|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 707 Week:

September 06 –September 12, 2021 Presentation:

September 17, 2021 707-43-22/Commentary:

Twenty Years On, 80% Of Britons Still Remember Where They Were On 9/11 Indian

Consumers, Reveals A Spending Propensity Of 90.71 Among Urban Indians This

Festive Season Three

In Ten Urban Indians Have Changed Their Primary Bank In The Past More

Than Three-Fourths (77%) Of Guineans Prefer Democracy To Any Other Form Of

Government A

Majority (58%) Of Tanzanians Say They Have Heard Of Social Media 7

In 10 Parents Worried About Their Children Catching Covid-19 When They Return

To School Just

One In Five Members Of The Public Have A Positive View Of The Foreign

Secretary More

Than Two In Five Think Christmas Will Be Free Of Pandemic Restrictions Twenty

Years On, 80% Of Britons Still Remember Where They Were On 9/11 55%

Of Arsenal Supporters Interviewed With Yougov Direct Said They Were Confident

In The Team Most

Britons 57% Want To Ban Cigarettes – And Half Want To Ban Vaping Products Ahead

Of The COVID-19 Recession The Unemployment Rate Was Below 4% 62%

Of Adults With A Disability Say They Own A Desktop Or Laptop Computer One

In Eight (13%) Canadians Is Completely Undecided On How To Vote The

Australian Economy Grew By A Stunning 9.6% Over The Year To June 2021 4

Out Of 10 Brazilians Want To Go Back To Working Outside The Home At The End

Of The Pandemic Most

Adults Vaccinated Against Covid-19 In All 13 Countries Surveyed Intend To Get

A Booster Shot INTRODUCTORY NOTE

707-43-22/Commentary:

Twenty

Years On, 80% Of Britons Still Remember Where They Were On 9/11

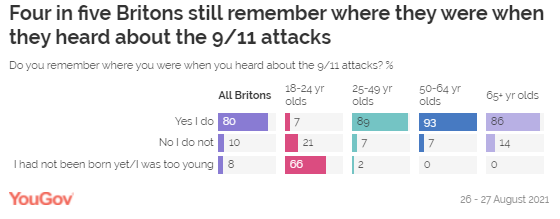

Two decades

have passed since terrorists brought down the Twin Towers in hijacked planes

in an unprecedented attack on the US, killing nearly 3,000 people. A new

YouGov survey now shows that 80% of Britons can still remember where they

were when they heard the news of the incident. Only one in ten people (10%)

can’t remember their whereabouts when hearing the news, while another 8% were

too young or not yet born. Britons aged

50 to 64 are the most likely to remember the day, with 93% saying it’s still

fresh in their memory. Among 18-24-year-olds, 7% remember where they were

when they first heard about the attacks, despite the oldest people in this

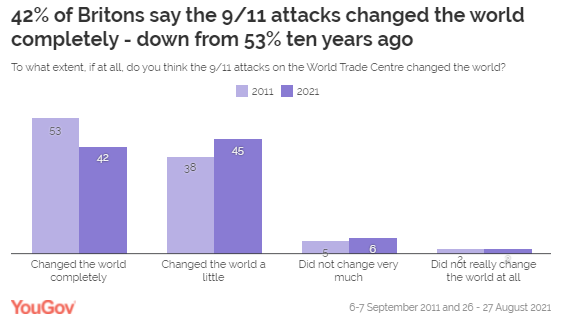

group having been only four years old at the time. Fewer Britons believe 9/11 changed the world completely than ten

years ago While a

large share of the public are convinced that the world was not the same after

9/11, this number of those believing it became radically different has fallen

over time. Two fifths of Britons (42%) say the terrorist incident “changed

the world completely” – down from 53% a decade ago. Another 45% believe it

changed it “a little”, which is slightly higher than in 2011, at 38%. Only one in

twelve people either say it did not change very much (6%) or not at all (2%),

which is similar to previously (5% not very much, 2% not at all). Three in

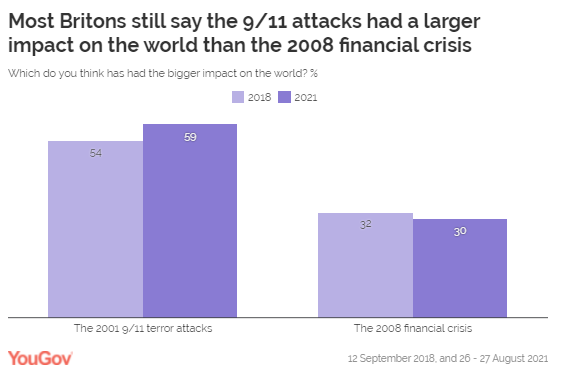

five Britons (59%) likewise say that the 11 September attacks have had a

larger impact on the world than the 2007-08 global financial crisis, a

similar figure to the number who said so in 2018 (54%) on the 10th anniversary

of the crisis. Around three in ten people (30%) currently believe the

financial crisis – which until the coronavirus pandemic had been the worst

recession since the 1920s – had a greater impact (from 32% in 2018). Conservative

voters are slightly more likely than Labour members to say the 9/11 attacks

had a larger impact on the world at 65% vs 54%. But while

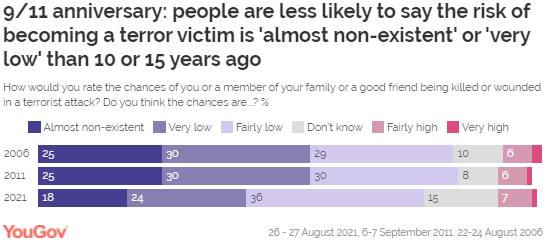

many people still vividly remember hearing about the attacks, and several

terror incidents having happened in the UK since, few Britons fear for their

safety in this context. Some 8% of

the public believe there’s a ‘very’ (1%) or ‘fairly’ (7%) high chance they or

someone close to them would become injured or killed in a terrorist attack.

This is similar to both in 2011 (1% very high, 6% fairly high) and 2006 (2%

very high, 6% fairly high). While the

proportion of people who feel the odds are high remains the same, fewer

people now say the possibility is ‘almost non-existent’ or ‘very low’ than

previously.

In 2006 and

2011, one in four Britons (25%) believed there was virtually no chance they

or a loved one could become a victim of terrorism, while another 29-30% felt

the chance was very low. Today, only

a fifth (18%) regard the possibility as near non-existent, while a quarter

(24%) see it as very low. Instead the most common answer is ‘fairly low’ at

36% - 5-6 points higher than in 2011 and 2006. (YouGov UK) September

09, 2021 707-43-23/Country Profile:

SUMMARY

OF POLLS

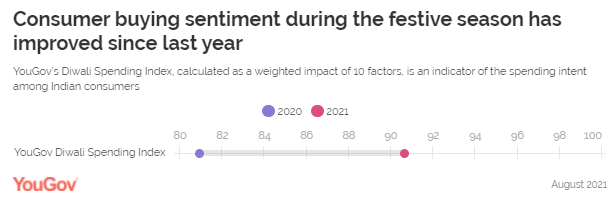

ASIA (India) Indian Consumers, Reveals A Spending Propensity Of 90.71

Among Urban Indians This Festive Season YouGov’s Diwali Spending Index, an

indicator of the spending intent among Indian consumers, reveals a spending

propensity of 90.71 among urban Indians this festive season. Even though it

is below average (of 100), the intent to spend is higher than last time

(80.96), indicating a recovering appetite to spend among urban Indians. (YouGov India) September 7, 2021 Three

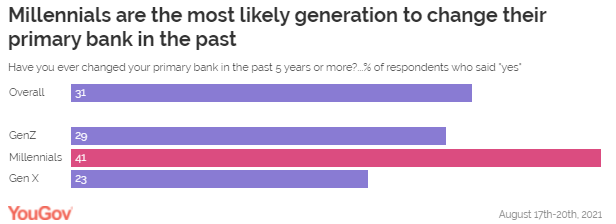

In Ten Urban Indians Have Changed Their Primary Bank In The Past YouGov’s latest survey reveals close to a

third (31%) of urban Indians claim to have changed their primary bank in the

past five years or more. Among different generations, millennials appear to

be the most visible switchers and are much more likely than Gen X to have

changed their primary bank in the past (41% vs 23%). Among the genders, men

as compared to women are more likely to switch in the future (58% vs 50%). (YouGov India) September 9, 2021 AFRICA (Guinea) More Than Three-Fourths (77%) Of Guineans Prefer Democracy

To Any Other Form Of Government Dissatisfaction with the country’s economic

conditions and citizens’ personal living conditions has increased, as have

negative ratings of the government’s economic performance and provision of

essential public services. Only three in 10 citizens are satisfied with the

way their democracy is working. But the study also shows that most Guineans

endorse elections as the best way to choose leaders and that citizens’

preference for democracy has remained consistently high over the years. (Afrobarometer) 6 September 2021 (Gambia) More Than One In Four Gambian Citizens (28%) Say They Or A

Member Of Their Family Suffered Human-Rights Abuses Under Jammeh’s Regime Almost three-fourths (73%) of Gambians say

perpetrators of crimes and human-rights abuses during Jammeh’s regime should

be tried in court, a 5-percentage-point increase compared to 2018. More than

one in four citizens (28%) say they or a member of their family suffered

human-rights abuses under Jammeh’s regime. Citizens expect the TRRC’s work to

lead to a variety of outcomes, including national peace, reconciliation,

forgiveness, and healing (34%). (Afrobarometer) 6 September 2021 (Tanzania) A

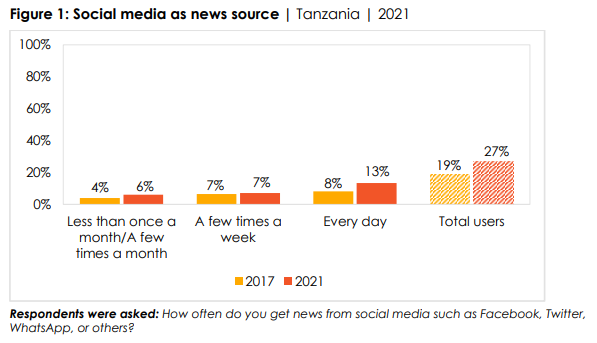

Majority (58%) Of Tanzanians Say They Have Heard Of Social Media One in five Tanzanians say they get news

from social media every day (13%) or “a few times a week) (7%). In total, 27%

of citizens say they use social media for news at least on occasion, a

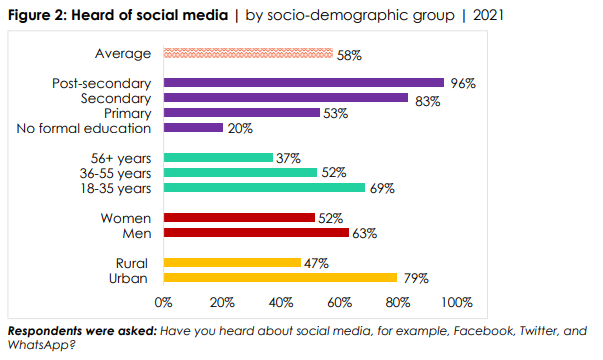

9-percentage-point increase compared to 2017. A majority (58%) of Tanzanians

say they have heard of social media. Awareness of social media is higher

among men and urbanites than among women and rural residents, and increases

strongly with respondents’ education level, ranging from 20% of those with no

formal education to 96% of those with post-secondary qualifications. (Afrobarometer) 8 September 2021 (South

