|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 695-696 Week:

June 14 –June 27, 2021 Presentation:

July 05, 2021 16%

Pakistanis Claim To Have Bought Something Online During The Past 6 Months Awareness

Levels Of The New RTR Guidelines Amongst Consumers Is Quite Low 17% In South

Africa 4

In 10 (44%) Britons Believe That There Are Still Many Important Issues To

Finalise With The EU One

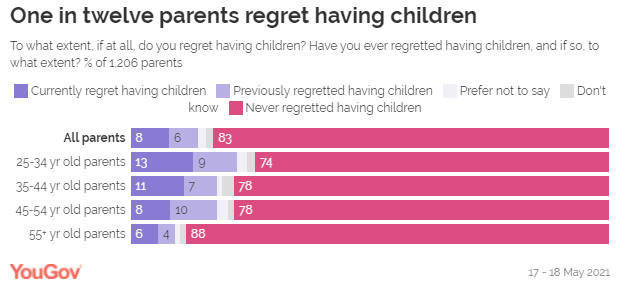

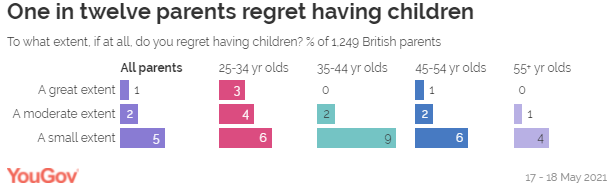

In Twelve Parents Say They Regret Having Children 1

In 5 Spaniards Will Continue To Use The Mask Despite Not Being Mandatory Nearly

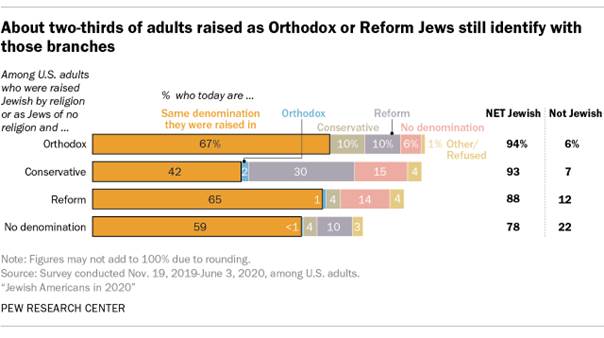

Nine-In-Ten U.S. Adults Who Were Raised Jewish (88%) Are Still Jewish Today About

Six-In-Ten U.S Adults (63%) Have A “Very” Or “Mostly” Favorable Opinion Of

Pope Francis Eight

In Ten (82%) Canadians Vaccinated Or Awaiting Vaccine; Remaining 18% Need To

Be Convinced ALP

(50.5%) Leads L-NP (49.5%) On A Two-Party Preferred Basis – No Bounce For Pm

From G7 Trip Three

In Five Urban Indians Would Watch More Of Women’s Sport If It Was More

Accessible On TV YouGov In

Five Of Seven MENA States At Least 40 Percent Have A Favorable View Of France

Overall Global

Country Average Of 74% Say There Is At Least A Fair Amount Of Tension Between

Rich And Poor INTRODUCTORY NOTE

695-696-43-45/Commentary: 69% Americans Are Most Likely To Indicate They Will

Currently Still Wear A Mask On Airplanes Or Trains

We explored

where Americans will continue to wear masks, and whether they assume that

people wearing a mask have not been vaccinated. The questions about

mask-wearing were only asked to Americans because a greater proportion of the

American population is currently fully vaccinated. With second doses of

COVID-19 vaccines being available earlier in certain provinces, we also

explored Canadians’ perspectives on receiving a second dose. This survey is conducted in collaboration with the Association for

Canadian Studies (ACS) and published in the Canadian Press. This series

of surveys is available on Leger’s

website THE FUTURE

OF WEARING A MASK IN THE UNITED STATES

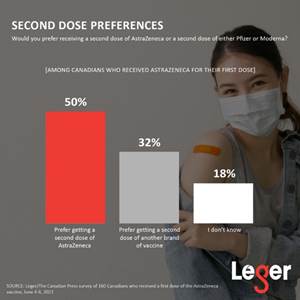

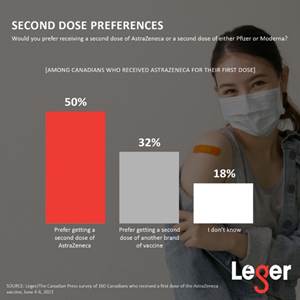

RECEIVING A

SECOND DOSE OF ASTRAZENECA

(Leger) June 15th,

2021 Source: https://leger360.com/surveys/legers-north-american-tracker-june-15-2021/ 695-696-43-46/Country Profile:

SUMMARY

OF POLLS

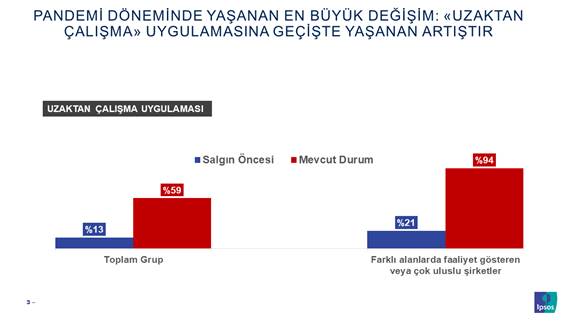

ASIA (Turkey) Among

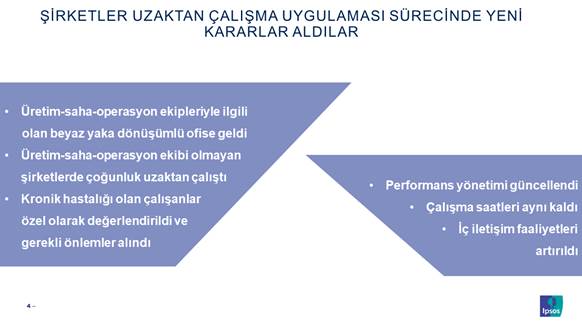

White-Collar Employees, The Remote Working Practice, Which Was 13% Before The

Epidemic, Has Now Reached 59% In Turkey According to the data we gathered from

white-collar employees, the remote working practice, which was 13% before the

epidemic, has now reached 59%. In multinational companies or operating

in different fields, we see that remote working has increased from 21% to

94%. Decisions were made on which teams would come to the office, which teams

would work remotely, applications for those with chronic diseases,

performance system adaptations, working hours and how internal communication

activities would be carried out. (Ipsos Turkey) 21 June 2021 (Pakistan) 16% Pakistanis Claim To Have Bought

Something Online During The Past 6 Months According to a survey conducted by Gallup

& Gilani Pakistan, 16% Pakistanis claimed to have shopped online during

the past 6 months. A nationally representative sample of adult men and

women from across the four provinces was asked the following question, “Have you done any online shopping during the past

six months i.e. did you buy any thing/product online?” In

response to this question, 16% said ‘Yes’, 82% said ‘No’ while 2% did not

know/did not respond. (Gallup Pakistan) June 23, 2021 AFRICA (Nigeria) 88 Percent Of Nigerians Believe That Child Labor Is

Prevalent In Nigeria While 12 Percent Mentioned That It Is Not Prevalent To commemorate the Child Labour Day,

NOIPolls conducted a survey to gauge the opinion of Nigerians on child labour

and the result revealed that 88 percent of Nigerians believe that child

labour is prevalent in Nigeria while 12 percent mentioned that it is not

prevalent. This further corroborates the findings of the International Labour

Organisation (ILO) which states that there are 152 million children in the

whole world engaged in child labour while there are 15 million children

undergoing different forms of child labour in Nigeria which is the highest in

West Africa[3]. (NOI Polls) June 16, 2021 (South

Africa) 3 In Ten (27%) Adult South Africans And Four In Ten (37%)

Young People In The Country Are Looking For Work; Youth Day 2021 Figures from Statistics South Africa confirmed that the Youth unemployment

rate in South Africa increased to 63.3% in the first quarter of 2021 from

63.2% in the fourth quarter of 2020. By no means do we want to underplay the

dire need for job creation in our country, as roughly 3 in ten (27%) adult

South Africans and four in ten (37%) young people in the country are looking

for work. The frightening high figure of youth unemployment needs some

unpacking. (Ipsos South Africa) 16 June 2021 Awareness Levels Of The New RTR Guidelines

Amongst Consumers Is Quite Low 17% In South Africa The current awareness levels of the new RTR

guidelines amongst consumers are low - with only 17% of respondents saying

they have heard of it and have a good grasp or thorough knowledge of what the

new guidelines entail. The main advantages for consumers relate to “freedom

of choice” when choosing which warranty and/or maintenance plan to purchase.

This allows them to “shop around” and decide on where to service or repair

their vehicles. Further to this, 50% of consumers feel that RTR will

financially benefit them. (Ipsos South Africa) 17 June 2021 More Than Half 63% Of The Owners Of Small,

Medium And Micro Enterprises (SMME’s) Saying They Experienced Great

Uncertainty Regarding The Sustainability Of Their Businesses The impact of the pandemic and subsequent

lockdown on business performance have been significant, with 63% of SMME’s

stating that they are performing “Not Well” or “Not Very Well” after

lockdown, while larger enterprises are seemingly more resilient, with a third

(35%) stating that they are still performing “Well” or “Very Well” after

lockdown. (Ipsos South Africa) 27 June 2021 (Zimbabwe) 81% Zimbabweans Strongly Agree With The Fact That Even If

The Lockdown Had Negative Impacts But It Was Necessary A new Afrobarometer survey shows that even

though almost half of Zimbabwean households lost a primary source of income

during the COVID-19 pandemic, most citizens approve of the government’s

overall management of the pandemic. Most Zimbabweans endorse lockdowns and

school closures as painful but necessary. (Afrobarometer) 17 Jun 2021 WEST

EUROPE (UK) Only 6% Of Brits Think Increasing House Prices Would Be

Beneficial For The Country, But One-Fifth (20%) Say It Would Be Advantageous

For Their Personal Finances Most recent figures show that the housing

market is growing at its fastest rate in seven years – a jump of 9.5% in the year to May.

Experts suggest that ‘market activity continues to be

boosted by the government’s stamp duty holiday’ and that this boom period may

continue as the ‘unexpected savers’ of the pandemic look to invest their

extra money. Now, new YouGov tracking data shows that 58% of Brits expect

prices of homes to go up in the year ahead while 21% expect them to stay

about the same, and only 6% anticipate a dip. (YouGov UK) June 14, 2021 Three In Ten (31% Of 18-34’s) Football Fans

Say Live TV Is A Thing Of The Past (Compared To 20% Of Over 35s) Comparing football fans aged 18-34 and

over-35s reveals key differences in viewing preferences. While TV

is still the most popular way to watch the game, older fans are more likely

to turn on the telly to watch live football

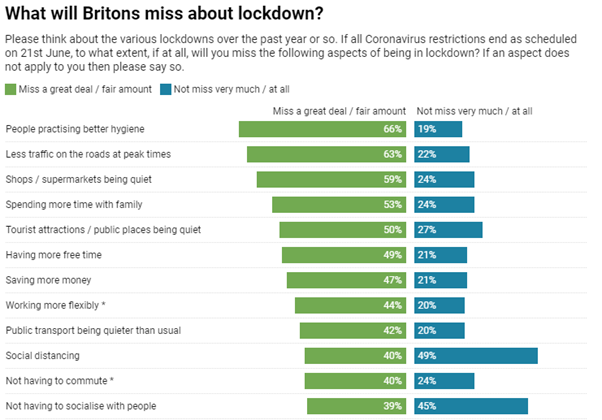

(87% vs. 82% of 18-34s) and highlights (67% vs. 61% of 18-34s). (YouGov UK) June 17, 2021 Britons Will Miss Practicing Better Hygiene

(66%), Less Traffic On Roads At Peak Times (63%) And Quiet Shops And

Supermarkets (59%) New polling by Ipsos MORI shows that while

many will be ready to see the end of lockdown, there are plenty of aspects of

lockdown that will be missed. Among the things most likely to be looked back

on fondly are people practising better hygiene with two-thirds saying they

will miss this at least a fair amount (66%), less traffic on roads at peak

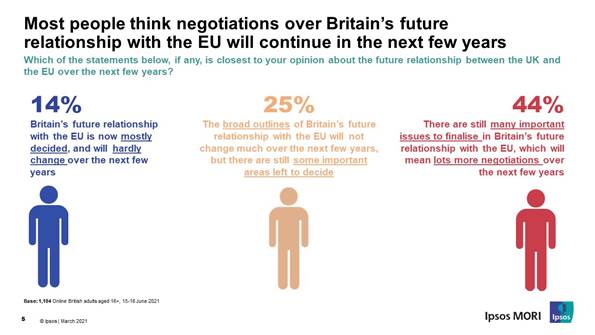

times (63%) and quiet shops and supermarkets (59%). (Ipsos MORI) 20 June 2021 4 In 10 (44%) Britons Believe That There

Are Still Many Important Issues To Finalise With The EU New polling by Ipsos MORI, in partnership

with UK

in a Changing Europe,

finds that 4 in 10 (44%) Britons believe that there are still many important

issues to finalise with the EU, with Remain voters most likely to feel this

way about negotiations (62%). In contrast, 30% of leave voters say

there are still many important issues to discuss. (Ipsos MORI) 23 June 2021 Around Two In Five (63%) Of The

Unvaccinated Are Convinced By Arguments Which Say There Hasn’t Been Enough

Time To See What The Side-Effects Of The Vaccine Might Be Before the vaccine roll-out began late last

year, the majority of Britons were convinced by the argument that there had

not been enough time to see the side-effects of the vaccine – now just two in

five (41%) think the same, down 20ppt. Similarly, only three in ten

(31%) are convinced by the argument that vaccine doses will be limited, and

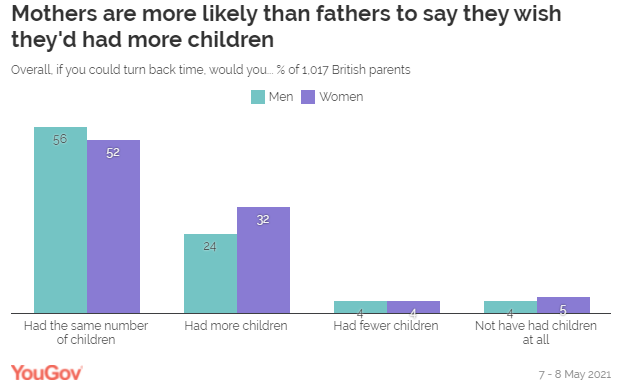

others will need them more, 20ppt fewer than last November. (Ipsos MORI) 24 June 2021 One In Twelve Parents Say They Regret

