PEW) JUNE 3, 2021 Source: https://www.pewresearch.org/internet/2021/06/03/mobile-technology-and-home-broadband-2021/ 693-43-13/Poll 60% Of U.S. Adults Favor The Death Penalty For People Convicted Of

Murder

The use of the death penalty is gradually disappearing in the United

States. Last year, in part because of the coronavirus outbreak, fewer people

were executed than in any year in more than three decades.

Chart shows majority of Americans favor death penalty, but nearly

eight-in-ten see ‘some risk’ of executing the innocent Yet the death penalty for people convicted of murder continues to

draw support from a majority of Americans despite widespread doubts about its

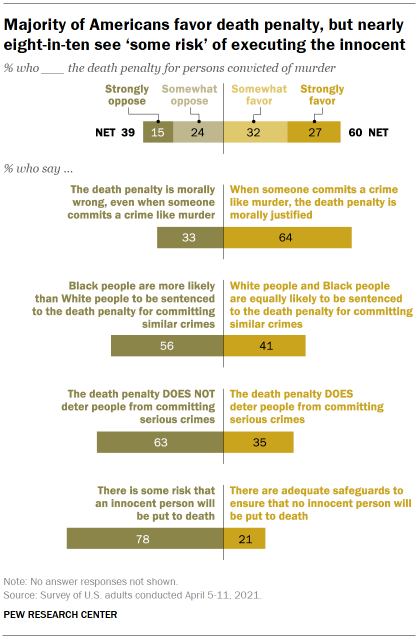

administration, fairness and whether it deters serious crimes. More Americans favor than oppose the death penalty: 60% of U.S.

adults favor the death penalty for people convicted of murder, including 27%

who strongly favor it. About four-in-ten (39%) oppose the death penalty, with

15% strongly opposed, according to a new Pew Research Center survey. The survey, conducted April 5-11 among 5,109 U.S. adults on the

Center’s American Trends Panel, finds that support for the death penalty is 5

percentage points lower than it was in August 2020, when 65% said they

favored the death penalty for people convicted of murder. Chart shows since 2019, modest changes in views of the death penalty While public support for the death penalty has changed only modestly

in recent years, support for the death penalty declined substantially between

the late 1990s and the 2010s. (See “Death penalty draws more Americans’

support online than in telephone surveys” for more on long-term measures and

the challenge of comparing views across different survey modes.) Large shares of Americans express concerns over how the death penalty

is administered and are skeptical about whether it deters people from

committing serious crimes.

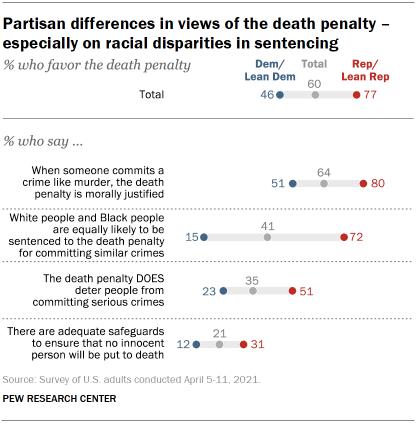

Nearly eight-in-ten (78%) say there is some risk that an innocent

person will be put to death, while only 21% think there are adequate

safeguards in place to prevent that from happening. Only 30% of death penalty

supporters – and just 6% of opponents – say adequate safeguards exist to

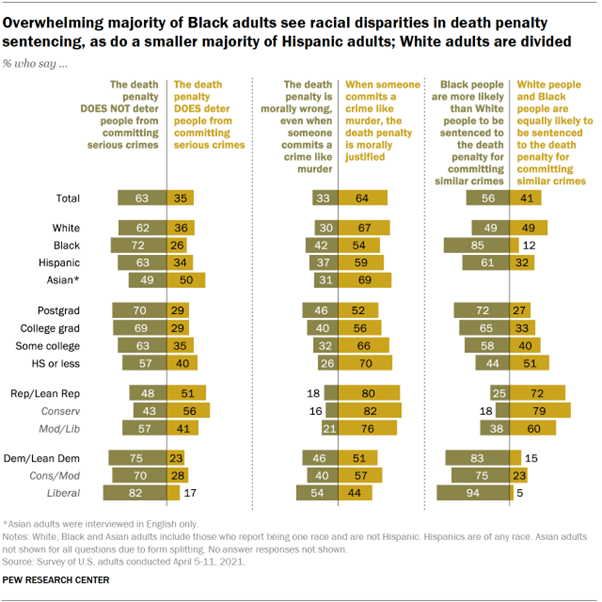

prevent innocent people from being executed. A majority of Americans (56%) say Black people are more likely than

