|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 709 Week:

September 20 –September 26, 2021 Presentation:

October 01, 2021 Urban

Indians Look Forward To A Golden Diwali, With Nearly Three In Ten Planning To

Spend On Gold Hindus

Made Up 79.8% Of India’s 1.2 Billion (120 Crore) Total Inhabitants In The

Most Recent Census 72%

Of Afghans Reported Lacking Money For Food In 2019, An All-Time High More

Than Half (52%) Of The UK Public Know Someone Who Has Been Diagnosed With

Dementia Manchester

United Is The Best-Supported Premier League Club In The UK, But There’s Close

Competition One

In Eleven Say The Coronavirus Act Should Be Made Permanent 54%

Of French People Believe That The School System Works Poorly In

U S, An Estimated 18 Million Can't Pay For Needed Drugs Half

Of Americans Said Their Area Had Experienced Extreme Weather Over The Past

Year US

Hispanic Population Reached More Than 62 Million In 2020 Fewer

Than Half Of U S Adults (44%) Now Approve Of The Way Biden Is Handling His

Job As President Majority

Of Australians 76% Report Unwavering Support For Abortion Access A

Median Of 79% Across 16 Publics Have A Favorable Opinion Of Germany In

Six Of 13 Countries, Online Lottery Is The Most Popular Online Product INTRODUCTORY NOTE

709-43-23/Commentary:

Urban

Indians Look Forward To A Golden Diwali, With Nearly Three In Ten Planning To

Spend On Gold

With the

festive season around the corner, YouGov’s Diwali Spending Index, an

indicator of spending propensity, reveals a recovering appetite to spend

during festive season among urban Indians. At 90.71,

the spending intent is higher than last year (80.96), however, it is yet to match

the pre-pandemic times. When asked

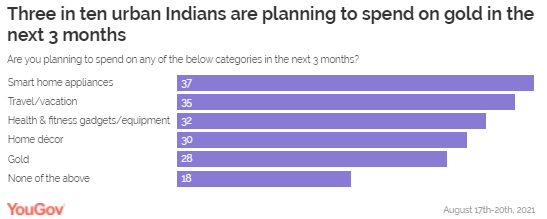

about where they are planning to spend in the next three months, nearly two

in five urban Indians claimed they are likely to spend on smart home

appliances (37%). Following this, roughly a third said they would be spending

on travel (35%) or health and fitness gadgets (32%). Almost three

in ten urban Indians (28%) are planning to spend on gold in the next 3

months. Millennials were most likely to say this as compared to the rest of

the generations, at 36%. Furthermore,

seven in ten (69%) of these prospective gold buyers agreed with the

statement, "Diwali and the

festive season is the best time to buy gold", highlighting

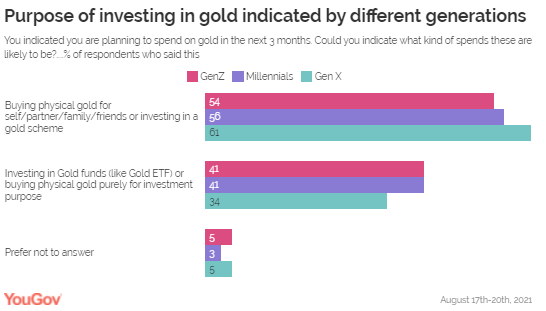

their inclination to spend during the festive season. Our data

suggests out of those looking to spend on gold in the near future, nearly

three in five respondents (58%) are planning to buy gold for personal/family

use either in physical gold form or through a gold scheme (like Tanishq Gold

Harvest Plan). The

remaining (38%) are likely to spend on the yellow metal for the purpose of

investment either through gold funds or in physical gold form. Among the

generations, the GenX are somewhat more likely than GenZ and millennials to

buy gold for personal use (61% GenX vs 56% millennials and 54% GenZ) while the

younger adults are more likely than their predecessors (41% millennials and

GenZ vs 34% GenX) to invest in gold this festive season. When we look

at this across regions, we see that respondents in South India are more

likely to buy gold for personal use while North Indians are keener to invest

in gold this festive season. Those buying

gold for personal use are most likely to buy it from branded jewellery stores

(56%), followed by local jewellers (36%). For investors, buying gold from

branded jewellery stores is the most likely option (23%), but it is closely

followed by investments through online trading apps or through banks (21%

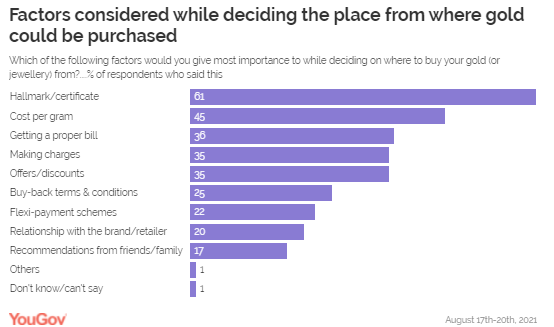

each). Hallmark or

certificate is the most important consideration factor when deciding where to

buy gold from (61%), followed by the cost per gram (45%) and a proper bill

for the purchase (36%). Flexi-payment schemes (22%), relationship with the

brand or retailer (20%) and recommendations from friends are family (17%) are

far less important to consumers. Hallmark/

certification and offers or discounts are notably more important in East

India (at 71% and 50% respectively) while making charges appeal more to South

Indians (at 46%) than the rest of the population. Similarly,

recommendations from friends and family are notably more important to men

than women (24% vs 10%) when deciding where to buy gold from. When asked

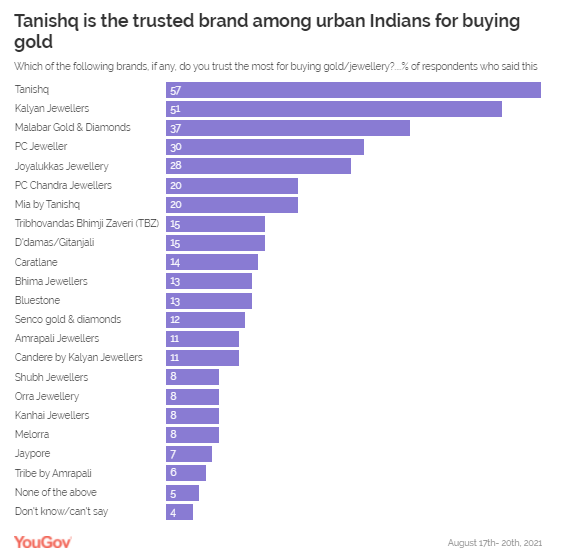

which brands do they trust the most for buying gold, a majority (57%) named

Tanishq as their most trusted brand. Kalyan Jewellers (51%), Malabar Gold

& Diamonds (37%) and PC Jewellers (30%) are other brands that are trusted

by people when it comes to buying gold. Interestingly,

all these brands appeal more strongly to the millennials than the rest of the

generations. (YouGov

India) September

22, 2021 Source: https://in.yougov.com/en-hi/news/2021/09/22/urban-indians-look-forward-golden-diwali-nearly-th/ 709-43-24/Country Profile:

SUMMARY

OF POLLS

ASIA (India) Urban

Indians Look Forward To A Golden Diwali, With Nearly Three In Ten Planning To

Spend On Gold When asked about where they are planning to

spend in the next three months, nearly two in five urban Indians claimed they

are likely to spend on smart home appliances (37%). Following this, roughly a

third said they would be spending on travel (35%) or health and fitness

gadgets (32%). Almost three in ten urban Indians (28%) are planning to spend

on gold in the next 3 months. Millennials were most likely to say this as

compared to the rest of the generations, at 36%. (YouGov India) September 22, 2021 Hindus Made Up 79.8% Of India’s 1.2 Billion

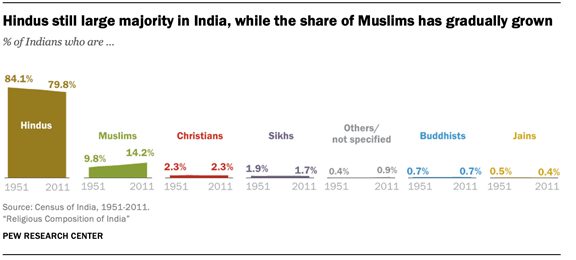

(120 Crore) Total Inhabitants In The Most Recent Census Hindus made up 79.8% of India’s 1.2 billion

(120 crore) total inhabitants in the most recent census, conducted in 2011.

That is 0.7 percentage points less than in the previous census in 2001, and

4.3 points below the 84.1% recorded in 1951. Meanwhile, the share of Muslims

grew from 13.4% in 2001 to 14.2% in 2011 – up by a total of 4.4 percentage

points since 1951, when the census found that Muslims comprised 9.8% of

India’s population. Christians, Sikhs, Buddhists and Jains, who together make

up nearly all of the remaining 6% of the population, were relatively stable

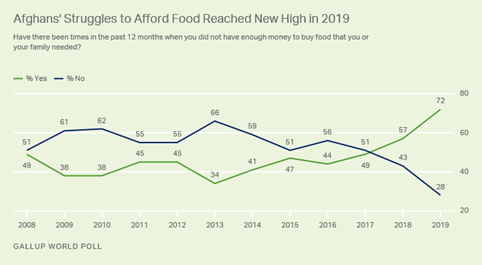

in their shares since the 1951 census. (PEW) SEPTEMBER 21, 2021 (Afghanistan) 72% Of Afghans Reported Lacking Money For Food In 2019, An

All-Time High Gallup World Poll data in recent years have

painted an increasingly difficult economic situation throughout the country

as Afghans have struggled to afford even the basics. In November/December

2019, just before the February 2020 signing of the U.S.-Taliban peace deal,

more than seven in 10 Afghans (72%) reported that there had been times in the

past 12 months when their household lacked enough money for food. This marked

a 15-percentage-point increase from 2018 and a new high since Gallup first

began measuring this item annually in Afghanistan in 2008. (Gallup) SEPTEMBER 23, 2021 WEST

EUROPE (UK) 86% Britons Support The Idea That Government Should Provide

More Information To The General Public About Levelling Up Ipsos MORI’s KnowledgePanel has found that

between March and July 2021, Britons’ awareness of the Government’s Levelling

Up strategy increased. Those knowing at least a little about it rose by

8 points from 48% to 56%, with an equivalent fall in those who know or heard

nothing about it These increases were seen across all regions except the West

Midlands, particularly the North East . (Ipsos MORI) 21 September 2021 More Than Half (52%) Of The UK Public Know Someone Who Has

