|

BUSINESS & POLITICS IN THE WORLD GLOBAL OPINION REPORT NO. 784-785 Week: March

27 – March 12, 2023 Presentation:

March 17, 2023 Inside

Afghanistan: Record Numbers Struggle to Afford Basics 11 UAE

Parents Have High Concerns over Their Child’s Exposure To Inappropriate

Online Content 13 Health

Insurance Coverage for Nigerians Still Abysmal; An Urgent Call For New

Strategy. 15 Labour

Voters More Wary about Politics of Child’s Spouse 17 Most

Brits Expect Recession, As Consumer Confidence Dips To Six-Year Low 19 Half

of Leave Voters Doubt Johnson Can Secure New Brexit Deal 21 Few

Believe the Government's Explanation of Why Parliament Is To Be Suspended 23 Brits

Oppose Parliament Suspension By 47% to 27% 24 5

Facts about the Abortion Debate In America 25 U.S.

Concern about Climate Change Is Rising, But Mainly Among Democrats 28 Most

Americans Say Science Has Brought Benefits to Society and Expect More to

Come 31 Parents'

Concern about School Safety Remains Elevated 34 As

Labor Day Turns 125, Union Approval Near 50-Year High 36 Americans'

Satisfaction with U.S. Education at 15-Year High 38 Most

Cannabis Consumers Use on a Weekly Basis or More 41 Ride-Sharing

App Uber Overtakes Taxis as Preferred Private Transport Service 43 Rising

Numbers of Australians Looking At Electric and Hybrid Vehicles for Their

Next Set of Wheels 45 Toyota

And Mazda Drivers Most Brand Loyal; Have The Luxury Brands Lost Their

Lustre? 48 Britons

Make Worst Tourists, Say Britons (And Spaniards And Germans) 50 Brazilians

Least Satisfied in Amazon With Environment 55 India

Ranks 9th on Happiness among 28 Global Markets: Ipsos Global Happiness

Survey 58 The

Biggest Beauty Influencer Isn’t Who You Think It Is 59 INTRODUCTORY NOTE This weekly report consists of thirty-five surveys.

The report includes eight multi-country studies from different states across

the globe. 784-785-43-36/Commentary: Out

Of The 64 Countries That Were Surveyed, South Korea Tops Security Preference

For US, Pakistan Tops Preference For China, While Serbia Tops The Preference

For Russia And Sweden For EU For Security Partnership: GIA And Gallup & Gilani Pakistan

According to a survey conducted by

Gallup International Association, out of the 64 countries that were surveyed, South Korea tops

security preference for US, Pakistan tops preference for China, while Serbia tops the preference for Russia and

EU for security partnership An opinion poll was conducted by

GIA in 64 countries covering over two thirds of the global population (and more than 90% of

those countries which are free to conduct and publish opinion research). This press release sheds

light on the findings of the survey regarding perceptions on strategic partnerships between countries. The question asked was “Which of

the following would you prefer your country to partner with for security – the US, China, Russia,

or The EU?” 84% people from South Korea said USA, 54% from Pakistan said China, 53% from

Serbia said Russia and 69% from Serbia said EU. The top 5 countries, with the

greatest number of people who responded USA were: 1. South Korea – 84% 2. Israel – 79% 3. Kosovo – 77% 4. Japan – 65% 5. Philippines – 63% The top 5 countries, with the

greatest number of people who responded China were: 1. Pakistan – 54% 2. Russian Federation – 50% 3. United Arab Emirates – 36% 4. Thailand – 25% 5. Palestinian Territories – 24% The top 5 countries, with the

greatest number of people who responded Russia were: 1. Serbia – 53% 2. Ethiopia – 46% 3. Syria – 45% 4. Armenia – 42% 5. Ivory Coast – 40% The top 5 countries, with the

greatest number of people who responded EU were: 1. Sweden – 69% 2. Ireland – 62% 3. Slovenia – 58% 4. Portugal – 54% 5. Switzerland – 52% Results by Demography (Security

Partnership): Age Differences in popularity of

Partnership on Security • Younger and middle-aged

populations are more amiable towards US when it comes to striking Security Partnership while the

older aged population prefers US and EU equally. • Across all age groups US was the

top preference across all the different parts of the world. Popularity Gap in terms of security

partnership between China and US • Among different religious groups,

US is ahead of China in preference for security partnership. • Hindu respondents most upbeat

about security partnership with US • After US, Christians and Hindus

prefer EU while Muslims prefer Russia Popularity of Security Partnership

by Per-capita Income. • Interesting to note that just

like economic preference, low-income economies prefer China for security partnership. • High-Income economies prefer EU

for security partnership, this could perhaps be explained by the fact that most high-income

economies belong to the EU while lower-middle income economies have the highest

preference for US as 39% responded so. Results by Region (Security

Partnership): Popularity of Security Partnership

with China • Popularity of security

partnership with China was found to be highest in South Asia followed by MENA region. The least support was

found in EU (with 3% saying they would prefer that) • Interestingly populations among

G7 countries, the support for partnership with China is highest in US where 16% seek security

partnership with China. The lowest in G7 country is Japan in its preference for China for security

partnership • Widespread support for security

partnership with US exists in East Asia and Oceania where 3 in 5 seek partnership. The lowest

support is non-EU Europe East (they seek partnership with EU and Russia) These interesting findings have

emerged out of an annual, 64 country research conducted by Gallup International (founded by the

world-renowned scholar and pollster Dr. George Gallup in 1947). The survey in Pakistan was done by

Gallup Pakistan, Pakistan’s oldest and trusted survey firm, working since 1979.

(Gallup Pakistan) March 08, 2023 Source: https://gallup.com.pk/wp/wp-content/uploads/2023/03/08-March-GIA-PR_merged.pdf ASIA (Japan) Japan Activists Demand

Dual-Surname Option On Women’s Day Women’s rights activists in Japan

renewed their demand Wednesday for the government to allow married couples

the option to keep both of their surnames, saying the current practice in

which most women face social pressure to adopt their husbands’ surnames--a

prewar tradition based on paternalistic family values--widens gender

inequality. “We strongly urge the parliament to face the issue and promptly

achieve a revision to the civil code,” the activists said in a statement they

handed to lawmakers who also attended the rally in Tokyo. (Asahi Shimbun) March 9, 2023 MENA (UAE) Inflation Is Changing Consumer

Priorities And FMCG Spend In The UAE Inflation and the resulting price

rises are putting pressure on consumers in the United Arab Emirates (UAE).

Spending has remained high since 2019 and this ongoing financial strain is

leading consumers to change the way they shop. But despite this, the UAE

economy ended 2022 solidly and signs suggest this growth will continue, but might

slow in the first half of 2023. Despite the inflationary pressures, the FMCG

industry grew in 2022. Spend on beverages tumbled by -4% and personal care by

-5% due to shoppers shifting their spend to food and home care products,

which grew by 5% and 7%, respectively. (Kantar) 09 March 2023 AFRICA (South Africa) Despite Growing Evidence,

Climate Change Is Still Unknown To Many South Africans About half (49%) of South Africans

said they had heard of climate change, a 7- percentage-point increase since 2018.

Awareness of climate change was particularly low among citizens with less

than a secondary education (36%%), the poor (37%), and rural residents (42%).

o Awareness was slightly above average among citizens who get daily news from

the Internet (58%), newspapers (56%), and social media (55%). Among those who

were aware of climate change, more than six in 10 (62%) said it is making

life in South Africa “somewhat worse” (30%) or “much worse” (32%). (Afrobarometer) 9 March 2023 WEST EUROPE (UK) A Quarter Of Britons Say They

Have A Phobia Of Heights According to the Cambridge

Dictionary, a phobia is “an extreme fear or dislike of a particular

thing or situation, especially one that is not reasonable”. The

NHS states that severe phobias can cause a person to

“organise their life around avoiding the thing that's causing them anxiety.” Five

in ten Britons (21%) say they suffer from arachnophobia, more widely known as

an extreme or irrational fear of spiders. This phobia is more common among

women, with a quarter (26%) saying they suffer from it compared to 16% of

men. (YouGov UK) February 27, 2023 Half Of Britons Say Feminism Is

Still Needed In The UK In 2023 Despite generations of women and

their male allies battling to achieve equality of the sexes, Britons

generally still think there’s work to be done in the UK. The large majority

of the public maintain equality for women and girls has not yet been achieved

across several key areas, from home and family life to work, education, media

representation, crime and politics. One in ten Britons (10%) think there’s

equality for women and girls in the workplace, while 41% say the country is

close to achieving equality and 38% say it’s not close. (YouGov UK) March 08, 2023 Four In Ten

Britons Say They’ve Witnessed Drug Deals In Their Neighbourhoods According to a new YouGov poll,

four in ten Britons (41%) have seen suspected drug deals close to their

doorsteps at least once or twice – including 8% who say they’ve witnessed

dealing “many times”. Young people are more likely to suspect dealing is

going on in their neighbourhoods, with half of 18 to 24-year-olds (51%)

saying they think they’ve witnessed at least one deal in progress, including

14% who’ve seen suspected drug deals on many occasions. (YouGov UK) March 10, 2023 Rising Energy

Costs And Long-Term Price Pressures On UK Farmers Most Likely To Be Seen As

Causes For Fruit And Vegetables Shortages As fruit and vegetable shelves go

empty in supermarkets across the UK, new research by Ipsos shows rising

energy costs and long-term price pressures on UK farmers are most likely to

be seen as key contributors to the shortages with 76% and 73% saying each respectively

has contributed a great deal or fair amount. Other key contributors,

according to people in the UK, include climate change/weather challenges in

countries from which food is imported (65%), agricultural labour shortages

(61%) and Britain leaving the EU (58%). (Ipsos MORI) 6 March 2023 7 In 10 Britons Do Not Think

The Government’s Policies Will Improve Public Services Almost two-thirds think Sunak’s

government has done a bad job managing the economy. The latest Ipsos

Political Monitor, taken, February 22nd to March 1st shows 70% of British

adults do not believe that the government’s policies will improve the state

of public services in the long term, with just 23 per cent thinking they

will. This marks a sharp fall in figures from March last year (2022) where

60% disagreed and 31% agreed, and is the worst set of results for a

government since Ipsos started asking this question in 2001. (Ipsos MORI) 7 March 2023 How Can Advertising Drive

Gender Equality Women had a difficult time during COVID-19

– more women lost jobs, had to give up income, or handled home education

while continuing to work. And with the current cost of living crisis,

Kantar’s Global

Issues Barometer shows that women are more susceptible to the

implications of recession and inflation, and also felt a lower sense of

wellbeing. Among the ads that men enjoy compared to women we saw higher

numbers of ads with rational messages (+3%) and more use of continuous

voiceovers (+2%) and ads with promotions (+2%). (Kantar) 07 March 2023 (Russia) Romir/M-Holding Research:

Results Of 2022 For The Three Leaders Of The Fast Food Market The research holding

"Romir" (part of "M-Holding") analyzed how the purchasing

behavior of Russians changed towards the most popular fast food restaurants

(QSR) in 2022: Tasty, KFC, Burger King. In total, the top three fast food

restaurants maintained turnover in 2022 (compared to 2021, turnover increased

by 1%). However, the number of visits at the same time decreased by 16% in

annual dynamics, which indicates an increase in prices or the average

receipt. (Romir) 01 March 2023 (Germany) Almost Two Out Of Five Germans

Use Account Sharing For Their Streaming Subscriptions Almost two out of five Germans (38

percent) share their streaming accounts, including 23 percent within their

own household, 8 percent outside the household and 7 percent

both. Overall, men use account sharing more frequently than women (40

vs. 35 percent). 16 percent of all respondents in Germany say that they do

not share their video or audio streaming accounts with others; men also make

this statement more frequently than women (18 vs. 14 percent). These are

the results of a survey by YouGov in cooperation with Statista. (YouGov Germany) March 09, 2023 Every Fourth German Can Imagine

A Workation For Himself 25 percent of Germans have not yet

done any workation, but can imagine doing so in the future. The “potential

workationers” are significantly more common between the ages

of 45 and 54 compared to the general population (25 vs. 20 percent). In

this potential group, 36 percent have a university or technical college

degree (vs. 30 percent of the total population). 75 percent of

"potential workationers" say that stress makes them ill (vs. 66

percent), 51 percent like to volunteer for a good cause in their free time

(vs. 44 percent). 88 percent say it's okay to be a father these days

(vs. 78 percent), and 79 percent say it's important to be physically

attractive (vs. 69 percent of the general German population). (YouGov Germany) March 09, 2023 NORTH AMERICA (USA) Immigrants And Children Of