Having Children YouGov data shows that while the vast

majority of parents (83%) insist they’ve never felt this way, a small number

admit to it. One in twelve parents (8%) say they regret having children,

while another 6% have previously had regrets but don’t now. While there’s no

difference between mothers and fathers, younger parents aged 25 to 34 are the

most likely to feel regretful, with one in five either rueing their choice

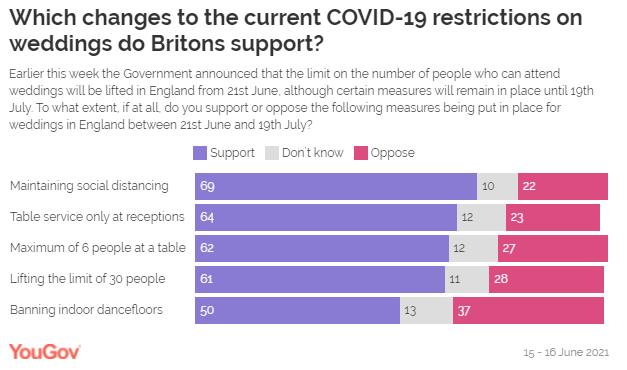

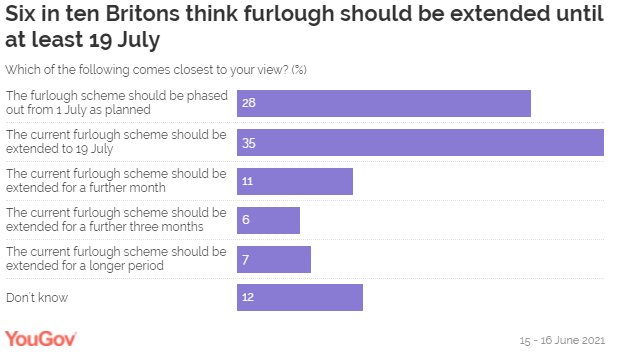

(13%) or having done so (9%). (YouGov UK) June 24, 2021 Despite General Hesitancy For Loosening

Restrictions, 61% Of The Public Support Lifting The Limit Of 30 Attendees In

Weddings Despite

general hesitancy for loosening restrictions, 61% of the public support

lifting the limit of 30 attendees. Perhaps unsurprisingly, three quarters

(74%) of those who are attending a wedding in the next month support the

measure, compared to 60% of people who will not be affected by the rule

change. Despite the delay to the roadmap, the government has stated that the

furlough scheme will be phased out from 1 July as planned. Through the

pandemic, furloughed workers have had 80% of their wage paid by the

government (YouGov UK) June 24,

2021 (Germany) Around 13,000 People In Germany Develop Blood Cancer Every

Year, For Which A Stem Cell Donation Is Often The Last Chance Of A Cure In addition to the 22 percent who are

already entered in a stem cell donor register or have even donated stem

cells, another 40 percent of those questioned are potential donors. One

in ten (10%) is already determined to register, almost one in three (30%) is

“perhaps ready”. Among the 18- to 34-year-olds, one in four (25%) is

already registered and, at 17 percent, a clearly above-average proportion

decided to register. Another 28 percent may be willing to donate stem

cells. The potential for potential donors is particularly high among

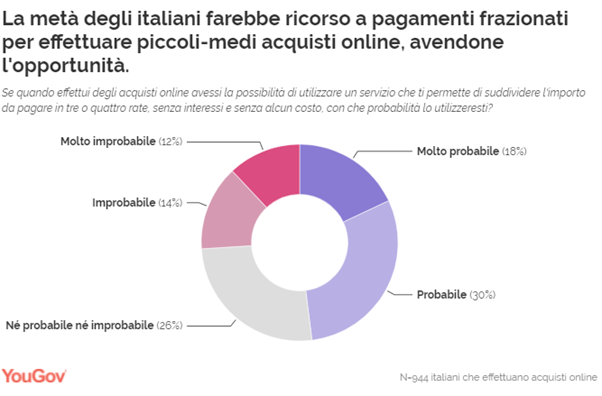

younger adults. (Ipsos Germany) June 24, 2021 (Italy) Nearly Half (48%) Of People Who Regularly Shop Online Would

Use “Buy Now, Pay Later” Service If It Were Available Italians are receptive to this

idea. In fact, nearly half (48%)

of people who regularly shop online would use such a service

if it were available. However, the new services are not yet well known: at

the moment in Italy there are three brands that offer this service, and

knowledge of all of them is still very limited: these are Scalapay (11%),

Klarna (5%) and Afterpay (3%) (YouGov Italy) June 14, 2021 (France) Since 2018, Internet Sales Are Twice As

Popular (Going From 11% To 22%) - Particularly By Women (28%) And Young

People (39% Of 25-34 Year Olds) Donations to associations come first (39%),

followed by internet sales (22%) and donations to people around them (14%). Since

2018, internet sales are twice as

popular (going from 11% to 22%) - particularly by women (28%)

and young people (39% of 25-34 year olds).

Note: 12% of respondents say they leave things they no longer carry in their

closet (-4 points since 2018) and 7% throw them in the trash. (YouGov France) June 14, 2021 (Spain) 1 In 5 Spaniards Will Continue To Use The Mask Despite Not

Being Mandatory Next Saturday one of the Covid-19 sanitary

measures that generated the most controversy from the beginning and that, in

turn, most bothered many will be modified: the mandatory use of masks outdoors . Although the

specific details are not yet known, starting next Saturday, June 26,

Spaniards will be able to walk through the streets, beaches and mountains

without having to use a complement that was already part of everyone's

routine. (Ipsos Spain) June 22, 2021 NORTH AMERICA (USA) 69% Americans Are Most Likely To Indicate They Will

Currently Still Wear A Mask On Airplanes Or Trains Americans are most likely to indicate they

will currently still wear a mask on

airplanes or trains (69%), at large stores (grocery, general goods, etc.)

(65%) and/or in small stores (convenience stores, etc.) (62%). More than

three-in-ten Americans who still wear a mask on airplanes/trains, at large

stores, at small stores, at sporting events or concerts, and/or at

bars/restaurants think they will not

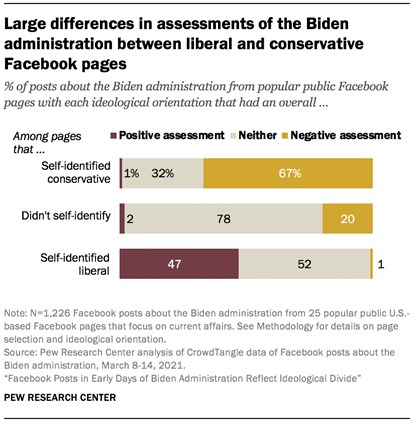

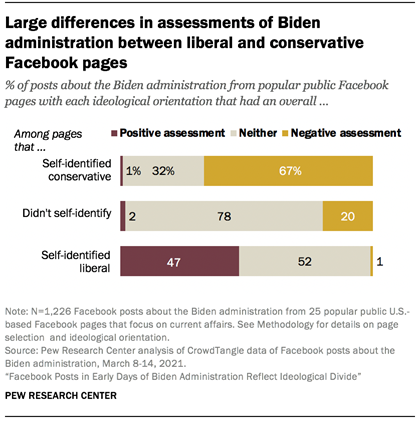

stop wearing a mask at/in each of these until 2022. (Leger) June 15th, 2021 About One-Third (32%) Of The Posts On

Conservative Facebook Pages And Roughly Half (52%) On Liberal Pages Were

Neither Positive Nor Negative Among popular Facebook pages that describe

themselves as conservative (12 of the 25 pages studied), 1% of posts

carried positive assessments of the Biden administration, while

67% were negative. For those pages that self-identified as liberal (11 of the

25), only 1% of the posts carried negative assessments while 47% had a

positive one. About one-third (32%) of the posts on conservative Facebook

pages and roughly half (52%) on liberal pages were neither positive nor

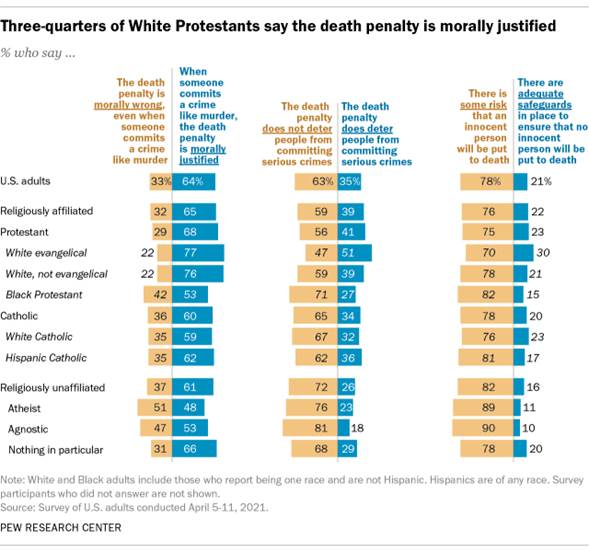

negative.2 (PEW) JUNE 14, 2021 Roughly Two-Thirds Of Atheists (65%) And

Six-In-Ten Agnostics (57%) Either “Strongly” Or “Somewhat” Oppose The Death

Penalty For People Convicted Of Murder Roughly two-thirds of atheists (65%) and

six-in-ten agnostics (57%) either “strongly” or “somewhat” oppose the death

penalty for people convicted of murder. Atheists and agnostics are small

religious groups, representing less than 10% of the adult population, but their share has grown in recent

years. Meanwhile, 60% of U.S. adults overall favor the death penalty, including 75% of White

evangelical Protestants and 73% of White non-evangelical Protestants,

according to the survey, which was conducted in early April. White

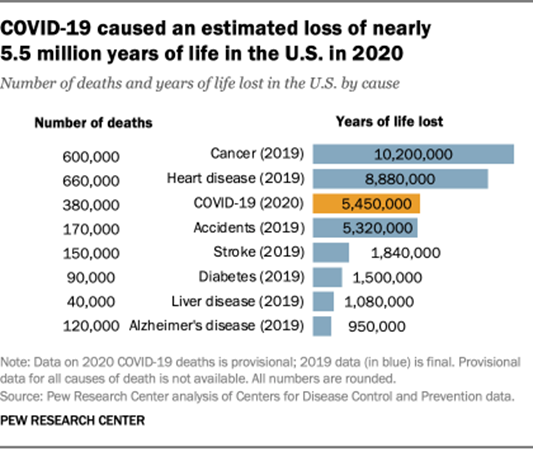

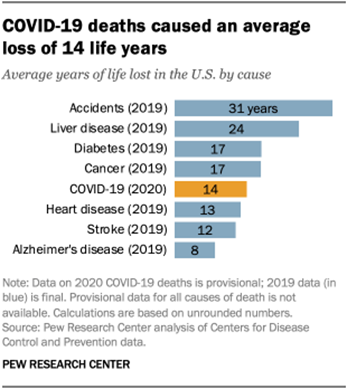

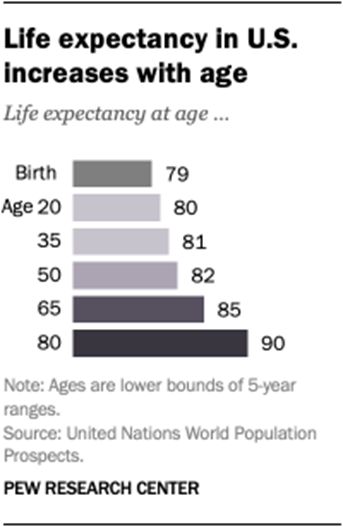

Protestants account for about 29% of the U.S. population, a share that has shrunk in recent years. (PEW) JUNE 15, 2021 Americans Lost More Years (5.5 Million) Of

Life To Covid-19 In 2020 Than To All Accidents Combined In A Typical Year Average life spans change with age as

common causes of death shift over time. By the time a U.S. adult lives to 65,

they are unlikely to die from some common causes of death among younger

people, such as homicide, pregnancy complications or congenital diseases. At

the same time, older Americans are more likely than their younger

counterparts to die from causes including heart disease, Alzheimer’s – and

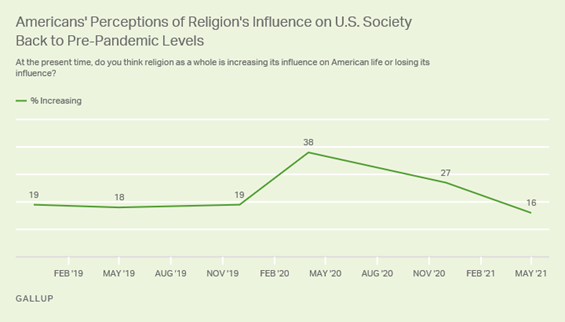

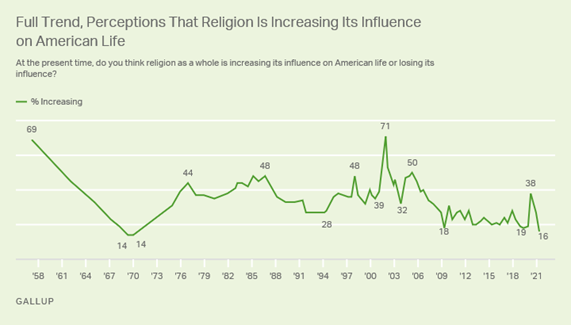

now COVID-19. (PEW) JUNE 16, 2021 The Percentage Of Americans Who Believe

That Religion Is Increasing Its Influence On American Life Has Retreated To

16%, In Line With Pre-Pandemic Levels After doubling last spring and staying

elevated in December, the percentage of Americans who believe that religion

is increasing its influence on American life has retreated to 16%, in line

with pre-pandemic levels. Line graph. Sixteen percent of U.S. adults say

religion is increasing its influence on American life, down from 38% in May

2020 and 27% in December 2020. In late 2018 and late 2019, a consistent 19%

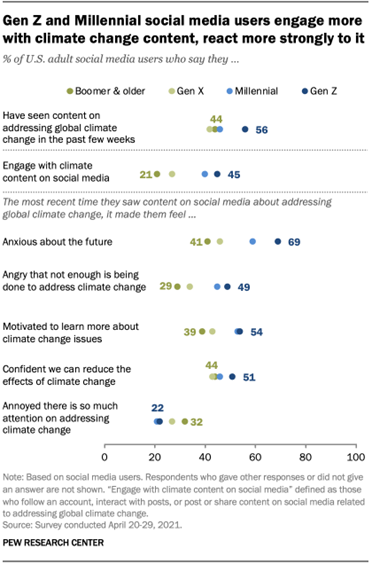

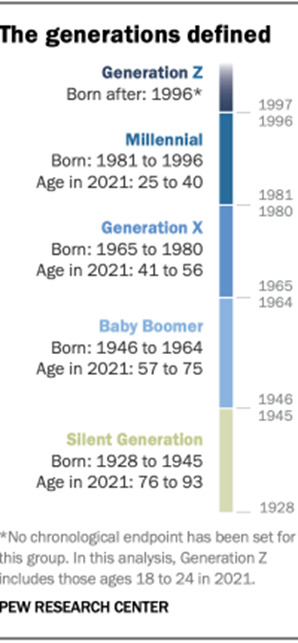

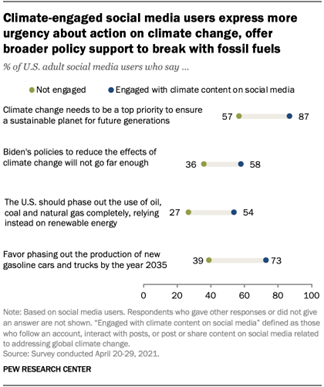

said religion was increasing its influence. (Gallup USA) JUNE 21, 2021 45% Of Gen Z Adults And 40% Of Millennials