Africa) Seven In Every Ten (71%) South Africans Have Indicated That

They Would Vote In The Coming Local Government Elections Countrywide almost half (49.3%) will draw a

cross next to the name of the ANC, while the support for both the DA (17.9%)

and the EFF (14.5%) respectively, is also in double figures. South Africa has

a plethora of registered political parties, but very few of them currently

garner more than one percent of support. (Ipsos South

Africa) 7 September 2021 WEST

EUROPE (UK) 7

In 10 Parents Worried About Their Children Catching Covid-19 When They Return

To School With children starting to head back to the

classroom, polling by Ipsos MORI shows a large majority of British parents

with school-age children are concerned about the risk of their child(ren)

catching COVID-19 while at school. Seventy per cent are concerned about this

risk with only 3 in 10 untroubled. Worry increases slightly among

mothers with children at school, 74% of whom are worried compared to 64% of

fathers. (Ipsos MORI) 6 September 2021 Just

One In Five Members Of The Public Have A Positive View Of The Foreign

Secretary Only one in five people (19%) now hold a favourable

view of Raab, down 3pts since mid-August. A majority of people now hold an

unfavourable view of him (58%), an increase of 9pts versus August. This

represents the highest level of unfavourable opinion Raab has held since our

polling of him began in 2020. Overall, these latest favourability scores give

the foreign secretary a net score of -39 among the general public. (YouGov UK) September 06, 2021 41% Of Britons Said Brexit Is The Main

Reason For Reported Shortage Of Drivers And Supply Chain Issues In recent weeks there has been a growing

issue with a shortage of delivery drivers, with the media reporting widely on

supermarkets, fast food restaurants and pubs facing problems with their

supply chain. Many commentators have associated this problem with Brexit. Asked

what the main reason is for the reported shortage of drivers and supply chain

issues, 41% of people said Brexit, 25% the impact of the coronavirus, 11%

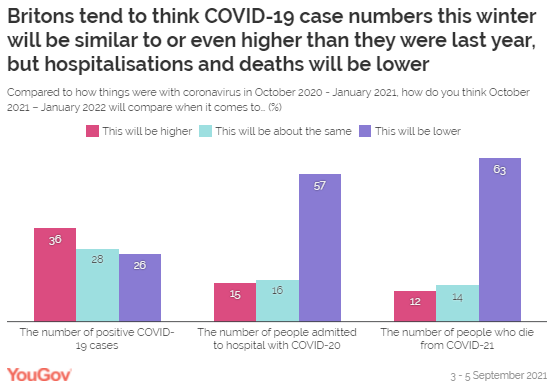

working conditions for drivers and 7% drivers' pay. (YouGov UK) September 07, 2021 More Than Two In Five Think Christmas Will

Be Free Of Pandemic Restrictions According to reports, the October lockdown

could be implemented if COVID-19 hospitalisations continue at their current

rate and overwhelm the NHS - something the government has since denied.

However, most people (57%) predict that October 2021 to January 2022 will see

fewer hospitalisations than the same period a year ago – a period that

encompassed the bulk of the UK’s second wave. Yet some 31% of people think that

this year could be on par (16%) or worse (15%) than the previous period in

terms of people admitted to hospital. (YouGov UK) September 08, 2021 Twenty Years On, 80% Of Britons Still

Remember Where They Were On 9/11 Two decades have passed since terrorists

brought down the Twin Towers in hijacked planes in an unprecedented attack on

the US, killing nearly 3,000 people. A new YouGov survey now shows that 80%

of Britons can still remember where they were when they heard the news of the

incident. Only one in ten people (10%) can’t remember their whereabouts when

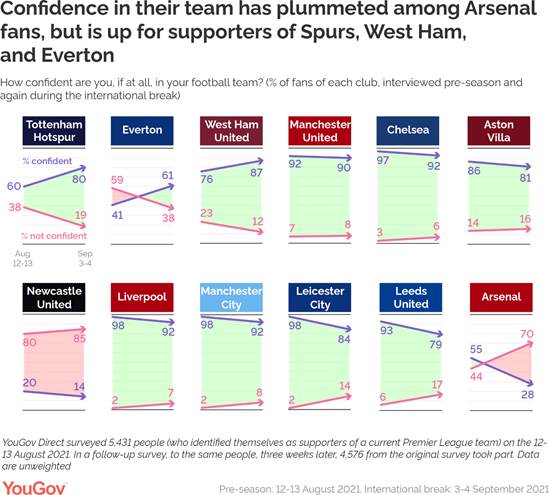

hearing the news, while another 8% were too young or not yet born. (YouGov UK) September 09, 2021 55% Of Arsenal Supporters Interviewed With

Yougov Direct Said They Were Confident In The Team Arsenal have had a rough start to the

2021/22 season, with three back-to-back losses sending them to the bottom of

the table. As a result, confidence among Gunners fans has taken a significant

dive. Before the season kicked off, 55% of Arsenal supporters interviewed

with YouGov Direct said they were confident in the team. This figure has

since dropped 27pts to just over a quarter (28%). This trend is not limited

to Arsenal, with fans of several other teams having lost a lot of faith,

including Leeds United (79%, down 14 pts from pre-season) and Leicester City

(84%, down 13pts). (YouGov UK) September 09, 2021 4 In 10 Britons Think Country Heading In

Wrong Direction But Johnson Much More Popular Than Starmer Among Their Own

Voters Ahead of party conference season, a new

Ipsos MORI poll of Britons aged 18+ (taken before the recent NI announcement)

shows that 44% of Britons think things are heading in the wrong direction (no

change from July) and 29% think things are heading in the right direction (-1

point). The data shows a predictable party split on this measure with 48% of

2019 Conservative voters saying things are heading in the right direction

compared to 64% of Labour voters saying things are heading in the wrong

direction. (Ipsos MORI) 10 September 2021 Most Britons 57% Want To Ban Cigarettes –

And Half Want To Ban Vaping Products It’s a move that’s broadly in tune with

public sentiment: new polling from YouGov shows that close to three in five

Britons (57%) support an outright ban on the sale of cigarettes, compared to

a third (32%) who do not. And while one in five (19%) are in favour of a ban

from 2030 onwards, two in five (38%) want the government to move even faster

– outlawing these products either immediately or in the near future. (YouGov UK) September 10, 2021 NORTH AMERICA (USA) Ahead Of The COVID-19 Recession The Unemployment Rate Was

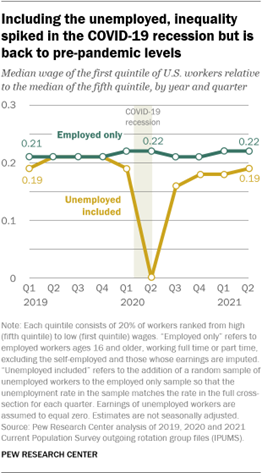

Below 4% The median wage of employed U.S. workers

had held steady at about $21 per hour for several calendar quarters before

the coronavirus outbreak. With the unemployment rate hovering below 4% ahead

of the COVID-19 recession, even if unemployed workers were included – at zero

earnings – there was little effect on the estimated median wage, nudging it

down to about $20 in 2019, but no more. (Wages are adjusted for inflation and

expressed in 2021 second-quarter dollars.) (PEW) SEPTEMBER 7, 2021 62% Of Adults With A Disability Say They Own A Desktop Or

Laptop Computer Some 62% of adults with a disability say

they own a desktop or laptop computer, compared with 81% of those without a

disability, according to a Pew Research Center survey of U.S. adults

conducted Jan. 25-Feb. 8, 2021. And when it comes to smartphone ownership,

there is a gap of 16 percentage points between those with a disability and

those without one (72% vs. 88%). (PEW) SEPTEMBER 10, 2021 (Canada) 46% Of Canadians Who Say They Are Going To Support A Party

On Election Day Are Absolutely Certain Of Their Vote Choice According to a new Ipsos poll conducted on

behalf of Global News, only 46% of Canadians who say they are going to

support a party on election day are absolutely certain of their vote choice,

leaving the remaining voters less sure (39% fairly certain; 11% not very

certain; 4% not at all certain). Conservative voters (49%, +3 since the start

of the campaign) and Liberal voters (49%, +1) are most likely to be

absolutely certain of their choice, with NDP (43%, +6), Bloc (43%, +13) and

Green Party (26%, +13) supporters less certain of their choice. (Ipsos Canada) 6 September 2021 One In Eight (13%) Canadians Is Completely Undecided On How

To Vote Over the course of the election campaign,

Ipsos polling has revealed that one in eight (13%) Canadians is completely

undecided on how they will vote in this federal election. A closer

examination of this key group of voters reveals who they are, how they feel

and what is important to them when considering how to cast their ballot. Two

in three (67%) are women; one in three (33%) are men. (Ipsos Canada) 9 September 2021 AUSTRALIA The Australian Economy Grew By A Stunning 9.6% Over The

Year To June 2021 Retailers have been the big winners during

this period and the top four most

trusted brands again comprise some of Australia’s leading

retail brands led by Woolworths, Coles, Bunnings Warehouse and ALDI in fourth

place. Notably, there have been four big improvers in the June quarter 2021

with Department Stores Kmart, Myer, Big W and Target all improving their

standing as some of Australia’s most trusted brands. Kmart has entered the

top 5, both Myer and Big W are new entrants to the top 10 and Target jumped

seven spots in the quarter to be just outside the top 10. (Roy Morgan) September 07 2021 MULTICOUNTRY STUDIES 4 Out Of 10 Brazilians Want To Go Back To Working Outside

The Home At The End Of The Pandemic The Return to the Workplace 2021 Global

Survey, carried out by Ipsos in 29 nations – including Brazil – showed that

40% of respondents in the country want to work outside their homes in the

post-pandemic period. A slightly smaller percentage, 31%, prefer to work

more or completely at home-office. 9% prefer to work from home as much

as they used to do before the health crisis, 10% did not know how to answer

and 11% said that the nature of their work does not allow them to choose

where to work. On the global average, the percentage of people who want

to work outside the home is 33%. (Ipsos Brazil) 8 September 2021 Most Adults Vaccinated Against Covid-19 In All 13 Countries

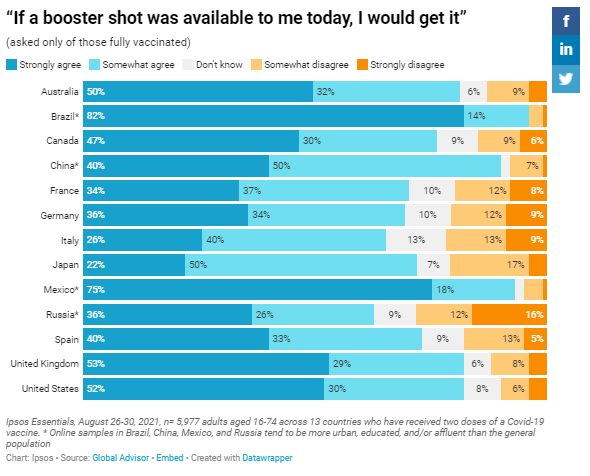

Surveyed Intend To Get A Booster Shot In each of the 13 countries surveyed, a

large majority of adults who have received two doses of a COVID-19 vaccine

strongly or somewhat agree they would get a booster shot if it were available

today, 90%+ in Brazil (96%), Mexico (93%), and China (90%); 80%+ in Australia

(82%), the United Kingdom (82%), and the United States (81%); 70%+ in Canada

(77%), Spain (73%), Japan (72%), France (70%), and Germany (70%); and 60%+ in

Italy (66%) and Russia (62%). (Ipsos Canada) 10 September 2021 Source: https://www.ipsos.com/en-ca/news-polls/global-attitudes-covid-19-vaccine-booster-shots ASIA

707-43-01/Polls Indian

Consumers, Reveals A Spending Propensity Of 90.71 Among Urban Indians This

Festive Season

The festive season has commenced in India

and now everyone is eagerly awaiting the festival of lights. Although brands

are betting big on Diwali to light up sales, are consumers ready to shop

again? YouGov’s Diwali Spending Index, an

indicator of the spending intent among Indian consumers, reveals a spending

propensity of 90.71 among urban Indians this festive season. Even though it

is below average (of 100), the intent to spend is higher than last time (80.96),

indicating a recovering appetite to spend among urban Indians.