Immigrants Make Up At Least 15% Of The 118th Congress Immigrants and children of

immigrants account for at least 15% of the 118th Congress, a share that has

steadily grown over the past three Congresses. At least 81 voting members of

Congress are foreign born or have at least one parent who was born in another

country, according to a Pew Research Center analysis of members’ biographical

information gathered from the Congressional Research Service, news articles,

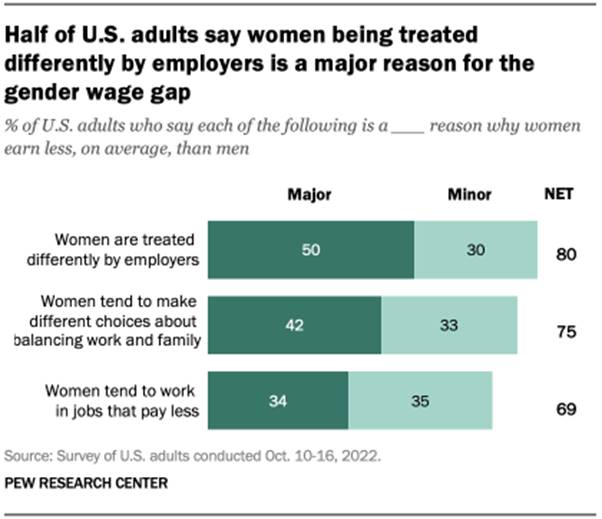

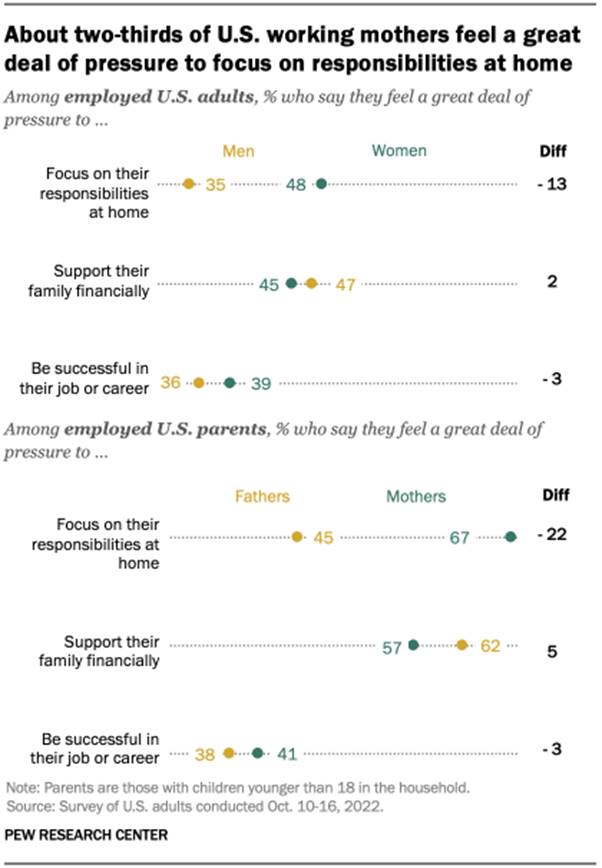

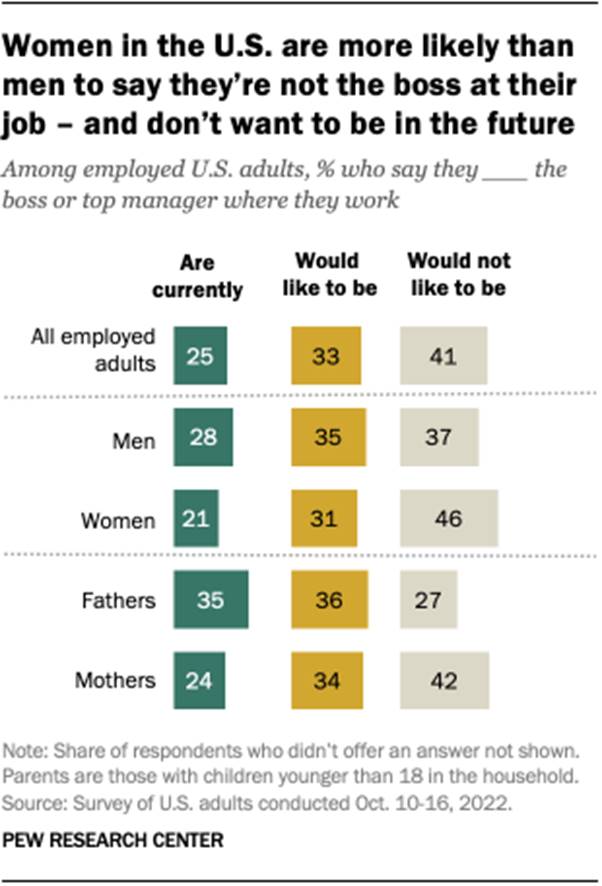

congressional offices and other sources. (PEW) FEBRUARY 28, 2023 Gender Pay Gap In U.S. Hasn’t

Changed Much In Two Decades The gender gap in pay has remained

relatively stable in the United States over the past 20 years or so. In 2022,

women earned an average of 82% of what men earned, according to a new

Pew Research Center analysis of median hourly earnings of

both full- and part-time workers. These results are similar to where the pay

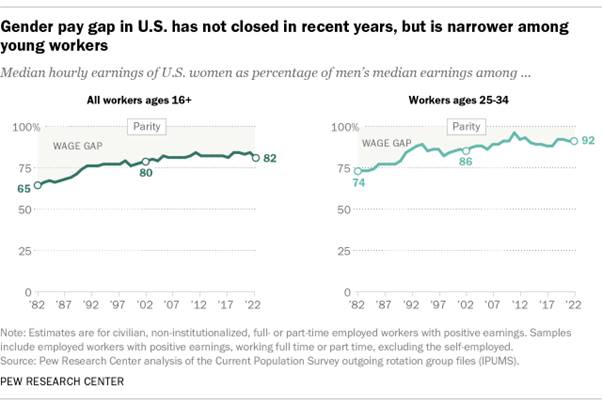

gap stood in 2002, when women earned 80% as much as men. In 2022, women ages

25 to 34 earned an average of 92 cents for every dollar earned by a man in

the same age group – an 8-cent gap. By comparison, the gender pay gap among

workers of all ages that year was 18 cents. (PEW) MARCH 1, 2023 Mental Health And The

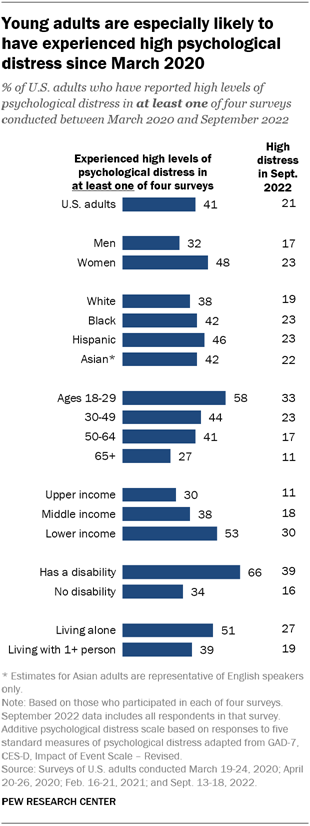

Pandemic: What U.S. Surveys Have Found At least four-in-ten U.S. adults

(41%) have experienced high levels of psychological distress at some point

during the pandemic, according to four

Pew Research Center surveys conducted between March 2020 and

September 2022. Young adults are especially likely to have faced high levels

of psychological distress since the COVID-19 outbreak began: 58% of Americans

ages 18 to 29 fall into this category, based on their answers in at least one

of these four surveys. Women are much more likely than men to have

experienced high psychological distress (48% vs. 32%), as are people in

lower-income households (53%) when compared with those in middle-income (38%)

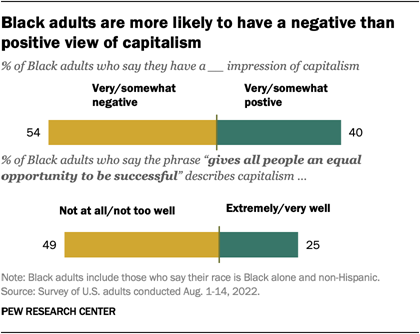

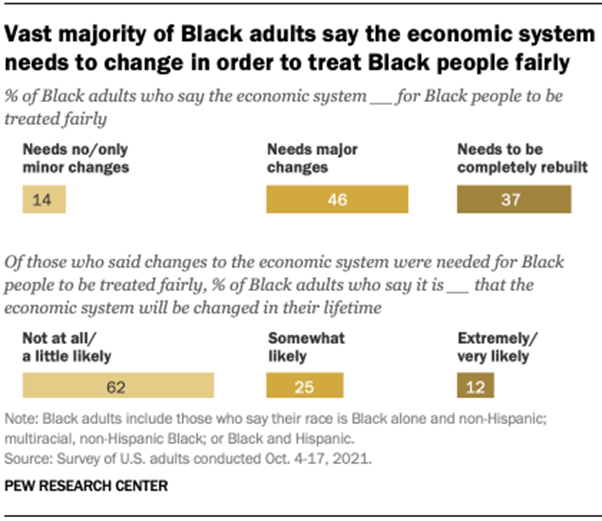

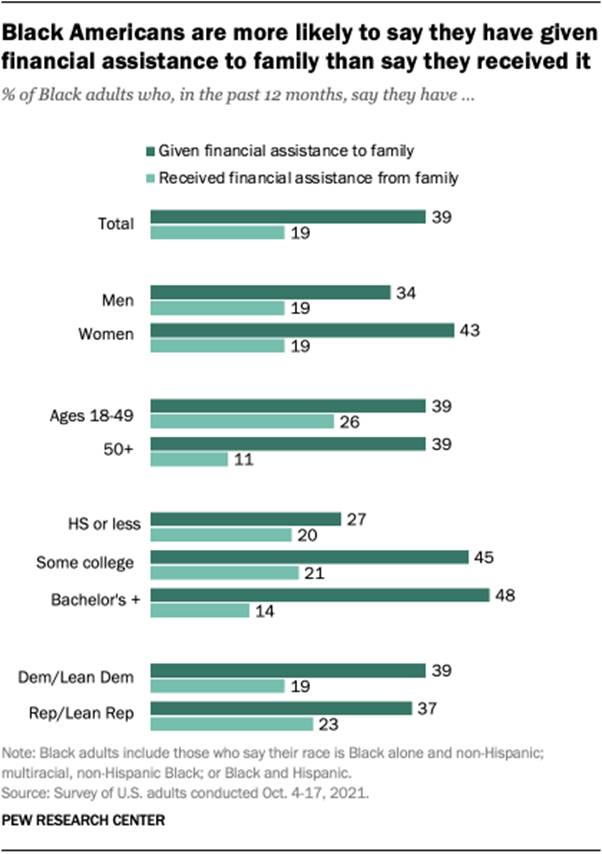

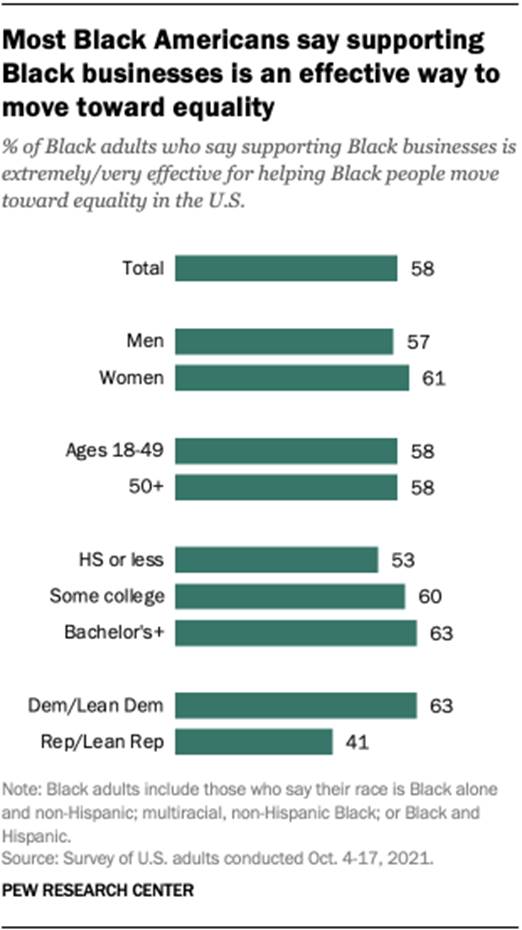

or upper-income (30%) households. (PEW) MARCH 2, 2023 Black Americans

View Capitalism More Negatively Than Positively But Express Hope In Black

Businesses Today, most Black adults say the

U.S. economic system does not treat Black people fairly. And though they are

increasingly dissatisfied with capitalism, most Black adults say supporting

Black businesses will help achieve equality, according to recent Pew Research

Center surveys. Four-in-ten Black adults held a very or somewhat positive

view of capitalism in 2022, down from 57% in 2019. Views of capitalism also

grew more negative among other racial and ethnic groups during this period,

but the movement was particularly pronounced among Black Americans. (PEW) MARCH 8, 2023 (Canada) Eight In Ten (79%) Canadians

Believe Acts Of Violence Will Increase In Canada In The Future A new Ipsos poll conducted on

behalf of Global News finds that Canadians feel more violence in the country

may be on the horizon (79%). For the six in ten (58%) who report feeling that

there has been an increase in violence in their community since the COVID-19

pandemic began, the pandemic’s impacts on mental health (65%), the breakdown

of common values (51%), and economic uncertainty (48%) are believed to be the

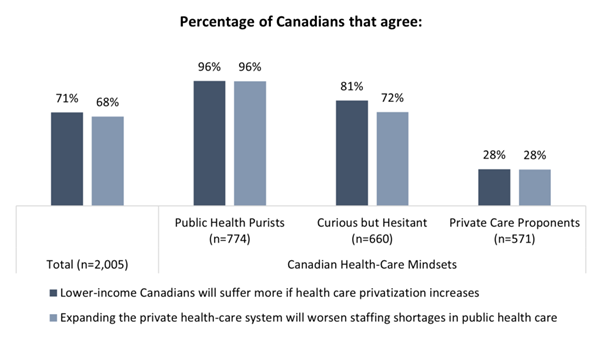

main causes. (Ipsos Canada) 9 March 2023 Public Purists,

Privatization Proponents And The Curious: Canada’s Three Health-Care Mindsets A new study from the non-profit

Angus Reid Institute finds Canadians divided about privatization – and

disagreement over how to define it. Two-in-five (39%) are Public Health

Purists: they see little to no place for privatization and say any movement

in this direction only exacerbates current challenges within the system. On

the other end of the spectrum, approximately three-in-ten (28%) are Private

Care Proponents: they say increasing privatization is a necessary evolution

in Canadian health care and are supportive of seeing a host of hybrid care

options from other countries such as Australia, Germany, and Britain brought

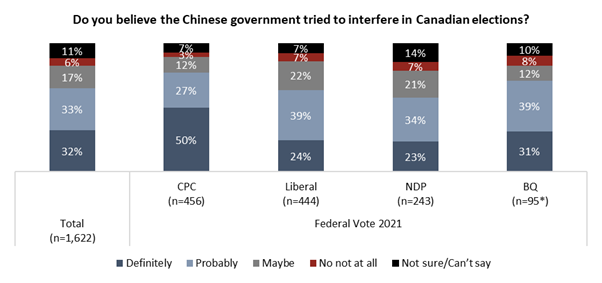

to their own provinces. (Angus Reid Institute) February 27, 2023 China, Canada And