Been Diagnosed With Dementia Wave 2 of the Monitor has revealed that

more than half (52%) of the UK public know someone who has been diagnosed

with the condition - a figure that remains unchanged since Wave 1. This is

most often a grandparent (17%) or parent (13%). The majority of people (68%)

correctly disagree with the statement ‘dementia is an inevitable part of

getting older’ - up from 60% in Wave 1. The proportion who are unsure whether

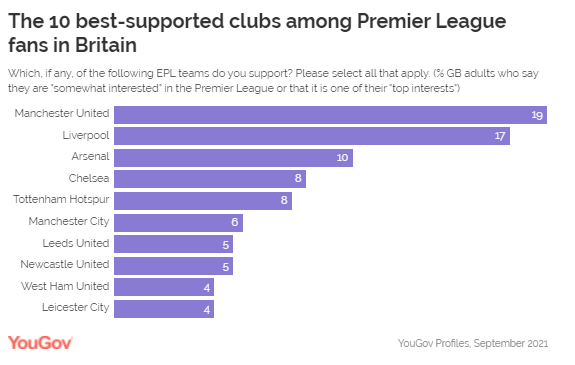

dementia is inevitable has fallen from 17% to 11%. (Ipsos MORI) 22 September 2021 Manchester United Is The Best-Supported

Premier League Club In The UK, But There’s Close Competition Starting off, Manchester United claim the

top spot with Liverpool hot on their heels. Almost a fifth of Premier League

fans in Britain support the Red Devils (19%), while Jurgen Klopp’s team

enjoys support from 17%. While the contest is close at the top of the table,

there is a significant gap between them and the rest. Arsenal come in at No.3

in the support stakes,with one in ten followers of the Premier League saying

they support the Gunners (10%). Chelsea and Tottenham Hotspur are next in

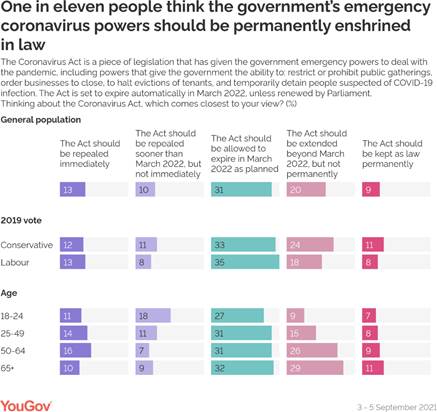

line with 8% of Premier League followers saying they support those clubs. (YouGov UK) September 24, 2021 One In Eleven Say The Coronavirus Act

Should Be Made Permanent New YouGov research shows that nearly three

in ten people think the act should be extended, however. This includes 20% of

people who think the Act should be extended temporarily and 9% who think it

should be permanently enshrined in law. Conservative voters are more likely

to think the Coronavirus Act should be extended or made permanent (35%) than

Labour voters (26%). However, Labour voters are not necessarily more in

favour of repealing the Act early, with a higher proportion unsure (18%) than

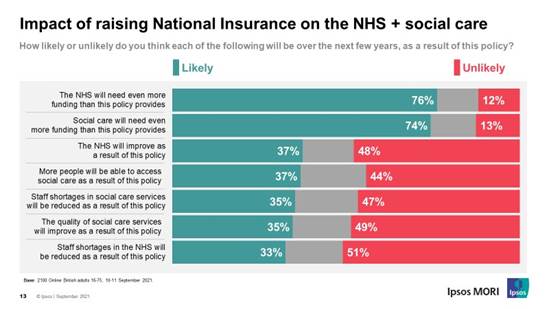

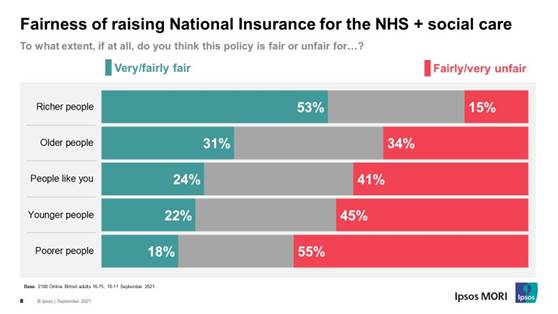

Tories (8%). (YouGov UK) September 24, 2021 Over A Third Say The Quality Of Social Care Is Likely To

Improve As A Result Of The Plan To Raise National Insurance To Help Fund

Health And Social Care Last week, the UK

Government announced a plan to raise National Insurance to help fund health

and social care. Now, new research by Ipsos MORI shows many Britons are split

in their support for the policy, the impact it will have on the NHS and

social care, and how fairly it treats different groups. Just over a

third say the quality of social care is likely to improve as a result of this

policy (35%) while 37% are hopeful for improvement in the NHS. However half

are more sceptical, thinking it is unlikely that the NHS or the quality of

social care will improve (48% and 49% respectively). (Ipsos MORI) 26 September 2021 (France) 54%

Of French People Believe That The School System Works Poorly At first glance, the school system is

primarily associated with the acquisition of skills (55% of French people

associate this notion with it). However, it is also linked to negative

notions such as obligation / constraint and the forbidding aspect

(respectively 42% and 39%). (Ipsos France) 22 September 2021 NORTH AMERICA (USA) In U S, An Estimated 18 Million Can't Pay For Needed Drugs Seven percent of U.S. adults --

representing an estimated 18 million persons -- reported in June that they

were unable to pay for at least one doctor-prescribed medication for their

household during the prior three months, according to the most recent West Health and Gallup survey. This percentage is

in line with the 6% reported in March. Among those in households earning less

than $24,000 per year, however, the percentage has jumped from 10% to 19%, a

statistically significant increase. (Gallup) SEPTEMBER 21, 2021 Roughly A Quarter Of American Adults (23%) Say They Haven’t

Read A Book In Whole Or In Part In The Past Year Adults whose annual household income is

less than $30,000 are more likely than those living in households earning

$75,000 or more a year to be non-book readers (31% vs. 15%). Hispanic adults

(38%) are more likely than Black (25%) or White adults (20%) to report not

having read a book in the past 12 months. (The survey included Asian

Americans but did not have sufficient sample size to do statistical analysis

of this group.) (PEW) SEPTEMBER 21, 2021 Half Of Americans Said Their Area Had Experienced Extreme

Weather Over The Past Year Nearly 5 million NFIP policies were in

force as of July 2021, the most recent month available. That figure hasn’t

varied much for the past few years, though it’s down from a peak of 5.7 million policies at the end of 2009. Flood insurance

is available in over 22,000 communities throughout the country, but it’s

particularly important in states that border the Gulf of Mexico: 60% of all

policies in force, accounting for a somewhat higher share of covered property

value, are in Florida, Texas and Louisiana. (PEW) SEPTEMBER 22, 2021 US Hispanic Population Reached More Than 62 Million In 2020 Of the 42.7 million adults with Hispanic

ancestry living in the U.S. in 2015, an estimated 5 million people, or 11%, said they do not

identify as Hispanic or Latino, according to a Pew Research Center survey

of U.S. adults. These people aren’t counted as Hispanic in Pew Research

Center surveys. The Census Bureau generally takes a similar approach in its

decennial census. Hispanic self-identification varies across immigrant

generations. Among the foreign born from Latin America, nearly all

self-identify as Hispanic. But by the fourth generation, only half of people

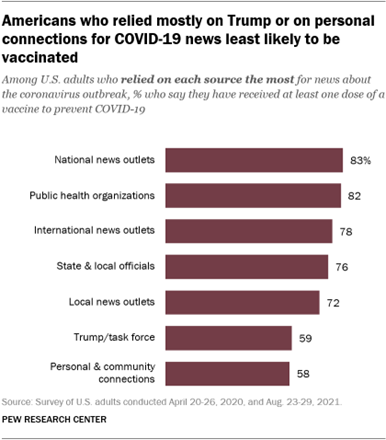

with Hispanic heritage in the U.S. self-identify as Hispanic. (PEW) SEPTEMBER 23, 2021 Roughly Six-In-Ten (59%) Of Those Who Relied Most On Trump

Say They Have Received At Least One Dose Of A Covid-19 Vaccine Those who cited Trump and his task force

and those who cited personal and community networks as their favored COVID-19

news sources are far less likely than those who relied on other source types

to have received at least one shot of the vaccine. Roughly six-in-ten (59%)

of those who relied most on Trump say they have received at least one dose of

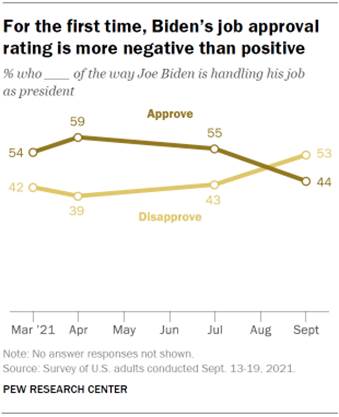

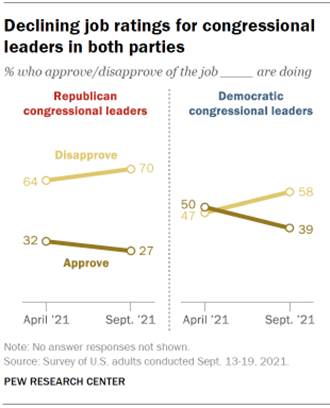

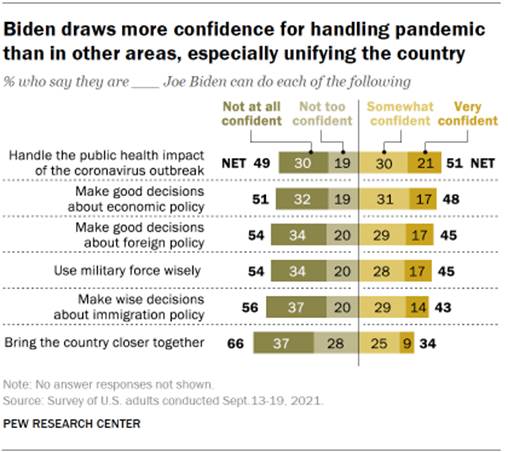

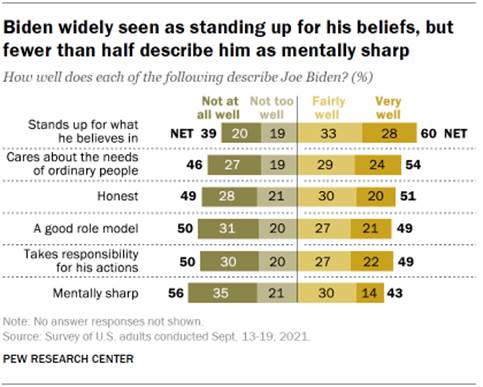

a COVID-19 vaccine, while 38% say they have not received a vaccine. (PEW) SEPTEMBER 23, 2021 Fewer Than Half Of U S Adults (44%) Now Approve Of The Way

Biden Is Handling His Job As President Since spring, public confidence in Biden

has declined across several issues. In March, majorities expressed confidence in him

across six of seven dimensions, including his handling of the public health

impact of the coronavirus, and foreign and economic policies. Today,

about half still express confidence in his handling of the coronavirus and

the economy – but majorities have little or no confidence in him in four

other areas. (PEW) SEPTEMBER 23, 2021 (Canada) 4 Out Of 5 Canadians (83%) Agree That It Is A Priority To

Retain Canada’s Key Capacity To Train Military Pilots Under Canadian Control As the pandemic continues to exert

pressures, Canadians are looking inwards at how best to secure sovereignty

and domestic economic growth. According to a recent survey study conducted by

Ipsos, 4 out of 5 Canadians (83%) agree that it is a priority to retain

Canada’s key capacity to train military pilots under Canadian control.