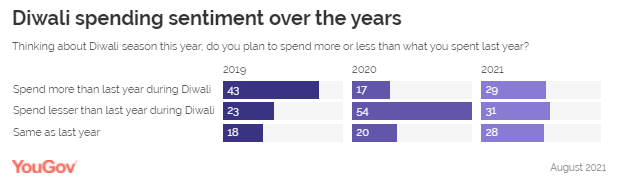

Among the 10 factors, the number one driver

for people to spend more this year is their anticipation for the festival.

Nearly a third (31%) agreed with the statement “I am looking forward to Diwali this year since the

rest of the year has been quite dull because of Covid-19”. With nearly two years having passed and

shoppers having no opportunity to spend, this is likely to be the factor that

has improved the overall sentiment to spend more this Diwali as compared to

last. Even though there is an improvement, the

biggest barrier to spending continues to be the same as last year. Close to

50% of respondents last year said they are more careful with their finances

today than they used to be in the past. And now a similar proportion (43.6%)

said the same thing, indicating the fear of the uncertain is still strong

among the public. Given 2021 witnessed a devastating wave of

covid, despite excitement among the public for Diwali this year, the consumer

sentiment is yet to match the pre-pandemic times.

In YouGov’s Diwali series, we will see the

impact of the pandemic on consumers’ buying sentiment across different

sectors to see if the upcoming festive season can be a game-changer for

businesses and brands. (YouGov India) September 7, 2021 Source: https://in.yougov.com/en-hi/news/2021/09/07/urban-indians-festive-spending-intent-has-improved/ 707-43-02/Polls Three In Ten

Urban Indians Have Changed Their Primary Bank In The Past

YouGov’s latest survey reveals close to a

third (31%) of urban Indians claim to have changed their primary bank in the

past five years or more. Among different generations, millennials appear to

be the most visible switchers and are much more likely than Gen X to have

changed their primary bank in the past (41% vs 23%).

While convenience was the main reason to

switch for all the surveyed respondents, nearly a quarter (23%) switched in

order to move to a bank that offers digital services or is a digital only

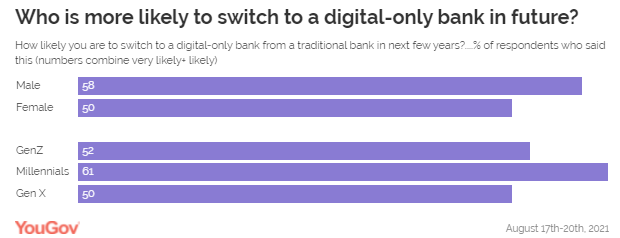

bank, highlighting the building appetite for online banking in the country. Looking into the future banking

preferences, we see more than half of urban Indians (54%) said they are likely

to switch from a traditional to a digital bank in the near future. Once again

we see millennials being most likely to say they will switch their bank in

the future (at 61%), perhaps because they are already used to shifting banks

and are more likely to be swayed by better services and benefits. Among the genders, men as compared to women

are more likely to switch in the future (58% vs 50%).

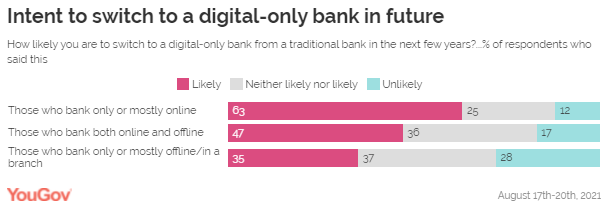

While the intent to switch to an

online-only bank in the future is higher among respondents who only or mostly

bank online (at 63%), those who bank both online and offline were also more

likely than unlikely (47% vs 17%) to say they will switch to a digital bank

in the future.

Cashbacks and rewards appeal more to the

millennials than the GenX, while the older cohort is more likely to find the

round-the-clock accessibility as well as ease and convenience of banking the

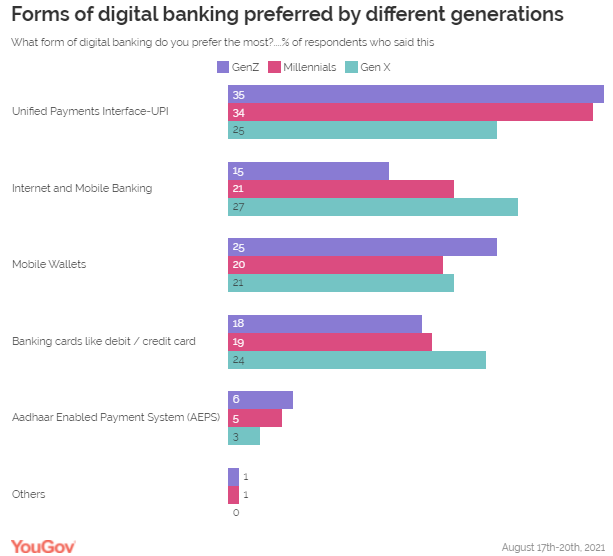

biggest advantage of digital banking. When asked about the various forms of

digital banking, Unified Payments Interface or UPI payments emerged as the

most preferred form of digital banking for nearly a third (31%) of

respondents. Other preferred forms include internet & mobile banking

(22%), mobile wallets, and banking cards (21% each) are other preferred forms

of digital banking.

Commenting on this, Deepa Bhatia, General

Manager, YouGov India said, “Banking has

been considered for long as a more traditional industry with high switching

costs but with the advent of digital banking services, we can see the

switching costs come down. Millennials, those aged between 30 and 40years

old, one of the most sought-after cohorts have been particularly open to

switching their primary bank accounts and are fairly open to digital banks.

Banking needs to learn about the changing motivations of their customers so

as to better serve them and retain them.” (YouGov India) September 9, 2021 Source: https://in.yougov.com/en-hi/news/2021/09/09/three-ten-urban-indians-have-changed-their-primary/ AFRICA

707-43-03/Polls More Than

Three-Fourths (77%) Of Guineans Prefer Democracy To Any Other Form Of

Government

Despite widespread dissatisfaction with the

government’s performance, Guineans strongly prefer democracy to any alternative form of

governance, the most recent Afrobarometer survey shows. Barely a year after claiming a third term

in office amidst widespread opposition, President Alpha Condé has been detained since a coup

d’état last Sunday. Coup leader Lt. Col. Mamady Doumbouya has cited pervasive

poverty and corruption as reasons for the takeover. Afrobarometer findings from late 2019 show

majorities of Guineans believe that the country is heading in the wrong direction, that the

level of corruption has increased, and that the government is doing a poor job of fighting

corruption. Dissatisfaction with the country’s economic conditions and citizens’ personal

living conditions has increased, as have negative ratings of the government’s economic

performance and provision of essential public services. Only three in 10 citizens are

satisfied with the way their democracy is working. But the study also shows that most Guineans

endorse elections as the best way to choose leaders and that citizens’ preference for

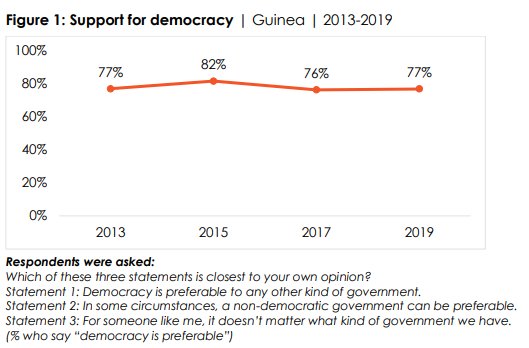

democracy has remained consistently high over the years. Key findings ▪ More than three-fourths (77%) of

Guineans prefer democracy to any other form of government. Support for democracy has

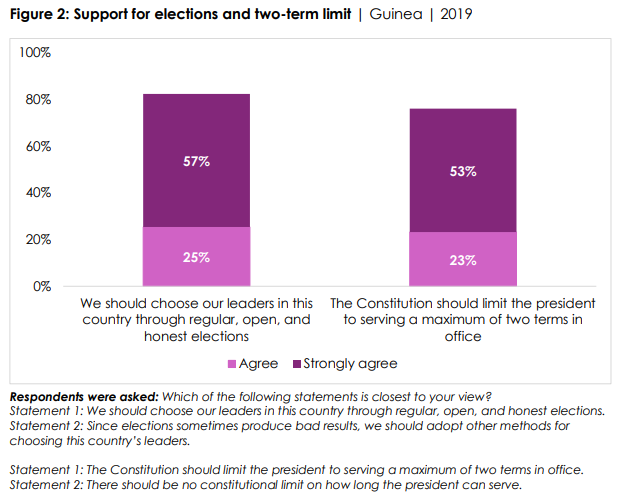

remained high since Afrobarometer began its surveys in Guinea in 2013 (Figure 1). ▪ Eight in 10 Guineans (82%) endorse

free, fair, and honest elections as the best way to choose leaders, including 57% who “strongly

agree” with this view (Figure 2). o A similar majority (76%) want the

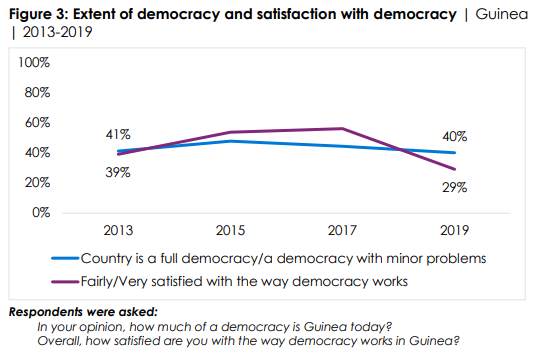

president to serve a maximum of two terms in office. ▪ Only four in 10 Guineans (40%)

describe the country as “a full democracy” or “a democracy with minor problems” (Figure 3). o Only three in 10 (29%) say they are

“fairly satisfied” or “very satisfied” with the way democracy works, a sharp decline from 2017

(56%) after consistent improvement from 2013 (39%). ▪ Almost two-thirds of Guineans (64%)

say the country is heading in “the wrong direction.” ▪ The perception that “most” or “all”

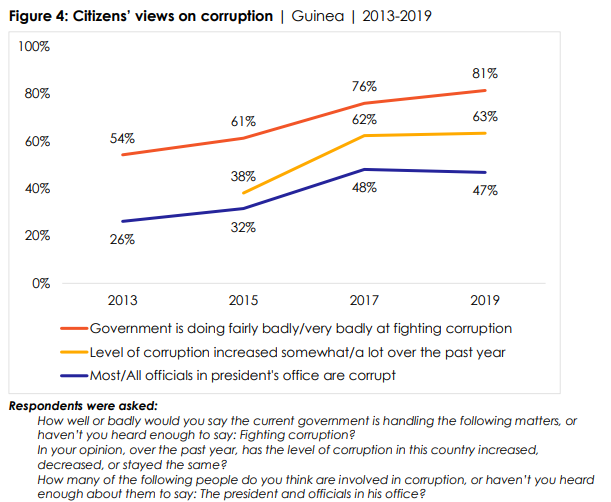

officials at the Presidency are corrupt has increased from 26% in 2013 to 47% (Figure

4). o Almost two-thirds (63%) of citizens say

the level of corruption in the country increased during the year preceding the

survey, a 25-percentage-point increase compared to 2015 (38%). o Eight in 10 citizens (81%) say the

government is performing “fairly badly” or “very badly” in fighting corruption, a

27-percentage-point increase compared to 2013 (54%). ▪ Almost seven in 10 citizens (68%)