White people to be sentenced to the death penalty for being convicted of

serious crimes. This view is particularly widespread among Black adults: 85%

of Black adults say Black people are more likely than Whites to receive the

death penalty for being convicted of similar crimes (61% of Hispanic adults

and 49% of White adults say this). Moreover, more than six-in-ten Americans (63%), including about half

of death penalty supporters (48%), say the death penalty does not deter

people from committing serious crimes. Yet support for the death penalty is strongly associated with a

belief that when someone commits murder, the death penalty is morally justified.

Among the public overall, 64% say the death penalty is morally justified in

cases of murder, while 33% say it is not justified. An overwhelming share of

death penalty supporters (90%) say it is morally justified under such

circumstances, compared with 25% of death penalty opponents. Chart shows greater support for death penalty in online panel surveys

than telephone surveys The data in the most recent survey, collected from Pew Research

Center’s online American Trends Panel (ATP), finds that 60% of Americans

favor the death penalty for persons convicted of murder. Over four ATP

surveys conducted since September 2019, there have been relatively modest

shifts in these views – from a low of 60% seen in the most recent survey to a

high of 65% seen in September 2019 and August 2020. In Pew Research Center phone surveys conducted between September 2019

and August 2020 (with field periods nearly identical to the online surveys),

support for the death penalty was significantly lower: 55% favored the death

penalty in September 2019, 53% in January 2020 and 52% in August 2020. The

consistency of this difference points to substantial mode effects on this

question. As a result, survey results from recent online surveys are not

directly comparable with past years’ telephone survey trends. A post

accompanying this report provides further detail and analysis of the mode

differences seen on this question. And for more on mode effects and the

transition from telephone surveys to online panel surveys, see “What our

transition to online polling means for decades of phone survey trends” and

“Trends are a cornerstone of public opinion research. How do we continue to

track changes in public opinion when there’s a shift in survey mode?” Partisanship continues to be a major factor in support for the death

penalty and opinions about its administration. Just over three-quarters of

Republicans and independents who lean toward the Republican Party (77%) say

they favor the death penalty for persons convicted of murder, including 40%

who strongly favor it. Democrats and Democratic leaners are more divided on this issue: 46%

favor the death penalty, while 53% are opposed. About a quarter of Democrats

(23%) strongly oppose the death penalty, compared with 17% who strongly favor

it. Over the past two years, the share of Republicans who say they favor

the death penalty for persons convicted of murder has decreased slightly – by

7 percentage points – while the share of Democrats who say this is

essentially unchanged (46% today vs. 49% in 2019). Chart shows partisan differences in views of the death penalty –

especially on racial disparities in sentencing

Republicans and Democrats also differ over whether the death penalty

is morally justified, whether it acts as a deterrent to serious crime and

whether adequate safeguards exist to ensure that no innocent person is put to

death. Republicans are 29 percentage points more likely than Democrats to say

the death penalty is morally justified, 28 points more likely to say it

deters serious crimes, and 19 points more likely to say that adequate

safeguards exist. But the widest partisan divide – wider than differences in opinions

about the death penalty itself – is over whether White people and Black

people are equally likely to be sentenced to the death penalty for committing

similar crimes. About seven-in-ten Republicans (72%) say that White people and Black

people are equally likely to be sentenced to death for the same types of

crimes. Only 15% of Democrats say this. More than eight-in-ten Democrats

(83%) instead say that Black people are more likely than White people to be

sentenced to the death penalty for committing similar crimes. Differing views of death penalty by race and ethnicity, education,