Have Interacted With Content On Social Platforms That Focuses On The Need For

Action On Climate Change Among U.S. social media users, 45% of Gen Z

adults and 40% of Millennials have interacted with content on social

platforms that focuses on the need for action on climate change by following

an account, liking or commenting on a post, or posting or sharing content

about the need for action on climate change. By contrast, much smaller shares

of Gen X (27%) and Baby Boomer and older social media users (21%) have

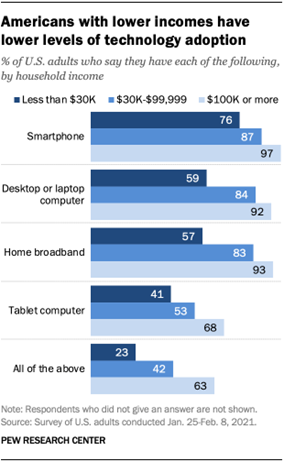

engaged with content about climate change in any of these ways. (PEW) JUNE 21, 2021 About Four-In-Ten Adults With Lower Incomes

Do Not Have Home Broadband Services (43%) Or A Desktop Or Laptop Computer

(41%) Roughly a quarter of adults with household

incomes below $30,000 a year (24%) say they don’t own a smartphone. About

four-in-ten adults with lower incomes do not have home broadband services

(43%) or a desktop or laptop computer (41%). And a majority of Americans with

lower incomes are not tablet owners. By comparison, each of these

technologies is nearly ubiquitous among adults in households earning $100,000

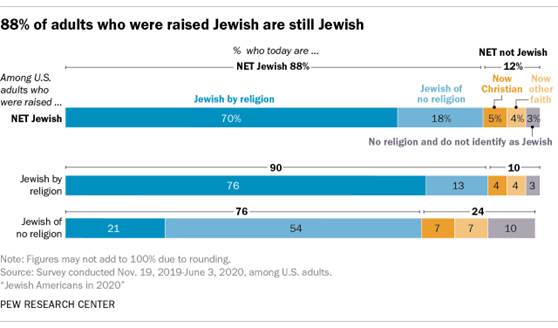

or more a year. (PEW) JUNE 22, 2021 Nearly Nine-In-Ten U.S. Adults Who Were

Raised Jewish (88%) Are Still Jewish Today Overall, nearly nine-in-ten U.S. adults who

were raised Jewish (88%) are still Jewish today. This includes 70% who

identify with the Jewish religion and 18% who don’t identify with any

religion but who consider themselves Jewish in some other way, such as

culturally, ethnically or by family background. (PEW) JUNE 22, 2021 About Six-In-Ten U.S Adults (63%) Have A

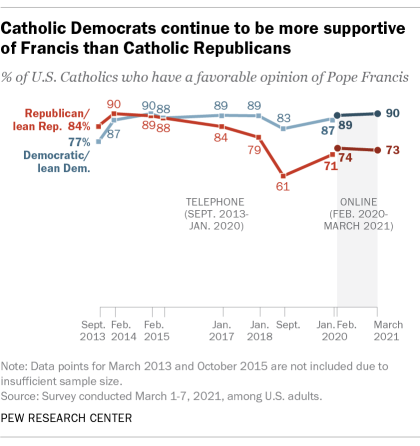

“Very” Or “Mostly” Favorable Opinion Of Pope Francis About six-in-ten U.S adults (63%) have a

“very” or “mostly” favorable opinion of Pope Francis, according to a Pew

Research Center survey conducted in March using the Center’s online American Trends Panel. This is nearly identical to the share of

adults who had a favorable view of Francis in February 2020 (64%). The pope’s

favorability also has remained steady among U.S. Catholics, with 82% of

Catholics in both the March 2021 and February 2020 surveys saying they have a

favorable opinion of the pope. (PEW) JUNE 25, 2021 (Canada) The Housing Crisis In Canada: Three-Quarters (75%) Of

Canadians Who Don’t Own A Home But Want To Buy One, Say They Can’t Afford To A new Ipsos poll conducted on behalf of

Manulife Bank reveals that there might be an affordability crisis in Canada,

with many struggling to keep up with the cost of living or admitting that

home ownership has become a pipe dream for them. The situation has developed

into a tragedy for many prospective homeowners, as three-quarters (75%) of

those who do not own a home but want to buy one feel like they can’t afford

to do so. What’s more, most (71%) of those who do not own a home worry about

saving up for one, including four in ten (39%) who worry a lot about this. (Ipsos Canada) 17 June 2021 Eight In Ten (82%) Canadians Vaccinated Or Awaiting

Vaccine; Remaining 18% Need To Be Convinced The poll found that nearly three-quarters

(73%) of Canadian adults say they have received at least one dose of a

vaccine and another 10% say that they would like to be vaccinated. With the

most recent data from the Government of Canada indicating that 70% of those

aged 12 years and older have received at least one dose,[1] these findings are in line with

overall population trends. (Ipsos Canada) 18 June 2021 Half (51%) Of Canadians Anxious About Returning To Normal

Life Following The Pandemic, Though Cautious Optimism Evident A recent Ipsos poll on conducted on behalf

of Global News finds that half (51%) of Canadians feel nervous about resuming

normal activities post-pandemic, and a third (35%) feel their province is

re-opening too quickly, suggesting that there may be a ways to go before we

truly feel “normal” again, and mixed feelings when it comes to changes many

may have been looking forward to for over a year. (Ipsos Canada) 19 June 2021 One Quarter Of Canadians (26%) Are Not Confident That Their

Family Would Be Able To Pay For Mortgage/Rent/Housing Costs, If They Were To

Pass Away Over the course of the pandemic, Canadians

admit they are having more frequent conversations about important topics.

According to a recent survey study done by Ipsos, over half of Canadian

parents (56%) are having more frequent conversations about their children’s

future. Additional conversations include concerns about finances/financial

goals/debt (38%), and family’s financial security if they were to pass away

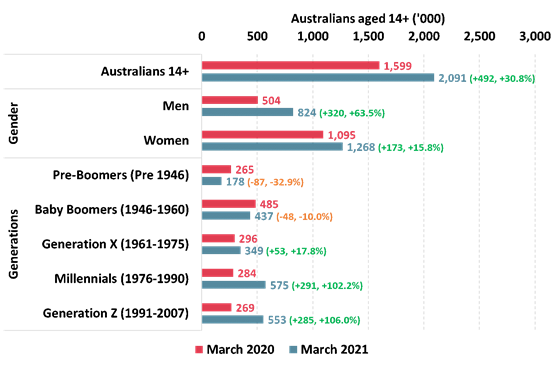

(28%). (Ipsos Canada) 22 June 2021 AUSTRALIA Over 2 Million Australians Are Now Reading Puzzle Magazines

– Up An Exceptional 492,000 (+30.8%) From A Year Ago Women are the most avid readers of puzzle

magazines – now read by 1,268,000 women, up 173,000 (+15.8%) from a year ago.

However, readership of puzzle magazines by men has increased far faster and

is up by 320,000 (+63.5%) to 824,000. There has also been growth among Gen X

with 349,000 now reading Puzzle Magazines, up 53,000 (+17.8%) from a year

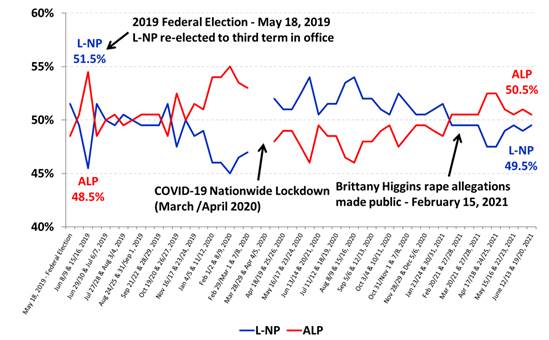

ago, but older generations have not seen growth over the last year. (Roy Morgan) June 21 2021 ALP (50.5%) Leads L-NP (49.5%) On A

Two-Party Preferred Basis – No Bounce For Pm From G7 Trip If a Federal Election were held now it

would be too close to call with a higher than usual 7.5% of electors

undecided about who they would vote for and with the real possibility

Australia would have a hung Parliament for the first time in nearly a decade.

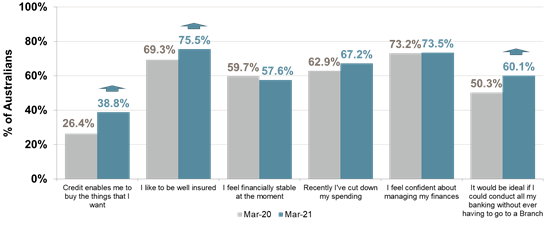

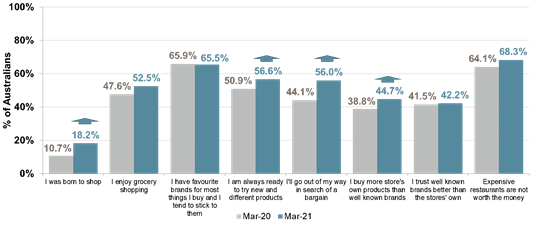

Normally around 3-4% of electors can’t say who they would vote for. (Roy Morgan) June 23 2021 In The 12 Months To March 2021 A

Fast-Rising 38.8% Of Australians Agree That ‘Credit Enables Me To Buy

The Things I Want’ – An Increase Of 12.4% Points From A Year Ago

Pre-Covid-19 In the 12 months to March 2021 a

fast-rising 38.8% of Australians agree that ‘Credit enables me to buy the things I want’ – an

increase of 12.4% points from a year ago pre-COVID-19. This is the largest

increase for any of the financial attitudes covered here and suggests the

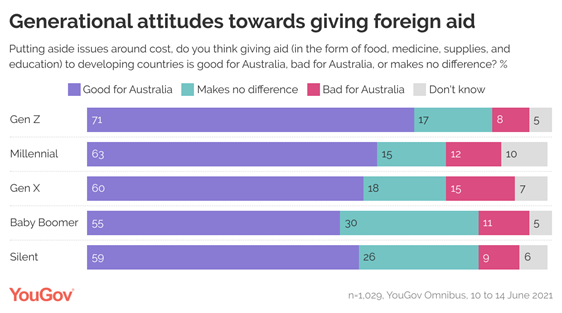

long-term decline in usage of credit is being reversed as alternative payment systems such as Zip and Afterpay enter the market. (Roy Morgan) June 25 2021 60% Of Australians Believe That Giving Aid

To Developing Nations Is Good For Australia, Compared With 21% Who Believe

That It Makes No Difference Data collected by YouGov, the international

data and polling company, shows that Australians are inclined to think that

sending aid to developing nations is good for their country. 60% of

Australians believe that giving aid to developing nations is ‘good for

Australia’, compared with 21% who believe that it ‘makes no difference’, and

just 12% that hold the opposite opinion that such aid is ‘bad for Australia’.