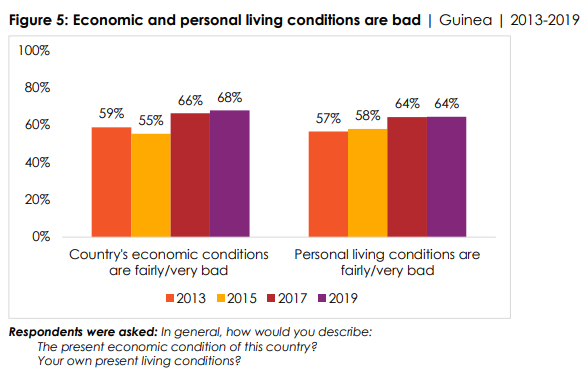

describe the country’s economic conditions as “fairly bad” or “very bad,” a significant increase

compared to 2013 (59%) (Figure 5). o The proportion who say their personal

living conditions are “fairly bad” or “very bad” has also increased, to 64%. ▪ About nine in 10 Guineans say the

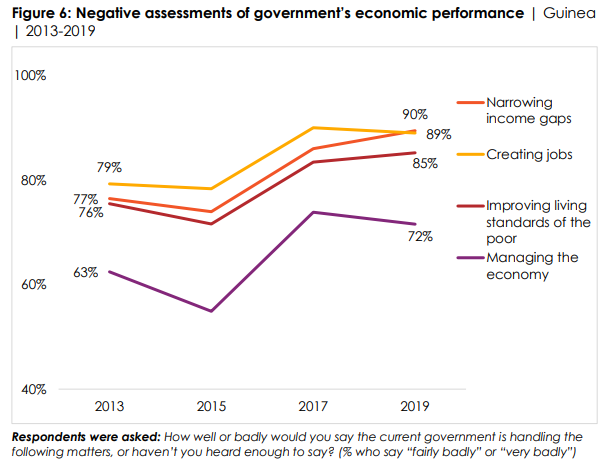

government is doing “fairly badly” or “very badly” at narrowing income gaps (90%), creating

jobs (89%), and improving living standards of the poor (85%) (Figure 6). o Seven in 10 (72%) rate the government

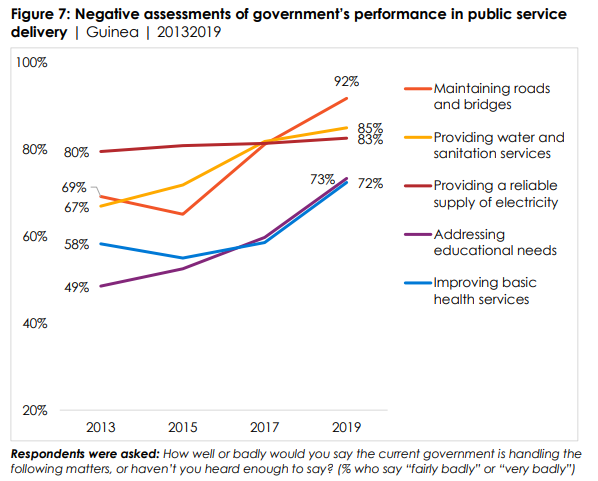

poorly on its performance in managing the economy. ▪ Overwhelming majorities also say

the government is doing a poor job of maintaining roads and bridges (92%), providing water

and sanitation services (85%), providing a reliable supply of electricity (83%),

addressing educational needs (73%), and improving basic health services (72%)

(Figure 7). (Afrobarometer) 6 September 2021 707-43-04/Polls More Than

One In Four Gambian Citizens (28%) Say They Or A Member Of Their Family

Suffered Human-Rights Abuses Under Jammeh’s Regime

A growing number of Gambians want

perpetrators of crimes and human-rights abuses during former President Yahya Jammeh’s

administration to be tried in court, the latest Afrobarometer study shows. Over the past three years, the proportion

of citizens in favour of seeking Jammeh’s extradition has also increased

significantly. However, opinions are divided on the government’s decision to sell Jammeh’s

properties and on whether he should be allowed to return to the country. The Gambia’s Truth, Reconciliation and

Reparations Commission (TRRC) was established by Parliament in December 2017 as part of a

broad transitional-justice mechanism to address human-rights abuses under Jammeh’s

regime and prevent their recurrence. After two years of televised public

hearings, the commission is expected to submit its final report to President Adama Barrow in

September 2021. Although widely credited with highlighting past human-rights abuses, the

commission has also been engulfed in controversies, including accusations of

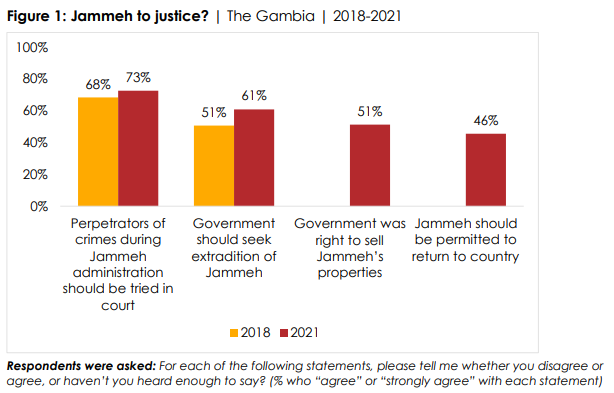

conducting a witch-hunt against Jammeh. Key findings ▪ Almost three-fourths (73%) of

Gambians say perpetrators of crimes and human-rights abuses during Jammeh’s regime should be

tried in court, a 5-percentage-point increase compared to 2018 (Figure 1). ▪ Six in 10 Gambians (61%) say the

government should seek the extradition of Jammeh, a 10-percentage point increase compared to

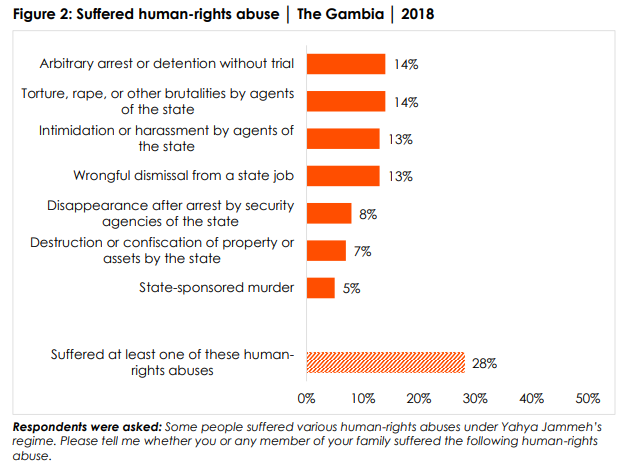

2018. ▪ More than one in four citizens

(28%) say they or a member of their family suffered human-rights abuses under Jammeh’s regime

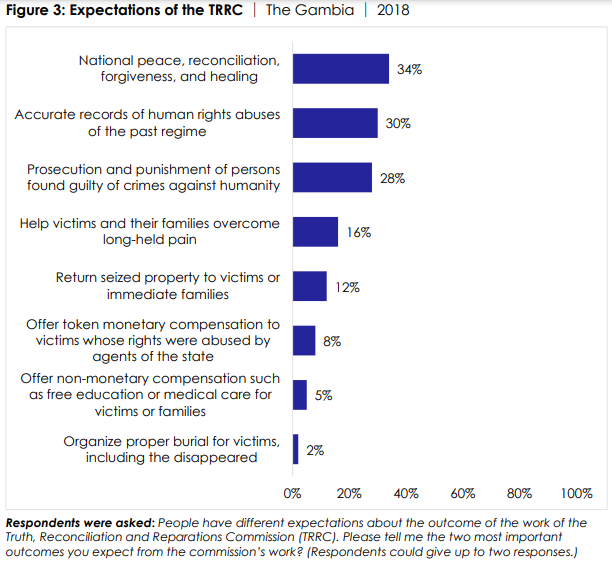

(Figure 2). ▪ Citizens expect the TRRC’s work to

lead to a variety of outcomes, including national peace, reconciliation, forgiveness, and

healing (34%); accurate records of humanrights abuses of the previous regime

(30%); prosecution of accused perpetrators (28%); and support for victims and their

families to overcome long-held pain (16%) (Figure 3). (Afrobarometer) 6 September 2021 707-43-05/Polls A Majority

(58%) Of Tanzanians Say They Have Heard Of Social Media

A majority of Tanzanians support unrestricted

access to social media, but most are also wary of its potential dangers, the latest

Afrobarometer survey shows. Among Tanzanians who have heard of social

media, large majorities believe that such platforms help make people more informed

and effective citizens. However, most also say that social media make people more likely

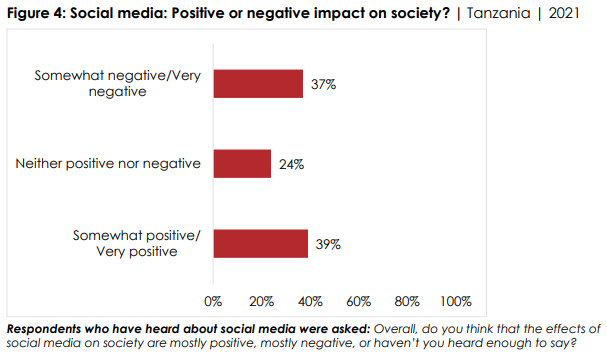

to believe false news and more intolerant of people with different opinions. Overall, Tanzanians are almost evenly

divided on whether the impact of social media on society is positive or negative. Key findings One in five Tanzanians say they get news

from social media every day (13%) or “a few times a week) (7%). In total, 27% of

citizens say they use social media for news at least on occasion, a 9-percentage-point

increase compared to 2017 (Figure 1). A majority (58%) of Tanzanians say they

have heard of social media (Figure 2). o Awareness of social media is higher among

men and urbanites than among women and rural residents, and increases

strongly with respondents’ education level, ranging from 20% of those with no

formal education to 96% of those with post-secondary qualifications. Youth (69%)

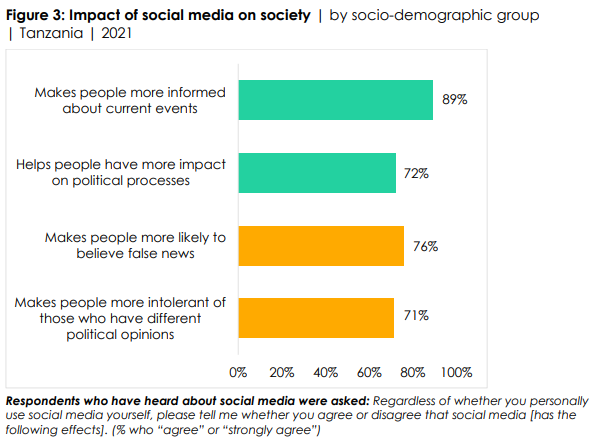

are almost twice as likely to be familiar with social media as older citizens (37%). Among those who have heard of social media: o Most believe that it makes people more

aware of current happenings (89%) and helps people impact political processes

(72%) (Figure 3). o But large majorities also say that it

makes people more likely to believe false news (76%) and more intolerant of others with

different political opinions (71%). o Overall, Tanzanians are almost evenly

split in their views on the effect of social media on society: 39% see its impact as

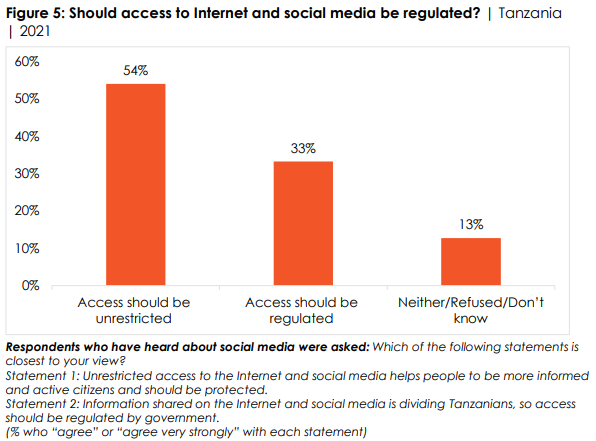

positive, while 37% say it is negative (Figure 4). More than half (54%) of Tanzanians say that

access to social media and the Internet should be unrestricted, while one-third

(33%) want access to be regulated by the government (Figure 5). o Educated citizens, youth, men, and urban

residents are less likely to support the regulation of social media. (Afrobarometer) 8 September 2021 707-43-06/Polls Seven In

Every Ten (71%) South Africans Have Indicated That They Would Vote In The

Coming Local Government Elections

The IEC, supported by some political parties,

brought this application before the apex court due to the complications in

organising local government elections in the middle of the Covid-19 pandemic.