Challenging Diplomacy: Two-In-Three Canadians Believe Beijing Did Attempt

Election Interference Amid allegations Beijing attempted

to influence the outcomes of both the 2019 and 2021 elections

to ensure the federal Liberal Party formed a minority government over the

opposition Conservatives, two-thirds of adult Canadians express belief that

Beijing “definitely” (32%) or “probably” (33%) tried to meddle. Majorities

across the political spectrum are of this view, while half of Canadians say

this attempted interference represents a serious threat to democracy (53%). (Angus Reid Institute) March 1, 2023 Lacking The Will:

Half Of Canadians Say They Don’t Have A Last Will And Testament, Including

One-In-Five Aged 55+ New data from the non-profit Angus

Reid Institute finds 50 per cent of Canadians in a similar boat as Harris

before his tragic accident. Half of adults in this country say they don’t

have a last will and testament; a proportion that remains consistent since

ARI surveyed on this subject five years ago. As one might expect, younger

Canadians are less likely to have one. Four-in-five Canadians younger than 35

say they do not have a will, but even half of those between the ages of 45

and 54 say the same. (Angus Reid Institute) March 7, 2023 Islamophobia In

Canada: Four Mindsets Indicate Negativity Is Nationwide, Most Intense In

Quebec A new study from the non-profit

Angus Reid Institute finds unfavourable views of Islam prevalent across the

country at varying levels and highest in Quebec. Indeed, two-in-five

Canadians outside of Quebec (39%) hold an unfavourable view of Islam. In

Quebec that number reaches half (52%). These views take more concrete forms,

however, than just the overall sentiment that the religion receives. Its

followers face the risk of being unwelcome in a number of areas of Canadian

society. (Angus Reid Institute) March 13, 2023 AUSTRALIA Think News Brands And Roy

Morgan Total News Figures Show 20.6 Million Australians Over The Age Of 14

Engage With News Every Month The readership figures, produced by

Roy Morgan for ThinkNewsBrands, refer to the 12 months to December 2022 and

show that Total News reaches 97 per cent of the population over the age of

14. Total News represents all news brands across print and digital as well as

standalone news websites. The latest release of Total News readership shows a

slight softening for news consumption, down 0.5 per cent compared to the same

period in 2021 with 20.6 million Australians continuing to consume news in a

four-week period. (Roy Morgan) February 27, 2023 Four In Five Shoppers

Believe Buying Australian-Made Is Important New research shows Australians’

preference for Australian-made goods hasn’t wavered. The data collected by

Australian market research company, Roy Morgan, found that more than four in

five (86%) Australians say buying Australian-made products is important to

them. While very few people, only 2%, said buying Australian-made wasn’t

important to them. Most Australians (67%) stated in the survey that they

‘often’ or ‘always’ buy Australian-made products, citing supporting local

jobs and the economy as their reason for doing so, followed by the quality or

reliability of Australian-made products. (Roy Morgan) February 27, 2023 ‘Mortgage Stress’

Increases To Its Highest Since April 2012 With 24.9% Of Mortgage Holders Now

‘At Risk’ The proportion of mortgage holders

now considered ‘At Risk’ of mortgage stress in the three months to January

2023 (24.9%) is the highest for over a decade since June 2012 and is now

significantly above the long-term average of 22.8% stretching back to early

2007. The number of Australians ‘At Risk’ of mortgage stress has increased by

486,000 over the last year as the RBA increased interest rates for nine

consecutive monthly meetings. Official interest rates are now at 3.35% in

February 2023, the highest official interest rates since October 2012 over a

decade ago. (Roy Morgan) February 28, 2023 Australian Full-Time

Employment Hit A Record High Above 8.9 Million In February As Unemployment

Falls 0.6% To 10.1% Australian employment increased by

99,000 to 13,517,000 in February. The increase was driven by an increase in full-time

employment, up 48,000 to a new record high of 8,949,000 while part-time

employment also increased, up 51,000 to 4,568,000. 1,521,000 Australians were

unemployed (10.1% of the

workforce) in February, a decrease of 86,000 from January

with fewer people looking for full-time work, down 42,000 to 602,000 and

fewer people looking for part-time work, down 44,000 to 919,000. (Roy Morgan) March 06, 2023 ANZ-Roy Morgan Consumer

Confidence At 79.9 – Virtually Unchanged For Second Straight Week In Early

March Consumer Confidence had mixed

results around the country and was up in Queensland and South Australia, down

in New South Wales and Western Australia and unchanged in Victoria. Now 21%

of Australians (down 1ppt) say their families are ‘better off’ financially

than this time last year compared to 48% (unchanged) that say their families

are ‘worse off’ financially. Looking forward, under a third of Australians,

32% (unchanged), expect their family to be ‘better off’ financially this time

next year while just over a third, 35% (unchanged), expect to be ‘worse off’. (Roy Morgan) March 07, 2023 Over Half Of

APAC’s Consumers (54%) Say That Better Money Management Is On Their List Of

Goals For This Year Close to half (47%) of all

Australian residents say there has been no change in their household finances compared to one

month ago. Data from YouGov Profiles reflect cumulative responses over the

past 52 weeks. Three in ten (31%), however, report worsening household finances, while

less than one in five (18%) say their financial situation has improved. Higher income households are significantly more likely

to report that their financial situation has improved (11-15 percentage points higher on average

than middle to lower income households) and significantly less likely to say

their finances have worsened.

(YouGov Australia) February 28, 2023 MULTICOUNTRY STUDIES Confounding And Confirming