In turn, only half the British feel this way, and a quarter thinks it makes

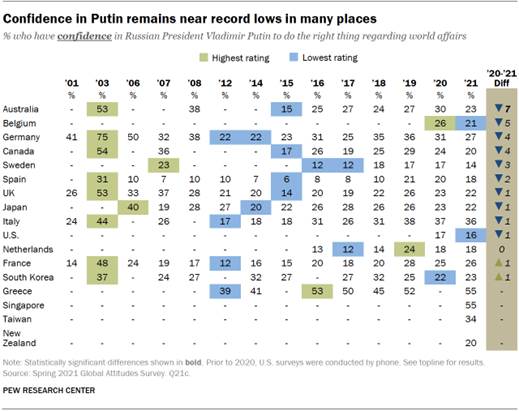

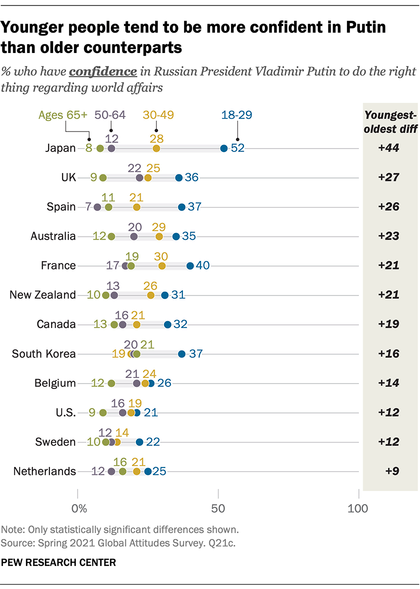

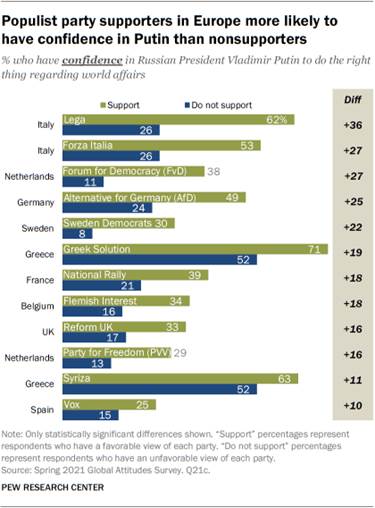

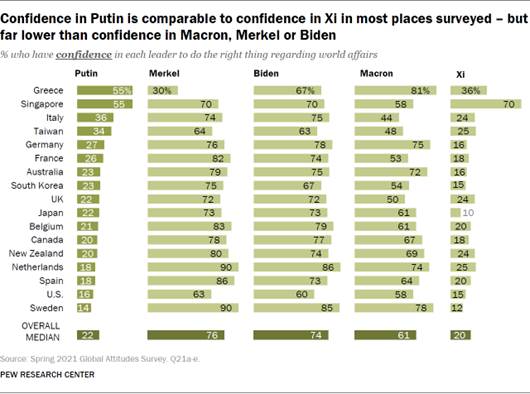

no difference. (YouGov Australia) June 23, 2021 MULTICOUNTRY STUDIES Among 17 Advanced Economies A Median Of 22% Say They Have

Confidence In Putin To Do The Right Thing In World Affairs, Compared With A

Median Of 74% Who Say They Have No Such Confidence Pew Research Center survey conducted this

spring in 17 advanced economies shows that negative views of him are at or

near historic highs in most places. Today, a median of 22% say they have

confidence in Putin to do the right thing in world affairs, compared with a

median of 74% who say they have no such confidence. Singapore (55%), Greece

(55%), Italy (36%) and Taiwan (34%) stand out as the only places surveyed

where roughly a third or more say they have confidence in the Russian

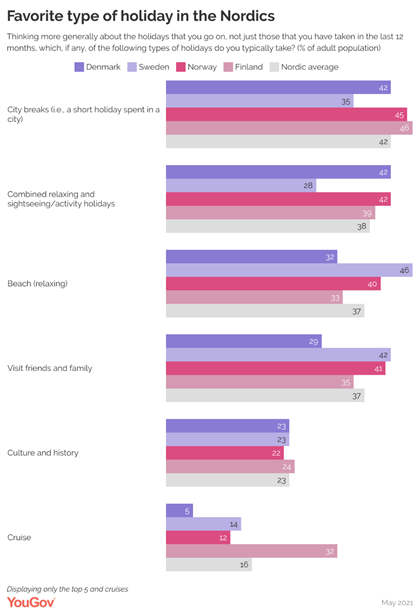

president. Confidence is lowest in Sweden (14%) and the United States (16%). (PEW) JUNE 14, 2021 People In The Nordics Are Mostly Into City

Breaks i.e. Short Holidays Spent In A City, With An Average Of 42 % People

Choosing This Type Of Holiday (Ranging From 35 % Of Swedes To 46 % Of Finns) Overall, people in the Nordics are mostly

into city breaks i.e. short holidays spent in a city, with an average of 42 %

people choosing this type of holiday (ranging from 35 % of Swedes to 46 % of

Finns). Next up are holidays that combine relaxing and sightseeing/activity,

with an average of 38 % – however, this applies to only 28 % of the Swedish

population. Holidays that involve culture and history are furthermore popular

across the Nordic countries (23 %). (YouGov Denmark) Source: https://yougov.dk/news/2021/06/15/most-popular-holiday-types-nordics/ 3 In 4 Britons Believe In The Right To Seek

Refuge, But 2 In 5 Want To Shut Borders Completely At This Time A global survey by Ipsos shows almost

three-quarters of Britons (73%) agree with the principle that people should

be able to take refuge in other countries, including Britain, to escape from

war or persecution. Only 17% of Britons disagree with this, which is lower

than the average across the 28 countries (23%). However, although the

proportion of people disagreeing with the right to seek refuge has remained

largely the same since 2020 (15%), the proportion of Britons agreeing has

decreased by 5 percentage points (78%). (Ipsos MORI) 16 June 2021 Canadians Agree (72%) People Should Be Able

To Seek Refuge From War And Persecution, But Few (10%) Like The Idea Of

Letting In More Refugees Post-Pandemic The attitudes of Canadians mirror those of

the broader international community: the global average shows that 47% agree

that refugees will integrate successfully into their new societies, while 44%

disagree. The attitudes of Canadians fall near the centre: they are not as

optimistic about refugee integration as respondents in Saudi Arabia (76%),

India (68%), or Argentina (60%), but neither are they as pessimistic as

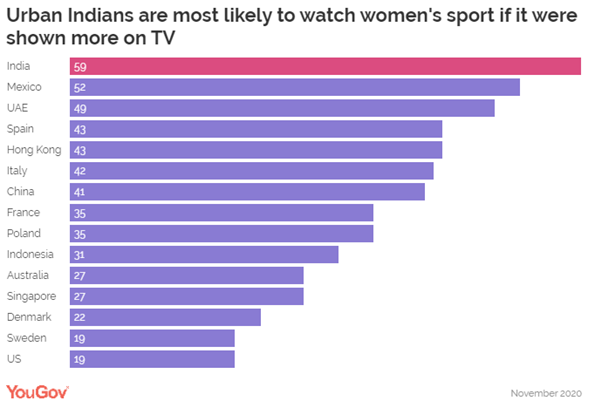

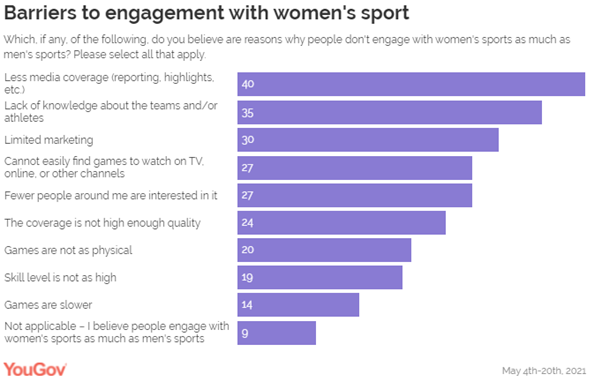

residents of South Korea (29%), France (25%), or Japan (23%). (Ipsos Canada) 22 June 2021 Three In Five Urban Indians Would Watch

More Of Women’s Sport If It Was More Accessible On TV YouGov Globally, a third of

people (33%) say they would watch more women’s sport if it was more

accessible on TV. Agreement with this statement is the highest in India,

followed by Mexico and UAE. The most popular reason people give around the

world for not following women’s sports is the lack of media coverage (40%).

Other supply-side factors acting as barriers to engagement include lack of

knowledge about women’s teams or athletes (35%), lack of marketing (30%) and

limited accessibility of women’s sport on TV (27%). The speed, quality and

physicality of women’s sport is much less likely to be a reason for not

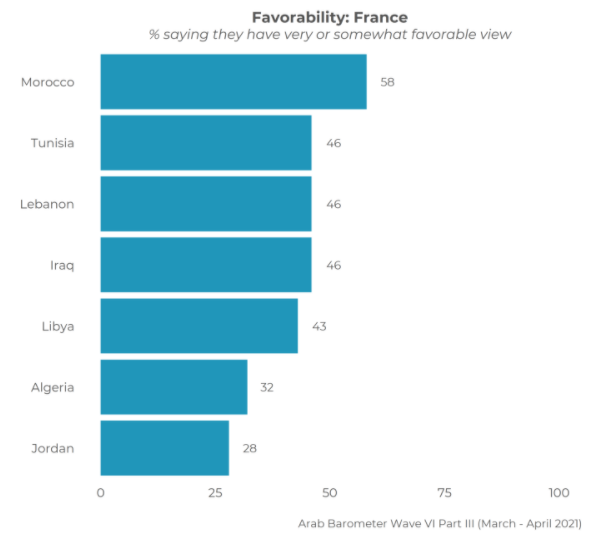

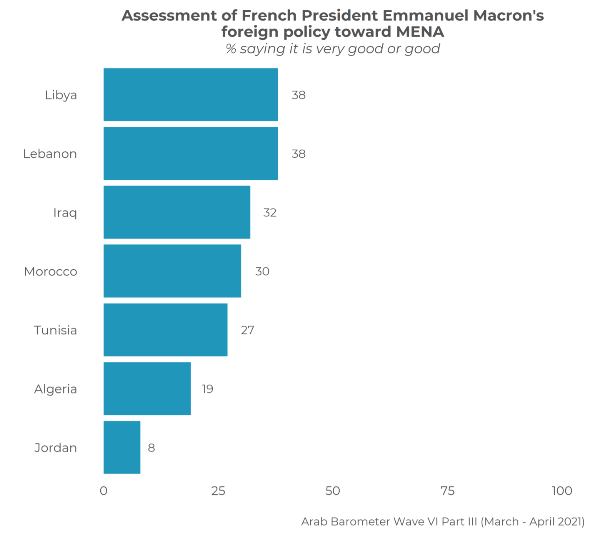

engaging. (YouGov India) Source: https://in.yougov.com/en-hi/news/2021/06/24/three-five-urban-indians-would-watch-more-womens-s/ In Five Of Seven MENA States At Least 40

Percent Have A Favorable View Of France Overall In 2020, he personally interceded to try to

find a solution to the crisis in Lebanon and has worked to deepen engagement

with other countries in the region. Nevertheless, his personal

engagement appears to have yielded limited results. Although views of France

are moderately positive across the countries surveyed in Arab Barometer’s sixth wave – in five of seven at least 40

percent have a favorable view of France overall – views of Macron himself lag

significantly. In no country surveyed do 40 percent of citizens have a

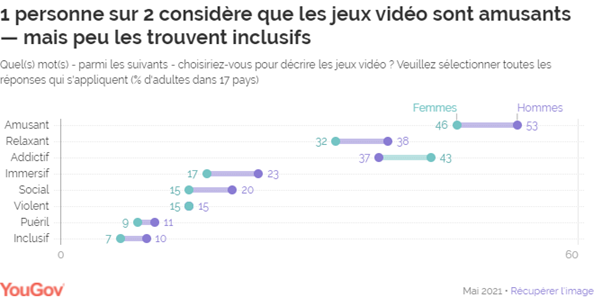

positive view of his policies. (Arabbarometer) June 24, 2021 Source: https://www.arabbarometer.org/2021/06/mena-pulse-on-france-macron/ In 17 Countries Only 8% Of Respondents

(Gamers And Non-Gamers) Would Describe Video Games As Inclusive A global study conducted in 17 countries

shows that only 8% of respondents (gamers and non-gamers) would describe

video games as “inclusive”. We observe that the French (22%) and the Danes (14%) are

the most likely to share this opinion. At the same time, nearly half (49%) of

global consumers rate video games as fun -

a figure that is on the rise by men (53%). While 35% find video games to

be relaxing , 40%

think they are addictive (43%

of women vs. 37% of men). (YouGov France) June 24, 2021 Source: https://fr.yougov.com/news/2021/06/24/comment-les-jeux-video-sont-ils-percus-en-2021/ In Many Markets Such As Spain, Mexico And

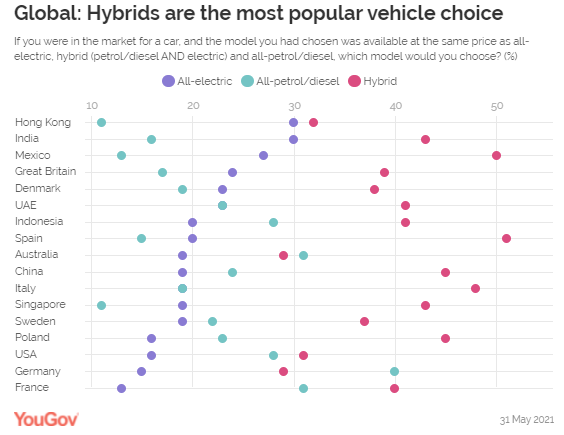

China, The Ratio Of People Who Prefer Hybrids To Electrics Is Around 2:1 Hong Kong is the only market where electric

cars come close to matching hybrids in terms of overall preference: three in

ten (30%) say they would opt for an electric car, all things being equal,

while nearly a third (32%) say they would go for a hybrid. In many markets such

as Spain (51% vs. 20%), Mexico (50% vs. 27%) and China (45% vs. 19%), the

ratio of people who prefer hybrids to electrics is around 2:1. (YouGov UK) June 24,

2021 Global Country Average Of 74% Say There Is

At Least A Fair Amount Of Tension Between Rich And Poor The poll,

which was conducted online between 23 December 2020 and 8 January 2021, shows

people in South Africa (58%), India (57%) and the US (57%) are most likely to

feel that their country is divided by “culture wars”, with a significant gap

in opinion between them and people in Brazil (47%), who are next most likely

to think their nation is divided in this way. Those in Germany (19%),

Russia (18%) and Japan (9%) are least likely to feel divided. In most

countries, relatively few actively disagree with the statement (Global

Country Average of 14%). (YouGov

Egypt) 25 June 2021 Source: https://www.ipsos.com/en-eg/culture-war-around-the-world ASIA

695-696-43-01/Poll Among White-Collar Employees, The Remote Working

Practice, Which Was 13% Before The Epidemic, Has Now Reached 59% In Turkey

The Biggest Change During the Pandemic

Period: The Increase in the Transition to «Remote Working» Application According to the data we gathered from

white-collar employees, the remote working practice, which was 13% before the

epidemic, has now reached 59%. In multinational companies or operating

in different fields, we see that remote working has increased from 21% to

94%.

Decisions were made on which teams would

come to the office, which teams would work remotely, applications for those

with chronic diseases, performance system adaptations, working hours and how

internal communication activities would be carried out.