Sovereignty remains at the forefront of Canadians’ minds, with a near

consensus (92%) agreeing that it is essential to national sovereignty and

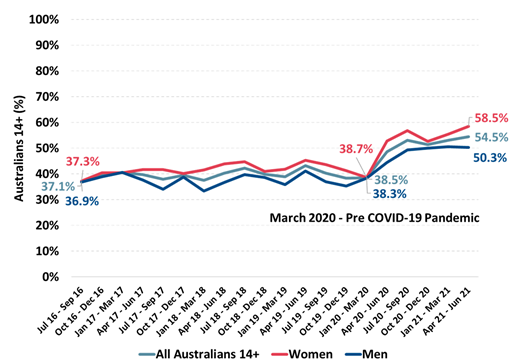

security that Canada retain the training of its military pilots. (Ipsos Canada) 20 September 2021 AUSTRALIA Covid-19 Pandemic Drives Australians To Increasingly ‘Shut

Themselves Off From The Rest Of The World’ When At Home Prior to the pandemic agreement with this

statement had barely changed over the preceding four years, increasing by

just over 1% point since the September quarter 2016. Women have driven a

larger share of this increase since the pandemic began than men. A clear

majority of 58.5% of women agree with the statement in the June quarter 2021,

an increase of 19.8% points from the March quarter 2020 and up over 21%

points from five years ago. (Roy Morgan) September 21 2021 MULTICOUNTRY STUDIES Majority Of Australians 76% Report Unwavering Support For

Abortion Access Seven in 10 Australian adults support

access to abortion, an online study by Ipsos has found. The study, conducted

across 27 countries, also found that global support for access to abortion

has been steadily increasing since 2014, with the largest increases seen in

South Korea and parts of Latin America. In Australia, support for abortion

has remained consistent over the past eight years: 76% supported abortion in

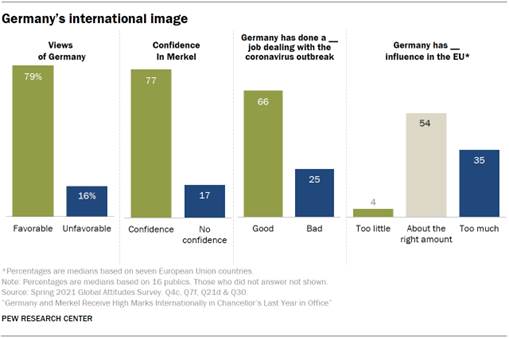

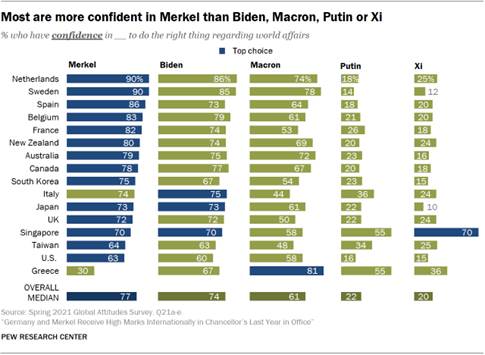

2021, compared to 74% in 2018, and 77% in 2014. (Ipsos Australia) 20 September 2021 Source: https://www.ipsos.com/en-au/majority-australians-report-unwavering-support-abortion-access A Median Of 79% Across 16 Publics Have A Favorable Opinion

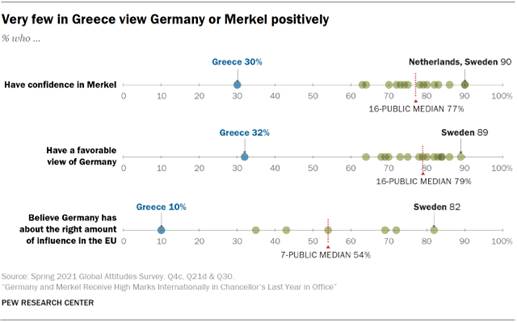

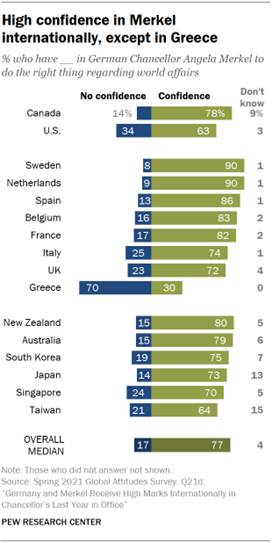

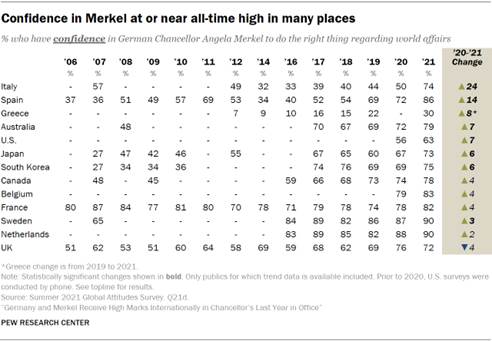

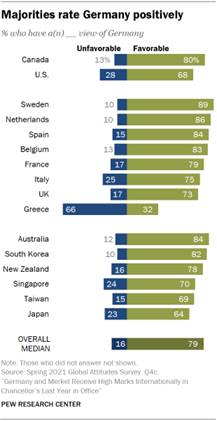

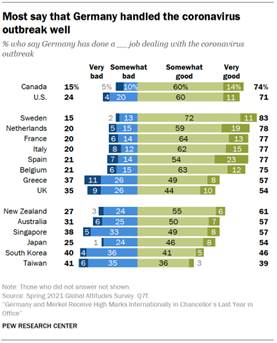

Of Germany Majorities in nearly every public surveyed

have confidence in Merkel to do the right thing in world affairs, including

nine-in-ten in the Netherlands and Sweden. Merkel has enjoyed generally high

ratings in a number of countries since she first took office, with confidence

growing as more people became familiar with her over time. In most places

surveyed, trust in the German chancellor has never been higher. (PEW) SEPTEMBER 22, 2021 Of 28 Countries, Brazil Is The One That Most Believes That

Women In Political Leadership Would Bring Peace To The World More than 7 out of 10 Brazilians believe

the world would be more peaceful and successful if we had more female

political leaders. This is what a survey on global leadership conducted

with respondents from 28 nations, including Brazil, points out. While

72% agree with the statement, 18% disagree and 10% did not know how to give

their opinion on the subject. Of the 28 countries evaluated, in 18 the

percentage that bets on female leaders to bring peace and success to the

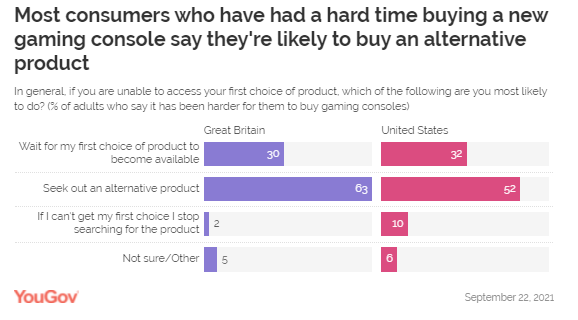

world is greater than or equal to 50%. (Ipsos Brazil) 23 September 2021 Three In Ten Consumers Shopping For

Consoles In Both Britain (30%) And The United States (32%) Say They Are

Willing To Wait For Their First Choice To Become Available The PlayStation 5 and the Xbox Series X

have both been hard to come by. However in some markets, it has been

easier to get the less expensive (but less capable) Xbox series S, which may

give Microsoft’s entry-level offering a competitive advantage. The

latest consoles from Xbox and PlayStation have been elusive to consumers.