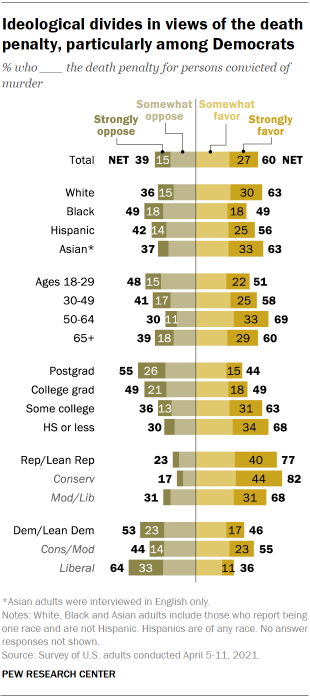

ideology There are wide ideological differences within both parties on this

issue. Among Democrats, a 55% majority of conservatives and moderates favor

the death penalty, a position held by just 36% of liberal Democrats (64% of

liberal Democrats oppose the death penalty). A third of liberal Democrats

strongly oppose the death penalty, compared with just 14% of conservatives

and moderates. Chart shows ideological divides in views of the death penalty,

particularly among Democrats

While conservative Republicans are more likely to express support for

the death penalty than moderate and liberal Republicans, clear majorities of

both groups favor the death penalty (82% of conservative Republicans and 68%

of moderate and liberal Republicans). As in the past, support for the death penalty differs across racial

and ethnic groups. Majorities of White (63%), Asian (63%) and Hispanic adults

(56%) favor the death penalty for persons convicted of murder. Black adults

are evenly divided: 49% favor the death penalty, while an identical share

oppose it. Support for the death penalty also varies across age groups. About

half of those ages 18 to 29 (51%) favor the death penalty, compared with

about six-in-ten adults ages 30 to 49 (58%) and those 65 and older (60%).

Adults ages 50 to 64 are most supportive of the death penalty, with 69% in

favor. There are differences in attitudes by education, as well. Nearly

seven-in-ten adults (68%) who have not attended college favor the death

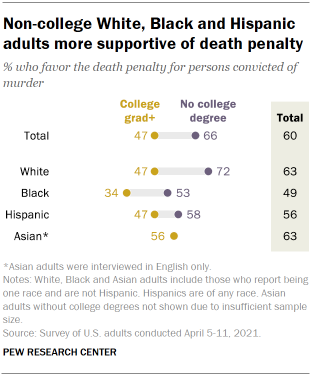

penalty, as do 63% of those who have some college experience but no degree. Chart shows non-college White, Black and Hispanic adults more

supportive of death penalty About half of those with four-year undergraduate degrees but no

postgraduate experience (49%) support the death penalty. Among those with

postgraduate degrees, a larger share say they oppose (55%) than favor (44%)

the death penalty.

The divide in support for the death penalty between those with and

without college degrees is seen across racial and ethnic groups, though the

size of this gap varies. A large majority of White adults without college

degrees (72%) favor the death penalty, compared with about half (47%) of

White adults who have degrees. Among Black adults, 53% of those without

college degrees favor the death penalty, compared with 34% of those with

college degrees. And while a majority of Hispanic adults without college

degrees (58%) say they favor the death penalty, a smaller share (47%) of

those with college degrees say this. Intraparty differences in support for the death penalty Republicans are consistently more likely than Democrats to favor the

death penalty, though there are divisions within each party by age as well as

by race and ethnicity. Republicans ages 18 to 34 are less likely than other Republicans to

say they favor the death penalty. Just over six-in-ten Republicans in this

age group (64%) say this, compared with about eight-in-ten Republicans ages

35 and older. Chart shows partisan gap in views of death penalty is widest among

adults 65 and older

Among Democrats, adults ages 50 to 64 are much more likely than

adults in other age groups to favor the death penalty. A 58% majority of 50-

to 64-year-old Democrats favor the death penalty, compared with 47% of those

ages 35 to 49 and about four-in-ten Democrats who are 18 to 34 or 65 and

older. Overall, White adults are more likely to favor the death penalty than

Black or Hispanic adults, while White and Asian American adults are equally

likely to favor the death penalty. However, White Democrats are less likely

to favor the death penalty than Black, Hispanic or Asian Democrats. About

half of Hispanic (53%), Asian (53%) and Black (48%) Democrats favor the death

penalty, compared with 42% of White Democrats.