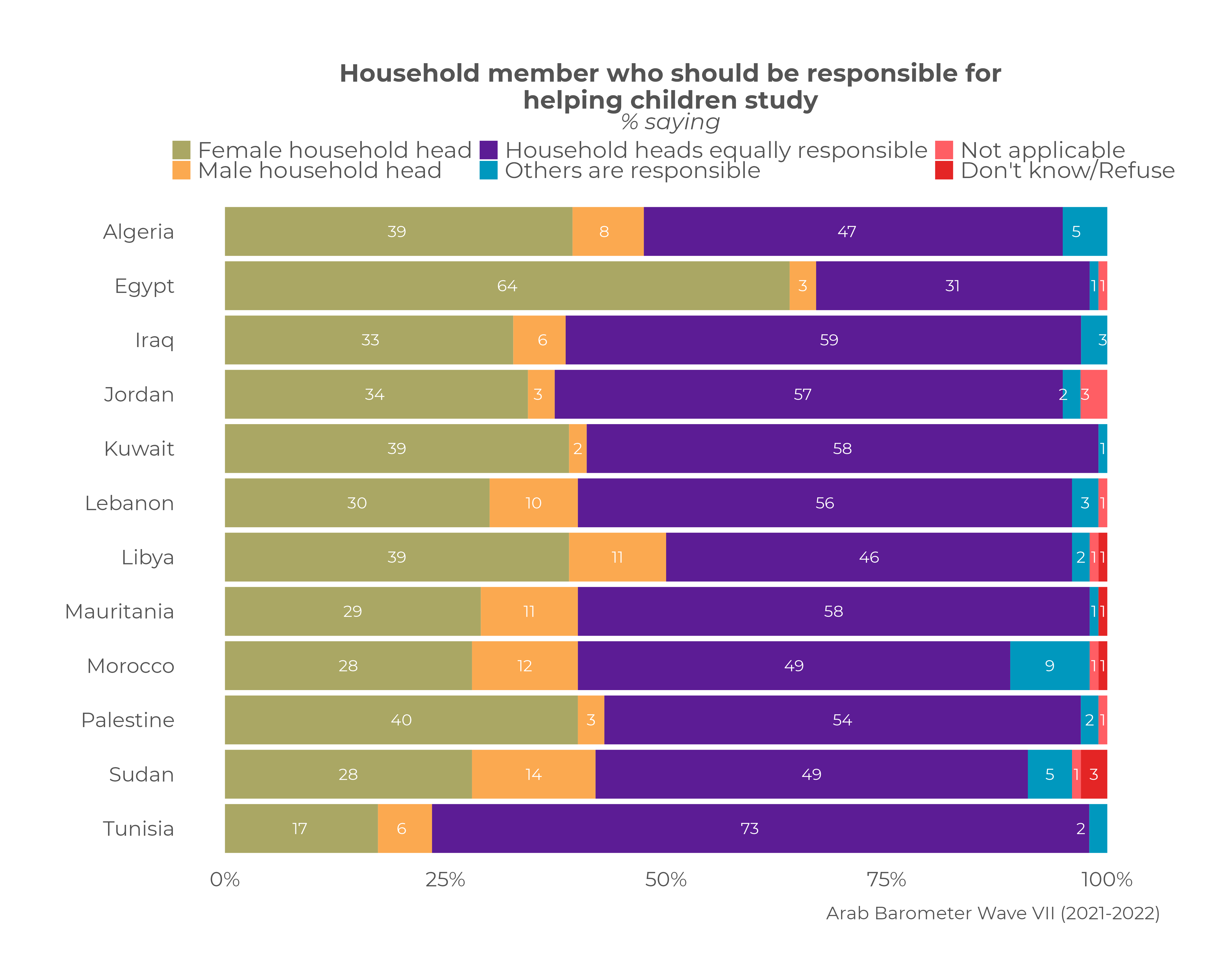

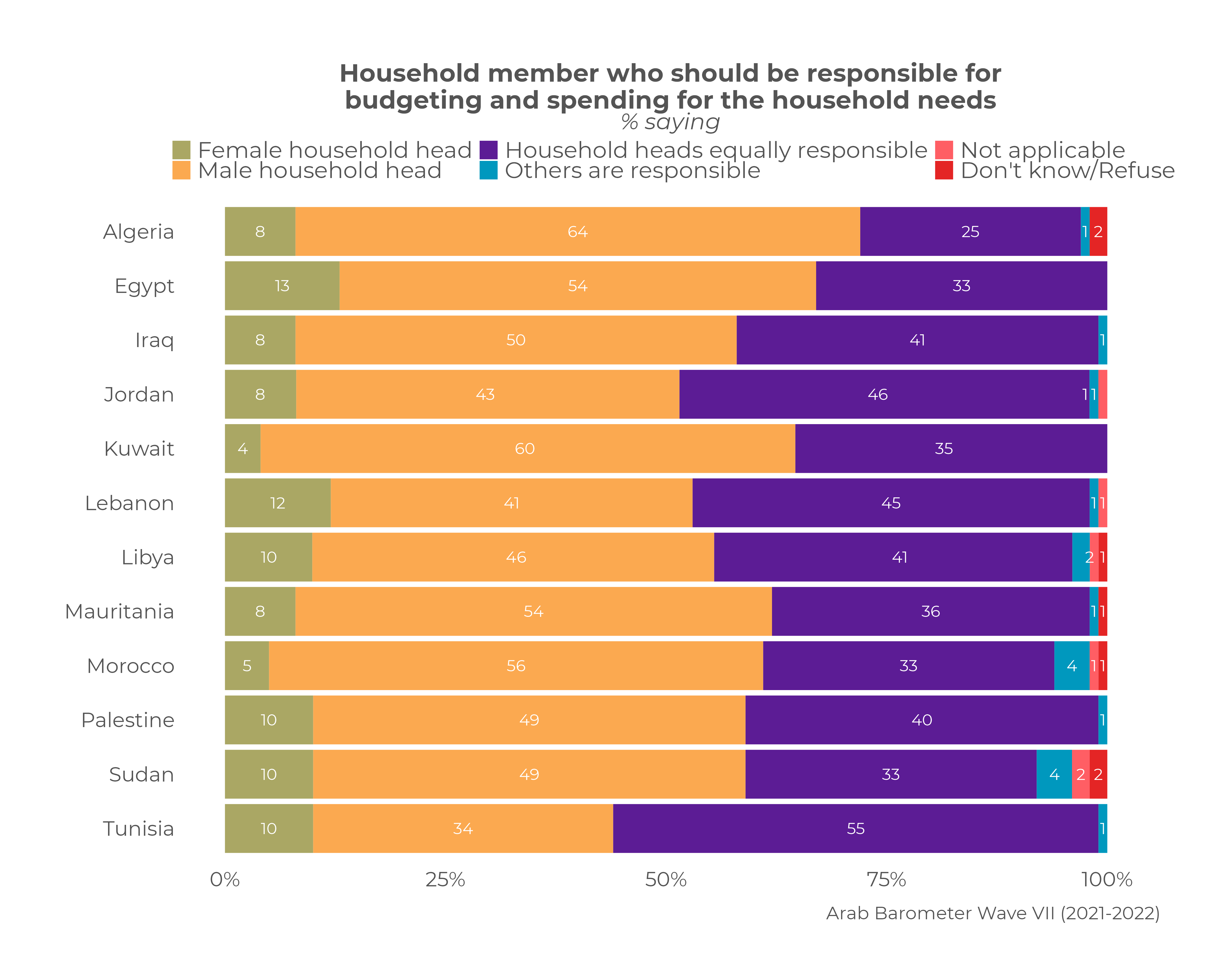

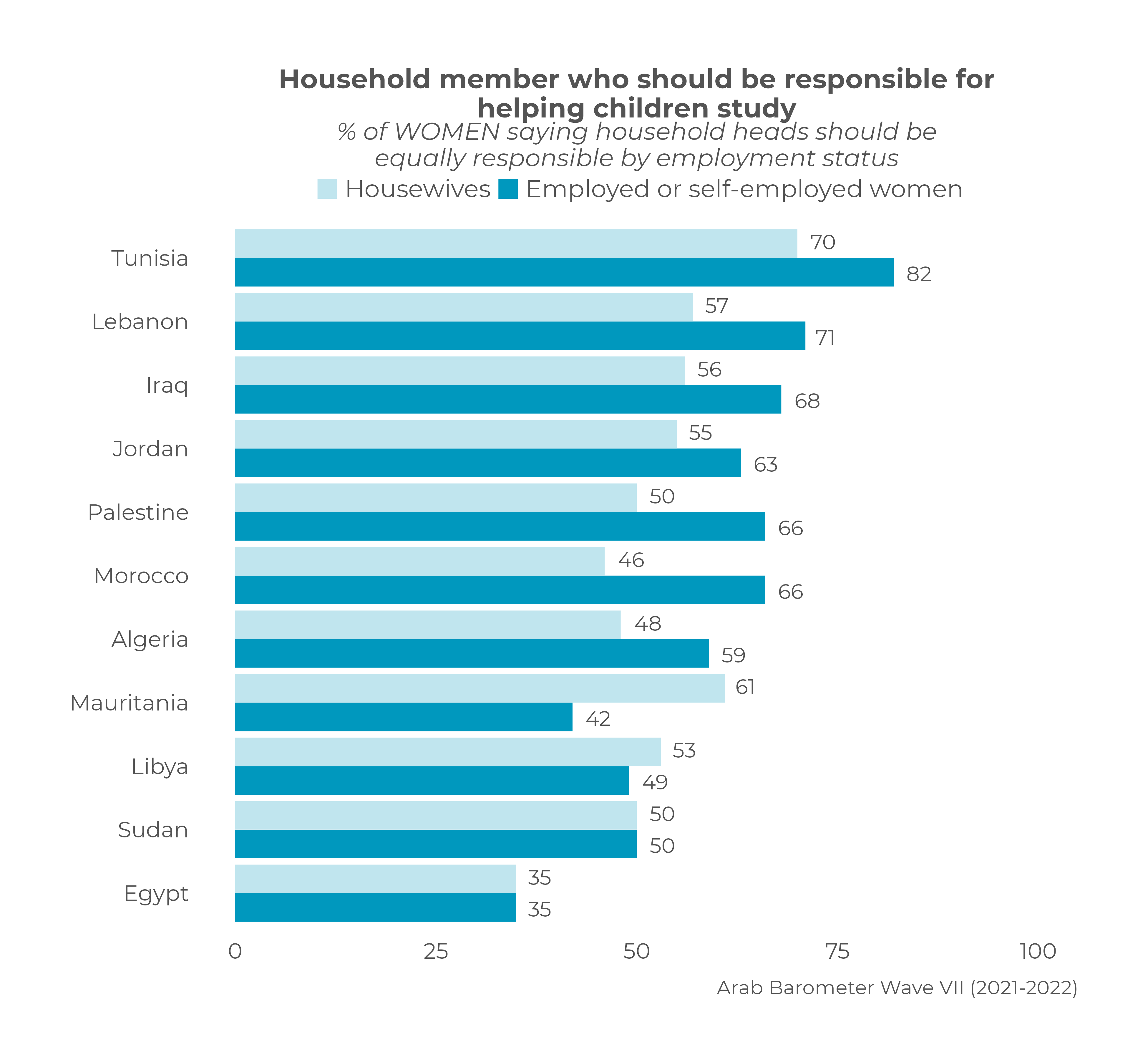

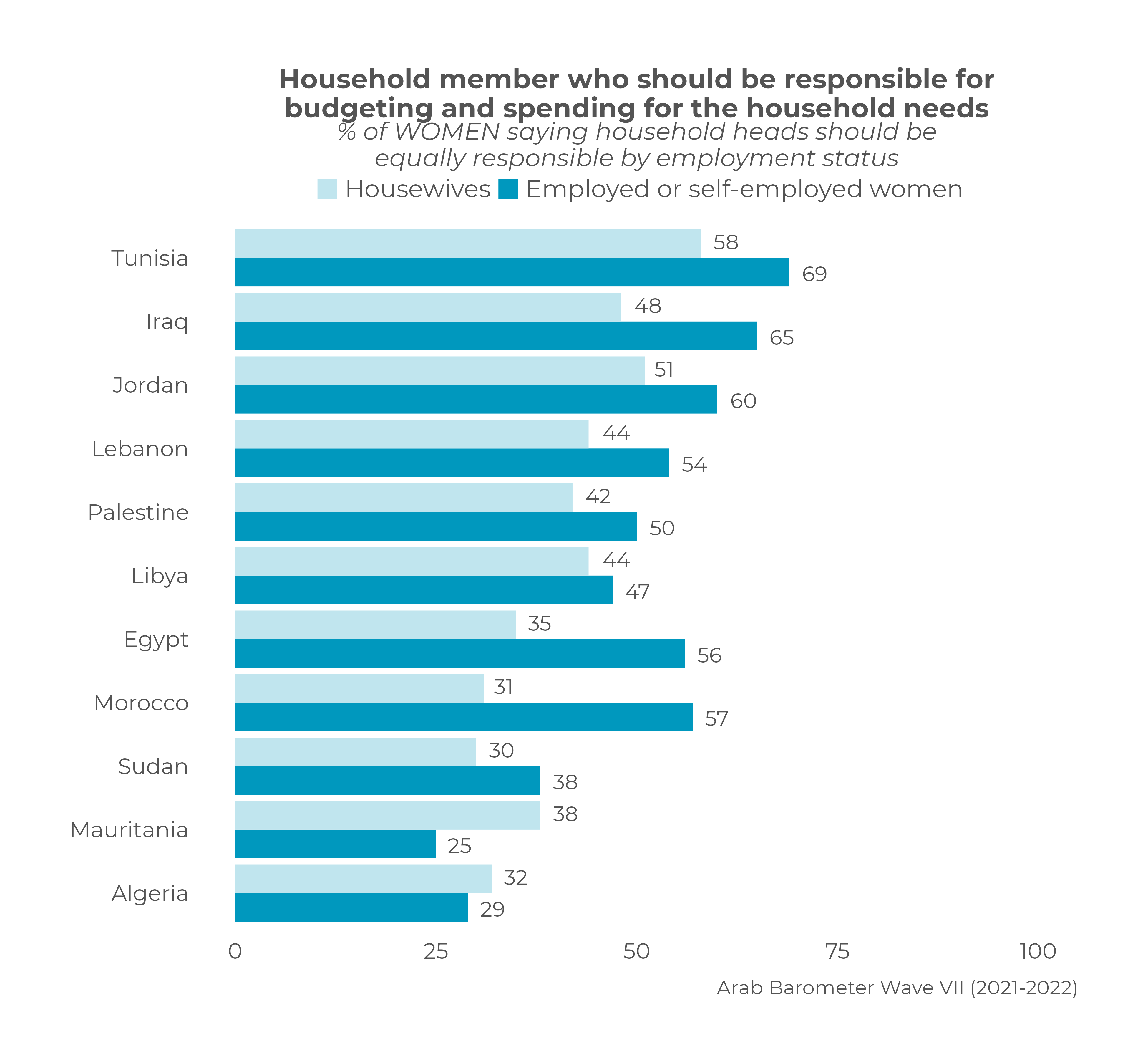

Expectations On The “Care Economy” In MENA, A Survey In 12 Arab Nations Arab Barometer findings from 12

countries surveyed in the seventh wave (2021-2022) partially confound

expectations on unpaid care work in the region. Where it is often assumed

that childcare—including help with schoolwork—is relegated exclusively to

women, survey results instead suggest that most citizens believe helping

children study is a responsibility that should be shared by both male and

female household heads, regardless of who currently completes this

responsibility. Nearly half of citizens or more in nine out of 12 countries

say household heads should be equally responsible for helping children study. (Arabbarometer) March 6, 2023 Female Political