The Constitutional Court ruled that the elections should be scheduled between

27 October and 1 November 2021. The court

ruled that the IEC must comply with the Constitutional prescription that

elections should be held within five years and ninety days of the date of the

previous local government elections. The IEC has also been ordered to

announce a date for a voter registration weekend within three days of the

court’s ruling. Although the

IEC could still approach the Parliament of the Republic of South Africa and seek a postponement of the

elections by amending the Constitution, this will require a two-thirds

majority in Parliament, and it is uncertain if there will be enough support

to delay the polls. Approaching

Parliament would probably limit the little time left to organise and

formulate the logistics of this rather complex process. As there are 278

municipalities1 in South Africa, this essentially means that

everything necessary to successfully organise and implement 278

mini-elections should be done in less than two months. The national

picture – uncertainty and a limited appetite for voting On the

ground very little campaigning has so far been done for these elections and

it is difficult for political

parties to

organise meetings, rallies and all the other usual opportunities to speak to

voters. The reasons are clear. Covid-19 restrictions limit the number of

people who can get together in the same place. But how do

South African voters feel about these elections? There are around 39 million

South Africans eligible to vote – i.e. 18 years or older, but not all of them

are registered. In fact, less than 20 million voted in the last national

election in 2019. Will South

Africans turn out to vote this time or will fear of Covid-19 keep them away?

Or will those who want to vote now visit vaccination centres in droves? In both

the 2016

local government elections and the 2019 national and provincial

elections, voter turnout was down from previous elections. So, is voter

apathy still an issue? Voters have

expressed their discontent with politics and political parties in various

ways over the last few years. Will this have an influence on voter turnout,

or perhaps on the political parties themselves? Traditionally

the voter turnout in local government elections is lower compared to national

and provincial elections – will this be the case again? Ipsos has undertaken a CATI (Computer

Assisted Telephone Interviewing) study from 16 to 20 August 2021,

interviewing 1,501 randomly selected adults in the country about some of

these issues2. The table

overleaf look at some comparisons over time:

Please note

that this table shows results for ALL SOUTH AFRICANS 18 YEARS AND OLDER – it

cannot in any way be construed as a possible prediction of

the outcome of the local government elections.

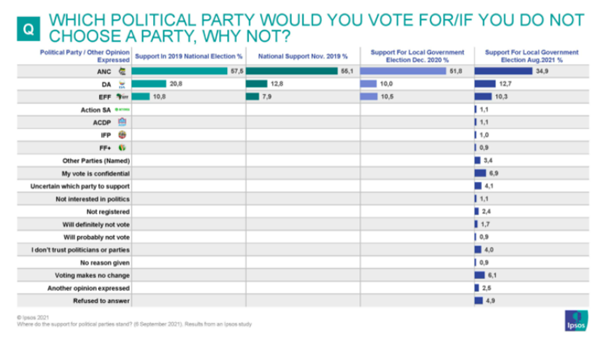

This table

shows a steady decline in support for the ANC in polls involving the total

population eligible to vote since after the previous National Election in May

2019. Over the time of the three Ipsos studies mentioned, the DA and the EFF support stayed relatively constant,

however, none of these two parties were threatening the position of the ANC

as the most popular party in the country. Some

interesting reasons mentioned for not considering voting were3:

A more

realistic view – what if 7 out of every 10 turn out to vote? It is

abundantly clear that not all eligible voters will vote in the local

government elections at the end of October, so, “if there were a local government election tomorrow, which political

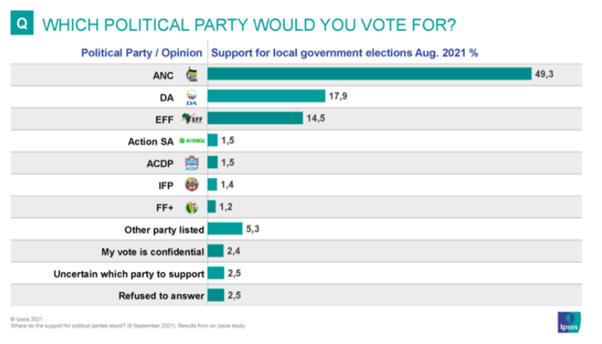

party or organisation will you vote for?” Seven in

every ten (71%) have indicated that they would vote in the coming local

government elections. The data suggest they would also support a wide variety

of parties, as reflected in the graph below. Countrywide almost half (49.3%) will draw a

cross next to the name of the ANC, while the support for both the DA (17.9%)

and the EFF (14.5%) respectively, is also in double figures. South Africa has

a plethora of registered political parties, but very few of them currently garner

more than one percent of support. Please note

that this is also not a prediction of the election, although

a large proportion of voters have made up their minds, 7.4% of those who

indicated that they will vote in the local government elections are not (yet)

allocated to a political party. Predictions, for what they are worth, should

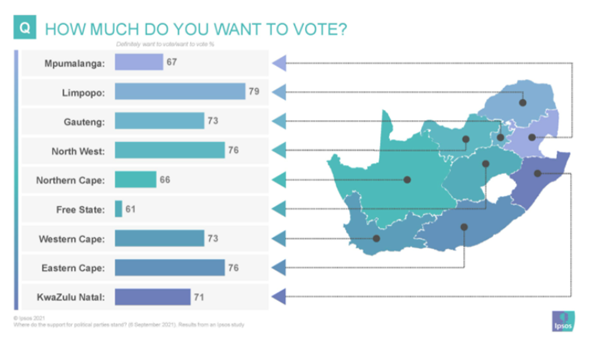

only be made much closer to election day. Who wants to

vote? Looking at

those who indicated that they do want to vote in the local government

elections, it is interesting that the more rural provinces of Limpopo, North

West and the Eastern Cape top the list. And yet, metropolitan areas feature

much more frequently in the travel plans of political leaders. The Free

State has experienced a lot of political turmoil since the last national

election, very much like North West. It reacted totally differently with a

much smaller proportion of voters wanting to participate in the local

government elections. (Ipsos South

Africa) 7 September 2021 Source: https://www.ipsos.com/en-za/where-do-support-political-parties-stand WEST

EUROPE

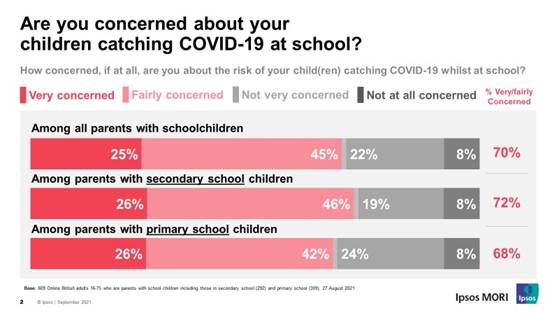

707-43-07/Polls 7 In 10 Parents Worried About Their Children Catching Covid-19 When

They Return To School

With children starting to head back to the classroom, polling by

Ipsos MORI shows a large majority of British parents with school-age children

are concerned about the risk of their child(ren) catching COVID-19 while at

school. Seventy per cent are concerned about this risk with only 3 in 10

untroubled. Worry increases slightly among mothers with children at school, 74%

of whom are worried compared to 64% of fathers. Those with children at

secondary school are more likely to worry, 72% are concerned about the risk

of their children catching COVID-19 while 68% of primary school parents feel

the same.

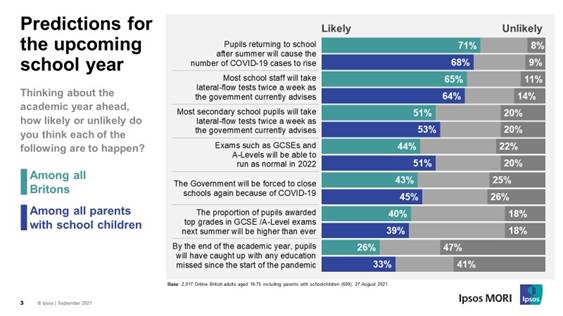

While almost two-thirds (65%) think most school staff will take

lateral-flow tests twice a week, as the government currently advises, only

half of secondary school pupils are likely to so the same (51%).

Less than half of Britons (44%) expect to see exams such as GCSEs and

A-Levels run as normal in 2022, 22% think this is unlikely. Parents are

slightly more hopeful, 51% say exams are likely to run as usual. Four in 10

(40%) say it is likely that the proportion of pupils awarded top grades in

their GCSE and A-Level exams will be higher than ever, 1 in 5 (18%)

disagree. More than 4 in 10 (43%) believe the Government will once again be

forced to close schools because of COVID-19, 1 in 4 disagree. Therefore, it

may be no surprise that almost half say it is unlikely that by the end of the

upcoming academic year, pupils will have caught up with any education missed

since the start of the pandemic (47%), only a quarter think this is likely to

happen (26%), increasing to a third of parents (33%). Kelly Beaver, Managing Director of Public

Affairs at Ipsos MORI, said: As pupils return to schools across the

country, it’s clear that there is a certain degree of concern and trepidation

about the impact of that on COVID cases, as well as concern among parents

about the more direct impacts on them and their children. There are also

broader educational concerns about the way that exams will be run next year

and about the degree to which pupils will have ‘caught up’ on time lost

academically from last year. These are important issues for parents, who’ll

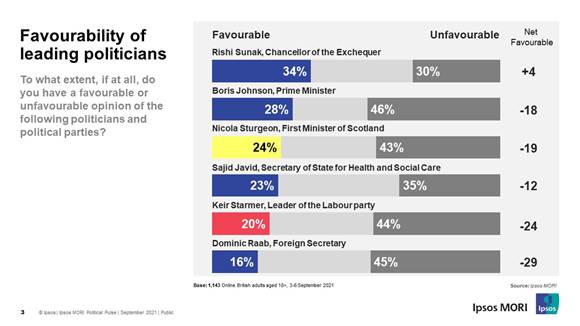

be watching closely to see what the Government does around this crucial area. (Ipsos MORI) 6 September 2021 707-43-08/Polls Just One In Five Members Of The Public Have A Positive View Of The

Foreign Secretary

The foreign secretary Dominic Raab has been under intense scrutiny

following his handling of the crisis in Afghanistan - from being on holiday during

the start of the crisis, to delegating

important tasks to junior aides. The newest YouGov favourability

data shows that this approach has sent Raab’s standing with members of the

public to an all-time low. Only one in five people (19%) now hold a favourable view of Raab, down

3pts since mid-August. A majority of people now hold an unfavourable view of

him (58%), an increase of 9pts versus August. This represents the highest

level of unfavourable opinion Raab has held since our polling of him began in

2020. Overall, these latest favourability scores give the foreign secretary

a net score of -39 among the general public.