About eight-in-ten White Republicans favor the death penalty, as do

about seven-in-ten Hispanic Republicans (69%). Differences by race and ethnicity, education over whether there are

racial disparities in death penalty sentencing There are substantial demographic differences in views of whether

death sentencing is applied fairly across racial groups. While 85% of Black

adults say Black people are more likely than White people to be sentenced to

death for committing similar crimes, a narrower majority of Hispanic adults

(61%) and about half of White adults (49%) say the same. People with

four-year college degrees (68%) also are more likely than those who have not

completed college (50%) to say that Black people and White people are treated

differently when it comes to the death penalty. Chart shows overwhelming majority of Black adults see racial

disparities in death penalty sentencing, as do a smaller majority of Hispanic

adults; White adults are divided About eight-in-ten Democrats (83%), including fully 94% of liberal

Democrats and three-quarters of conservative and moderate Democrats, say

Black people are more likely than White people to be sentenced to death for

committing the same type of crime – a view shared by just 25% of Republicans

(18% of conservative Republicans and 38% of moderate and liberal

Republicans). Across educational and racial or ethnic groups, majorities say that

the death penalty does not deter serious crimes, although there are

differences in how widely this view is held. About seven-in-ten (69%) of

those with college degrees say this, as do about six-in-ten (59%) of those

without college degrees. About seven-in-ten Black adults (72%) and narrower

majorities of White (62%) and Hispanic (63%) adults say the same. Asian

American adults are more divided, with half saying the death penalty deters

serious crimes and a similar share (49%) saying it does not. Among Republicans, a narrow majority of conservative Republicans

(56%) say the death penalty does deter serious crimes, while a similar share

of moderate and liberal Republicans (57%) say it does not. A large majority of liberal Democrats (82%) and a smaller, though

still substantial, majority of conservative and moderate Democrats (70%) say

the death penalty does not deter serious crimes. But Democrats are divided

over whether the death penalty is morally justified. A majority of

conservative and moderate Democrats (57%) say that a death sentence is

morally justified when someone commits a crime like murder, compared with

fewer than half of liberal Democrats (44%). There is widespread agreement on one topic related to the death

penalty: Nearly eight-in-ten (78%) say that there is some risk an innocent

person will be put to death, including large majorities among various racial

or ethnic, educational, and even ideological groups. For example, about two-thirds

of conservative Republicans (65%) say this – compared with 34% who say there

are adequate safeguards to ensure that no innocent person will be executed –

despite conservative Republicans expressing quite favorable attitudes toward

the death penalty on other questions. Overwhelming share of death penalty supporters say it is morally

justified Those who favor the death penalty consistently express more favorable

attitudes regarding specific aspects of the death penalty than those who

oppose it. Chart shows support for death penalty is strongly associated with

belief that it is morally justified for crimes like murder

For instance, nine-in-ten of those who favor the death penalty also

say that the death penalty is morally justified when someone commits a crime

like murder. Just 25% of those who oppose the death penalty say it is morally

justified. This relationship holds among members of each party. Among

Republicans and Republican leaners who favor the death penalty, 94% say it is

morally justified; 86% of Democrats and Democratic leaners who favor the

death penalty also say this. By comparison, just 35% of Republicans and 21% of Democrats who

oppose the death penalty say it is morally justified. Similarly, those who favor the death penalty are more likely to say

it deters people from committing serious crimes. Half of those who favor the

death penalty say this, compared with 13% of those who oppose it. And even

though large majorities of both groups say there is some risk an innocent

person will be put to death, members of the public who favor the death

penalty are 24 percentage points more likely to say that there are adequate

safeguards to prevent this than Americans who oppose the death penalty. On the question of whether Black people and White people are equally

likely to be sentenced to death for committing similar crimes, partisanship

is more strongly associated with these views than one’s overall support for

the death penalty: Republicans who oppose the death penalty are more likely

than Democrats who favor it to say White people and Black people are equally

likely to be sentenced to death. Among Republicans who favor the death penalty, 78% say that Black and

White people are equally likely to receive this sentence. Among Republicans

who oppose the death penalty, about half (53%) say this. However, just 26% of

Democrats who favor the death penalty say that Black and White people are

equally likely to receive this sentence, and only 6% of Democrats who oppose

the death penalty say this. (PEW) JUNE 2, 2021 693-43-14/Poll Four In Ten (40%) Working Canadians Say They’ve Experienced A Decline