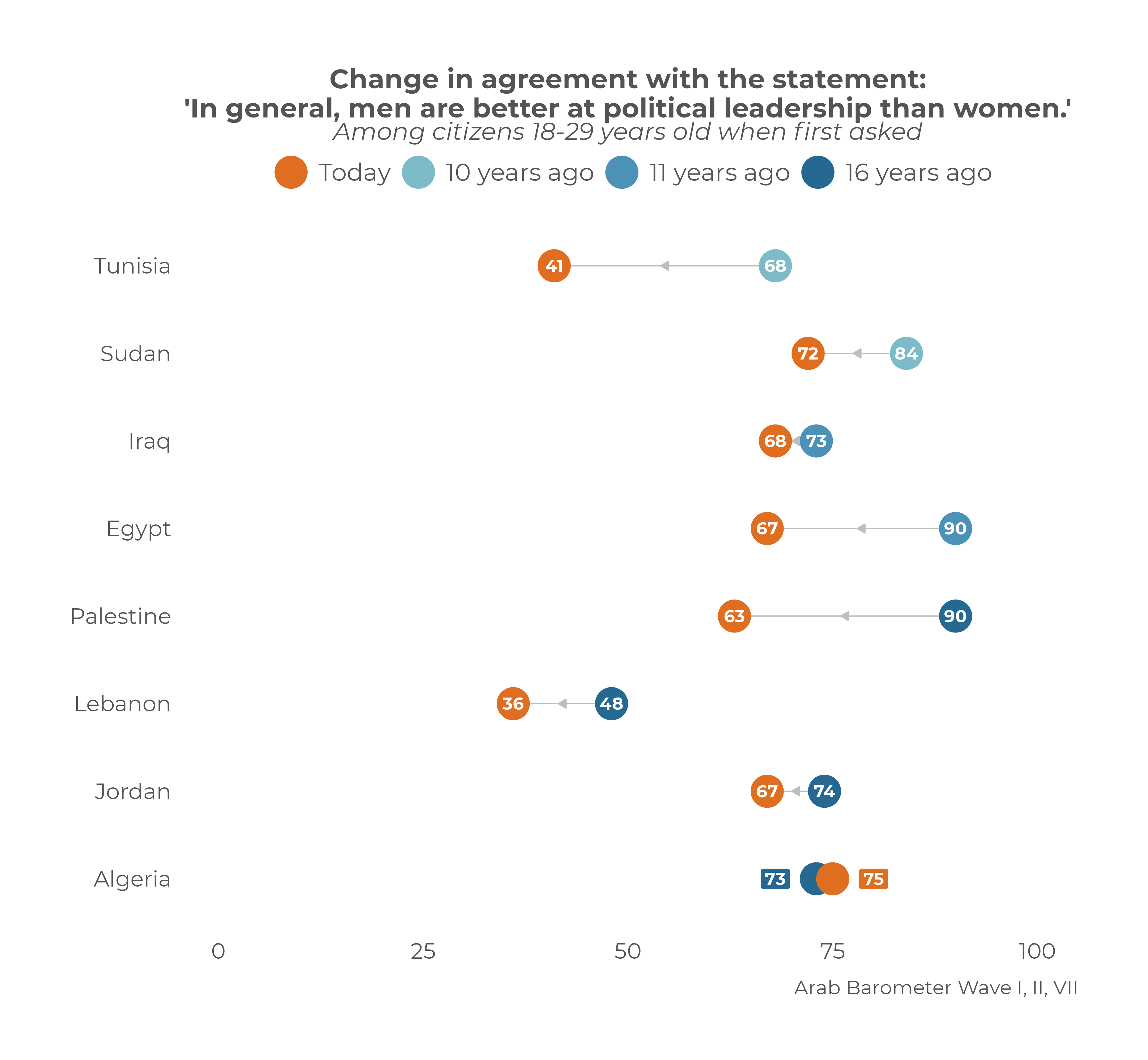

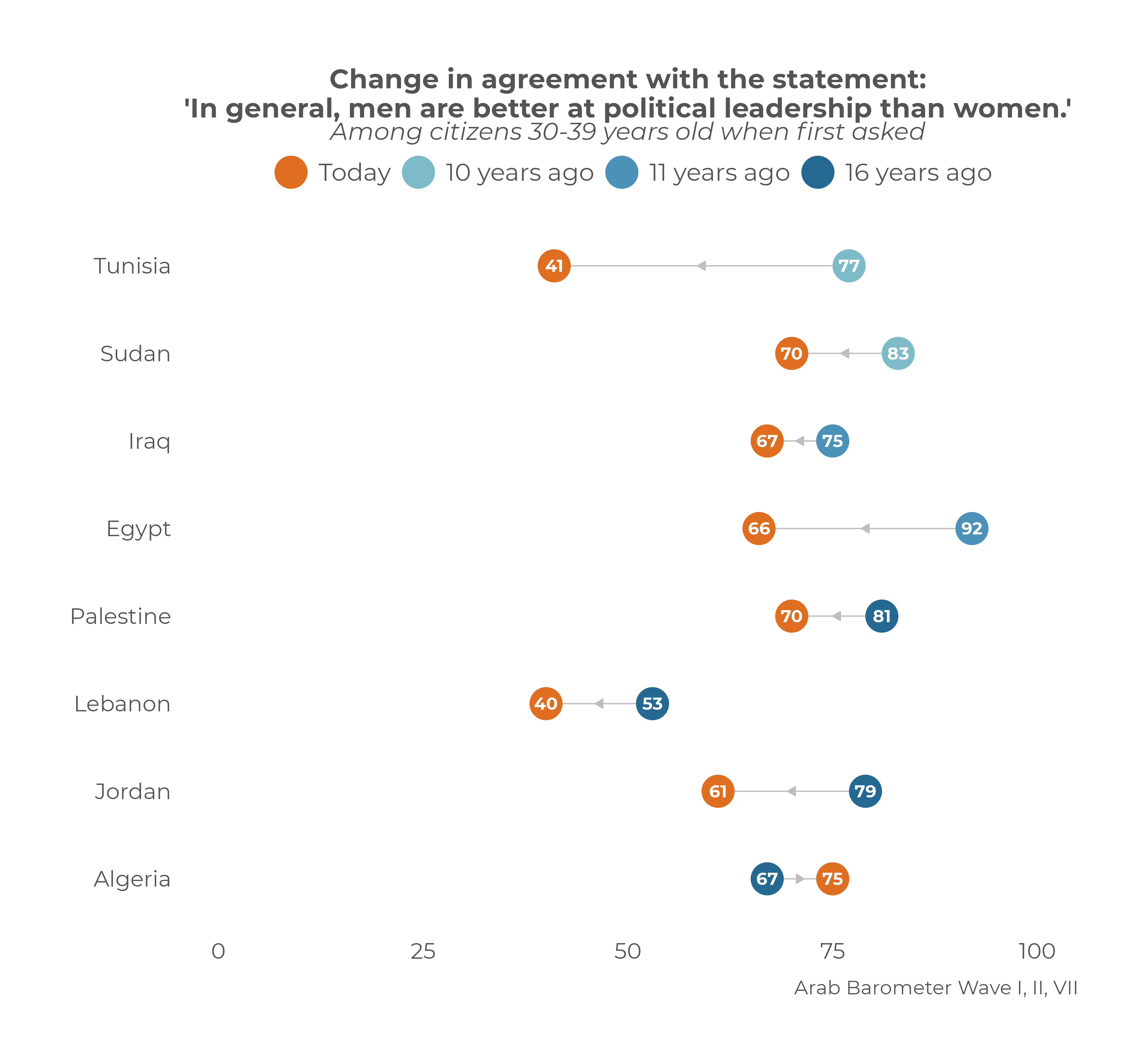

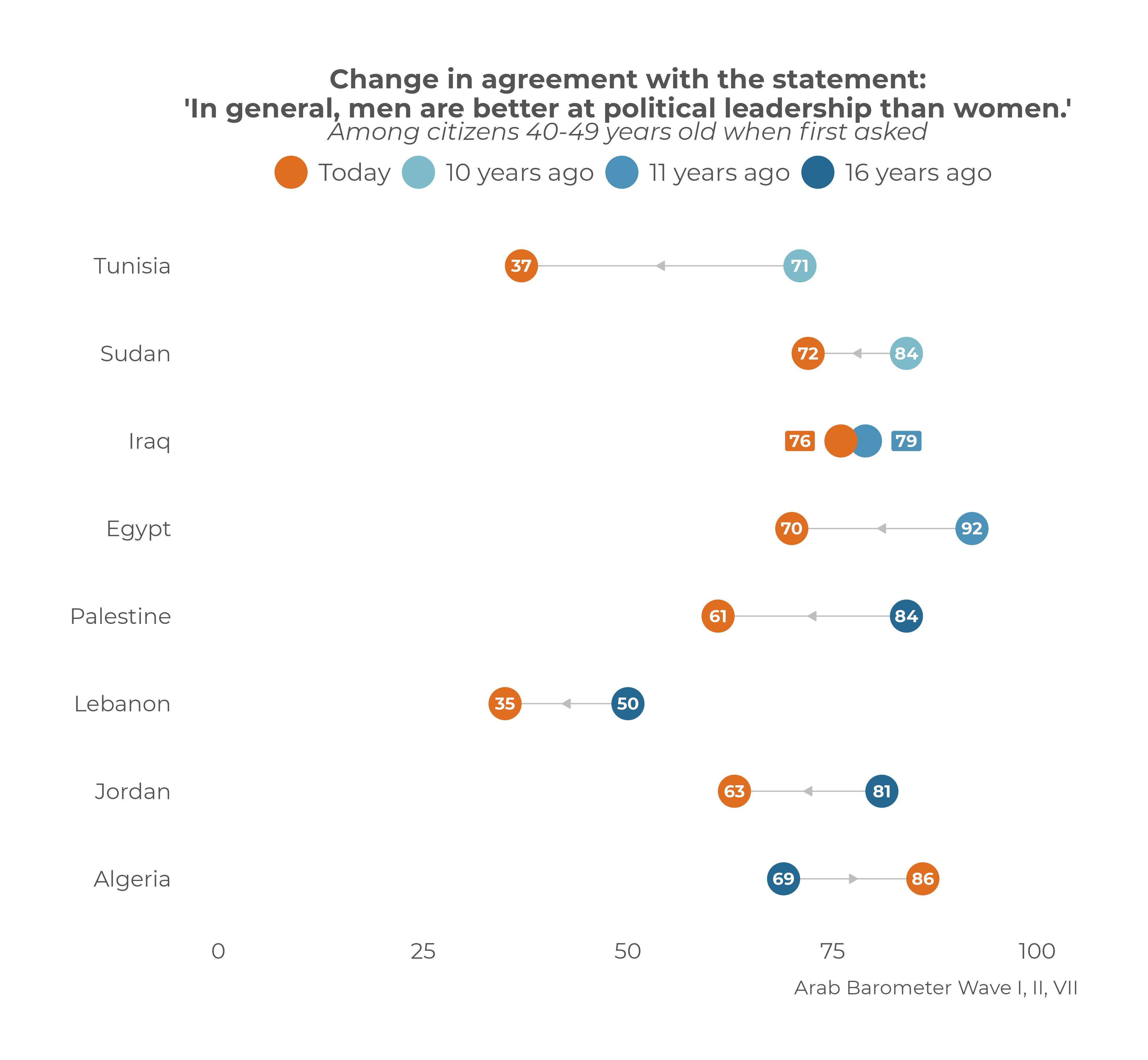

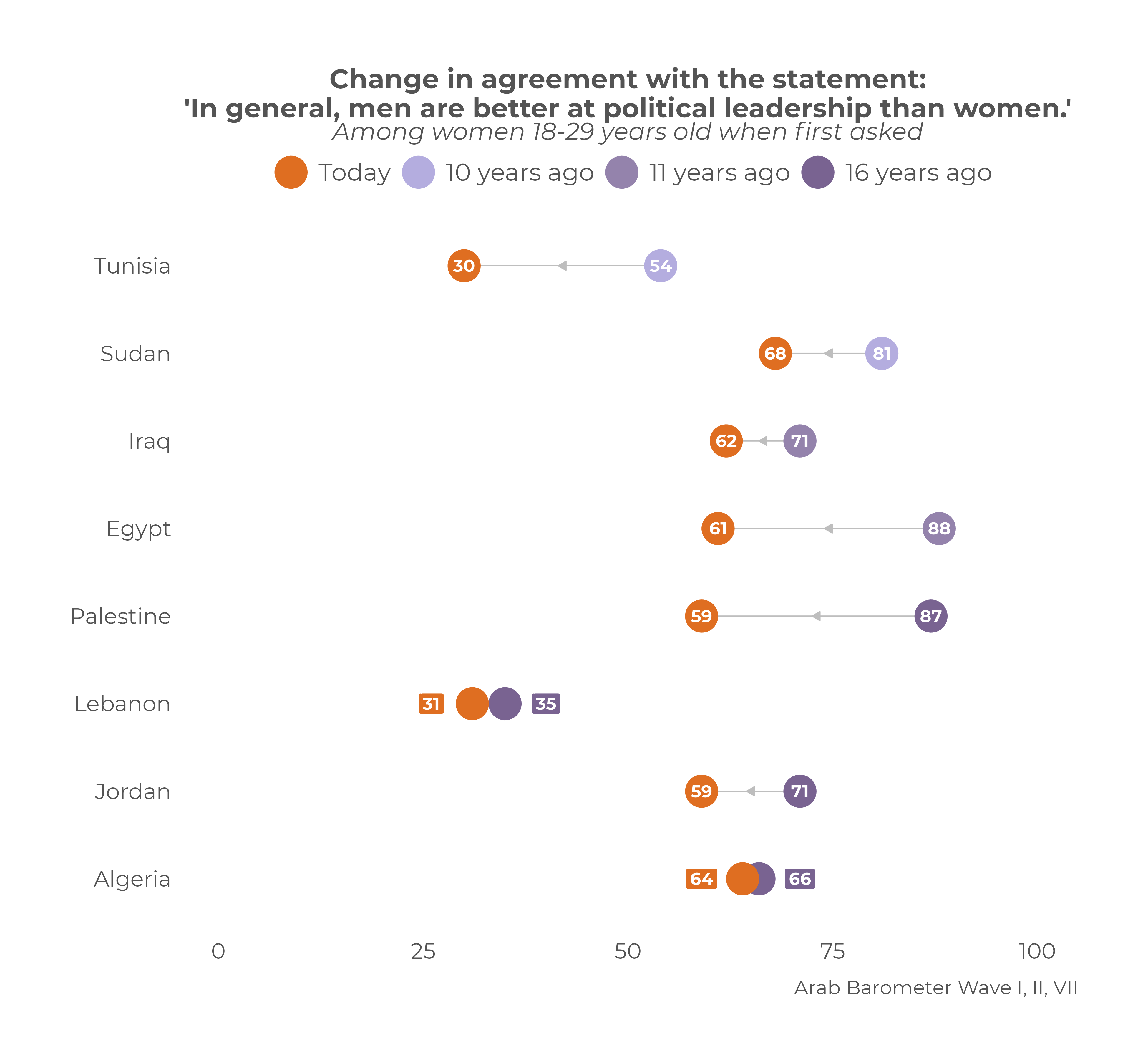

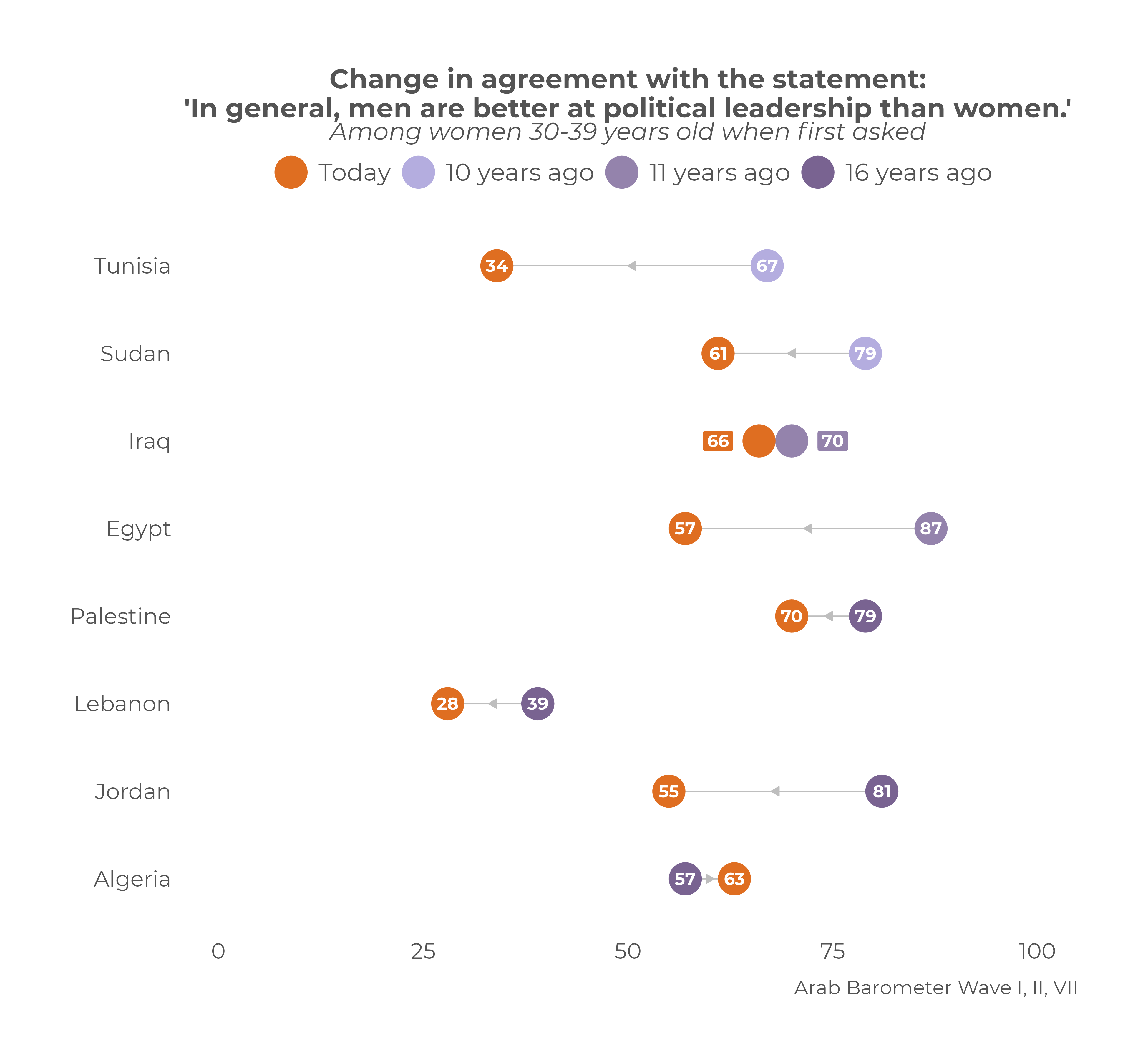

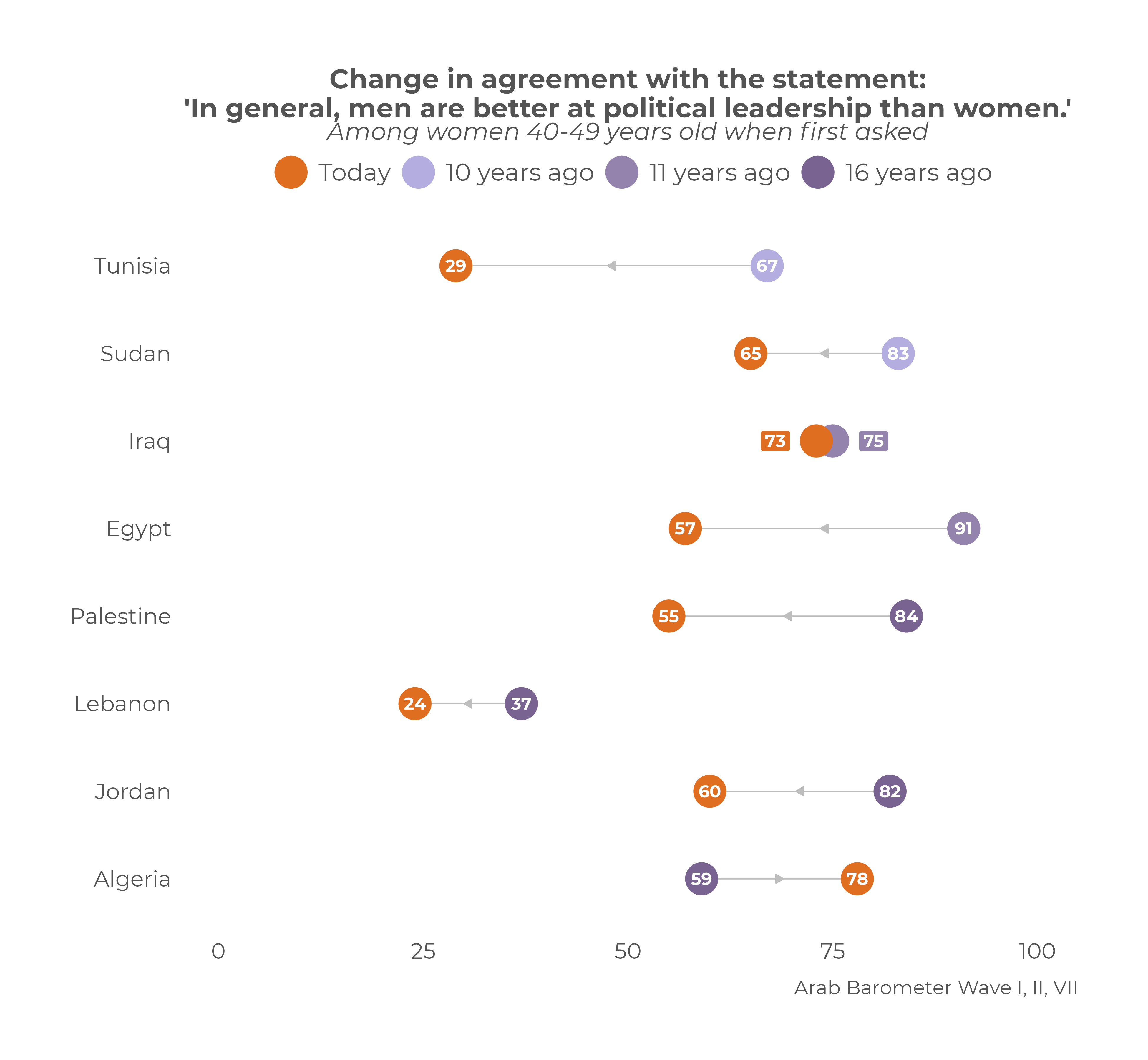

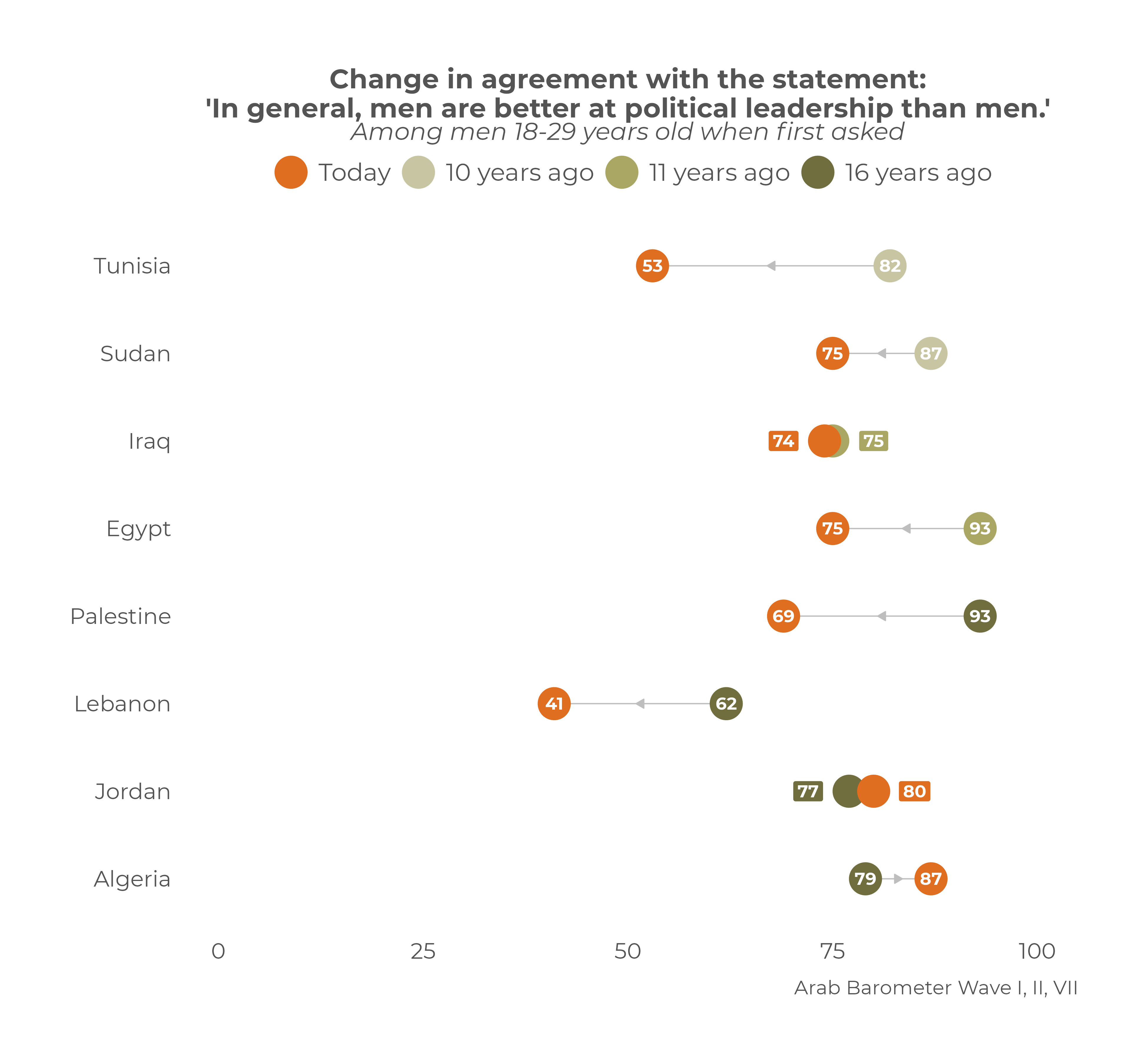

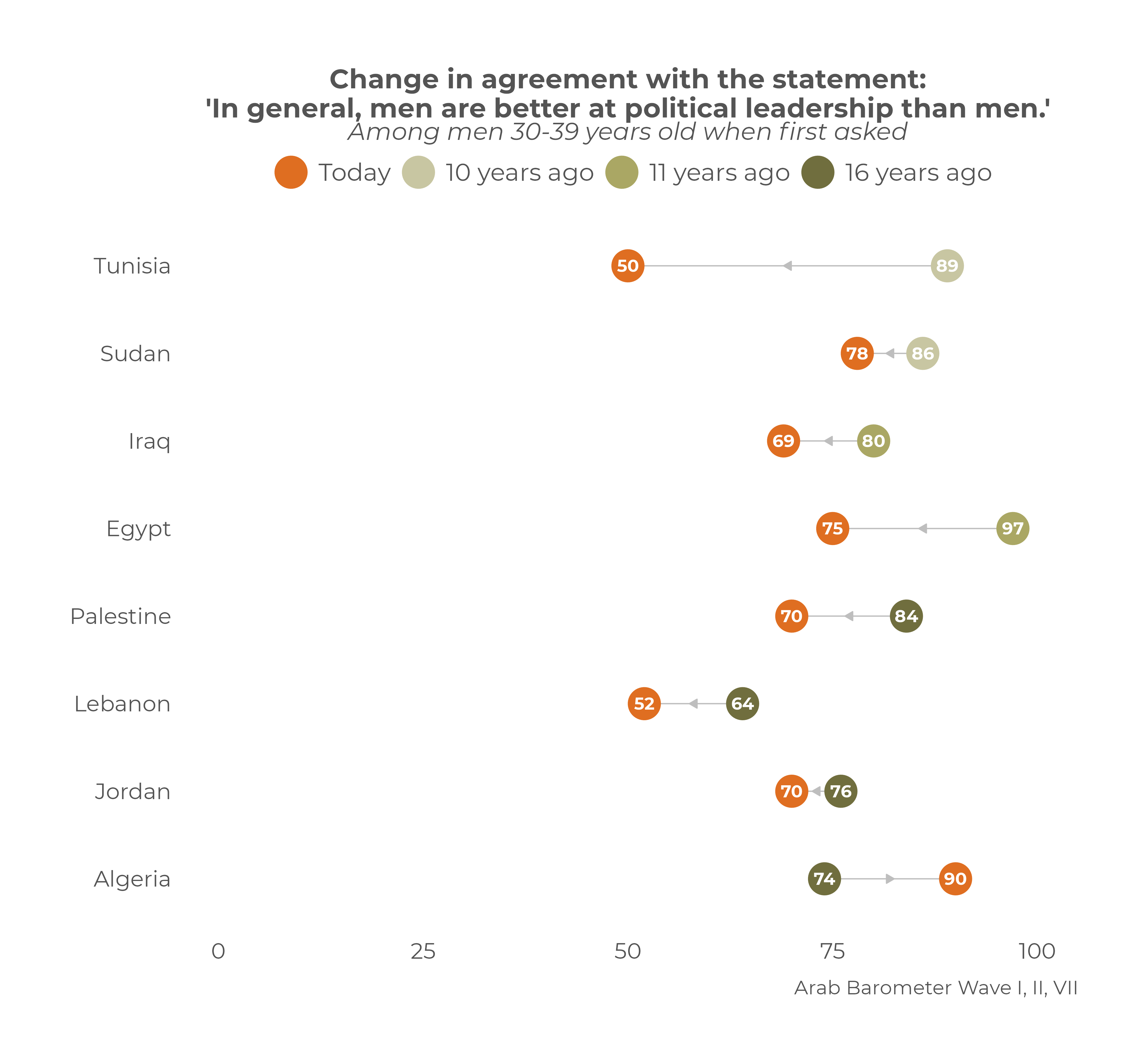

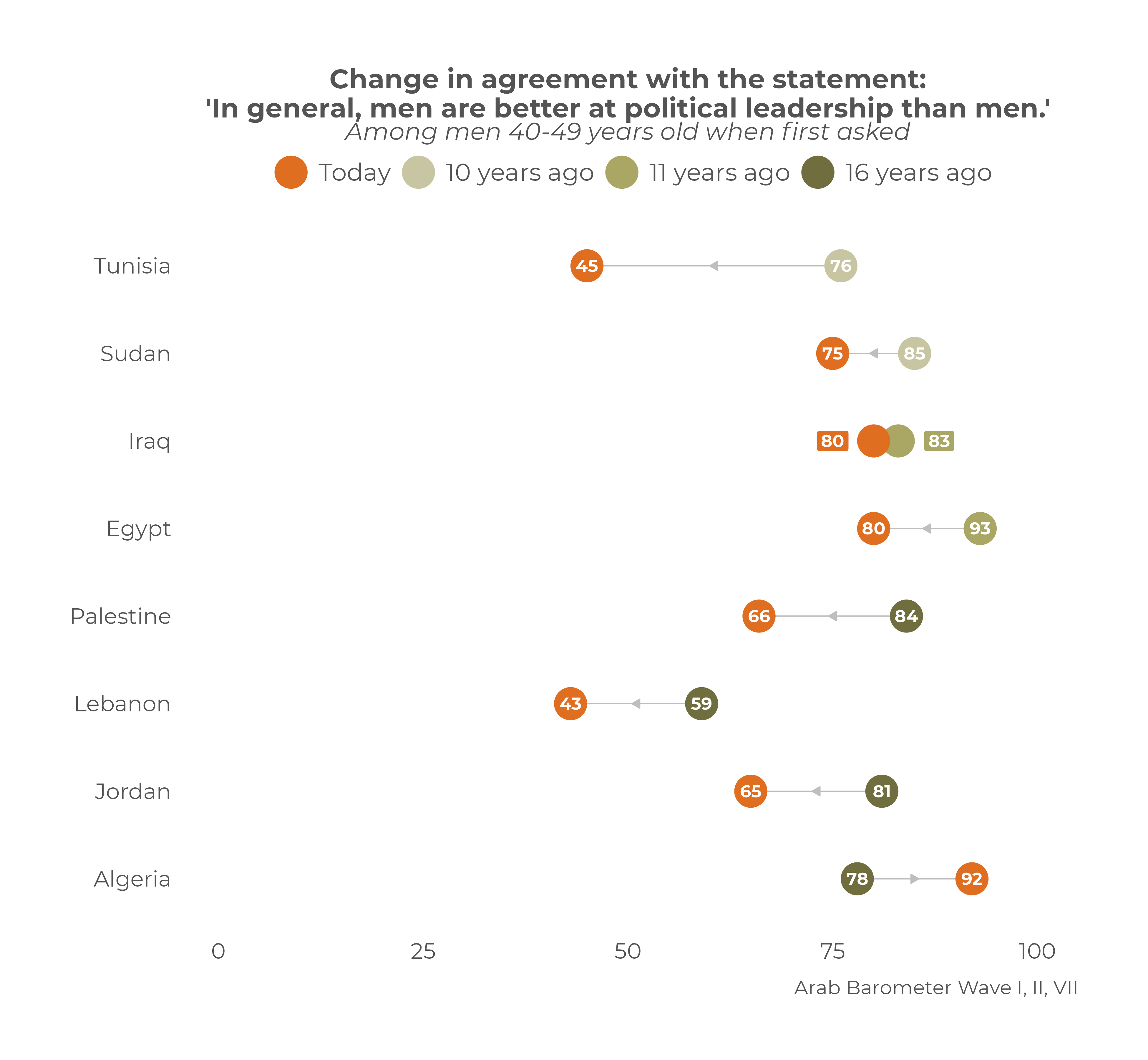

Participation Inspires Confidence In Female Political Leadership In MENA, An

8 Country Survey Eight of the countries Arab

Barometer surveyed during its seventh wave were also surveyed at least ten

years ago during the first or second wave.[2] This allows us to compare a

nationally representative cross-section of different age groups to see how

their opinions have changed since they were first surveyed. For this

analysis, we broke the population up into three age cohorts. Cohort I

consists of citizens who were 18 to 29 the first time they were surveyed;

Cohort II is citizens originally aged 30 to 39; and Cohort III is citizens

originally aged 40 to 49.[3] Except for a small overlap in Cohort I, the

citizens in question have now [4] aged out of their original cohort. (Arabbarometer) March 6, 2023 International Women's Day:

Global Opinion Remains Committed To Gender Equality, But Half Now Believe It

Is Coming At The Expense Of Men, A 32-Country Survey A new global study conducted

in 32 countries by Ipsos in collaboration with the Global Institute for

Women’s Leadership at King’s College London for International Women’s Day

shows that: Two-thirds (68% globally, 63% in the U.S.) agree there is

currently inequality between men and women in terms of social, political,

and/or economic rights in their country, down slightly from 2017. However, 1

in 2 globally (54%) and more than 1 in 3 in the U.S. (37%) say that when it

comes to giving women equal rights with men, things have gone far enough in

their country – proportions that have gradually increased since 2019. (Ipsos USA) 7 March 2023 Out Of The 64