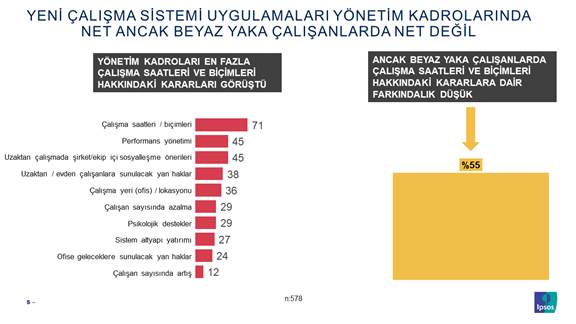

Management staff in companies mostly

discussed and made decisions on issues related to «working hours and forms»; however,

awareness of these issues is low among white-collar employees.

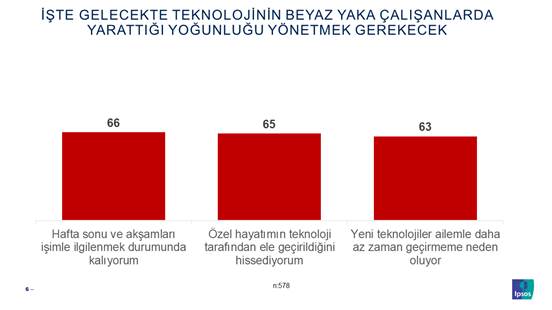

Two out of every three white-collar workers

“have to go about their job on weekends and evenings”, “feel that their

private life is being taken over by technology” and “have to spend less time

with their family”.

Physical environments will be preferred to

provide team spirit and socialize White-collar employees welcome socialization

activities that can be done in the physical environment, such as

"planning department communication dinners every quarter, participating

in in-company trainings as a team, and getting teams together outdoors at

least once a year".

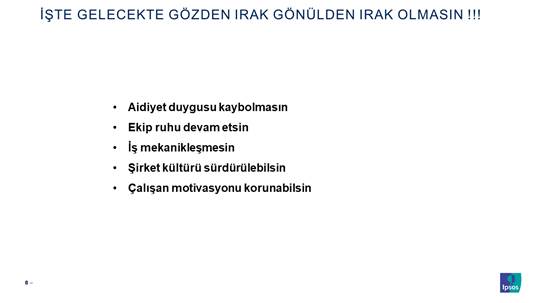

Here's Iraq in the Future Here, basic problems such as “work

mechanisation” and “no sense of belonging” are feared in the

future. Although different solutions are discussed, there is no

established practice. Therefore, the most fundamental problem that

awaits companies in the future will be to develop and sustain practices for

the sense of belonging. Ece Ertürk, Country Leader of Ipsos UU

& Public Affairs, commented on the subject: The effects of the pandemic on business

life as well as its effects on our social life continue to change and

transform according to new developments and expectations. As of the

pandemic, one of the biggest changes we have seen in business life has been

the transition to remote working with

a rate of 59% . This was followed by hybrid study models with a rate

of 49% . With the effect of these changes, working hours and styles , performance management and

productivity were the two topics that the management staff talked and

discussed the most. It is obvious that clarifying the decisions

and practices that are relatively clear for the management staff in this

period and minimizing uncertainties for the employees will have a positive

impact on the employee satisfaction and belonging issues that have been

damaged in the pandemic and are being tried to be redefined. In this

world, where the mechanized business cycle, decreasing corporate unity &

socialization during the pandemic period have reduced the commitment of

employees to their companies, companies and managers should not

allow what is out of sight to remain out of heart . (Ipsos Turkey) 21 June 2021 Source: https://www.ipsos.com/tr-tr/pandemi-uzaktan-calisma-uygulamasina-gecisi-artirdi 695-696-43-02/Poll 16%

Pakistanis Claim To Have Bought Something Online During The Past 6 Months

According to a survey conducted by Gallup

& Gilani Pakistan, 16% Pakistanis claimed to have shopped online during

the past 6 months. A nationally representative sample of adult

men and women from across the four provinces was asked the following

question, “Have you done any online

shopping during the past six months i.e. did you buy any thing/product

online?” In response to this question, 16% said ‘Yes’, 82%

said ‘No’ while 2% did not know/did not respond. (Gallup Pakistan) June 23, 2021 Source: https://gallup.com.pk/post/31906 AFRICA

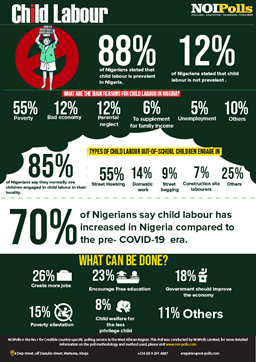

695-696-43-03/Poll 88 Percent

Of Nigerians Believe That Child Labor Is Prevalent In Nigeria While 12

Percent Mentioned That It Is Not Prevalent

June 12th every year is a

day set aside by the United Nations and International Labour Organisation as

the Child Labour Day which is a day set aside to identify with children who

are caught in the web of the excruciating ventures of all forms of child

labour around the globe. The day also seek to showcase the progress made so

far in the fight against the menace of child labour and buttress the need to

bring it to a grinding halt. It is an opportunity to call on all stakeholders

on the fight against child labour to intensify effort towards eradicating the

menace that has robbed a lot of children of a glorious and productive future.

Additionally, the Child Labour Day seek to encourage actions towards

achieving the SDG 8.7 of the United Nations Millennium Development Goals.[1] The SDG 8.7 states thus “take

immediate and effective measures to eradicate forced labour, end modern

slavery and human trafficking and secure the prohibition and elimination of

the worst forms of child labour, including recruitment and use of child

soldiers, and by 2025 end child labour in all its forms”[2]. To commemorate the Child Labour Day,

NOIPolls conducted a survey to gauge the opinion of Nigerians on child labour

and the result revealed that 88 percent of Nigerians believe that child

labour is prevalent in Nigeria while 12 percent mentioned that it is not prevalent.

This further corroborates the findings of the International Labour

Organisation (ILO) which states that there are 152 million children in the

whole world engaged in child labour while there are 15 million children

undergoing different forms of child labour in Nigeria which is the highest in

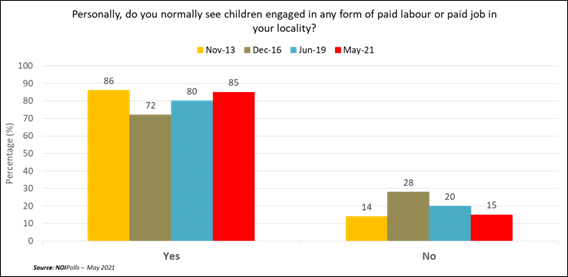

West Africa[3]. The poll results which further revealed

that 85 percent of respondents stated that they see children engaged in child

labour within the North-East, South-East and South-South all tied at 92

percent, having the highest proportion of respondents who stated that they

see children engaged in child labour in their locality. The Child Rights Act

which was passed into law in 2003 stated that a child is one who is below the

age of eighteen years, and it provides that the interest of such shall be

paramount in all consideration. It is disappointing to note that eighteen

years after incorporating the Child Rights Act, millions of children have

continued to be involved in child labour in the country. This can be

buttressed with findings from the poll which revealed that children are often

seen engaged in different forms of labour which include; Street hawking (55

percent), Domestic work (14 percent), Street begging (9 percent) and

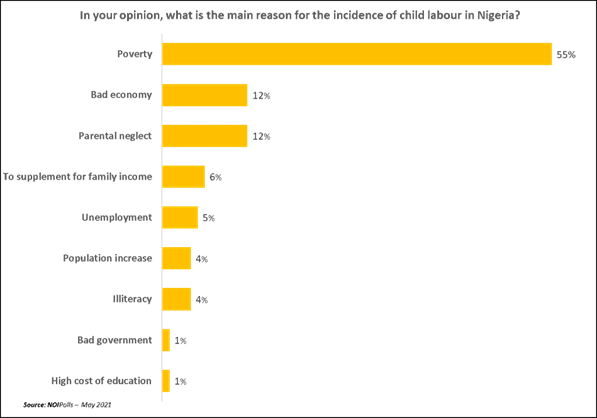

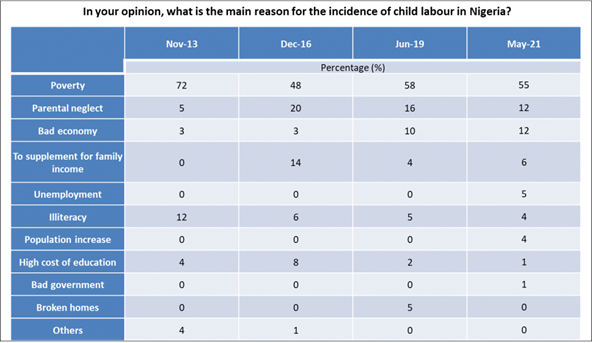

Construction site (7 percent). More findings revealed that poverty (55

percent) is the main cause of child labour in Nigeria. This is followed by

bad economy and Parental neglect (12 percent each), to supplement for the

family income (6 percent), unemployment (5 percent), population increase and

illiteracy (4 percent) amongst others. Subsequently, respondents were asked what should

be done to end child labour in the country and the poll result revealed that

26 percent of the respondents are of the opinion that creating jobs is the

solution to the problem of child labour. Other recommendations include;

encourage free education (23 percent), improve economy (18 percent), poverty

alleviation (15 percent) and child welfare (8 percent) amongst other

solutions proffered. Lastly, 70 percent of the respondent disclosed that the

incidence of child labour in the country has increase when compared to the

pre COVID-19 era. These are some of the key findings from the child labour

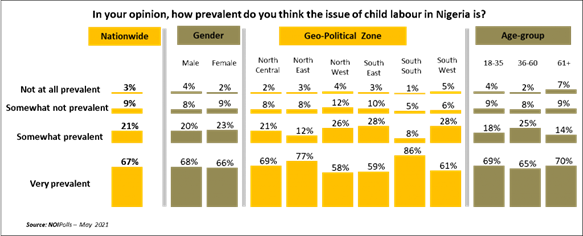

survey conducted in the week of 24th May 2021. Survey Findings The first question sought to know how

prevalent the issue of child labour is in the country and the survey

revealed that 88 percent of respondents stated that child labour is

prevalent in Nigeria, while 12 percent stated that child labour is not

prevalent in the country. Analysis across geo-political zones shows that

the South-South region (94 percent) has the highest proportion of

respondents who stated that child labour is prevalent, and this is followed

by respondents form the North-Central (90 percent). With regards to age

category, those aged 36-60 (90 percent) have the highest proportion of respondents

who stated that child labour is prevalent in Nigeria.

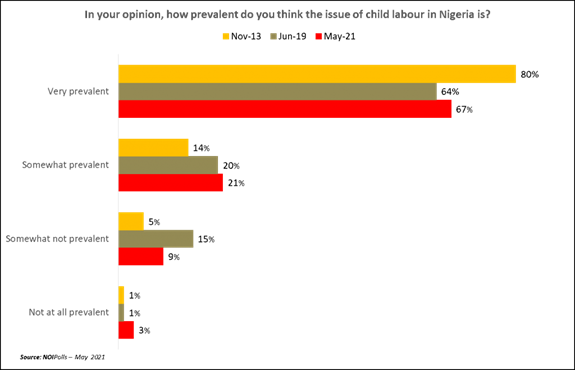

Trend analysis shows a 10 percent drop from

2013 to 2019 and 4 percent increase from 2019 to 2021 in terms of prevalence

of child labour in Nigeria.

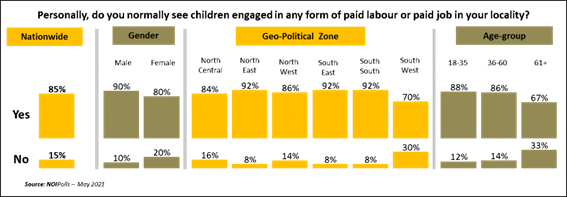

Respondents were asked if they see children

in their locality engaged in child labour and the result revealed that

85 percent of the respondents acknowledged that they see children engaged in

child labour in their locality with the North-East, South-East and

South-South all having 92 percent of respondents who mentioned this. Also,

those aged 18-35 (88 percent) have the highest proportion of respondents who

stated that they see child children engaged in child labour.

Trend analysis shows a 5-point increase in

the incidence of child labour from 2019 to 2021 of the respondents who stated

that they see children engaged in child labour in the country.

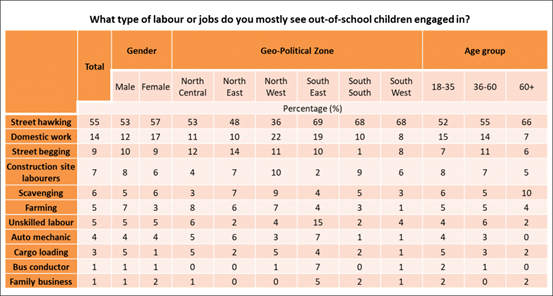

Respondents who stated that they see

children engaged in child labour in their locality were asked the types of

labour they see children engaged in and the poll result revealed that street

hawking (55 percent) have the highest proportion of respondents who

stated that they see children participating in child labour with the

South-East (69 percent) having the highest proportion of respondents and then

followed by South-South and South-west all tied at 68 percent. Others

include domestic work (14 percent), street begging (9

percent), construction site (7 percent), scavenging (6 percent) and

farming (6 percent) amongst others.

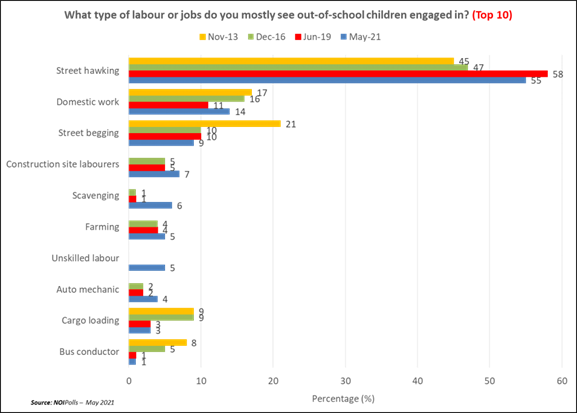

Trend analysis shows that street hawking

increased by 2 percent from 2013 to 2016 and had an 11 percent increase in

2019 though decrease by 3 percent in 2021.

The poll findings also revealed that

55 percent of respondents stated that poverty is the cause of child labour

while 12 percent ascribed it to bad economy. Others include parental neglect

(12 percent), to supplement family income (6 percent), unemployment (5

percent), population increase and illiteracy (4 percent) amongst others.