Substantial changes to worldwide demand for products during the pandemic

caused a semiconductor shortage. This shortage has been met with increased

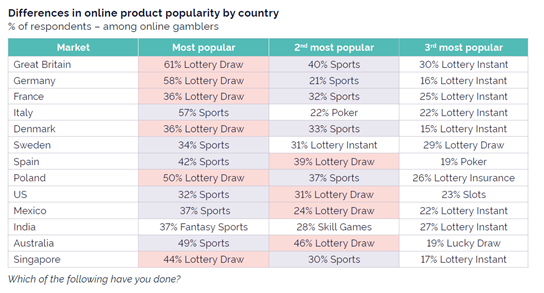

demand for the new console offerings. (YouGov UK) September 25, 2021 In Six Of 13 Countries, Online Lottery Is

The Most Popular Online Product Sports betting in Great Britain remains the

second most popular form of online betting among online gamblers (40%),

behind lottery draws (61%). These new insights are part of a fresh

YouGov whitepaper that delves deep into attitudes and habits around online

gambling in several global markets, including Great Britain and

beyond. The global popularity of lottery products – prize draws or

instant tickets – and sports betting is clear. In six of 13 countries, online

lottery is the most popular online product, and a further four have it as the

second most popular product. (YouGov UK) September 25, 2021 ASIA

709-43-01/Polls Urban

Indians Look Forward To A Golden Diwali, With Nearly Three In Ten Planning To

Spend On Gold

With the festive season around the corner,

YouGov’s Diwali Spending Index, an indicator of spending propensity, reveals

a recovering appetite to spend during festive season among urban Indians. At 90.71, the spending intent is higher

than last year (80.96), however, it is yet to match the pre-pandemic times. When asked about where they are planning to

spend in the next three months, nearly two in five urban Indians claimed they

are likely to spend on smart home appliances (37%). Following this, roughly a

third said they would be spending on travel (35%) or health and fitness

gadgets (32%). Almost three in ten urban Indians (28%) are

planning to spend on gold in the next 3 months. Millennials were most likely

to say this as compared to the rest of the generations, at 36%. Furthermore, seven in ten (69%) of these

prospective gold buyers agreed with the statement, "Diwali and the festive season is the best

time to buy gold", highlighting their inclination to spend

during the festive season. Our data suggests out of those looking to

spend on gold in the near future, nearly three in five respondents (58%) are

planning to buy gold for personal/family use either in physical gold form or

through a gold scheme (like Tanishq Gold Harvest Plan). The remaining (38%) are likely to spend on

the yellow metal for the purpose of investment either through gold funds or

in physical gold form. Among the generations, the GenX are

somewhat more likely than GenZ and millennials to buy gold for personal use

(61% GenX vs 56% millennials and 54% GenZ) while the younger adults are more

likely than their predecessors (41% millennials and GenZ vs 34% GenX) to

invest in gold this festive season. When we look at this across regions, we see

that respondents in South India are more likely to buy gold for personal use

while North Indians are keener to invest in gold this festive season. Those buying gold for personal use are most

likely to buy it from branded jewellery stores (56%), followed by local

jewellers (36%). For investors, buying gold from branded jewellery stores is

the most likely option (23%), but it is closely followed by investments

through online trading apps or through banks (21% each). Hallmark or certificate is the most important

consideration factor when deciding where to buy gold from (61%), followed by

the cost per gram (45%) and a proper bill for the purchase (36%).

Flexi-payment schemes (22%), relationship with the brand or retailer (20%)

and recommendations from friends are family (17%) are far less important to

consumers. Hallmark/ certification and offers or

discounts are notably more important in East India (at 71% and 50%

respectively) while making charges appeal more to South Indians (at 46%) than

the rest of the population. Similarly, recommendations from friends and

family are notably more important to men than women (24% vs 10%) when

deciding where to buy gold from. When asked which brands do they trust the

most for buying gold, a majority (57%) named Tanishq as their most trusted

brand. Kalyan Jewellers (51%), Malabar Gold & Diamonds (37%) and PC

Jewellers (30%) are other brands that are trusted by people when it comes to

buying gold. Interestingly, all these brands appeal more

strongly to the millennials than the rest of the generations. (YouGov India) September 22, 2021 Source: https://in.yougov.com/en-hi/news/2021/09/22/urban-indians-look-forward-golden-diwali-nearly-th/ 709-43-02/Polls Hindus Made

Up 79.8% Of India’s 1.2 Billion (120 Crore) Total Inhabitants In The Most

Recent Census

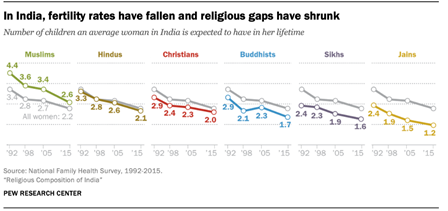

India’s fertility rate has been declining

rapidly in recent decades. Today, the average Indian woman is expected to

have 2.2 children in her lifetime, a fertility rate that is higher than rates

in many economically advanced countries like the United States (1.6) but much lower than India’s in

1992 (3.4) or 1950 (5.9).1 Every religious group in the country has

seen its fertility fall, including the majority Hindu population and Muslim,

Christian, Sikh, Buddhist and Jain minority groups. Among Indian Muslims, for

example, the total fertility rate has declined dramatically, from 4.4

children per woman in 1992 to 2.6 children in 2015, the most recent year for

which religion data is available from India’s National

Family Health Survey.

Muslims still have the highest fertility

rate among India’s major religious groups, followed by Hindus at 2.1. Jains

have the lowest fertility rate (1.2). The general pattern is largely the same

as it was in 1992, when Muslims had the highest fertility rate at 4.4,

followed by Hindus at 3.3. But the

gaps in childbearing between India’s religious groups are generally much

smaller than they used to be. For example, while Muslim women

were expected to have an average of 1.1 more children than Hindu women in

1992, the gap had shrunk to 0.5 by 2015. What do these trends mean for India’s

religious composition? India’s Muslim population has grown somewhat faster

than other religious groups because of fertility differences. But due in part

to declining and converging fertility patterns, there have been only modest changes in the overall

religious makeup of the population since 1951, when India

conducted its first census as an independent nation.

Hindus made up 79.8% of India’s 1.2 billion

(120 crore) total inhabitants in the most recent census, conducted in 2011.

That is 0.7 percentage points less than in the previous census in 2001, and

4.3 points below the 84.1% recorded in 1951. Meanwhile, the share of Muslims

grew from 13.4% in 2001 to 14.2% in 2011 – up by a total of 4.4 percentage

points since 1951, when the census found that Muslims comprised 9.8% of

India’s population. Christians, Sikhs, Buddhists and Jains, who together make

up nearly all of the remaining 6% of the population, were relatively stable

in their shares since the 1951 census.2 Over the decades, population growth rates

have slowed considerably – overall and among Muslims in particular. Before

its steep fertility declines, India was on a trajectory that would have

resulted in a much larger total population, as well as a greater change in

the distribution of religious populations. (See discussion of growth rates

in Chapter 1.) While changes at the national level have

been modest, they have not been distributed evenly across India. Some states

and union territories have experienced faster population growth or larger

changes in religious composition than other states or the country as a whole.

For example, the share of Hindus fell by nearly 6% in Arunachal Pradesh but

rose by about 2% in Punjab between 2001 and 2011. (See Chapter 3 for more information on the religious

demography of India’s states and territories.) India uses a number system that differs

from the international number system. This report presents numbers in the

international system and, in parentheses, the Indian system. The Indian

number system uses units such as lakhs and crores and places commas at

different intervals than the international system. Some examples of

equivalents: International number system vs. Indian

number system One hundred thousand (100,000) = 1 lakh

(1,00,000) These are among the key findings of a Pew

Research Center demographic analysis of data from India’s census and other

sources, designed to complement a major new public opinion survey, “Religion in India: Tolerance and

Segregation,”

published in June 2021. This analysis looks primarily at trends since India’s

independence, which was accompanied by major changes in the country’s

religious demographics. The Partition of 1947, at the end of Britain’s long

colonial rule, divided the Indian subcontinent along religious lines, causing

millions (tens of lakhs) of Muslims to move to the new nation of Pakistan.

Meanwhile, millions (tens of lakhs) of Hindus and members of other religious

groups migrated to the new India (see sidebar below). Migration is one of three main mechanisms,

along with fertility and conversion, that cause religious groups to shrink or

expand. But since the 1950s, migration has had only a modest impact on

India’s religious composition. More than 99% of people who live in India were

also born in India. Migrants leaving India outnumber immigrants three-to-one,

and religious minorities are more likely than

Hindus to leave.

Religious switching, or conversion – when an individual leaves one religion

for another or stops affiliating with any religion – also appears to have had

a relatively small impact on India’s overall composition, with 98% of Indian

adults still identifying with the religion in which they were raised. As a result, statistical analysis of census

and survey data shows that fertility

has been by far the biggest driver of the modest amount of religious change

in the decades since Partition (see Chapter 2 for details).3 Religion is only one of many factors tied

to fertility rates. While this report describes differences in the fertility

patterns of major religious groups in India, it cannot measure the full

impact of historical and cultural factors on these patterns, nor can it

quantify the direct role that religion plays when it comes to fertility and

family size. In India and elsewhere, education is a

primary factor in how many children women tend to have. Other prosperity

indicators – such as life expectancy and average levels of wealth – also

frequently correlate with fertility measures: Women who have better access to

schooling, jobs and health care tend to have fewer children. Population growth is driven not only by how

many children women have, but also by the concentration of women of

childbearing age. Younger populations have more women entering their prime

childbearing years and, as a result, tend to grow faster than older

populations. In addition, where people live within

India, as well as their history and cultural norms (which are harder to

measure), play a role in the choices they make about family matters. In short, people’s religion alone does not determine

how many children they will have. Religion is just part of a

complicated picture. (PEW) SEPTEMBER 21, 2021 Source: https://www.pewforum.org/2021/09/21/religious-composition-of-india/ 709-43-03/Polls 72% Of Afghans

Reported Lacking Money For Food In 2019, An All-Time High

WASHINGTON, D.C. -- Donor countries pledged

more than $1.2 billion last week to ward off an impending humanitarian crisis

in Afghanistan, as U.N. Secretary-General Antonio Guterres warned of

"the collapse of an entire country." There are concerns that rising

hunger and severe drought may compound an already perilous situation in

Afghanistan as the Taliban assert control over the national government for

the first time since 2001. Gallup World Poll data in recent years have

painted an increasingly difficult economic situation throughout the country

as Afghans have struggled to afford even the basics. In November/December

2019, just before the February 2020 signing of the U.S.-Taliban peace deal,

more than seven in 10 Afghans (72%) reported that there had been times in the

past 12 months when their household lacked enough money for food. This marked

a 15-percentage-point increase from 2018 and a new high since Gallup first

began measuring this item annually in Afghanistan in 2008.