Countries That Were Surveyed, South Korea Tops Security Preference For US,

Pakistan Tops Preference For China, While Serbia Tops The Preference For

Russia And Sweden For EU For Security Partnership: GIA And Gallup &

Gilani Pakistan According to a survey conducted by

Gallup International Association, out of the 64 countries that were surveyed,

South Korea tops security preference for US, Pakistan tops preference for

China, while Serbia tops the preference for Russia and EU for security

partnership. The question asked was “Which of the following would you prefer

your country to partner with for security – the US, China, Russia, or The

EU?” 84% people from South Korea said USA, 54% from Pakistan said China, 53%

from Serbia said Russia and 69% from Serbia said EU. (Gallup Pakistan) March 08, 2023 Source: https://gallup.com.pk/wp/wp-content/uploads/2023/03/08-March-GIA-PR_merged.pdf Reflections On

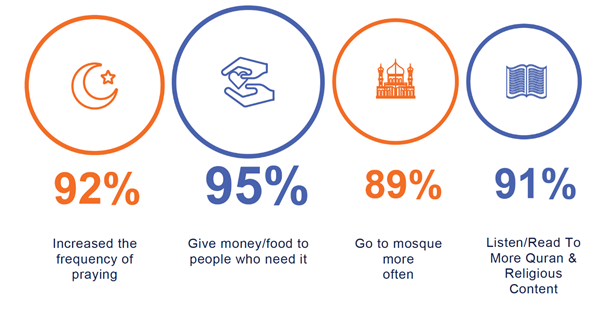

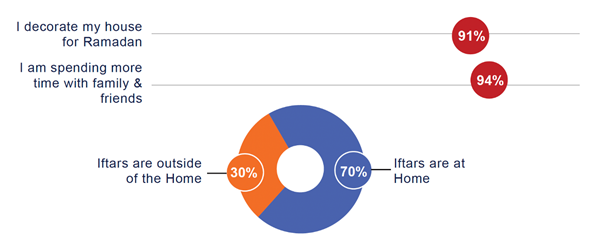

Ramadan, A Look Into Changing Habits Of KSA, UAE And Egypt Ramadan is a significant month for

Muslims in the MENA region, and while it is a time of spiritual reflection

and self-discipline, it is also a time of celebration and community. It’s

touted as a period for personal spiritual growth and development, but it is

also a time to strengthen family and community bonds. In the MENA region,

there has historically been a significant increase in media consumption

during the month of Ramadan. Partly due to the fact that many popular

television shows and dramas are broadcast during this time, and so viewership

naturally increases. (Ipsos UAE) 8 March 2023 Source: https://www.ipsos.com/en-ae/reflections-ramadan Data Dive: Looking Back At

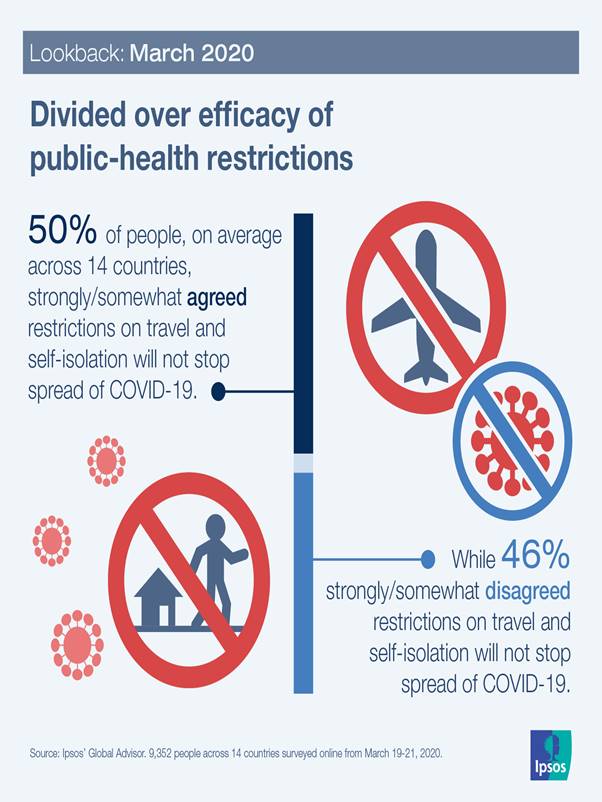

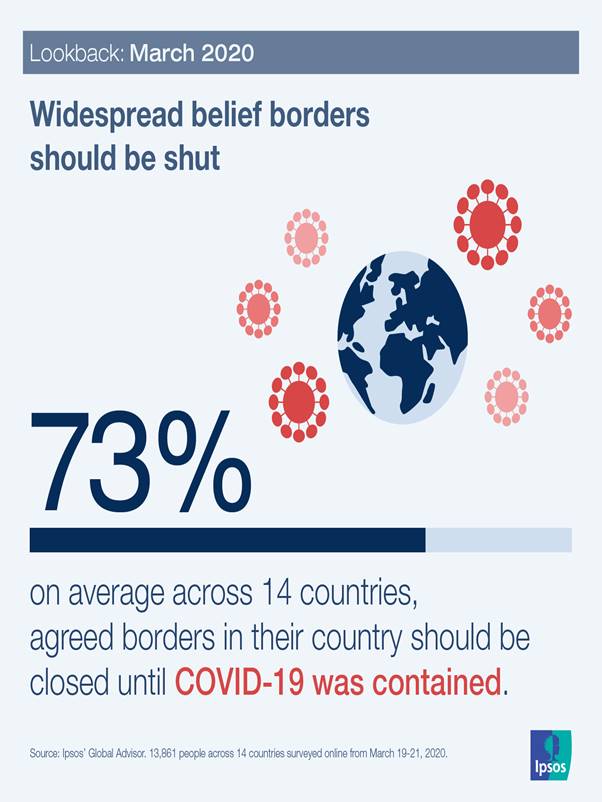

How The World Was Feeling As The COVID-19 Era Dawned, A Survey In 12

Countries The coronavirus crisis seemed small

and contained at first, but like a snowball rolling down a hill it quickly grew

in speed and size. In the days and weeks to come, citizens around the globe

started doing things that only a few months prior would’ve seemed like

something out of a cheesy sci-fi movie. People were wiping down and

quarantining groceries, fighting over dwindling supplies of hand sanitizer

and toilet paper and knocking pots and pans together nightly in honour of

healthcare heroes … not to mention that video of Gal Gadot and other celebs

singing “Imagine.” (Ipsos USA) 10 March 2023 Source: https://www.ipsos.com/en-us/data-dive-looking-back-how-world-was-feeling-covid-19-era-dawned According To Yougov Data,

Around 44% Of The World's Consumers Say They Try To Buy Only From Socially

And Environmentally Responsible Companies, A Survey Across 18 Global Markets According to YouGov data, around

44% of the world's consumers say they try to buy only from socially and

environmentally responsible companies. But how much can consumers trust

a brand's claims, given apparent high-profile shortcomings, such as those

highlighted by recent reports on fast-fashion brand H&M? The survey data

reveals that the majority of respondents globally (60%) are skeptical of

brands' green claims, suggesting that brands need to do better if they are to

earn their trust. While more than a quarter are undecided (28%), the

proportion of consumers who disagree with this statement is less than one in

ten (7%). (YouGov Spain) March 10, 2023 Source: https://es.yougov.com/news/2023/03/10/global-desconfian-los-consumidores-de-las-afirmaci/ Women Worldwide Still Facing

Uphill Battle For Equality And Safety, A 39 Country Survey Only 39% of people globally believe

that women have the same opportunities as men career-wise. This number has

improved from 2021 when an even lower 37% of respondents globally answered

positively. In some countries, the way to equality feels longer than in

others. In Chile, 62% of respondents perceive that women have fewer job

opportunities than men, and generally in the Americas, 46% of people are

feeling the same. Leading the discontent is Europe, where over 52% of

respondents think that women’s opportunities are limited. Italy (67%),

Croatia (64%) and France (58%) feel the most disparity. (WIN) 11 Mar 2023 Source: https://winmr.com/women-worldwide-still-facing-uphill-battle-for-equality-and-safety/ ASIA

784-785-43-01/Polls Japan Activists Demand

Dual-Surname Option On Women’s Day

Women’s rights activists in Japan

renewed their demand Wednesday for the government to allow married couples

the option to keep both of their surnames, saying the current practice in

which most women face social pressure to adopt their husbands’ surnames--a

prewar tradition based on paternalistic family values--widens gender

inequality. At a rally marking International

Women’s Day, representatives from dozens of women’s rights groups delivered a

joint statement to lawmakers urging them to do more to change the

125-year-old civil code, which forces married couples to choose one surname. “We strongly urge the parliament to

face the issue and promptly achieve a revision to the civil code,” the

activists said in a statement they handed to lawmakers who also attended the

rally in Tokyo. Public support for a dual-surname

option has grown, with surveys showing a majority now supports the option for

married couples to keep separate surnames. Some couples have also brought

lawsuits saying the current law violates the constitutional guarantee of

gender equality since women almost always sacrifice their surnames. Under the 1898 civil code, a couple

must adopt “the surname of the husband or wife” at the time of marriage--which

experts say is the only such legislation in the world. Although the law does

not specify which name, 95% of women adopt their husbands’ surnames, as

paternalistic family values persist and women are generally seen as marrying

into their husband’s household. A 1996 government panel

recommendation that would allow couples the option to keep separate surnames

has been shelved for nearly three decades due to opposition by the governing

Liberal Democratic Party. Prime Minister Fumio Kishida’s

conservative governing party faces growing calls to allow more diversity in

family values and marriage. Many in his Liberal Democratic Party support

traditional gender roles and a paternalistic family system, arguing that

allowing the option of separate surnames would destroy family unity and

affect children. Rally organizer Yoko Sakamoto, a

long-time activist calling for the change, said it’s time to push harder. “We

should even think about not voting for candidates who oppose the change in

next elections,” she said. Activists say the one-surname

requirement almost always forces women to compromise and go through the

trouble of changing their names in official documents and identification

cards at work or elsewhere. As more women pursue careers, a

growing number want to keep using their maiden names at work, while using

their registered surnames in legal documents. Some companies and government

offices now allow female employees to use their maiden names at work, but

they are a minority and the measure is voluntary. Because of outdated social and

legal systems surrounding family issues, younger Japanese are increasingly

reluctant to get married and have children, contributing to a low birthrate

and shrinking population. Some experts say Japan’s one-surname-only policy is

among the reasons women hesitate to get married. A 2015 Supreme Court ruling urged

parliament to discuss the surname issue instead of issuing a legal judgement,

but parliamentary deliberation has stalled amid opposition by conservative

members of the governing party. The rights gap between men and

women in Japan is among the world’s largest. Japan ranked 116th in a

146-nation survey by the World Economic Forum for 2022 that measured progress

toward gender equality based on economic and political participation, as well

as education, health and other opportunities for women. (Asahi Shimbun) March 9, 2023 Source: https://www.asahi.com/ajw/articles/14857297 MENA

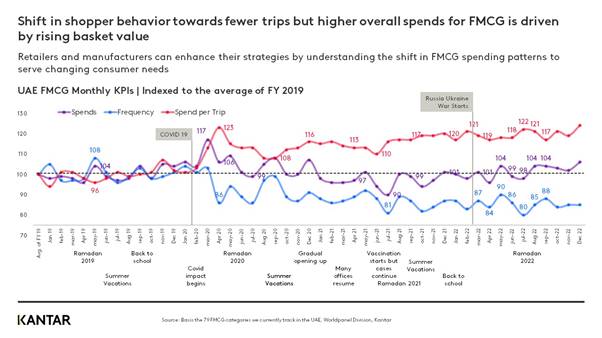

784-785-43-02/Polls Inflation Is Changing

Consumer Priorities And FMCG Spend In The UAE

Inflation and the resulting price

rises are putting pressure on consumers in the United Arab Emirates (UAE).

Spending has remained high since 2019 and this ongoing financial strain is

leading consumers to change the way they shop. But despite this, the UAE

economy ended 2022 solidly and signs suggest this growth will continue, but

might slow in the first half of 2023. Changing consumer priorities The FMCG market in the UAE continued

to thrive in 2022, partly driven by the expansion of the expatriate

population in the latter part of the year. However, FMCG spend shifted in a

way that suggested a change in consumer priorities and spending behaviour. People are shopping less often, but

spending more, and the gap between the two widened throughout 2022. This was

driven by a rising basket value which was sparked by the global pandemic and

compounded by the war in Ukraine and inflation. At the end of 2022, spend per

trip reached the highest level since COVID.

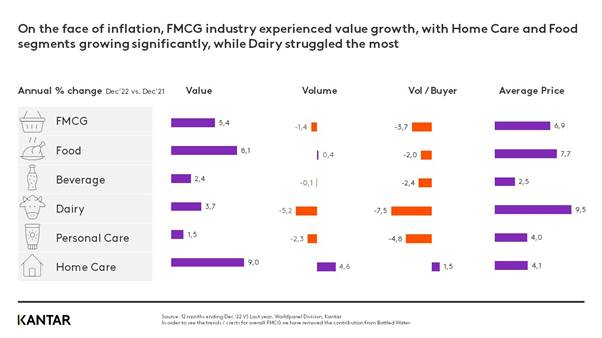

Shoppers prioritise food and home

care Despite the inflationary pressures,

the FMCG industry grew in 2022. Spend on beverages tumbled by -4% and

personal care by -5% due to shoppers shifting their spend to food and home

care products, which grew by 5% and 7%, respectively. Dairy struggled the

most and also experienced the biggest price rises. But not only are brands in

the personal care and beverage losing out to other segments, they also face

tougher competition and so it’s vital for them to adopt fresh marketing

strategies so they stand out in the market.