Trend analysis show that poverty as a

reason for child labour experienced a 24-point decrease from 2013 to 2016 and

then 10-points increase from 2016 to 2019 and then 3-point increase from 2019

to 2021.

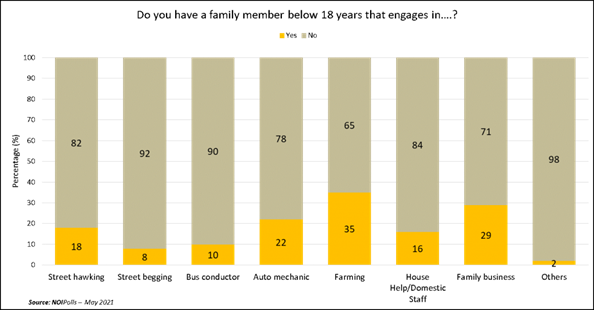

Furthermore, respondents were asked if

they have family members below age 18 who engage in labour/work and the poll

revealed that 35 percent disclosed that they have family members who engage

in farming, 29 percent mention family business, 22 percent stated auto

mechanic, 18 percent mention street hawking, 16 percent said domestic help and

10 percent mentioned bus conductor amongst other activities.

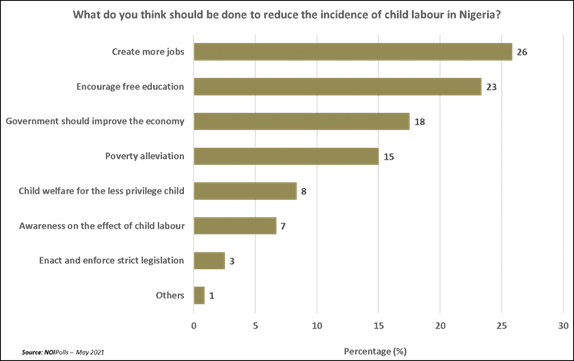

Respondents were asked about the solution

to child labour and the poll result revealed that 26 percent of the

respondents stated that more jobs should be created while 23 percent stated

that free education should be encouraged. Others include improve economy

(18 percent), poverty alleviation (15 percent), child welfare (8 percent),

awareness on effect of child labour (7 percent) amongst others.

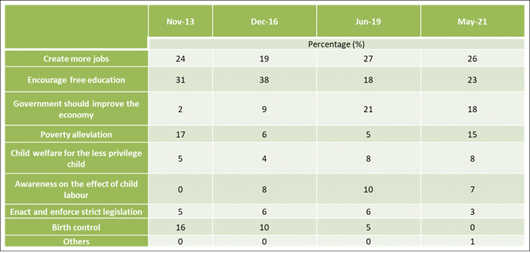

Trend analysis reveals a 1 percent decrease

in job creation when current result is compared the result obtained in 2021.

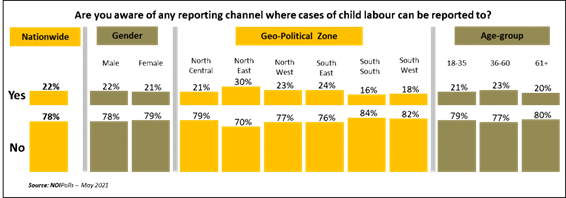

With regards to reporting incidence of

child labour, the poll revealed that majority of the respondents (78 percent)

claimed that they do not know where to report incidence of child labour in

Nigeria. However, 22 percent disclosed that they are aware of reporting

channels with the North-East (30 percent) having the highest proportion of

respondents in this category.

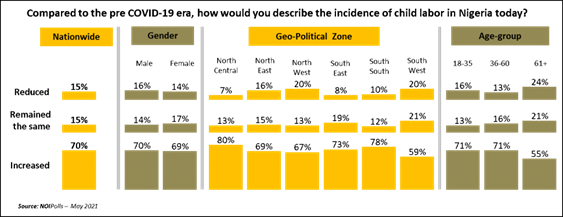

Respondents were asked to compare child

labour incidence before COVID-19 era and now and findings revealed

that 70 percent of respondents stated that it has increased when

compared to pre COVID-19 era. On the other hand, 15 percent stated that it

has remained the same while another 15 percent stated that it has decreased. Analysis

across geo-political zones shows that North-Central region (80 percent) have

the highest proportion of respondents who stated that child labour has

increased compared to pre COVID-19 era and this is followed by South-South

(78 percent).

Conclusion In conclusion, it is disheartening to note

that there is still prevalence of child labour in the country as indicated by

88 percent of respondents in the survey. This is calling on all stakeholders

to expedite action in the elimination of child labour in the country so that

the children involved can be accorded at least basic education to lead

productive lives thereby making the society a better place for all. According

to 55 percent of the respondents, the survey also revealed that the activity

most children engage in is street hawking. Others include domestic work (14

percent), street-begging (9 percent), construction site (7 percent) amongst

others, these are ventures that expose children to all forms of child labour

and dangers that could threaten their lives and hence should be discouraged

by all and sundry. The implementation of the child right act will go a long

way in curbing this act of child labour, but unfortunately it has not been

implemented by the various states concerned, therefore exacerbating the

incidences of child labour. The survey also revealed the causes of

child labour which include poverty (55 percent), bad economy and parental

neglect (12 percent), to supplement family income (6 percent) among other

causes. Nigerians proffered solution to the menace of child labour which

include creating jobs (26 percent), encourage free education (23 percent),

improve economy (18 percent) and poverty alleviation (15 percent) among other

solutions. This is calling on all to implement the recommendation proffered

by Nigerians which will ultimately eradicate the child labour conundrum and

ultimately make our society a better place for our children who are the

fulcrum and the necessary ingredient for a better society. (NOI Polls) June 16, 2021 695-696-43-04/Poll 3 In Ten

(27%) Adult South Africans And Four In Ten (37%) Young People In The Country

Are Looking For Work; Youth Day 2021

Figures from Statistics South Africa confirmed that the Youth unemployment

rate in South Africa increased to 63.3% in the first quarter of 2021 from

63.2% in the fourth quarter of 2020. In the midst of the Covid-19 pandemic,

Ipsos undertook a project called Mzansi Roars, that focused on the lives and

livelihoods of South Africans, their incomes and spending patterns, what they

eat and what they value, nutrition and health, their satisfaction with life,

the financial situation of households, traditions and culture, their

life-worlds, dreams and aspirations. For Youth Day 2021 we will take a look

at how some of these aspects, probed in the Mzansi Roars project, continue to

influence the lives of young people. Unemployment, variable earnings and very

little money to go around By no means do we want to underplay the

dire need for job creation in our country, as roughly 3 in ten (27%) adult

South Africans and four in ten (37%) young people in the country are looking for

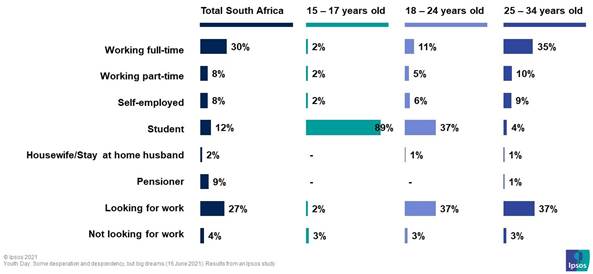

work. The frightening high figure of youth unemployment needs some unpacking. A large proportion of young South Africans

are studying to improve their chances of finding a job in the future, as is

evident from the 89% of 15-17 year olds, and 37% of 18-24 year olds who are

students. However, entrepreneurial spirit is alive and well among the young

people of South Africa, with a smaller number of youths creating a source of

income for themselves.

The contributions made to the income of the

younger age groups by means of Government Grants should not be

underestimated, with more than a third (35%) of 15-17 year olds receiving a

Government Grant. This support does get progressively less with age, with 29%

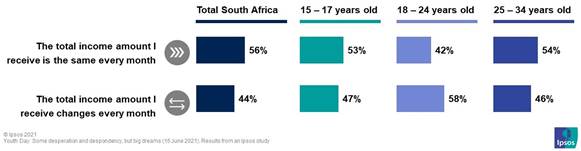

of 18-24 year olds and 27% of 25-34 year olds receiving Government Grants. The receipt of a regular income from a

Government Grant does however not guarantee a steady income. It is remarkable

that 44% of adult South Africans indicated that the amount of money they

receive on a monthly basis (from all sources) keeps on changing. This is an even bigger issue for younger

people, that complicates their planning for expenses and making accurate

budgeting near impossible.

With almost six in ten (59%) 15-17 year

olds and almost half (48%) of 18-24 year olds saying that they “never” have

any money left at the end of a month after personal and household expenses

are paid, it is another sign that numerous and varied demands are made on

their monthly income. In these circumstances where every rand is

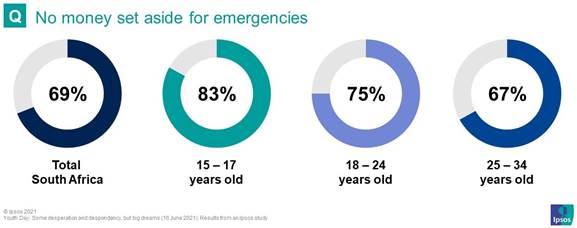

turned over quite a few times before spending, it should not be surprising

that South Africans of all ages do not have money set aside for emergencies.

From the figure below it is clear that younger adults are definitely less

prepared for unforeseen situations than older people – although a dearth of

planning and provision for emergencies seem to be quite common.

Are young people more deprived? A good question is whether this might be an

indication that younger adults are more deprived than older South Africans. A

variety of circumstances can be investigated to prove or disprove this

notion. Access to clean water is regarded as a basic human right: Is it more

difficult or laborious for younger people to access water than for older

people? Although these figures are probably saying

a great deal more about the inefficiency and lack of delivery of basic

services from local governments in all areas of the country, it is clear that

a smaller proportion of young people than older people have access to running

water inside their houses – and thus they have to make more of an effort to

access clean water for daily use. This undoubtedly has an influence on the

time available for other activities, like work and studying. The entrepreneurial spirit, living

standards and hope for the future In an international Global Advisor study published by Ipsos in early

2021, it was found that South

Africans are some of the most entrepreneurial in the world1. Focusing specifically on young people, more

than a third aged 34 and below agrees that “One

needs to have your own business in order to have a secure lifestyle2”

, showing that entrepreneurial spirit in the country is alive and well – and

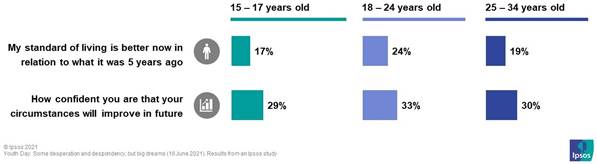

possibly fueled by a lack of other opportunities. Although moderate proportions of young

people agree that their standard of living is better now in relation to what

it was 5 years ago, they are definitely more confident that their

circumstances will improve in the future.

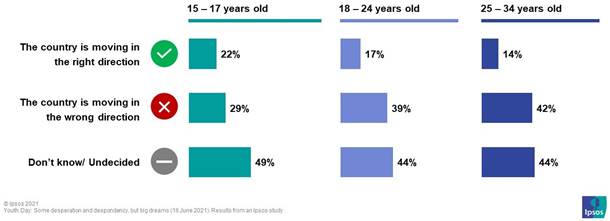

Politics are not high on the agenda3 However, this hope for the future is not

related to the political circumstances in the country. In fact, young people

(like older people) are rather unsure and apprehensive about the direction in

which the country is moving:

In addition, young people are not really

interested in politics and elections4, and about a third do not

want to vote in the upcoming Local Government Elections, and the same proportions do not feel

attached to any current political party in the country. This is about the

same proportion as older people in the country who feel this way. These opinions might be closely related to

the low levels of trust in politicians and political parties expressed by

young people (with the possible exception of the president). These figures

really bring the realisation home that political parties have their work cut

out before the Local Government Elections in October 2021, to convince young

people to go to the polls and participate in elections that can influence

their living conditions and local circumstances for the next five years. (Ipsos South Africa) 16 June 2021 Source: https://www.ipsos.com/en-za/youth-day-2021-some-desperation-and-despondency-big-dreams 695-696-43-05/Poll Awareness

Levels Of The New RTR Guidelines Amongst Consumers Is Quite Low 17% In South

Africa

A new online study by Ipsos, conducted

among car owners between 6 April to 10 May 2021, shows that respondents who

are aware of the new RTR Guidelines, share a positive outlook on the

implementation of these guidelines. This feeling was shared by respondents

who were not aware of the RTR Guidelines, but were informed during the

interviewing process. Competition Commission The Competition Commission has put out the final set of

guidelines for “Right to Repair” that has the potential to completely shake

up the automotive industry in terms of warranties and maintenance plans –

coming into effect on the 1st of July 2021. This ruling enables motorists to choose

independent service centres, without their dealership warranties being

affected. Not only will consumers be able to maintain a vehicle at

independent service centres without voiding their warranties, the way new

vehicles are quoted on and sold for will also change. Dealerships will be

required to split out the Warranty and Maintenance plan costs on the quote,

thereby giving the customer the option to include or exclude these, as part

of their vehicle purchase. This is a win for consumers, but it will

completely change the way the automotive industry operates and will elevate

the competitive landscape across the industry, more so in the small to medium

business sector. The nuts and bolts of the project The study used a multi-modal approach,

making use of qualitative and quantitative methodologies to gain a deep

understanding of consumers’ sentiments and the potential behaviour changes

due to RTR. Through the research, Ipsos was able to uncover the following

behaviours and consumer viewpoints on RTR:

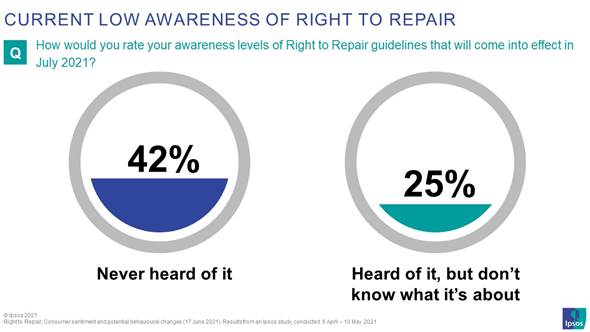

Current low awareness The current awareness levels of the new RTR

guidelines amongst consumers are low - with only 17% of respondents saying

they have heard of it and have a good grasp or thorough knowledge of what the

new guidelines entail.