Along political lines, some 45% of 2019 Conservative voters have an

unfavourable view of Raab versus 37% who think the opposite – giving him a

net score of -8 among his party’s voters. Of Labour voters, only 8% think

favourable of Raab, while 79% have an unfavourable opinion – a net score of

-71. Elsewhere, the party leaders have seen their scores increase compared

to August, however they remain firmly in the negative. Boris Johnson’s net

score has increased from -25 to -19, with 36% of the public viewing him

favourably and 55% unfavourably. Keir Starmer has seen his net score rise

7pts from -30 to -23. Approaching three in ten (29%) now view the leader of the

opposition favourably, while half (52%) hold an unfavourable view. (YouGov UK) September 06, 2021 707-43-09/Polls 41% Of Britons Said Brexit Is The Main Reason For Reported Shortage

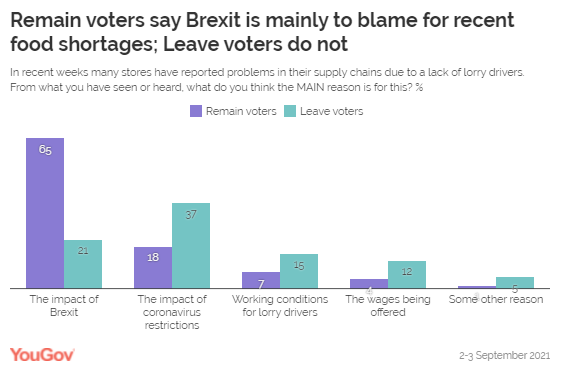

Of Drivers And Supply Chain Issues

In recent weeks there has been a growing issue with a shortage of

delivery drivers, with the media reporting widely on supermarkets, fast food

restaurants and pubs facing problems with their supply chain. Many

commentators have associated this problem with Brexit. Asked what the main reason is for the reported shortage of drivers

and supply chain issues, 41% of people said Brexit, 25% the impact of the

coronavirus, 11% working conditions for drivers and 7% drivers' pay. However, there's a big contrast between the views of Remainers and

Leavers. Among those respondents who voted Remain in 2016, 65% of people

blamed the supply chain problems mostly upon Brexit. Among those respondents

who voted to Leave in 2016, just 21% said the problems were due to Brexit.

Leave voters are most likely to say that coronavirus is the key to the recent

shortages (37%), and they are also more likely than Remain voters to think

that drivers’ pay or conditions are the biggest part of the problem.

In fact, even opinions on whether there are shortages appear influenced

by people's existing views on Brexit. Most people who voted Remain say they

have noticed shortages on the shelves to a large or significant extent (55%),

but only 40% of Leavers do. As with most other political events, our reactions to the drivers’ shortage

are largely driven by our existing views. If you are someone who thought

Brexit was a thoroughly bad thing, then you are more likely to blame it on

Brexit. If you are a supporter of Brexit, then you are more likely to find

another reason. So, whatever the long-term outcome of Brexit, don't necessarily

expect public opinion to rapidly change. Many perceived negative impacts of

Brexit will only be blamed upon Brexit by those already opposed; many

positive impacts will only be accepted by those who were already in favour. (YouGov UK) September 07, 2021 707-43-10/Polls More Than Two In Five Think Christmas Will Be Free Of Pandemic

Restrictions

News has broken that the government could be planning an October

lockdown – despite the promise that the lifting of pandemic

restrictions in July was “irreversible”. According to reports, the October lockdown could be implemented if

COVID-19 hospitalisations

continue at their current rate and overwhelm the NHS - something the

government has since denied. However,

most people (57%) predict that October 2021 to January 2022 will see fewer

hospitalisations than the same period a year ago – a period that encompassed

the bulk of the UK’s second wave. Yet some 31% of people think that this year

could be on par (16%) or worse (15%) than the previous period in terms of

people admitted to hospital. Approaching two thirds of the public (63%) think there will be fewer

deaths during this time than there were last winter, while 14% think the

death rate will be the same. One in eight (12%) think the coming winter could

bring a higher death toll. While people mostly think hospital admissions and deaths will

decrease, a third of Britons (36%) expect the number of COVID-19 cases to be

higher between October 2021 and January 2022 than the same time last year –

this includes one in eight (12%) who think cases will be “much higher”.

Another 28% of people think case numbers will be about the same. Only a

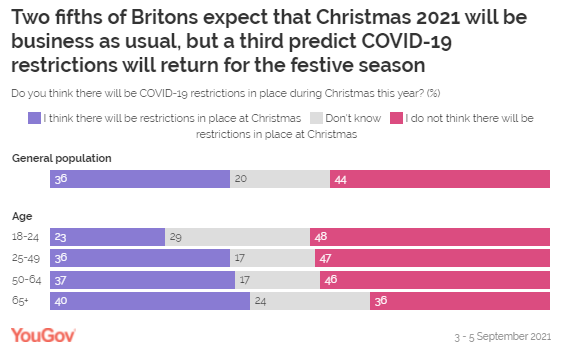

quarter of the public (26%) think that number of infections will be lower. Britons tend to think Christmas will be

free of lockdown restrictions It has been suggested that the so-called “firebreak lockdown” could

see the October

half-term extended, but makes no mention of what might happen later in

the year. Two fifths of Britons (44%), however, are expecting a Christmas

period free of pandemic restrictions. On the other hand, a third (36%) think

there will be some COVID-19 restrictions in place for the festive period once

again. Those aged 65 and above are the least likely to think Christmas will

be business as usual without restrictions (36%), but another 40% think there

will be some rules in place for the festive holiday. On the other hand, those

aged between 18 and 24 are the most hopeful of a restriction-free Christmas

(48%) with around a quarter (23%) thinking at least some form of rules will

be in place. (YouGov UK) September 08, 2021 707-43-11/Polls Twenty Years On, 80% Of Britons Still Remember Where They Were On

9/11

Two decades have passed since terrorists brought down the Twin Towers

in hijacked planes in an unprecedented attack on the US, killing nearly 3,000

people. A new YouGov survey now shows that 80% of Britons can still remember

where they were when they heard the news of the incident. Only one in ten

people (10%) can’t remember their whereabouts when hearing the news, while

another 8% were too young or not yet born. Britons aged 50 to 64 are the most likely to remember the day, with

93% saying it’s still fresh in their memory. Among 18-24-year-olds, 7%

remember where they were when they first heard about the attacks, despite the

oldest people in this group having been only four years old at the time. Fewer Britons believe 9/11 changed the

world completely than ten years ago While a large share of the public are convinced that the world was

not the same after 9/11, this number of those believing it became radically

different has fallen over time. Two fifths of Britons (42%) say the terrorist

incident “changed the world completely” – down from 53% a decade ago. Another

45% believe it changed it “a little”, which is slightly higher than in 2011,

at 38%. Only one in twelve people either say it did not change very much (6%)

or not at all (2%), which is similar to previously (5% not very much, 2% not

at all). Three in five Britons (59%) likewise say that the 11 September

attacks have had a larger impact on the world than the 2007-08 global

financial crisis, a similar figure to the number who said so in 2018 (54%) on

the 10th anniversary of the crisis. Around three in ten

people (30%) currently believe the financial crisis – which until the

coronavirus pandemic had been the worst recession since the 1920s – had a

greater impact (from 32% in 2018). Conservative voters are slightly more likely than Labour members to

say the 9/11 attacks had a larger impact on the world at 65% vs 54%. But while many people still vividly remember hearing about the

attacks, and several terror incidents having happened in the UK since, few

Britons fear for their safety in this context. Some 8% of the public believe there’s a ‘very’ (1%) or ‘fairly’ (7%)

high chance they or someone close to them would become injured or killed in a

terrorist attack. This is similar to both in 2011 (1% very high, 6% fairly

high) and 2006 (2% very high, 6% fairly high). While the proportion of people who feel the odds are high remains the

same, fewer people now say the possibility is ‘almost non-existent’ or ‘very

low’ than previously.

In 2006 and 2011, one in four Britons (25%) believed there was

virtually no chance they or a loved one could become a victim of terrorism,

while another 29-30% felt the chance was very low. Today, only a fifth (18%) regard the possibility as near

non-existent, while a quarter (24%) see it as very low. Instead the most

common answer is ‘fairly low’ at 36% - 5-6 points higher than in 2011 and

2006. (YouGov UK) September 09, 2021 707-43-12/Polls 55% Of Arsenal Supporters Interviewed With Yougov Direct Said They

Were Confident In The Team

A new YouGov Direct survey of Premier League fans reveals that the

opening weeks of the 2021/22 season have already prompted big swings in the

opinions of supporters. Using YouGov Direct, we

interviewed the same group of fans twice, once before the season in

mid-August, and again during the international break, to see how the start of

the season has affected attitudes. Are fans confident in their team and

manager? Arsenal have had a rough start to the 2021/22 season, with three

back-to-back losses sending them to the bottom of the table. As a result,

confidence among Gunners fans has taken a significant dive. Before the season

kicked off, 55% of Arsenal supporters interviewed with YouGov Direct said

they were confident in the team. This figure has since dropped 27pts to just

over a quarter (28%). This trend is not limited to Arsenal, with fans of

several other teams having lost a lot of faith, including Leeds United (79%,

down 14 pts from pre-season) and Leicester City (84%, down 13pts).

For others, however, it is quite the opposite. Tottenham Hotspur have

seen three consecutive winners under new boss Nuno Espírito Santo. This

winning streak, as well as successfully retaining key striker Harry Kane for

the foreseeable future, could be behind the 20pt rise in confidence in the

team. Some 80% of Spurs fans interviewed are now confident in the team,

compared to 60% of the same group before the season began. Everton too has

seen a 20pt boost in confidence, rising from 41% to 61% off the back of two

wins and a draw in the first three games of the season. Of the other teams in the league, Liverpool, Chelsea, and Manchester

City all tie for the highest level of confidence, with 92% of fans for each

team being confident in their squads. They are closely followed by 90%

of Manchester United fans. Newcastle United fans are the least confident, at

just 14%. It is a similar story when fans were asked about their club’s

manager. Unsurprisingly, confidence in Nuno Espírito Santo among Tottenham

fans YouGov interviewed grew from 64% to 83% following his successful opening

campaign, including nearly a quarter who are now “very confident” in Nuno

(24%). The opposite is true for Arsenal his rival, Mikel Arteta. Following a

poor start to the season, confidence among Gunners fans interviewed is down

32pts compared to before the season, with just a third (35%) now holding

confidence in the manager. Some six in ten (61%) of the Arsenal fans YouGov

interviewed are not confident in Arteta’s leadership - including 26% who are

“not at all confident” in their manager. Only Newcastle United manager Steve Bruce receives less confidence.

Just 19% of Newcastle fans interviewed say they have confidence in him,

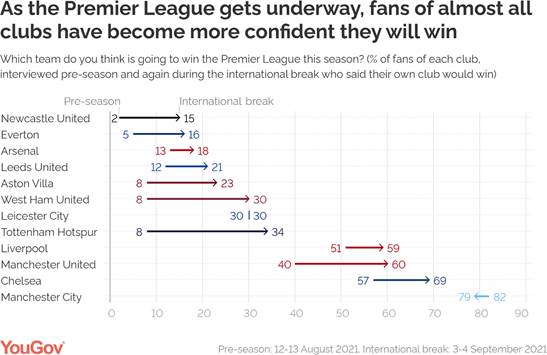

versus 71% who do not. Who will win the league this year? The big question, of course, is whether Manchester City will

make it another back-to-back Premier league win this year. They are the

bookies’ favourite to lift the trophy, but research with YouGov Direct shows

that the proportion of fans predicting another win for Pep Guardiola has

fallen since the start of the season. Overall, 32% of fans interviewed pick City as the winner, down 18pts

from 50% before the season began. Elsewhere, 19% say Chelsea are the likely

victors, up 7pts since the beginning of the season. Another 17% think that

Manchester United could secure their first Premier League win since Sir Alex

Ferguson left the club – also up 7pts since August. Following their strong start to the season, the proportion of Spurs

fans saying thinking Tottenham stand a chance of winning has risen an

additional 27pts on the pre-season survey – the biggest increase among the

teams surveyed. Tottenham fans are now split between 34% who think Spurs

could win, and 32% who think Manchester City will again. Elsewhere fans of teams also jostling for the top spot back

themselves, including 69% of Chelsea fans who think Chelsea will win – up

12pts from 57% in August. Six in ten (60%) Manchester United fans back

themselves, 20pts more than did so before the season began, and 59% of

Liverpool fans think Liverpool will win, increasing 8pts versus pre-season.