In Their Physical Health Throughout The Pandemic

Toronto, ON, June 1, 2021 — As

vaccination rates have ramped up across the country, and businesses are

starting to prepare for a post-pandemic future, working Canadians continue to

face a number of health-related challenges. Four in ten (40%) working

Canadians say they’ve experienced a decline in their physical health

throughout the pandemic, according to a recent Ipsos poll conducted on behalf

of RBC Insurance. The inability to socialize with family, friends or

co-workers (72%) and work-related stress (58%) were also cited as factors

impacting overall health. Barriers Remain for Some Workers Throughout the pandemic, working Canadians with chronic health issues

have faced increased barriers receiving the care they need, with over six in

ten (63%) noting the inability to visit a doctor or healthcare clinic has

negatively impacted their health. Those with a chronic health issue are more

likely to cite this compared to those without a chronic health issue (47%). Although a majority (58%) of working Canadians with a chronic health

issue or disability say their condition would deteriorate further without

their workplace benefits plan, four in ten (40%) say they have also

experienced challenges accessing their employees benefits due to their unique

needs. Virtual Care Solutions Useful for Employees

with Disabilities or Health Issues Among those who have group benefits or private coverage, Canadian

employees with a disability or a chronic heath issue are more likely to have

access to virtual care tools (48% and 51% respectively) compared to those who

do not. As well, those with a chronic health issue are more likely to agree

that using virtual tools to connect with mental health support has been

useful (64% vs 50% with no chronic health issue). (Ipsos Canada) 1 June 2021 AUSTRALIA

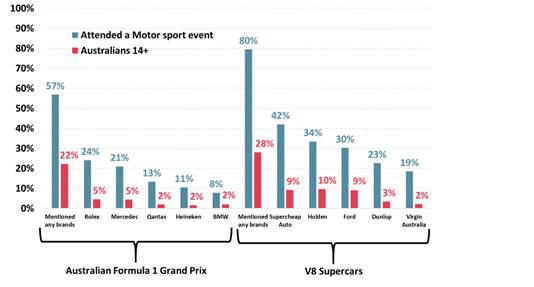

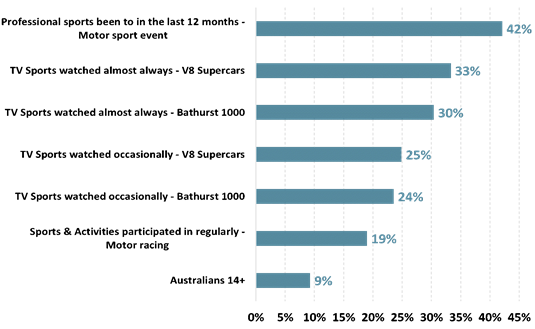

693-43-15/Poll Australian Formula 1 Grand Prix In Doubt For 2021 But It’s The

Ongoing V8 Supercars Series That Provides Value For Sponsors

Nearly 4.6 million Australians watched motorsports including Formula

1, V8 Supercars, the Bathurst 1000, Drag racing and Rally car racing on TV in

2020. The leading motor sports events watched by Australians on TV are the

Bathurst 1000 watched by over 3.1 million, the V8 Supercars watched by 2.6

million and the Formula 1 watched by nearly 2.3 million. Of the 362,000 who attended a motorsports event last year a large

majority of 80% can name at least one brand they associate with V8 Supercars

compared to a smaller majority of 57% who can name a brand associated with

the Australian Formula 1 Grand Prix. In contrast, only around a quarter of all Australians, 28%, can name

a brand associated with V8 Supercars and just over a fifth, 22%, can name a

brand associated with the Australian Formula 1 Grand Prix. For those attending motor sport events the top brand associated with

V8 Supercars is former Bathurst 1000 naming rights sponsor Supercheap Auto

mentioned by 42% of attendees ahead of well-known Australian car brands

Holden (34%) and Ford (30%). Former V8 Supercars series naming rights sponsor

Virgin Australia is mentioned by 19% of motor sport attendees and is the

fifth most recognised sponsor of V8 Supercars. Clearly the top two sponsors associated with the Australian Grand

Prix are current naming rights sponsor Rolex mentioned by 24% of motor sport

attendees and leading car manufacturer Mercedes mentioned by 21%. In a sign of how enduring sports sponsorship associations are it is

former naming rights sponsor Qantas in third that is mentioned by 13% of

motor sport attendees as being associated with the Grand Prix. Qantas was the

naming rights sponsor for the Australian Formula 1 Grand Prix from 2010-2012

– nearly a decade ago. Top 5 Brands associated with Formula 1

& V8 Supercars by Australians and motor sport attendees

Supercheap Auto recall is highest for motor

sport attendees ahead of TV viewers Analysing brand association for last year’s Bathurst 1000 naming

rights sponsor Supercheap Auto shows that Australians who have attended a