Positive reaction from consumers at first

glance The emotional impact was viewed in an

extremely positive light amongst respondents after they were made aware of

the RTR guidelines. There exists a genuine level of discomfort

from respondents that their warranties will be voided, should they choose to

service or repair their vehicles at any place other than the franchised

dealer. However, with the RTR guidelines, it is easing some of the discomfort

they are experiencing and providing them with peace of mind. The sentiment

from respondents was that the RTR guidelines will make them feel more

empowered and in control of their finances. Despite the RTR guidelines, respondents

indicated that they are still not comfortable with how disputes between

Original Equipment Manufacturers (OEM’s) and Independent Service Providers

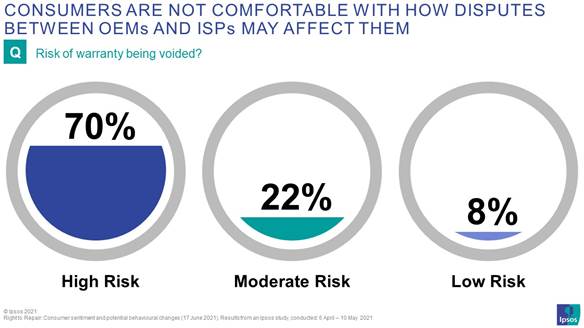

(ISP’s) will affect them. 70% of respondents indicated that, due to this fact

they still believe there is a high potential risk of their warranties being voided.

Effect on Franchised Dealerships The perception is that consumers and the

ISP’s have more to gain through the RTR guidelines, with the OEM’s having

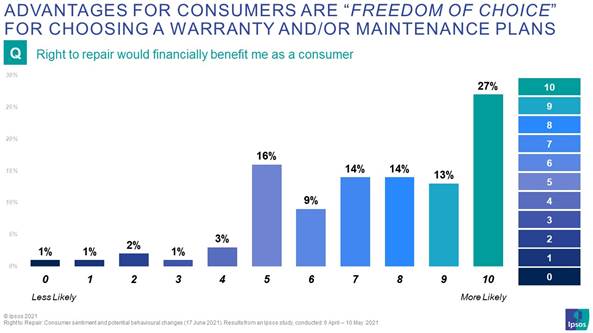

much more to lose. The main advantages for consumers relate to

“freedom of choice” when choosing which warranty and/or maintenance plan to

purchase. This allows them to “shop around” and decide on where to service or

repair their vehicles. Further to this, 50% of consumers feel that RTR will

financially benefit them. Taking a closer look at the advantages for

the Industry, respondents stated that these guidelines will create some

healthy competition in the market and empower smaller businesses to grow,

leading to job creation.

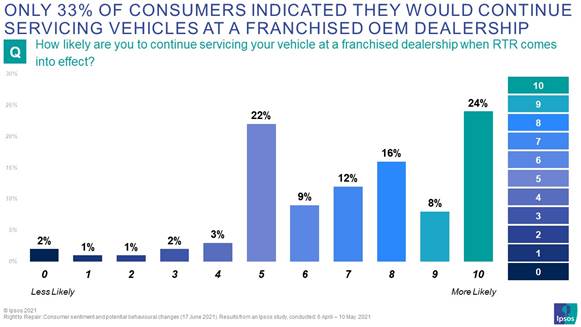

With consumers’ lack of knowledge and

understanding of the guidelines as it stands now, only 33% indicated that

they would continue servicing their vehicles at a franchised dealer, but that

they are eagerly waiting to have the freedom of choice to choose where to

send their vehicle, and possibly reaping the financial benefits.

(Ipsos South Africa) 17 June 2021 Source: https://www.ipsos.com/en-za/right-repair-consumer-sentiment-and-potential-behavioural-changes 695-696-43-06/Poll More Than

Half 63% Of The Owners Of Small, Medium And Micro Enterprises (SMME’s) Saying

They Experienced Great Uncertainty Regarding The Sustainability Of Their

Businesses

In October 2020, Ipsos shared insights into

the SMME

sector and how these businesses were impacted because of the Covid-19

pandemic,

with more than half of the owners of Small, Medium and Micro Enterprises

(SMME’s) saying they experienced great uncertainty regarding the

sustainability of their businesses. We continue the story by unpacking what

advice and support the SMME business owners state they need to recover in

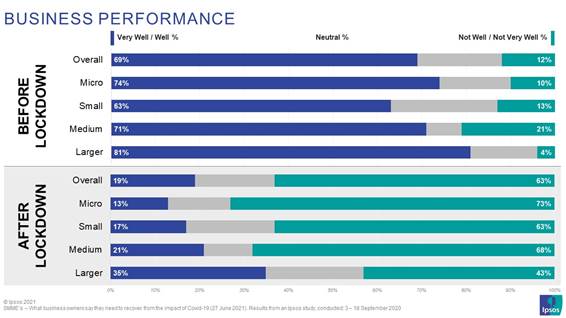

these pressing times. A quick recap on the business impact: The impact of the pandemic and subsequent

lockdown on business performance have been significant, with 63% of SMME’s

stating that they are performing “Not Well” or “Not Very Well” after

lockdown, while larger enterprises are seemingly more resilient, with a third

(35%) stating that they are still performing “Well” or “Very Well” after

lockdown.

More than half (54%) of business owners

used their personal savings to keep their businesses running and 36% had to

revise their company spending to reduce expenses. Staff and suppliers were

also impacted, and about a quarter (26%) of businesses had to let staff go,

stating that they could not pay their suppliers or accounts. Nevertheless, South

African business owners stayed true to their entrepreneurial spirit, adapting to survive by implementing key

changes within their business model. What behaviour changes do business owners

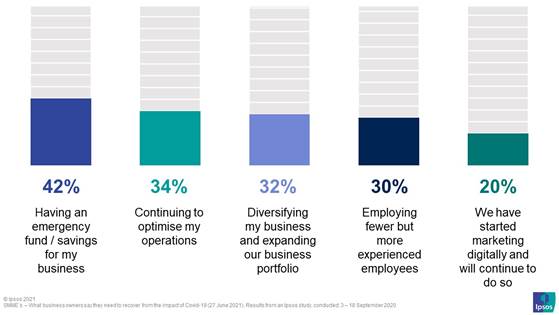

say they will continue with? We asked business owners what the main

lessons were that they learnt during the pandemic and that they will continue

to do in the future, with the top 5 mentioned lessons being:

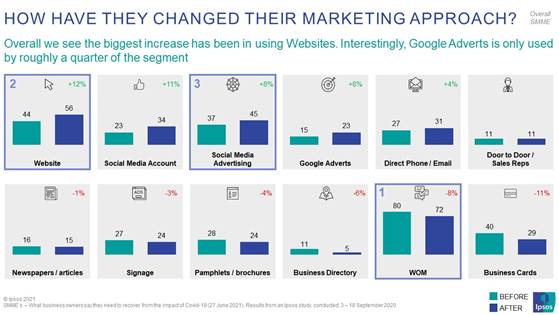

Taking a closer look at the marketing

changes that these business owners had to implement, we see that the SMME

sector still heavily relies on Word of Mouth as their main marketing source,

however a prominent shift towards digital marketing can be seen. This shift leans towards channels such as

their own websites (+12%) and other digital advertising channels such us

social media and Google Adverts (+8%). The largest decline of marketing

material used have been in the use of business cards, down by 11%.

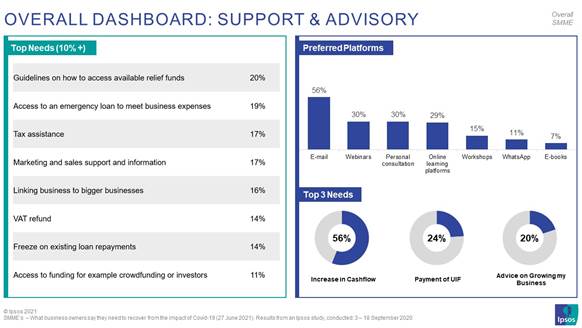

What advice and support do SMME Business

Owners need With various external forces playing a role

in the impact on their businesses such as customers spending less (55%) and

price increases from suppliers (44%), the majority are still looking to

financial institutions for advice, with the top advisory need raised by

business owners being advice / support on how to increase their cashflow

(56%), followed by payment of UIF (24%) and a fifth requesting advice on how

to growth their businesses. However, advice / support on increasing

cashflow and growing businesses are broad topics that can include many

different elements, the top needs (10%+) provide more direction in terms of

which topics need more support and include topics such as Tax Assistance

(17%), Marketing and sales support and information (17%) and linking business

to bigger business (16%). With varying levels of digital marketing

experience and limited marketing budgets, it is no surprise that marketing

advice and support was called out as one of the top 10 advisory requirements

from SMME business owners.

Looking at how they prefer to receive

advice, it is interesting to see that 56% of business owners still prefer

email as the main communication method, followed closely by webinars (30%),

personal consultations (30%) and online platforms (29%).

(Ipsos South Africa) 27 June 2021 Source: https://www.ipsos.com/en-za/smmes-what-business-owners-say-they-need-recover-impact-covid-19 695-696-43-07/Poll 81%

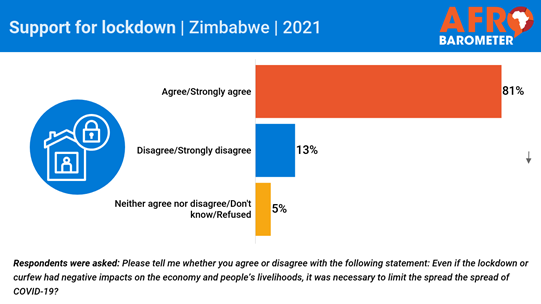

Zimbabweans Strongly Agree With The Fact That Even If The Lockdown Had

Negative Impacts But It Was Necessary

A new Afrobarometer survey shows that even

though almost half of Zimbabwean households lost a primary source of income

during the COVID-19 pandemic, most citizens approve of the government’s

overall management of the pandemic. Most Zimbabweans endorse lockdowns and

school closures as painful but necessary. But very few report receiving

pandemic-related assistance from the government, and a majority believe that

COVID-19 resources were lost to government corruption. A majority doubt the government’s ability

to ensure that COVID-19 vaccines are safe, and fewer than half say they are

likely to try to get vaccinated. (Afrobarometer) 17 Jun 2021 WEST

EUROPE

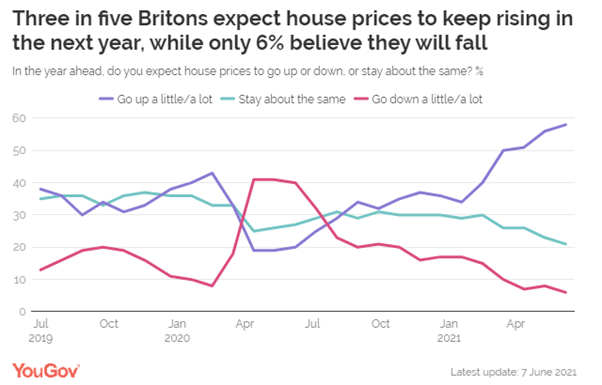

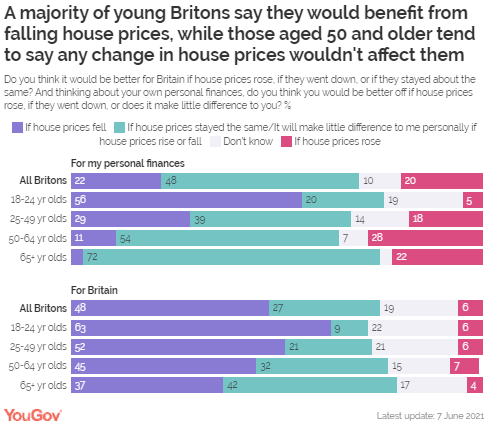

695-696-43-08/Poll Only 6% Of Brits Think Increasing House Prices Would Be Beneficial

For The Country, But One-Fifth (20%) Say It Would Be Advantageous For Their

Personal Finances

Most recent figures show that the housing market is growing

at its fastest rate in seven years – a jump of 9.5% in the year to

May. Experts suggest

that ‘market activity continues to be boosted by the government’s

stamp duty holiday’ and that this boom period may continue as the ‘unexpected

savers’ of the pandemic look to invest their extra money. Now, new YouGov tracking data shows that 58% of Brits expect prices

of homes to go up in the year ahead while 21% expect them to stay about the

same, and only 6% anticipate a dip. When asked in February last year, prior to the beginning of the

pandemic, 43% expected house prices to go up, compared to only 8% who thought

they would drop. Fast-forward to April 2020 - just after the UK entered its

first lockdown – and the number of those that thought house prices would

increase tumbled to just 19%, while those who anticipated a fall, increased

to 41%. Opinion remained static for a couple of months, before beginning to

rise from June to August, at which point it levelled off once again at around

35%. The success of the vaccination programme caused confidence to rebound,

with the number expecting house prices to go up shooting up from 35% in

mid-January 2021 to 50% in mid-March. Expectations that house prices will

rise have grown further since that point, reaching 58% in early June. Half of Brits think it would be better for

the country if house prices dropped In general, 48% of the public say it would be better for Britain if

house prices went down, while a much smaller proportion (6%) think it would be

better if prices increased. Around a quarter (27%) believe it would be best

if it remained at the current level. When asked the same question, but this time thinking about personal

finances, One-fifth of Brits (20%) say they would be better off if prices

rose. A similar proportion (22%) say it would be beneficial if prices fell.