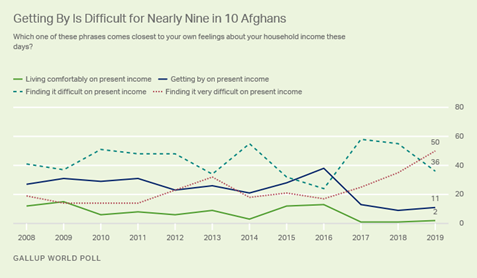

Line chart. Trend line showing the

percentage of Afghans who struggled to afford food. A record 72% in 2019

could not afford food at times for themselves or their families. After Kabul fell to the Taliban in August,

U.N. agencies have warned of disruptions in the distribution of emergency

aid, even calling for a "humanitarian airbridge" to be put in place

to ensure medicines and hospital supplies are delivered. But while the

collapse of the former Afghan government has exacerbated the country's

humanitarian crisis in recent weeks, the Food and Agriculture Organization of

the United Nations (FAO) has been sounding alarm bells for months, warning of

a potential 25% reduction in wheat yields in 2021, a crop that provides half

of all caloric intake in the country. Reflecting Afghans' increased inability to

afford food even before the Taliban's takeover, a record-high percentage of

Afghans in 2018 (90%) reported that they were finding it either

"difficult" or "very difficult" to get by on their

household income, a figure that remained at 86% in 2019. In 2019, however, a

record-high 50% of Afghans were in the "very difficult" category. More economic pain may be in store for

Afghanistan as a cash-strapped Taliban government asserts control of the

country. At least $10 billion of central bank funds remain outside the reach

of the country's new authorities, money badly needed to help pay salaries and

keep government ministries and programs running. Disruption within the financial

system has already reached ordinary Afghans as well, as local banks remain

closed -- creating a cash shortage for residents and businesses and a

resulting decrease in economic activity at a time of already heightened

economic uncertainty.

Line graph. Trend line showing how well

Afghans perceive they are getting by on their current household incomes. A

record 50% of Afghans found it very difficult to get by on their household

incomes in 2019. Eighty-six percent found it difficult or very difficult to

do so. Bottom Line After 20 years of insurgency, Afghanistan's

new Taliban government must now turn its attention to governing. Already

among the world's poorest countries, Afghans' economic outlook had taken a

turn for the worse in recent years, a situation now further compounded by

regional drought, isolation from the world financial system and political

uncertainty. Both Afghans and the world wait to see if

the Taliban's assurances of moderation on many issues will come to pass or if

the new regime will behave similarly to its last time in power from 1996 to

2001. Humanitarian pledges from the international community show a continued

commitment to the people of Afghanistan and a willingness to engage, even if

not recognize, Afghanistan's new rulers. Recent developments in Afghanistan have

increased the vulnerability of many Afghans who had already struggled for the

basics of survival. The likelihood of a reduced wheat harvest this year in

the face of severe drought threatens to push the country toward famine just

as the Taliban takes the helm of the country's ministries. The Taliban's

willingness to work alongside international aid agencies to address the

impending food crisis poses an early test of the new government's ability to

meet the needs of its population and gain a degree of acceptance among

nations. While the Taliban has proven its staying power as an insurgent

force, it may yet find that it was easier fighting people than feeding them. (Gallup) SEPTEMBER 23, 2021 Source: https://news.gallup.com/poll/354917/afghans-crisis-withdrawal.aspx WEST

EUROPE

709-43-04/Polls 86% Britons Support The Idea That Government Should Provide More

Information To The General Public About Levelling Up

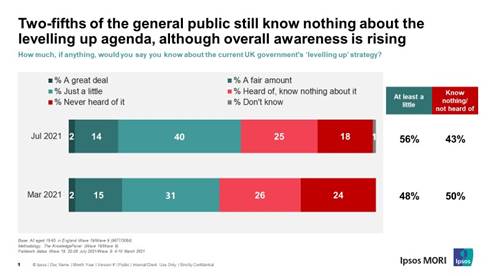

Ipsos MORI’s KnowledgePanel has found that between March and July

2021, Britons’ awareness of the Government’s Levelling Up strategy increased.

Those knowing at least a little about it rose by 8 points from 48% to

56%, with an equivalent fall in those who know or heard nothing about it

These increases were seen across all regions except the West Midlands,

particularly the North East .

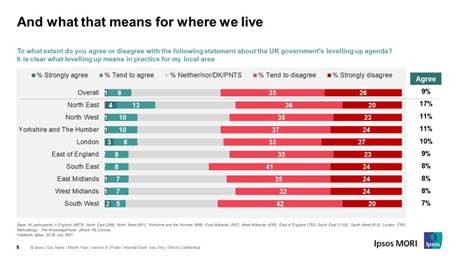

The increase in awareness, however, is among those who know just a

little rather than having a deeper understanding, and so this is still

complemented by a strong view that it should be a Government priority to

provide more information to the general public about levelling up, with 86%

supporting that idea, while only 9% of Britons believe it is clear what

levelling up means in practice for their local area. The region with the best

sense of understanding of what levelling up means for their area is the North

East, although still only 17%.

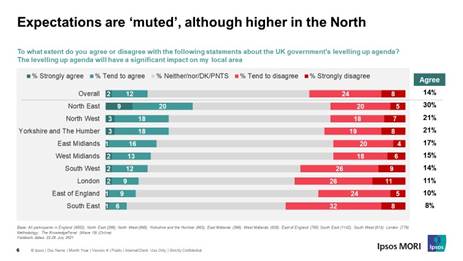

Britons in the North East are also most likely to expect the

levelling up agenda to have the biggest impact on their local area (30%),

with those in the South East most pessimistic (40% do not think it will have

much effect). Overall, expectations are muted: one in seven (14%) think

levelling-up will bring significant impacts, but twice as many (32%) disagree

– with even more (38%) sitting on the fence and still to be persuaded one way

or the other.

Kelly Beaver, Managing Director of Public

Affairs commented: It is clear that as Michael Gove comes into

a new expanded role looking at levelling up there is still work to do to help

the public feel informed about what it means both in general and for their

local area in practice. While awareness is increasing (including some signs

that the North East is particularly positive), there is still a way to go

before levelling up is fully understood by the public and, just as

importantly, that they are convinced it will deliver improvements for them. (Ipsos MORI) 21 September 2021 709-43-05/Polls More Than Half (52%) Of The UK Public Know Someone Who Has Been

Diagnosed With Dementia

Findings from the second wave of one of the most comprehensive

surveys of UK-wide public perceptions of dementia and research have been

revealed by Alzheimer’s Research UK, the UK’s leading dementia

research charity. Wave 2 of the Dementia Attitudes Monitor gives detailed

insight into the UK’s understanding of, and attitudes towards dementia,

building on findings from Wave 1 in 2018. More than half of us have been affected by

dementia Wave 2 of the Monitor has revealed that more than half (52%) of the

UK public know someone who has been diagnosed with the condition - a figure

that remains unchanged since Wave 1. This is most often a grandparent (17%)

or parent (13%). Wave 2 suggests a positive shift in understanding of the diseases

that cause the condition, though fear persists. The majority of people (68%) correctly disagree with the statement

‘dementia is an inevitable part of getting older’ - up from 60% in Wave 1.

The proportion who are unsure whether dementia is inevitable has fallen from

17% to 11%. In 2018, half (51%) of the public agreed with the statement ‘Dementia

is a cause of death’, despite it being the UK’s leading cause of death,

excluding COVID-19, since 2015. Three years on, 62% recognised the terminal

nature of the condition. Half (49%) of UK adults say that dementia is the health condition

they fear most about getting in the future, indicating an increase in concern

since Wave 1 of the Monitor (42%). Women (55% compared to 42% of men) and

older adults (60% of those aged 65 or over) are more likely to agree that

dementia is the health condition they fear most, reflecting findings from

2018. Awareness of risk and risk factors for

dementia remains low The latest evidence suggests that up to 40% of all cases of dementia

are linked to factors we may be able to influence ourselves, yet just a third

(33%) of UK adults think it’s possible for people to reduce their risk. Women

are less likely to think it’s possible to influence their dementia risk than

men (30% compared to 37%). When asked to consider what could increase a person’s risk, the most

common responses included ‘being less mentally active’ (mentioned by 22%) and

‘genetic factors’ (19%). Very few people named physical risk factors like

blood pressure and diabetes, despite evidence suggesting these are among the

factors most closely linked to dementia risk. Despite limited understanding of the ability to reduce dementia risk,

three quarters (75%) of people believe it’s possible for a person to

influence their brain health, suggesting that positively reframing dementia

risk reduction as ‘protecting brain health’ represents a major opportunity to

increase public engagement. The majority of people want to better understand their personal risk

and are open to using new technology to do so. Three quarters (74%) of UK adults say they would want to be told

about their personal risk of developing dementia later in life if their

doctor could provide this information (73% in Wave 1). There is widespread support for new techniques that could, in future,

be used to help measure dementia risk, with 75% of people willing to use

smartphone apps and wearable technology to do so. The Monitor shows that

reluctance to use technology in this way increases uniformly from the

youngest to oldest age groups. There is strong support for formal

diagnosis and early testing for dementia, even before symptoms show The vast majority of people (89%) would be likely to seek a formal

diagnosis if they were concerned they might be in the early stages of

Alzheimer’s disease or another form of dementia. The most common motivators

are to gain access to treatments that could help and to enable the person to

plan for the future (each mentioned by 32% of people who would seek a

diagnosis). Of the 9% who would be unlikely to seek a formal diagnosis, the main

reason given was that doing so would be too stressful. There is similarly strong support for very early detection and

diagnosis, with most people (87%) saying they would take a test, or set of

tests, that could tell whether they were in the very early stages of

Alzheimer’s or another form of dementia, even before any symptoms appeared

(85% in 2018). Finding a cure remains the UK’s top

research priority The Monitor once again identified strongest support for research into

ways to cure the diseases that cause dementia, cited as the most important

type of research by 28% of participants. Next, research into ways to prevent

dementia was chosen as most important by 22% of people. Positively, the majority (61%) of UK adults believe that one day the

diseases that cause dementia will be cured. 18% express uncertainty and just

16% disagree. Willingness to get involved in medical

research for dementia is at an all-time high Wave 2 of the Monitor found that the 69% of UK adults would now

consider getting involved in medical research for dementia - a marked

increase since Wave 1 (50%). Research being ‘the only answer to dementia’ is the main driver for

participation, mentioned by 46% of those expressing an interest in taking

part. As seen in Wave 1, uncertainty about what would be involved is the most

common reason for reluctance, mentioned by 23% of those who would not take

part. Nick Philp, Director in Ipsos Observer,

said: This second wave of the Dementia Attitudes

Monitor is tracking changing perceptions about dementia and research. We hope

it will shine a light on the opportunities to direct efforts towards a world

free from the fear, harm and heartbreak of dementia. (Ipsos MORI) 22 September 2021 Source: https://www.ipsos.com/ipsos-mori/en-uk/more-half-us-have-been-affected-dementia 709-43-06/Polls Manchester United Is The Best-Supported Premier League Club In The UK,