Some 15% of Newcastle fans think the Magpies could bring it back for

a win, up from 2% before the season. Hopes have risen among nearly all teams,

in fact, even among Arsenal fans. Some 18% now say that Arsenal will win the

Premier League this season, up 5pts from 13% in August. Manchester City supporters are the most confident they will win (79%)

– however they are the only team to see a decrease in confidence following

the start of the season. Before the season, 82% predicted a City win. Who is expecting a top four finish? Beyond the trophy, there are four Champion’s League spots up for

grabs for the top four teams, and while there are clear favourites among fans

YouGov interviewed, there is sure to be stiff competition. Some 96% of

Liverpool fans interviewed are confident in a top-four position, as are 93%

of United supporters, 92% of Manchester City fans, and 91% of Chelsea fans.

Elsewhere, some 65% of Leicester supporters think they could pinch a top-four

spot, although this is down 10pts since the beginning of the season. Emboldened by early victories, nearly two-thirds of Spurs fans

interviewed think Tottenham could see a return to the Champion’s League this

year. This represents an increase of 23pts from mid-August. At that time,

most fans (55%) had instead been predicting a mid-table finish. Just one in eight Arsenal fans (13%) are confident they will finish

among the top four, down from 33% in mid-August, with the majority (60%)

now expecting a mid-table finish. However, nearly a quarter (23%) expect to

be near the bottom of the table by the end of the season. Newcastle United fans do not hold out high hopes for the 2021/22

season either: 25% fear relegation is likely for the team this year, up from

5% before the season began. Some 60% expect to finish towards the bottom of

the table, a figure largely unchanged from pre-season, while the 30% who

initially thought a mid-table finish was possible has since dropped to

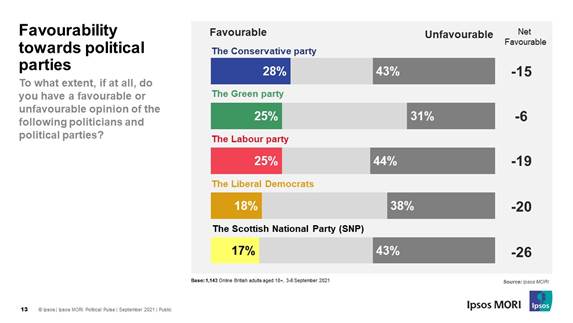

only 10%. (YouGov UK) September 09, 2021 707-43-13/Polls 4 In 10 Britons Think Country Heading In Wrong Direction But Johnson

Much More Popular Than Starmer Among Their Own Voters

Ahead of party conference season, a new Ipsos MORI poll of Britons

aged 18+ (taken before the recent NI announcement) shows that 44% of Britons

think things are heading in the wrong direction (no change from July) and 29%

think things are heading in the right direction (-1 point). The data shows a

predictable party split on this measure with 48% of 2019 Conservative voters

saying things are heading in the right direction compared to 64% of Labour

voters saying things are heading in the wrong direction. Favourability towards parties Roughly equal numbers of Britons are favourable towards the two main

political parties with more Britons being unfavourable than favourable for

both:

More Britons are unfavourable towards Prime Minister Boris Johnson

and Labour leader Keir Starmer than are favourable but Johnson enjoys higher

favourables than Starmer as Conservative voters feel warmer to him than

Labour voters do to Starmer.

Impact of Brexit

Commenting on the findings, Ipsos

MORI Research Director Keiran Pedley said As we approach party conference season

neither the Conservatives nor Labour enjoy a particular strong brand

position, with more Britons negative than positive about both. However,

Johnson goes into his conference in a stronger position than Starmer, with

Conservative voters more positive about the Prime Minister than Labour voters

are about their leader. Whether this remains to be the case as the row over

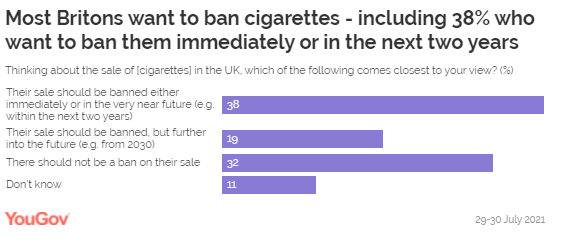

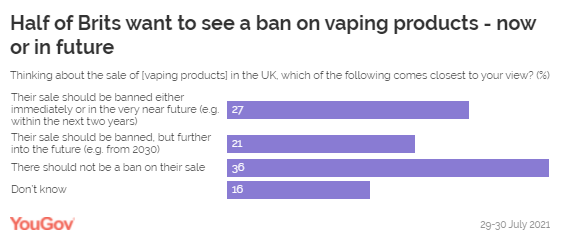

National Insurance and Social Care rumbles on is still to be determined. (Ipsos MORI) 10 September 2021 Source: https://www.ipsos.com/ipsos-mori/en-uk/4-in-10-britons-think-country-heading-wrong-direction 707-43-14/Polls Most Britons 57% Want To Ban Cigarettes – And Half Want To Ban Vaping

Products

The global tobacco firm Philip Morris International (PMI) recently

announced its support for a nationwide

ban on the sale of cigarettes within a decade. The Marlboro maker also

indicated that it would withdraw its own cigarette brands from UK shelves in

the same timeframe. It’s a move that’s broadly in tune with public sentiment: new polling

from YouGov shows that close to three in five Britons (57%) support an

outright ban on the sale of cigarettes, compared to a third (32%) who do not.

And while one in five (19%) are in favour of a ban from 2030 onwards, two in

five (38%) want the government to move even faster – outlawing these products

either immediately or in the near future.

PMI CEO Jacek Olczak says that government action would “end the

confusion” around “smoke-free alternatives” such as e-cigarettes, which the

Benson & Hedges manufacturer will emphasise as it attempts to evolve into

a “healthcare and wellness” company. But our research shows that Britons also tend to favour banning

vaping products: a quarter (27%) of the public would remove them from sale as

soon as possible, while a fifth (21%) would ban them from 2030 onwards.

Overall, half are in favour of a nationwide vape escape (48%) – now or later

– while just over a third are opposed (36%).

While an outright ban on smoking and vaping may not be on the cards

just yet, recent

reports suggest that the government is considering raising the legal age of

buying tobacco to 21 – and outlawing the sale of flavoured

e-cigarettes entirely. (YouGov UK) September 10, 2021 NORTH

AMERICA

707-43-15/Polls Ahead Of The COVID-19 Recession The Unemployment Rate Was Below 4%

Despite the severity of the shock

to the U.S. labor market from the coronavirus

pandemic, the earnings of employed workers overall were largely

unaffected by the pandemic. Inequality in earnings did rise during last

year’s recession, if the unemployed are assumed to

have had no compensation. Even so, the spike was relatively short-lived, in

keeping with the record

low duration of the recession, according to a new Pew Research

Center analysis of government data.

Earnings overall have held steady through the pandemic in part

because lower-wage workers experienced steeper job

losses. Thus, the typical employed worker in 2020 earned more than the

typical employed worker in 2019. A slowdown

in inflation in 2020 benefited all workers, boosting the purchasing

power of their earnings. While unemployed workers lost their earnings, at

least some relief came through unemployment

insurance, a federal package known as the CARES Act and a moratorium

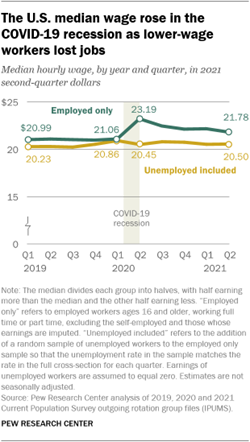

on residential evictions. The median wage of employed U.S. workers had held steady at about $21

per hour for several calendar quarters before the coronavirus outbreak. With

the unemployment rate hovering below 4% ahead of the COVID-19 recession, even

if unemployed workers were included – at zero earnings – there was little effect

on the estimated median wage, nudging it down to about $20 in 2019, but no

more. (Wages are adjusted for inflation and expressed in 2021 second-quarter

dollars.) As the pandemic struck, lower-wage workers proved most likely to

experience a job loss. The shift toward higher-wage workers among the

employed helped to raise the median hourly wage to $23 in the second quarter

of 2020. The median wage of all workers, including the unemployed, remained

unchanged at about $20 per hour, likely because many workers who lost their

job already earned less than the median. The median wage for employed and unemployed workers combined has

remained about the same since the end

of the recession in April 2020. But the median wage among employed

workers alone has drifted down since the second quarter of 2020 as the

unemployment rate dropped and lower-wage

jobs were partially restored. In the second quarter of 2021,

employed workers’ median wage stood at about $22 per hour. It is possible

that it may decrease further as employment in lower-wage jobs returns to

pre-pandemic levels.

Although the change in the composition of employed workers toward

higher-wage workers clouds the picture of how earnings have evolved during

the pandemic, it is possible to gain insight by focusing on the change in

earnings for the same workers

over time. Federal household survey data used

in this analysis records the earnings of many workers at two points in time a

year apart. The sample of employed workers matched over time is a subset of

the overall sample, which varies with the addition and departure of some

survey respondents. It offers another view of how earnings changed during the

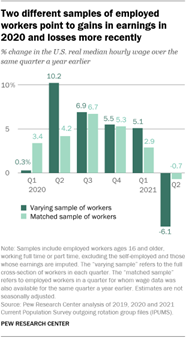

COVID-19 recession and afterward. The median wage of the varying sample

of employed workers – the full cross-section of workers by quarter – had

risen to $23.19 in the second quarter of 2020. This represented an increase of

10.2% over the median wage in the second quarter of 2019. The median wage for

the matched sample of

employed workers – the same workers over time – also increased over this

period, from $23.15 to $24.12, or by 4.2%. While both samples point to higher

earnings in 2020 despite the onset of the pandemic, the much greater increase

in the varying sample points to the sizable role played by the loss of

lower-wage jobs in driving up the increase in the median. Regardless of the sample, the earnings of employed workers in 2020

remained higher than in 2019, albeit less so with the passage of time. As the

unemployment rate fell, the initial rise in the median wage of the varying

sample of workers moderated through the course of 2020. By the fourth quarter

of 2020, the earnings of employed workers in either sample were about 5.5%

higher than in the fourth quarter of 2019. Nonetheless, despite the pandemic

and an economic slowdown, most workers saw higher earnings in 2020.

Those gains proved fleeting, however. In the first quarter of 2021,

the median wage of the matched sample of workers stood 2.9% higher than their

wage in the first quarter of 2020. But, by the second quarter of 2021, the

median wage of the matched sample was 0.7% less than it was a year earlier, and the median wage

of the varying sample had fallen by 6.1%. The larger decrease for the varying

sample is driven again by the changing composition of employed workers, this

time shifting toward lower-wage workers. The recent decline in wages, adjusted for inflation, is also partly

due to an acceleration in the growth in U.S. consumer prices in 2021.

Previously, consumer

prices increased 1.4% from 2019 to 2020, compared with 2.3% from

2018 to 2019. This helped sustain higher earnings for workers in 2020.

However, inflation

has ticked up recently, with consumer prices registering an increase of

4.8% in the second quarter of 2021 compared with the second quarter of 2020.