Half (48%) of Brits say it will make little difference to them

personally if house prices rise or fall. This is most apparent among those

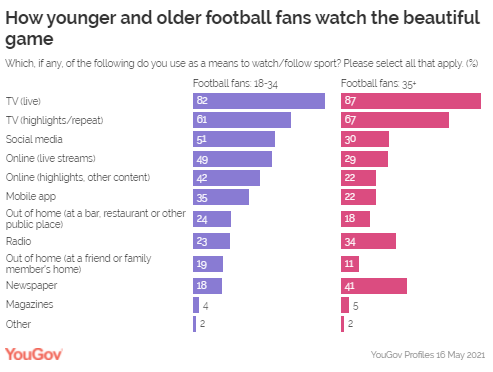

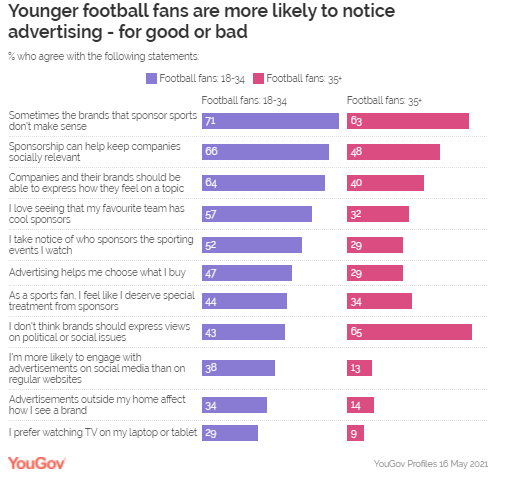

aged 65+ (72%) compared to only 20% of those aged 18 to 24 (YouGov UK) June 14, 2021 695-696-43-09/Poll Three In Ten (31% Of 18-34’s) Football Fans Say Live TV Is A Thing Of

The Past (Compared To 20% Of Over 35s)

In April, as he

offered a defence of the European Super League, Real

Madrid President Florentino Pérez declared that “young people are

no longer interested in football”. Yet those arguments

haven’t seemed to worry UK broadcasters, who this month signed up to

roll-over their existing contracts with the Premier League in

a £4.7bn deal. So what does YouGov’s data tell us about young people

and the beautiful game – and how can marketers and advertisers more

effectively reach them? How they watch football Comparing football fans aged 18-34 and over-35s reveals

key differences in viewing preferences. While TV is still the most

popular way to watch the game, older fans are more likely

to turn on the telly to watch live football

(87% vs. 82% of 18-34s) and highlights (67% vs. 61% of 18-34s).

Younger fans are more sceptical of the box. While

four in five watch sport on live TV (82%), some may be doing so reluctantly.

Three in ten (31%) say live TV is a thing of the past (compared to 20% of

over 35s), and nearly as many say streaming is better than live

TV (28%) compared to one in seven (14%) older football

fans. Where they watch football Looking at the four major broadcasters involved in the renewed

football rights deal shows that older fans are more likely

to have recently watched Sky Sports (39% vs. 30% of 18-34s),

BBC Sport (24% vs. 17%), and BT Sport (24% vs. 21%). There’s more parity when

it comes to Amazon Prime Video (30% vs. 31% of 18-34s)

but we shouldn’t assume too much from this, given

that the service comes free with the overall Amazon

Prime package. The gap can be partially explained through simple household

economics. Two in five (39%) of the younger demographic live with

their parents and therefore may not have control over their household

TV situation – including which channels their household subscribes

to. But it’s likely no accident that Now TV, which doesn’t tie viewers to

a longer-term contract, is more popular among 18-34s than over-35s (11% vs.

8%). Four in five younger football fans say streaming services

have “changed TV watching” for them (82% vs. 53% of over-35s),

and the more long-term contracts offered by more

traditional broadcasters could be putting them off. Offering more

short-term viewing options to younger fans may help broadcasters reap greater

commercial rewards among this group. Younger fans notice marketing but

expect more from it Our data suggests that younger football

fans are more attentive to marketing – but also expect more from

it. For instance, fans aged 18-34 are more likely to say they notice

the brands that sponsor events (52% vs. 29% of over 35s). They’re also

more likely to think sponsorship can help companies stay socially

relevant (66% vs. 48% of over-35s), and nearly three in five agree that they

love seeing that their favourite team has cool sponsors (57% vs 32%

of over 35s). How and where to advertise to younger

fans However, with attention comes scrutiny. Fans aged 18-34 are more

likely to say that the brands that sponsor sports don’t make sense (71% vs.

63% of over-35s), and that they deserve special discounts from those

brands (44% vs. 34%).They may also have a poorer attention span: 18-34s are

much more likely to say they’re bored all the time (40% vs. 25%). So clubs, broadcasters, and marketers should take care

when addressing this audience: they watch the game

differently, and they respond to promotions and communications

differently too. For example, while they’re less likely to say that TV ads have

the biggest chance of getting their attention (20% vs. 34% of

over-35s), online ads are more likely to catch their eye (31%

vs. 19%). A quarter are also on TikTok (23%), so a short-form

social strategy could also pay off. But content is key. Younger fans want different messages and

messengers A big, bold message may be risky with over-35s (65% of

them vs. 43% of 18-34s think brands shouldn’t express views on

political or social issues), but most 18-34s think brands should be free to

speak out when they feel strongly about an issue (64% of 18-34s vs.

40% of over-35s). Marketers may also wish to consider how they select brand

ambassadors aimed at younger fans. Fans aged 18-34 are more likely

to cite wonderkids in continental

leagues like Kylian Mbappe (16% vs. 9% of over-35s)

and Erling Haaland (15% vs. 6% of over-35s)

as favourites, while over-35s prefer Premier League stalwarts like Harry

Kane (23% vs. 18% of 18-34s) and Mo Salah (20% vs. 16%). While a campaign that appeals to naked self-interest – i.e. a

shirt sponsor promising exclusive discounts to fans of a particular team –

may pay off, an ad fronted by Jadon Sancho that sensitively tackles themes of

social responsibility could be just as effective. 2021 is half over, and the Premier League has already seen off the

threat of a breakaway competition and the prospect of an open-market auction

over broadcast rights. But while the current TV deals are

preserved in amber until 2025, there’s evidence that fans may

be changing. Will clubs, marketers, and broadcasters change

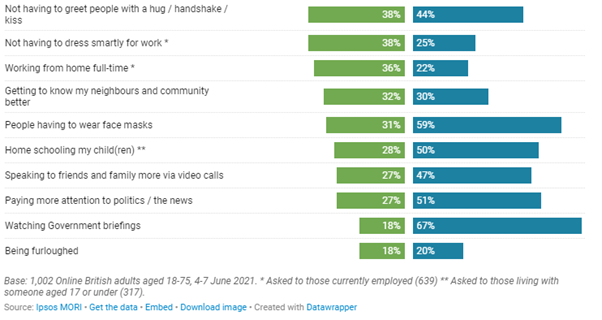

with them? (YouGov UK) June 17, 2021 695-696-43-10/Poll Britons Will Miss Practicing Better Hygiene (66%), Less Traffic On

Roads At Peak Times (63%) And Quiet Shops And Supermarkets (59%)

New polling by Ipsos MORI shows that while many will be ready to see

the end of lockdown, there are plenty of aspects of lockdown that will be

missed. Among the things most likely to be looked back on fondly are people

practising better hygiene with two-thirds saying they will miss this at least

a fair amount (66%), less traffic on roads at peak times (63%) and quiet

shops and supermarkets (59%). Over half (53%) will miss spending more time with family, while a

quarter (24%) will be not be unhappy to leave it behind. However, people are

more enthusiastic about seeing family in real life as opposed to video call,

almost half (47% not very much/at all) will not miss speaking to family/

friends more via technology. And despite being fond of the time they’ve spent

with their families, half of parents are keen to see the back of

home-schooling (50%), while three in ten (28%) will miss it. Many will miss the calmness created by lockdown. Half (50%) say they

will miss tourist attractions and public places being quiet, whilst 42% will

miss quieter public transport. Those currently employed will miss aspects of their working life

during lockdown; 44% will miss being able to work more flexibly, while 40%

will miss not having to commute. Almost four in ten (38%) will miss not

having to dress smartly for work and around a third (36%) say they’ll miss

working from home full time. Opinion is split when it comes to socialising again. Four in ten

(39%) will miss not having to socialise with other people, while 45% will not

miss this. Britons are also divided as to whether they will miss getting to

know their neighbours and community better – a third (32%) say they will miss

this whilst another three in ten (30%) will not. Two in three (67%) will not miss government briefings, whilst around

one in five will (18%). Similarly, half (51%) will not miss having to pay

more attention to politics and the news. Three in five (59%) will not

miss having to wear face masks, however opinion is more split concerning

other measures put in place to stop the spread of COVID-19. Forty-four per

cent will be pleased to see the end of not greeting people with hugs, kisses

or handshakes, against another four in ten (38%) who will miss it.

We know that there are many things people

are looking forward to when the coronavirus restrictions end, including

getting proper face time with friends and family. But we’ve also seen that

there will be at least some aspects of lockdown that people will miss – again

partly the opportunity to spend more time with family (if not

home-schooling), but also the peace and quiet, and the reassurance provided

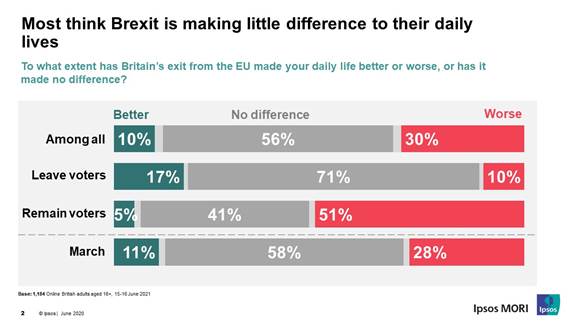

by people paying more attention to hygiene. (Ipsos MORI) 20 June 2021 Source: https://www.ipsos.com/ipsos-mori/en-uk/what-will-britons-miss-about-lockdown-ipsos-mori 695-696-43-11/Poll 4 In 10 (44%) Britons Believe That There Are Still Many Important

Issues To Finalise With The EU

New polling by Ipsos MORI, in partnership with UK in a Changing Europe,

finds that 4 in 10 (44%) Britons believe that there are still many important

issues to finalise with the EU, with Remain voters most likely to feel this

way about negotiations (62%). In contrast, 30% of leave voters say

there are still many important issues to discuss.

Five years after the referendum, the majority of Britons (56%) say it

hasn’t made any difference to their daily lives, however there is still a

significant split between leavers and remainers. Remainers are more

likely to say it has impacted their lives negatively (51%) and only 5% of

remain voters think it has made life better. Whilst only 1 in 10 leave voters

say it has impacted them negatively and 7 in 10 (71%) say it hasn’t changed

anything for them on a day-to-day basis.

When asked about whether they knew anyone whose job of business had

been impacted by Brexit, a quarter (25%) said they did know someone, compared

to 8% who said they knew someone that had been positively impacted. The

majority (59%) didn’t know anyone that had been affected by Brexit. Nearly half (47%) of people report that Brexit is working out as

expected, but unsurprisingly those that voted to remain in the EU are the

least positive – 48% of remainers say is working out worse, compared to 10%

of leave voters. Kelly Beaver, MD of Public Affairs, Ipsos

MORI, says: We are now five years on from Brexit and

the majority of people say it has no impact on their lives to date, however

nearly half of us also feel that we have many unresolved issues to negotiate

with the EU. The public remain divided on Brexit and there is potential

for this to become more pronounced when the pandemic ends and the spotlight

returns to the issue of Brexit. Will remainers be won over by new trade deals

and greater independence? Or will the reality of red tape on holidays

and promises that may not be fulfilled leave the leave voters feeling

disenchanted with Brexit? Paula Surridge, Deputy Director at UK in a

Changing Europe said: The full implications of the decision to

leave the European Union are not yet being felt widely among the British

public. The wider crisis of the last 18 months - tens of thousands of deaths,

an ever-growing health crisis, chaos in the school system, cancelled holidays

and lockdowns – may have both masked some impacts and changed what people

think is possible. But the Conservative majority is built on high

expectations for positive change as a result of Brexit, and it remains to be

seen, once other concerns have waned, whether the government is able to

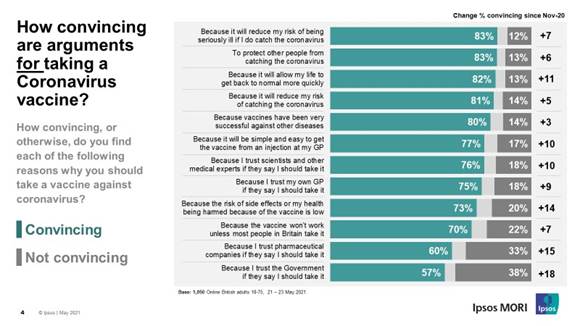

convince them that Brexit has delivered. (Ipsos MORI) 23 June 2021 Source: https://www.ipsos.com/ipsos-mori/en-uk/five-years-brexit-they-think-its-all-over-it-isnt 695-696-43-12/Poll Around Two In Five (63%) Of The Unvaccinated Are Convinced By Arguments

Which Say There Hasn’t Been Enough Time To See What The Side-Effects Of The

Vaccine Might Be

Before the vaccine roll-out began late last year, the majority of

Britons were convinced by the argument that there had not been enough time to

see the side-effects of the vaccine – now just two in five (41%) think the

same, down 20ppt. Just six months ago, around half thought there had not been enough

time to test whether the vaccine really works – now just a third (35%) think

that is a persuasive reason to not get vaccinated (down 23ppt). Similarly,

only three in ten (31%) are convinced by the argument that vaccine doses will

be limited, and others will need them more, 20ppt fewer than last November.

Britons yet to be vaccinated are more susceptible towards arguments

against getting jabbed. Around two in five (63%) of the unvaccinated are

convinced by arguments which say there hasn’t been enough time to see what

the side-effects of the vaccine might be. This compares to a third of those

who had at least one dose (33%). Similarly, around half of people unvaccinated are convinced by

arguments against taking it such as there has not been enough time to test

whether it works (52%), doses of the vaccine will be limited and others will

need it more (50%) or they don’t trust the Government telling them to take it

(49%). Meanwhile, the majority of Britons are now convinced by all the

arguments tested in favour of taking the vaccine. Among the most convincing

is that a vaccine will reduce the risk of people becoming seriously ill if

they do catch COVID-19 (83%), along with the belief that getting vaccinated

will protect others from catching the virus (83%).

In fact, overall, confidence in the vaccine remains high, as results

from our latest KnowledgePanel survey show. However, there are concerns about

its effectiveness against new variants of COVID-19; half (48%) say they are

worried about this. Despite these concerns, the survey of over 8,000 adults

in the UK shows that nine in ten people (91%) say it is important to get the

vaccine to stop the spread of new variants. In general, concerns about the effectiveness of the vaccine against

new variants do not seem to be diminishing intentions to have it; 94% of

people say they have already had the vaccine or will have it. However,

worries about its effectiveness are higher amongst groups with lower existing

levels of confidence in the vaccine. For example, concern is highest amongst