But There’s Close Competition

With the 2021-22 edition of the Premier League still in its early

stages, not much can be read into the table yet. So, we dive into our data to

put together a different kind of points table, looking at the best-supported

clubs in the UK. Starting off, Manchester United claim the top spot with Liverpool hot

on their heels. Almost a fifth of Premier League fans in Britain support the

Red Devils (19%), while Jurgen Klopp’s team enjoys support from 17%. Premier League fans in this piece are defined as those who are

“somewhat interested” in the Premier League or regard it as one of their “top

interests”. While the contest is close at the top of the table, there is a

significant gap between them and the rest. Arsenal come in at No.3 in the

support stakes,with one in ten followers of the Premier League saying they

support the Gunners (10%). Chelsea and Tottenham Hotspur are next in line

with 8% of Premier League followers saying they support those clubs. A good indication that a following for Premier League clubs is built

organically, and that on-field success takes a while to embed new supporters,

is the position of Manchester City in the table. Pep Guardiola’s team has

bagged the title three times in the last four seasons but enjoys the support

of just 6% of Premier League followers, one-third that of their intra-city

rivals Manchester United. Meanwhile, Leeds United and Newcastle United have the support of one

in 20 Premier League fans each (5%), while West Ham and Leicester City are

supported by 4%. (YouGov UK) September 24, 2021 709-43-07/Polls One In Eleven Say The Coronavirus Act Should Be Made Permanent

The government is expected to reveal next

week which parts of the Coronavirus Act will be repealed and which

will be kept. The Act is a piece of legislation that initially granted the

government emergency powers to deal with the pandemic. It includes the

ability to restrict public gatherings, order businesses to close and detain

people suspected of COVID-19 infection. Under current plans, the Act will

expire in March 2022. New YouGov research shows that nearly three in ten people think the

act should be extended, however. This includes 20% of people who think the

Act should be extended temporarily and 9% who think it should be permanently

enshrined in law.

The most commonly held view is that the Act should be kept for the

coming autumn and winter, and be allowed to expire as planned next March. One

in three Britons (31%) feel this way. Conservative voters are more likely to think the Coronavirus Act

should be extended or made permanent (35%) than Labour voters (26%). However,

Labour voters are not necessarily more in favour of repealing the Act early,

with a higher proportion unsure (18%) than Tories (8%). Britons aged between 18 and 24 are more likely to be in favour of

repealing the Act early (29%) than other age groups. This includes 11% who

think it should be repealed immediately and 18% who think it should be

scrapped before March 2022 but not immediately. Some 19% of Britons aged 65

and over are in favour of repealing the Act earlier than its intended date,

while 40% think it should be maintained beyond that – including 11% who think

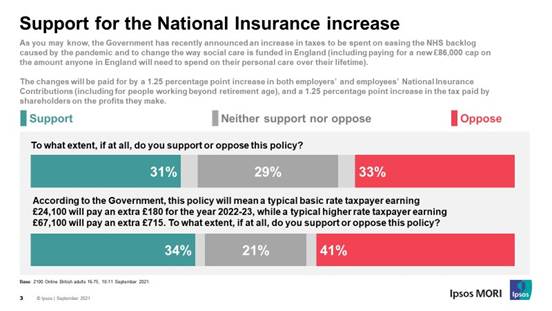

it should be permanent law. (YouGov UK) September 24, 2021 709-43-08/Polls Over A Third Say The Quality Of Social Care Is Likely To Improve As A

Result Of The Plan To Raise National Insurance To Help Fund Health And Social

Care

Last week, the UK Government announced a plan to raise National

Insurance to help fund health and social care. Now, new research by Ipsos

MORI shows many Britons are split in their support for the policy, the impact

it will have on the NHS and social care, and how fairly it treats different

groups. Just over a third say the quality of social care is likely to

improve as a result of this policy (35%) while 37% are hopeful for

improvement in the NHS. However half are more sceptical, thinking it is

unlikely that the NHS or the quality of social care will improve (48% and 49%

respectively).

There is though a feeling that even this funding boost will not be

enough. Three-quarters say it is likely that the NHS and social care

services will need even more funding than this policy provides over the next

few years (76% and 74% respectively). Similarly, a plurality of Britons

believe the money promised over the next 3 years is too little for both the

NHS (42%) and social care services (42%). Around a quarter 10 say it is

about the right amount (28% and 26%) while just over 1 in 10 think it too

much (12% and 13%). Most Britons to view this policy as unfair for poorer people (55% - a

view held among those on high, medium and low incomes), while a similar

proportion (53%) say it is fair for richer people. People also believe

it is unfair to younger people by a margin of 2:1 (45% vs 22% - again, a view

shared amongst all age groups), while they are split on whether it is fair

for older people (31% fair vs 34% unfair). Only a quarter (24%) think it is

fair for “people like me” while 41% think it is unfair (although this falls

to 32% among 55-75 year olds).

Support for the policy overall splits opinion - a third (31%) support

it, and the same proportion are against it (33%). When prompted with the

extra tax that would be paid for it, a third (34%) still support it, but 41%

oppose. Support is higher among older people and Conservative voters than

younger people and Labour voters. However, a majority of Britons knew little,

if anything, about the policy. Fifty-five per cent say they didn’t know very

much, had heard of the policy but knew nothing of it or knew nothing at all

before taking part in the survey.

Almost 6 in 10 (58%) expect the policy to make the Conservatives less

popular while only 12% expect their popularity to increase. Britons expect

the policy and Labour’s reaction to it to have less impact on Labour’s

reputation: 32% say it will make no difference while 26% expect it to harm

their popularity and 19% expect an improvement. Gideon Skinner, Head of Political Research

at Ipsos MORI, said: The public is split in its reaction to the

Government’s new levy or health and social care. Political partisanship

is playing a role, but there are other factors at play – on the one hand a

feeling that even more money may be needed to tackle the challenges faced by

the NHS and social care, to tackle staff shortages, improve the quality of

care and increase access, and on the other concerns about fairness towards

the young and poorer people (concerns that are shared by older people and

those on high incomes). And the reality of the extra tax that will need

to be paid is also having an effect. (Ipsos MORI) 26 September 2021 709-43-09/Polls 54% Of French People Believe That The School System Works Poorly

At first glance, the school system is primarily associated with the

acquisition of skills (55% of French people associate this notion with

it). However, it is also linked to negative notions such as obligation /

constraint and the forbidding aspect (respectively 42% and 39%). Despite a busy context, new generation

education must have a real place in the 2022 presidential campaign For 85% of French people, the debate on new generation education must

have an important or even essential place in the presidential campaign of

2022. Among them, 41% think that it is essential. At the same time, only

6% consider that this debate is irrelevant. These figures are striking

in several respects on the one hand, despite many strong concerns (Covid-19,

environment), education remains a major expectation there is no question of

putting it aside. Moreover, the French are convinced of their

opinion. It is not a question of a little marked wish but of a real will

on their part. Finally, the key to success lies

particularly in the involvement of students. More than three quarters of French people believe that the

modernization of school education in France must go through the

generalization of particularly "engaging" practices such as the

creation of a digital school space for each class (86% are in favor), the

fact ask students to be trainers themselves for a few sessions (81%) or to

impose interactivity in all lessons (77%). While digital technology is necessary (73% also consider that the

creation of digital diplomas and certifications is useful for this type of

knowledge to be recognized), it appears to the French more as a complementary

tool and not an end. in itself. Thus, although it is important or even

essential to train teachers in digital tools so that the divide in this area

is reduced (89%) or to educate students in digital technology to combine the

best of man and digital ( 79%), only a minority of French people are in favor

of replacing books with digital content (49%) or writing exclusively on

computers (18%). In short, digital must include more than exclude. The Covid 19 health crisis, a vector of

inequalities ... but also of opportunities! For nearly 8 in 10 French people, Covid-19 has had many negative

effects, including dropping out of school (87%), increasing inequalities

between pupils / students (83%) and not being ready to entering working life

for young graduates (79%). However, it is interesting to note two things

first, the youngest (although more concerned by these problems) are critical

but less than their elders. Secondly, the Covid-19 crisis has also enabled

many advances and in particular new ways of working. (Ipsos France) 22 September 2021 Source: https://www.ipsos.com/fr-fr/54-des-francais-estiment-que-le-systeme-scolaire-fonctionne-mal NORTH

AMERICA

709-43-10/Polls In U S, An Estimated 18 Million Can't Pay For Needed Drugs

WASHINGTON, D.C. -- Seven percent of U.S. adults -- representing an

estimated 18 million persons -- reported in June that they were unable to pay

for at least one doctor-prescribed medication for their household during the

prior three months, according to the most recent West

Health and Gallup survey. This percentage is in line with the 6%

reported in March. Among those in households earning less than $24,000 per

year, however, the percentage has jumped from 10% to 19%, a statistically

significant increase. U.S. Three-Month Medication Insecurity, Trended, by Household Income Has there been a time in the last three months when you or a member

of your household has been unable to pay for medicine or drugs that a doctor

had prescribed to you because you did not have enough money to pay for them?

(% Yes)

While affordability of prescription drugs is an issue for all age

groups, the inability to pay for a prescription runs twice as high for

households with an adult younger than 65, compared with households that have

at least one senior (8% to 4%, respectively). This is despite the fact that

prescription drug usage climbs significantly with age. Among seniors, for

example, 40% report currently having at least five prescription drugs,

compared with 23% among those aged 50-64 and less than 10% among those younger

than 50. These surveys were conducted by web from June 14-20, March 15-21 and

Jan. 25-31, 2021, with adults aged 18 and older, living in all 50 U.S. states

and the District of Columbia via the Gallup

Panel, a probability-based, non-opt-in panel of about 120,000 adults

nationwide. Medication Insecurity Climbs With Chronic

Conditions and Prescriptions Being unable to afford medication over the prior three months climbs

with medical need. Among respondents with three or more chronic conditions,

or eight or more prescriptions, reports of being unable to pay for a

prescribed drug in the household reach 11% and 18%, respectively. Among

respondents with no chronic conditions and no more than two prescribed drugs,

these household rates drop to 4% and 5%, respectively. U.S. Three-Month Medication Insecurity by Number of Prescription

Drugs and Number of Chronic Conditions Has there been a time in the last three months when you or a member

of your household has been unable to pay for medicine or drugs that a doctor

had prescribed to you because you did not have enough money to pay for them?