Thus, the earnings of workers have eroded in recent months, including for the

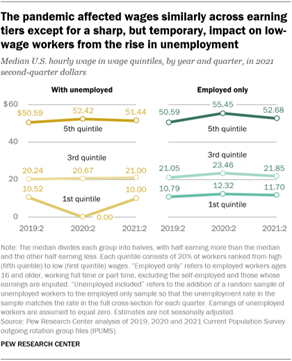

matched sample of workers. Earnings changed similarly for high- and

low-wage workers from 2019 to 2021, leaving inequality unaffected The earnings of low-wage workers – those in the first quintile of

earners – and high-wage workers – those in the fifth quintile of earners –

evolved similarly from 2019 to 2021. The sole exception is the drop in the

median wage of the first quintile of earners in 2020 when the unemployed are

retained in the sample. Among the employed, the median wage of low-, middle- and high-wage

workers all increased in the second quarter of 2020, followed by a gentle

decline. Over the two-year period from the second quarter of 2019 to the

second quarter of 2021, the median hourly wage of high-wage workers increased

from $50.59 to $52.68 and the median for low-wage workers increased from

$10.79 to $11.70. Overall, wages for the three earning tiers of employed

workers are slightly higher in 2021 than in 2019.

Including the unemployed in the sample has a dramatic effect on the

median earnings of low-wage workers, but relatively briefly. The median

hourly wage of these workers fell from $10.52 in the second quarter of 2019

to $0.00 in the second quarter of 2020, followed by a rebound to $10.00 in

the second quarter of 2021. As the U.S. unemployment rate reached near 13% in

the second quarter of 2020, the unemployed – with zero earnings – comprised a

majority of low-wage workers. Thus, the median wage of this group plunged to

zero amid the recession, but then increased with the restoration of jobs.

With the impact on the median earnings of low-wage workers being of limited

duration, the pandemic also does not seem to have left a lasting imprint on

income inequality. In 2019, the median earnings of low-wage workers were

about 20% of the median earnings of high-wage workers. Among employed

workers, this ratio budged little through the recession and in the period

since, with low-wage workers earning 22% as much as high-wage workers in the

second quarter of 2021. Including the unemployed shows the potential for a widening of income

inequality at the start of the pandemic. In the second quarter of 2020,

low-wage workers earned nothing (0%) at the median compared with high-wage

workers – or any other group, for that matter. But the wage ratio increased

to 16% by the third quarter of 2020 and had ascended to 19% by the second

quarter of 2021, comparable to the levels in 2019. Overall, what happened to wage inequality during the COVID-19

recession depends to a large degree on what truly happened to the financial

resources of unemployed workers. If the loss in wages was

replaced by unemployment insurance, supplemental relief under the

CARES Act, or by other

means, there may have been no change in income inequality. But inequality

may yet widen in the near future. Some 39% of the unemployed had been without

work for six

months or longer in July 2021. Evidence shows that these workers are

likely to experience

a loss in earnings as they find new jobs. Meanwhile, there is no

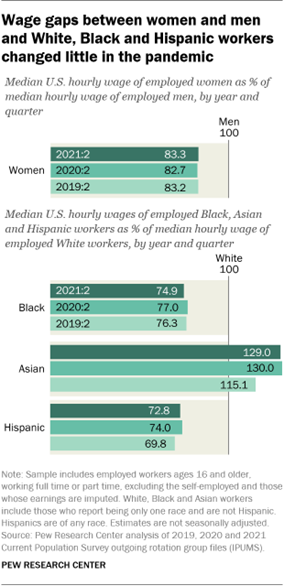

guarantee of financial relief from the government beyond September. Inequality also manifests itself in the form of wage gaps between men

and women and across racial and ethnic groups. Although unemployment

initially increased more among women – to 14.1% in the second quarter of 2020

compared with 12.1% among men – it has fallen more quickly since, according

to government

estimates. The difference in the unemployment rate for women (5.7%) and

men (6.1%) in the second quarter of 2021 is relatively small, as was the case

before the pandemic. Likewise, there was virtually no movement in the gender

wage gap, with employed women earning 83.3% as much as employed men at the

median in the second quarter of 2021, about the same as in 2019. Indeed,

the gender

wage gap has held steady at this level since about 2005.

The earnings of employed Black and Hispanic workers relative to the

earnings of employed White workers have also changed little during the

pandemic. In the second quarter of 2021, Black workers earned 74.9% as much

as White workers at the median, compared with 76.3% in the second quarter of

2019. For Hispanic workers, this ratio edged up from 69.8% to 72.8% over the

same period. The most notable change was among Asian American workers, who

have historically

earned more at the median than other racial and ethnic groups. In

the second quarter of 2019, employed Asian workers earned 115.1% as much as

employed White workers. This ratio jumped to 130.0% in the second quarter of

2020 and has since remained at about that level. But the changes in relative earnings, especially for Asian workers,

need to be viewed with caution. In the second quarter of 2021, the

unemployment rate among U.S. Asian workers was 5.6%, more than double its

level of 2.3% in the second quarter of 2019. The proportional increase in the

unemployment rate – or in the number unemployed – for other racial and ethnic

groups has been much less. This suggests that the composition of employed

Asian workers may still lean more towards higher-wage workers than the composition

of other employed workers. Moreover, the median wage of Asian workers may be affected more than

the median for other workers by the shift in who is employed. That is because

the income ladder among Asian Americans is the steepest, with wide gaps

in income among origin groups and more

income inequality than among other groups. Since job losses by

lower-wage workers essentially push the median wage up the earnings ladder,

the group with the steepest ladder – Asian workers – is likely to have seen

the biggest increase. If the unemployed are included in the analysis, the estimated

increase in the earnings of Asian workers relative to the earnings of White

workers from 2019 to 2021 is cut in half. Instead of increasing by 14

percentage points – from 115.1 in 2019 to 129.0 in 2021 – the increase with

unemployed workers included is 7 points. But including the unemployed has no

effect on the estimated change in the earnings of Black and Hispanic workers

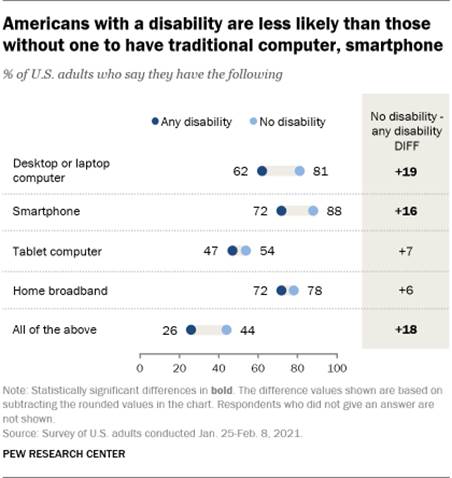

relative to the earnings of White workers. (PEW) SEPTEMBER 7, 2021 707-43-16/Polls 62% Of Adults With A Disability Say They Own A Desktop Or Laptop

Computer

More than 40 million people in the United States have a disability,

according to the U.S.

Census Bureau. But even as majorities of these Americans report having

certain technologies, the digital divide between those who have a disability

and those who do not remains for some devices.

Some 62% of adults with a disability say they own a desktop or laptop

computer, compared with 81% of those without a disability, according to a Pew

Research Center survey of U.S. adults conducted Jan. 25-Feb. 8, 2021. And

when it comes to smartphone ownership, there is a gap of 16 percentage points

between those with a disability and those without one (72% vs. 88%). Despite these gaps, similar shares of Americans – regardless of

disability status – say they have broadband at home or a tablet computer. For

example, 72% of adults with a disability report having high-speed internet at

home, a figure that does not differ statistically from the 78% of adults

without a disability who say the same. And there is no statistically

significant difference in tablet ownership between adults who report having a

disability (47%) and those who do not have a disability (54%). There is, however, variation by disability status when considering

ownership of all these

devices that enable people to go online. Roughly a quarter of Americans with

disabilities (26%) say they have high-speed internet at home, a smartphone, a

desktop or laptop computer and a

tablet, compared with 44% of those who report not having a disability.

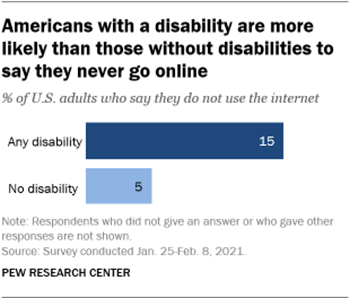

Whether or not someone goes online also varies by disability status.

Americans with disabilities are three times as likely as those without a

disability to say they never go online (15% vs. 5%). And while three-quarters

of Americans with disabilities report using the internet on a daily basis,

this share rises to 87% among those who do not have a disability. Overall, roughly one-in-five U.S. adults (18%) report that they have

a disability, according to this survey, which asked respondents if any

“disability, handicap, or chronic disease keeps you from participating fully

in work, school, housework, or other activities, or not.” (It is important to

note that there are various forms of disabilities, often differing in

severity, and a range of ways to measure disability in public opinion

surveys.) Older Americans are more likely than younger adults to report having

a disability. At the same time, these older age groups generally have lower

levels of digital adoption than the nation as a whole. There are tools on the market aimed at making the digital experience

more accessible to Americans with disabilities. For example, a new search

engine is in the works to help those with disabilities find websites

that are accessible to them. And social media companies have experimented

with artificial

intelligence to help the visually impaired use their platforms,

while other companies are expanding their screen-reading

software and mobile apps. At the same time, there have been many

lawsuits over the years claiming some websites are not accessible to

those with disabilities. (PEW) SEPTEMBER 10, 2021 707-43-17/Polls 46% Of Canadians Who Say They Are Going To Support A Party On

Election Day Are Absolutely Certain Of Their Vote Choice

According to a new Ipsos poll conducted on behalf of Global News,

only 46% of Canadians who say they are going to support a party on election

day are absolutely certain of their vote choice, leaving the remaining voters

less sure (39% fairly certain; 11% not very certain; 4% not at all certain).

Conservative voters (49%, +3 since the start of the campaign) and Liberal

voters (49%, +1) are most likely to be absolutely certain of their choice,

with NDP (43%, +6), Bloc (43%, +13) and Green Party (26%, +13) supporters

less certain of their choice. The NDP appears to have the most room to grow their vote between now

and September 20th. Among those voters who express a first-choice party, 22%

say they’d choose to vote for the NDP as their second choice. This contrasts

with the Liberals (15%), Conservatives (11%), Greens (11%), PPC (7%), Bloc

(3%) or some other party (3%) as preferred second choices. Three in ten (28%)

voters don’t know who they would choose second, led by Conservative voters,

37% of whom wouldn’t identify a preferred second choice. This suggests that

Conservative voters are least likely to be considering a second party. Two thirds (67%) of Canadians say they are completely certain they

will vote in this election. Looking at this intention by party support

reveals no clear turnout advantage for any party: NDP (69%), Conservative

(68%) and Liberal (67%) voters are equally likely to say that they are

certain to vote on or before E-Day. Bloc (63%) and Green (44%) voters are

less enthusiastic about voting. The campaign has clearly had an impact on who Canadians are

considering voting for. Reflecting their positive momentum in the horserace

figures since the start of the campaign, the Conservatives and NDP have

increased their appeal among a greater number of voters than the other

parties. Conversely, vote consideration for the Liberals, Bloc and Green

Party has been decidedly negative. The chart below shows the proportion of

Canadians who say they have become more or less likely to vote for each party

since the start of the campaign, with the change in consideration since last

week in brackets.

Canadians acknowledge the broader trend that Ipsos has been measuring

in its recent polls: one in three (34%) believe the Conservatives have been

gaining the most popularity and momentum over the coming weeks (up 10 points

since last week), while one in four (24%, +7) say it is the NDP who has been

gaining the most strength. Just 17% (-5) believe that it is the Liberals who

are on a roll. In fact, even Liberal voters believe they’re stalling, as just

39% believe they are the party with the most momentum, far behind the

proportion of Conservative (72%) and NDP (67%) voters who say their own party

is gaining the greatest traction in the campaign. Despite this momentum, Canadians still believe the Liberals are the

favorite to win the election, although those odds are less certain than

before. Four in ten (38%) Canadians believe the Liberals will win (down 6