(% Yes)

Respondents with certain chronic conditions are significantly more

likely to suffer medication insecurity than are adults generally. These

include those who have been diagnosed with diabetes (12%), chronic

obstructive pulmonary disease or COPD (12%), depression (12%), and those who

are immune compromised (15%). One in 10 Skip Pills to Save Medicine,

Money While 7% of Americans report that they have or a family member has

gone without at least one prescribed medication because of costs, 10% report

skipping dosages in the prior 12 months as a way of saving medicine and,

therefore, money. This rate is considerably higher among lower-income

households. Among respondents in households earning less than $48,000

annually, for example, 18% report that they or someone in their household had

skipped a pill. Even among higher-income households earning $90,000-$180,000,

7% of respondents report having skipped a pill in the prior 12 months. Adults younger than 65 are also about twice as likely as seniors to

report skipped doses in their households as a way to preserve medicine and

save money, a pattern similar to what this research found with the inability

to pay for prescriptions in the prior three months. Skipping Prescribed Medication to Save Money, by Annual Household

Income and Age Thinking about the last 12 months, have you or a family member

skipped a pill to save medication in order to save money? (% Yes)

Implications The latest results from the West Health-Gallup research into U.S.

healthcare add to a growing body of data indicating how Americans cope with

the high cost of care. Chief among the prior insights are that an estimated

18% of adults, or about 46 million people, could

not afford needed care if they required it today and, separately,

that 16% of workers remain

in unwanted jobs so they can keep the health benefits the job

provides them. Beyond care itself, the second main aspect of healthcare costs in the

U.S. is the price consumers pay for prescription drugs. Before President Joe

Biden's inauguration, lowering drug costs was the

second-highest healthcare priority Americans had for him, after reducing

health insurance premiums. Two-thirds of U.S. adults said reducing drug costs

was a "high" or the "highest" priority, including 62% of

Republicans. The roughly 7% of Americans who have been unable to pay for

prescribed drugs in the prior three months and the 10% who are skipping doses

to save medication because of costs further expose this issue in stark terms.

These practical manifestations of how Americans manage their healthcare costs

underscore the urgency of the issue, particularly for those younger than 65,

nearly all of whom do not yet qualify for Medicare. The disproportionate manner in which prescription drug prices are

affecting sicker and lower-income Americans is also apparent. This reveals an

unfortunate scenario whereby those who are most in need of prescription drugs

are also the most likely to ration their use if they are able to afford them

at all. Substantial majorities of U.S. adults, in turn, support government

involvement in a number of aspects of cost control, including setting

limits on drug price increases and allowing government negotiation of prices

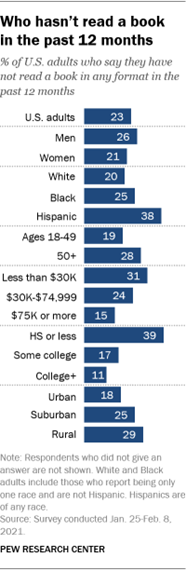

for high-cost drugs for which there are no competitors. (Gallup) SEPTEMBER 21, 2021 Source: https://news.gallup.com/poll/354833/estimated-million-pay-needed-drugs.aspx 709-43-11/Polls Roughly A Quarter Of American Adults (23%) Say They Haven’t Read A

Book In Whole Or In Part In The Past Year

Roughly a quarter of American adults (23%) say they haven’t read a

book in whole or in part in the past year, whether in print, electronic or

audio form, according to a Pew Research Center survey of U.S. adults

conducted Jan. 25-Feb. 8, 2021. Who are these non-book readers? Several demographic traits are linked with not reading books,

according to the survey. For instance, adults with a high school diploma or

less are far more likely than those with a bachelor’s or advanced degree to

report not reading books in any format in the past year (39% vs. 11%). Adults

with lower levels of educational attainment are also among the least likely to own

smartphones, an increasingly

common way for adults to read e-books. How we did this

In addition, adults whose annual household income is less than

$30,000 are more likely than those living in households earning $75,000 or

more a year to be non-book readers (31% vs. 15%). Hispanic adults (38%) are

more likely than Black (25%) or White adults (20%) to report not having read

a book in the past 12 months. (The survey included Asian Americans but did

not have sufficient sample size to do statistical analysis of this group.) Although the differences are less pronounced, non-book readers also

vary by age and community type. Americans ages 50 and older, for example, are

more likely than their younger counterparts to be non-book readers. There is

not a statistically significant difference by gender. The share of Americans who report not reading any books in the past

12 months has fluctuated over the years the Center has studied it. The 23% of

adults who currently say they have not read any books in the past year is

identical to the share who said this in 2014. The same demographic traits that characterize non-book readers also

often apply to those who have never been to a library. In a 2016

survey, the Center found that Hispanic adults, older adults, those living

in households earning less than $30,000 and those who have a high school diploma

or did not graduate from high school were among the most likely to report in

that survey they had never been to a public library. (PEW) SEPTEMBER 21, 2021 Source: https://www.pewresearch.org/fact-tank/2021/09/21/who-doesnt-read-books-in-america/ 709-43-12/Polls Half Of Americans Said Their Area Had Experienced Extreme Weather

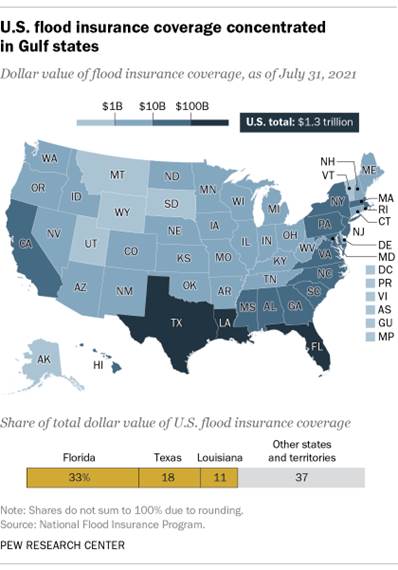

Over The Past Year

According to a recent Washington

Post analysis, nearly a third of Americans live in a county that was

struck by a weather disaster this past summer, and around two-thirds live in

places that experienced a multiday heat wave. In an April

Pew Research Center survey, half of Americans said their area had

experienced extreme weather over the past year. Human-caused climate change will make extreme weather events more

frequent and more damaging in the coming decades, according to the latest

report from the United Nations Intergovernmental Panel on Climate

Change. While the nations of the world struggle to agree on how to address

the root causes of climate change, there are various ways people can prepare

to deal with the immediate effects on a household level. This analysis examines the prevalence of four specific tools to endure

extreme weather in the United States: flood insurance, air conditioning,

portable generators and home insulation. (As we’ll see, some of these tools

may have their own climate impacts.) Flood insurance Standard homeowner or renter insurance seldom, if ever, protects

against flood damage. While some private

companies sell their own flood insurance, the primary provider of

such coverage in the United States is the National Flood Insurance Program (NFIP),

managed by the Federal Emergency Management Agency.

Nearly 5 million NFIP policies were in force as of July 2021, the

most recent month available. That figure hasn’t varied much for the past few

years, though it’s down from a peak of 5.7

million policies at the end of 2009. Flood insurance is available in

over 22,000 communities throughout the country, but it’s particularly

important in states that border the Gulf of Mexico: 60% of all policies in

force, accounting for a somewhat higher share of covered property value, are

in Florida, Texas and Louisiana. More than a quarter of U.S. homeowners (27%) said in a 2020

survey by the Insurance Information Institute, or Triple-I, that

they had flood insurance – more than twice the share who said they had it in 2018

(13%). However, the Triple-I itself has expressed some doubt about whether

flood coverage is that high. Noting that the NFIP data implies a lower

coverage rate, the institute said, “It is possible that [people] with

homeowners insurance believe they have flood coverage when they actually do

not … homeowners may not fundamentally understand what flood coverage is and

how it works. Or they may think flood coverage encompasses water damage from

a burst pipe instead of a weather-related event like a hurricane or from a

river flooding.” Next month, NFIP will change the way it

sets its insurance rates to better reflect each individual property’s actual

flood risk. The current system, which has been in place since the 1970s,

relies mainly on a property’s elevation and location within a floodplain.

Critics have long argued that the program’s flood maps aren’t updated

frequently enough and understate

true flood risks, and that the guaranteed availability of flood insurance

can encourage flooded-out owners to rebuild

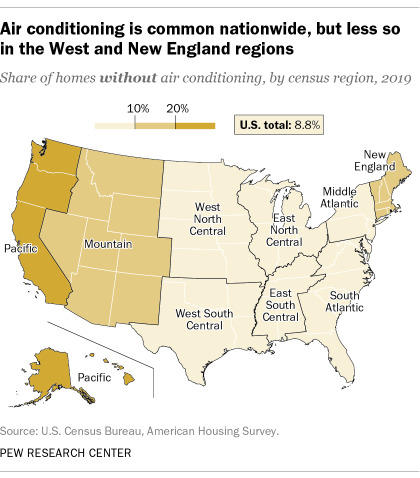

structures rather than move them to safer ground. Air conditioning

Air conditioning, either central or room-based, has become the

default in American homes – a boon during oppressive summer

heat waves. Nationwide, only 8.8% of housing units lacked some form of

air conditioning in 2019, according to the Census Bureau’s American Housing

Survey for that year. But that ubiquity obscures some important geographic

and demographic variations. In Northern California and the Pacific Northwest, for instance,

residents long were accustomed to cool, rainy winters and mild, low-humidity

summers. The consequence: 55.7% of housing units in Seattle have no air

conditioning of any sort, nor do 52.7% in San Francisco and 21.4% in

Portland, Oregon. But long stretches of days with temperatures of 100 degrees

and higher reportedly have sent at least some Northwesterners fleeing to home

improvement stores and HVAC contractors in search

of relief. Americans with higher incomes are moderately more likely to have

access to air conditioning, according to the Census Bureau data, though the

differences are smaller than you might expect: 92.2% of households with

incomes of $100,000 or more have some form of air conditioning, compared with

88.9% of households with incomes of less than $30,000. The type of AC, however, does vary more substantially by income.

Among below-$30,000 households with air conditioning, 70.1% have central air

and 29.9% have window units, which generally can only effectively cool a

single room. Among households earning $100,000 or more, the split is 85.6%

central, 14.2% window. Either way, air conditioning uses prodigious amounts of electricity,

and depending on how that electricity is generated, AC can exacerbate the

very problem it’s trying to alleviate. AC units can also emit waste

heat and greenhouse gases of their own into the atmosphere. As The

Guardian put it a few years back, “The warmer it gets, the more we

use air conditioning. The more we use air conditioning, the warmer it gets.” Generators Of course, air conditioners won’t work without electricity. Nor will

refrigerators, washers, computers or any number of other critical appliances

– not to mention lights. People who live in storm-prone areas, such as the

Gulf Coast or North Carolina’s Outer Banks, often have portable generators in

case the local electricity grid fails (as it did this year in New

Orleans after Hurricane Ida).

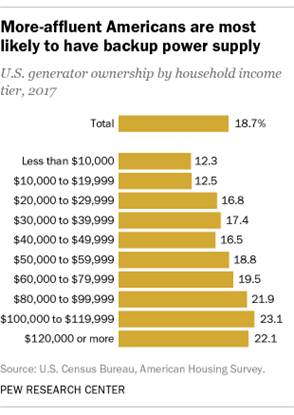

The American Housing Survey’s latest data on generator ownership is

from 2017. That year, only about 19% of U.S. households reported owning the

devices. (The question was only asked of people living in single-family homes

and small apartment buildings.) The income difference on generator ownership

was much more pronounced than with air conditioning: 22.4% of households

earning $100,000 or more reported having a generator, versus 14.1% of

households making less than $30,000. The regional differences are noteworthy too. Nearly a quarter (24.2%)

of New England housing units surveyed had a generator, versus just 14.2% in

the Mountain states. Among metro areas, Richmond, Virginia, and Miami-Fort

Lauderdale stood out, with 28.8% and 26.6%, respectively, of housing units

having generators. California’s Bay Area was a notable laggard, with just

6.3% of units in San Francisco and 7.5% in San Jose having generators. Most home generators, however, burn fossil fuels such as gasoline,

diesel or propane to generate electricity, which means they’re also

generating greenhouse gases that are major drivers of climate change. Clean

energy groups advocate for different

approaches: combining storage batteries with solar panels mounted on

homes, businesses and other structures, for instance, or installing

neighborhood-scale “microgrids” that

can operate on their own if the wider transmission grid goes down. Insulation Climate change doesn’t just mean warmer temperatures. As extreme

weather of all types, such as the wave of winter

storms and bone-chilling cold that nearly paralyzed much of Texas

last winter, becomes more common, millions can be left without heat, water

and power for days on end. That’s where insulation – a relatively low-tech solution that can

increase a home’s energy efficiency so that it stays warmer in the winter and

retains cool air-conditioned temperatures in the summer – can make a big

difference. Many homes in Texas, it turned out, had inadequate

or nonexistent insulation, which led to cracked pipes and frigid indoor

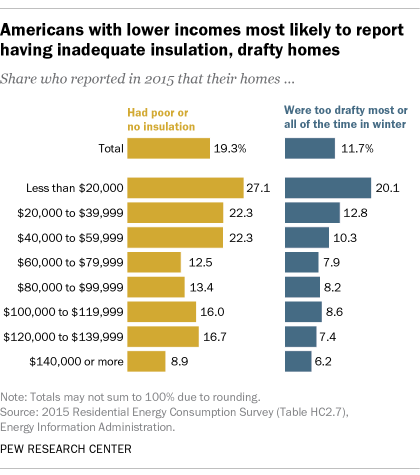

temperatures. The best data on home insulation comes from the 2015 Residential

Energy Consumption Survey (RECS), a project of the federal Energy

Information Administration. In addition to asking people how adequately they

thought their home was insulated, the RECS researchers asked how often their

home felt drafty in the winter (because previous surveys had found few people

knew details about the amount or quality of their home’s insulation).

Overall, 19.3% of households said they had poor or no insulation, a

slight improvement from the 21% who said that in the 2009 RECS. And 11.7%

said their homes were drafty most or all of the time in winter, down from

15.4% in 2009. A quarter (25.1%) of respondents in the Pacific region said they had

poor or no insulation, though only 12.3% said their homes were drafty most or

all of the time in the winter. Only 14.3% of householders in the Mountain

North subregion (Colorado, Idaho, Montana, Utah and Wyoming) characterized

their insulation as poor or nonexistent, and just 9.5% said their homes were

drafty most or all of the time. In the Mountain South states of Arizona, New

Mexico and Nevada, where 16.3% said their homes had poor or no insulation,

just 7% said their homes were that drafty. In general, the lower one’s household income, the worse one’s home

was insulated and the draftier it was. More than a quarter (27.1%) of people

whose household income was less than $20,000 said they had poor or no

insulation, and a fifth (20.1%) said their homes were drafty most or all of

the time in winter. For people with household incomes of $140,000 or more,

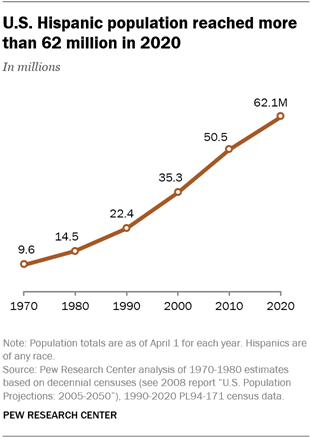

those figures were 8.9% and 6.2%, respectively. (PEW) SEPTEMBER 22, 2021 709-43-13/Polls US Hispanic Population Reached More Than 62 Million In 2020

Debates over who

is Hispanic and who is not have often fueled conversations about

identity among

Americans who trace their heritage to Latin America or Spain. Most

recently, the 2020 census has drawn attention to some of the many layers of

Hispanic identity, providing fresh details about how Hispanics view their

racial identity. So, who is considered

Hispanic in the United States? And how are they counted in public opinion

surveys, voter exit polls and government surveys such as the 2020 census? The most common approach to answering these questions is

straightforward: Who is Hispanic? Anyone who says they are. And nobody who

says they aren’t.

Pew Research Center uses this approach and the U.S. Census Bureau

largely does so too, as do most other research organizations that conduct

public opinion surveys. By this way of counting, the Census Bureau estimates

there were roughly 62.1

million Hispanics in the United States as of 2020, making up 19% of

the nation’s population. Behind the official Census Bureau number lies a long history of

changing labels, shifting

categories and revised question

wording on census

forms – all of which reflect evolving cultural norms about what it

means to be Hispanic or Latino in the U.S. today. Here’s a quick primer on the Census Bureau’s approach of using

self-identification to decide who is Hispanic. I immigrated to Phoenix from Mexico. Am I

Hispanic? You are if you say so. My parents moved to New York from Puerto

Rico. Am I Hispanic? You are if you say so. My grandparents were born in Spain but I

grew up in California. Am I Hispanic? You are if you say so. I was born in Maryland and married an

immigrant from El Salvador. Am I Hispanic? You are if you say so. One of my great grandparents came to the

U.S. from Argentina and settled in Texas. That’s where I grew up, but I don’t

consider myself Hispanic. Does the Census Bureau count me as Hispanic?

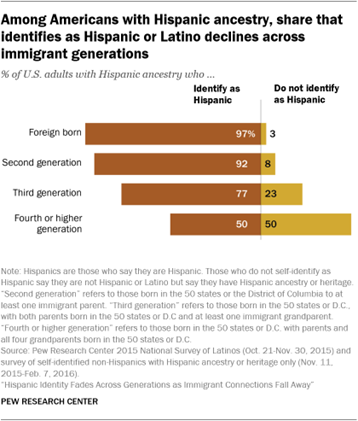

Not if you say you aren’t. Of the 42.7 million adults with Hispanic

ancestry living in the U.S. in 2015, an estimated 5

million people, or 11%, said they do not identify as Hispanic or Latino,

according to a Pew Research Center survey of U.S. adults. These people aren’t

counted as Hispanic in Pew Research Center surveys. The Census Bureau

generally takes a similar approach in its decennial census. Hispanic

self-identification varies across immigrant generations. Among the foreign

born from Latin America, nearly all self-identify as Hispanic. But by the

fourth generation, only half of people with Hispanic heritage in the U.S.

self-identify as Hispanic. But isn’t there an official definition of

what it means to be Hispanic or Latino? In 1976, the U.S. Congress passed what

was the only law in this country’s history that mandated

the collection and analysis of data for a specific ethnic group:

“Americans of Spanish origin or descent.” The language of that legislation

described this group as “Americans who identify themselves as being of

Spanish-speaking background and trace their origin or descent from Mexico,

Puerto Rico, Cuba, Central and South America, and other Spanish-speaking

countries.” This includes 20 Spanish-speaking nations from Latin America and

Spain itself, but not Portugal or Portuguese-speaking Brazil. Standards for

collecting data on Hispanics were developed by the Office of Management

and Budget in

1977 and revised in

1997. Using these standards, schools, public health facilities and other

government entities and agencies keep track of how many Hispanics they serve

– the primary goal of the 1976 law. However, the Census Bureau does not apply this definition when

counting Hispanics. Rather, it relies entirely on self-reporting and lets

each person identify as Hispanic or not. The 2020 decennial census form asked

the question this way:

What’s the difference between Hispanic and

Latino? The terms “Hispanic” and “Latino” are pan-ethnic terms meant to

describe – and summarize – the population of people living in the U.S. of

that ethnic background. In practice, the Census Bureau most often uses the

term “Hispanic,” while Pew Research Center uses the terms “Hispanic” and

“Latino” interchangeably when describing this population. Some have drawn sharp distinctions between these

two terms, saying for example that Hispanics are people

from Spain or from Spanish-speaking countries in Latin America (this

excludes Brazil, where Portuguese is the official language), while Latinos

are people from Latin America regardless of language (this includes Brazil

but excludes Spain and Portugal). Despite this debate, the “Hispanic” and

“Latino” labels are not universally embraced by the population that has been

labeled, even as they are widely used.

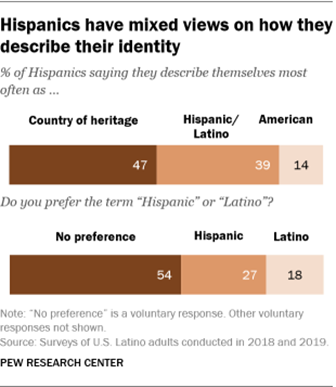

Instead, Pew Research Center surveys show a preference for other

terms to describe identity. A 2019

survey found that 47% of Hispanics most often describe themselves by

their family’s country of origin; 39% use the terms Latino or Hispanic, and

14% most often describe themselves as American. As for a preference between

the terms Hispanic or Latino to describe themselves, a 2018

survey found that 27% prefer “Hispanic,” 18% prefer the term

“Latino” and the rest (54%) have no preference. These findings have changed