It's time to take a fresh look at

the traditional promotional strategy Promotions no longer have the power

they once had. Their impact has dwindled over the past two years leading many

brands to cut their promotional spend. Alternative marketing strategies and

tactics may produce better results, such as improving the in-store

experience, enhancing the product offering, leveraging social media and

influencer marketing, and personalising the customer journey through

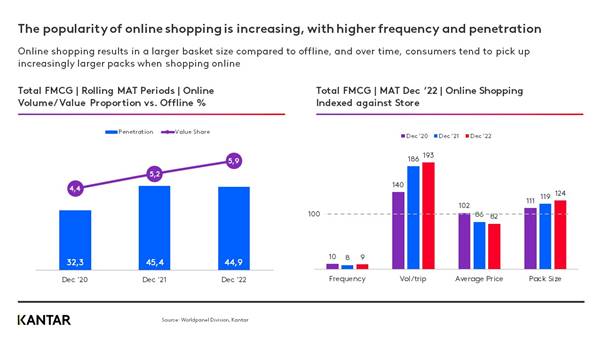

data-driven insights. But while promotions declined, the

popularity of online shopping continued to grow in 2022. Consumers purchased

nearly 6% of all FMCG products online, showing a preference for larger pack

sizes and higher purchase quantities compared to offline shopping.

Adapting strategy to changing

shopper behavior and going online is essential for brand growth. As the UAE economy faces a

slowdown, it's becoming increasingly important for retailers and

manufacturers to adapt their strategies to keep pace with the changing

spending patterns of consumers. In particular, the growing popularity of

online shopping is something that cannot be ignored - this trend has only

been accelerated by the COVID-19 pandemic. To succeed in this environment,

better targeting is crucial. This could mean renewing the appeal of premium

brands to affluent segments or offering the right product assortment and

bundles to attract middle-class shoppers. By identifying and responding to

the unique needs and preferences of different customer segments, retailers

and manufacturers can position themselves for growth and success. (Kantar) 09 March 2023 AFRICA

784-785-43-03/Polls Despite Growing Evidence,

Climate Change Is Still Unknown To Many South Africans

In recent years, South Africa has

experienced several catastrophic climate-related events, most notably the

Orange River floods in 2011, the worst drought on record in 2015, the Knysna

fires in 2017 (World Bank, 2021; Khoza, 2019), and the recent floods that

wreaked havoc in the coastal city of Durban and its surrounds, claiming more

than 400 lives and leaving thousands displaced (Ogunmodede, 2022). Climate

change is making its presence felt in the country, impacting South African

ecosystems, economies, and livelihoods (USAID, 2021). Despite the country’s

standing as the most developed economy in the Southern African Development

Community (SADC), it is not insulated from the severe harms that the range of

climate-change impacts adds to its challenges of constrained financial

resources, a sluggish economy, and persistent unemployment (King, 2021). In

response, the national government has approved critical actions that

prioritise climate mitigation and adaptation strategies, emissions

reductions, and waste management. The South African Cabinet has forged ahead

with the creation of a Presidential Climate Change Coordinating Commission, a

Low Emissions Development Strategy, a National Climate Change Adaptation

Strategy, a National Waste Management Strategy 2020, a carbon tax, and a

draft Climate Change Bill (South African Government, 2020). What are South

Africans’ experiences and perceptions of climate change? Findings from the

most recent Afrobarometer survey in South Africa, in 2021, show that popular

awareness of climate change, though increasing, remained relatively low.

Among those who were aware of it, a growing number said climate change is

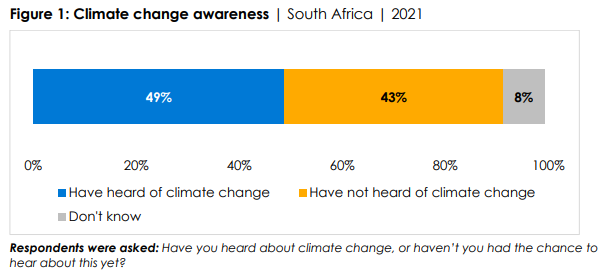

making life in the country worse. Key findings §

About half (49%) of South Africans said they had heard of climate change, a

7- percentage-point increase since 2018. o Awareness of climate change was

particularly low among citizens with less than a secondary education (36%%),

the poor (37%), and rural residents (42%). o Awareness was slightly above

average among citizens who get daily news from the Internet (58%), newspapers

(56%), and social media (55%). §

Among those who were aware of climate change, more than six in 10 (62%) said

it is making life in South Africa “somewhat worse” (30%) or “much worse”

(32%). § Compared to 2018, the proportion of citizens

who said climate change is making life worse increased by 9 percentage

points. Do South Africans know about climate change? About half (49%) of

South Africans said they had heard of climate change, while the other half

said they were unfamiliar with the concept (43%) or didn’t know how to answer

the question (8%) (Figure 1). Compared to 2018, the proportion of South

Africans who said they had heard about climate change increased by 7

percentage points (Figure 2).

Women were less likely than men to

be familiar with climate change (45% vs. 53%), as were rural residents

compared to their urban counterparts (42% vs. 52%) (Figure 4). The youngest

respondents (53%) were more aware of climate change than their elders.

Awareness of climate change increased with respondents’ education level,

ranging from 36% of those with primary or no formal schooling to 62% of those

with post-secondary qualifications. Similarly, economically better-off

citizens (60%) were far more likely to know about climate change than those

experiencing various levels of lived poverty1 (37%-50%), even though climate

change often affects disadvantaged communities the most (GIZ, 2022).

Awareness of climate change was at above-average levels among daily consumers

of news via the Internet (58%), newspapers (56%), and social media (55%),

though differences were marginal for those receiving daily news from the

radio (51%) and television (52%) (Figure 5).

How is climate change impacting

life in South Africa? Among South Africans who were aware of climate change,

62% said it is making life in the country worse, compared to 16% who said it

is making things better (Figure 6). The share of respondents who saw climate

change as making life worse increased by 9 percentage points compared to

2018, suggesting that people are feeling the effects of climate change

(Figure 7). Similar to awareness of climate change, perceptions of its

negative impact are more common in cities (64%) than in rural areas (57%),

and among the poor (68%) than among the well-off (63%). South Africans with a

post-secondary education (69%) are also more likely to perceive the impact of

climate change as undesirable, as are the youngest respondents (71% of those

aged 18-25 years) (Figure 8).

Most important problems When

respondents were asked what they considered to be the most important problems

that their government should address, climate change ranked very far down the

list – fewer than 1% of respondents cited it among their top three priorities

for government action (Figure 9). Unemployment was far and away the top

concern, cited by 63% of citizens, and 23 other problems outranked climate

change.

Conclusion General awareness of

climate change in South Africa was relatively low, especially among people

with limited education, the poor, and rural residents. This suggests

opportunities for increasing citizens’ knowledge through education and

information campaigns in order to boost support for meaningful, collective

climate action. Most South Africans who were aware of climate change said it

is making life in the country worse. But climate change ranked very low among

the problems they considered most important – a challenge for activists who

consider climate change the existential issue of our times. (Afrobarometer) 9 March 2023 WEST EUROPE

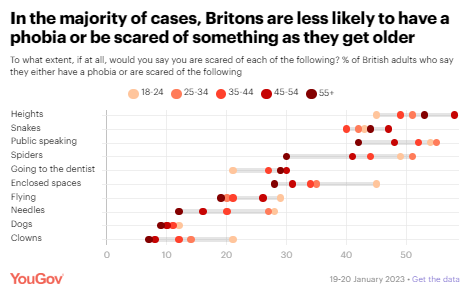

784-785-43-04/Polls A

Quarter Of Britons Say They Have A Phobia Of Heights

According to the Cambridge Dictionary, a phobia is “an extreme fear or dislike

of a particular thing or situation, especially one that is not

reasonable”. The NHS states that severe phobias can cause

a person to “organise their life around avoiding the thing that's causing

them anxiety.” Now, a new YouGov RealTime survey

has revealed that, of 10 phobias asked about, heights (or acrophobia) is the

one that Britons are most likely to suffer from, with 23% saying it affects

them. Glossophobia, or a fear of public

speaking, also features highly, with 15% of Britons admitting to having an

overwhelming and debilitating fear of having to stand up and speak in front

of people.

What are Britons

scared of? While not going so far as to say

they have a phobia, many Britons also admit to being scared of some of the

items on our list. Including the aforementioned 23%

who say they have a phobia of heights, half of Britons (52%) say they have

some form of fear of being up high, with the further 29% being either “very”

or “somewhat” scared of heights. Overall, half of the British public

(49%) also admit to either having a phobia or being scared of speaking in

front of people. And, although the chances of

encountering one in the wild in Britain are slim, two in five Britons (42%)

say they have some form of fear of snakes.

This expanded fear question reveals

further gender differences. More than half of women (57%) say they have some

form of fear of public speaking, compared to 39% of men. The same proportion

of women also admit to being afraid of heights to some extent, compared to

46% of men. However, the gender gap is at its

largest when it comes to spiders, with half of women (50%) confessing to

having either a phobia or being cared of arachnids, compared to 28% of men. Women are also almost twice as

likely as men to say they are either claustrophobic or scared of enclosed

spaces. Two in five women (42%) say they have some form of fear of enclosed

spaces such as lifts and tunnels compared to 23% of men.

In the majority of cases asked

about, fear diminishes with age. This, according

to psychologist Kevin Gournay, could be a result of producing less

adrenaline as we age, meaning the fears experienced at a younger age are less

of an issue later in life. For instance, half of those aged 18

to 24 (49%) say they either suffer from arachnophobia or are otherwise scared

of spiders (49%) compared to 30% of those aged 55 and over. The youngest age group are three

times as likely to say they have either a phobia or are scared of clowns

(21%) as the oldest generation (7%). Those aged 18 to 24 are also more than

twice as likely to admit to having some form of fear of needles (28%)

compared to those aged 55 and over (12%).

February

27, 2023 Source: https://yougov.co.uk/topics/society/articles-reports/2023/02/27/what-do-britons-say-they-have-phobia

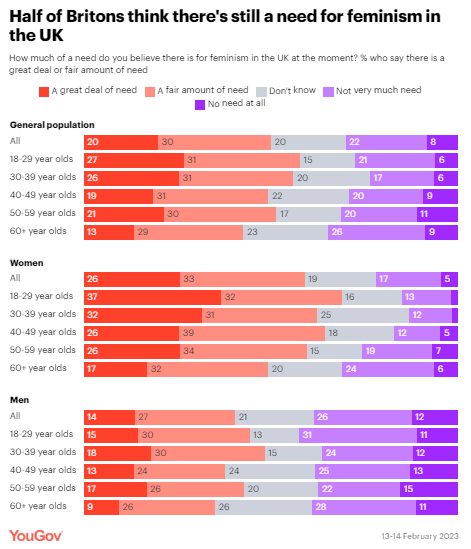

784-785-43-05/Polls Half

Of Britons Say Feminism Is Still Needed In The UK In 2023

Education is where the largest

proportion of Britons believe equality has already been won – but even then,

just 20% say so. Half (52%) say the UK is “very” or

“fairly” close to achieving equality in education, but 17% say it is not yet

close to being achieved.

The area where work is most needed,

according to most Britons, is around crime. Just 7% of the public say women and

girls’ experience of crime is on a par with men’s, while 52% say equality in

this area is not close to being achieved – 20%, however, believe equality is

close. Across every measure asked, men are

notably more likely than women to suggest equality for women and girls has

already been achieved. The most significant gender gaps

are around media representation (24% of men believe equality is achieved

compared to 8% of women), education (28% to 13%) and politics (19% to 7%).

Half of Britons

believe the UK still needs feminism The efforts of feminists are still

needed in the UK, according to half of Britons (50%), including 20% who say

there’s a great deal of need for feminism in the UK at the moment. However, three in ten Britons

believe there’s not very much need (22%) or no need at all (8%) for feminism in

this country.

At 59% to 41%, women are more

likely than men to believe feminism is still needed, with young women most

likely to say so – 69% of 18 to 29-year-old women say feminism is needed,

compared to 47% of women aged 65 and over. Those who are 65 and older are

generally least likely to think the UK needs feminism, with just 32% of men

in that age group saying so compared to between 42% and 45% of men of other

ages. March

08, 2023

784-785-43-06/Polls Four

In Ten Britons Say They’ve Witnessed Drug Deals In Their Neighbourhoods

The government

isn’t doing enough to crack down on neighbourhood drug crime, according to

57% of the public Labour has announced plans to flood

drug dealing hotspots with police officers in a crackdown on

drug crime if elected, news likely to be welcomed by a significant proportion

of Britons who claim to have seen dealers operating in their neighbourhoods. In contrast, a third of those aged

65 and over (33%) suspect they’ve seen drug dealing in their neighbourhood at

least once or twice, with 5% witnessing it on many occasions. Half of Britons (50%) have never

witnessed a suspected deal in their area.

One in eleven

Britons “very regularly” see drug users in their neighbourhood Three in ten Britons (29%) say they

regularly see people they suspect to be under the influence of drugs in their

neighbourhood, with 9% saying they see drug users “very” regularly. Just 24% of the British public say

they never have. Again, young people are more likely

to say they often see drug users in their neighbourhoods – 13% of 18 to

24-year-olds say they see people under the influence of drugs very regularly,

compared to 5% of those aged 65 and over.

Britons believe

the authorities don’t do enough to tackle neighbourhood drug crime Last year, the government set out

plans for a “swift,

certain, tough” approach to drug possession – but according

to more than half of the public (57%), the government is doing too little to

tackle neighbourhood drug crime. In comparison, 17% say the

government’s efforts are about right, while 3% say they do too much. Six in ten people (61%) who voted

Conservative in the last general election are among those who believe the

government isn’t doing enough, with 58% of Labour supporters saying the same. Overall, a quarter of Britons (26%)

believe their local police forces are doing about the right amount of work to

tackle neighbourhood drug crime, though half (49%) say they do too little –

just 2% say police do too much. Half of the public (50%) believe

local councils don’t do enough to address the problem, with 20% saying they

do enough and 1% too much.

March

10, 2023

784-785-43-07/Polls Rising

Energy Costs And Long-Term Price Pressures On UK Farmers Most Likely To Be

Seen As Causes For Fruit And Vegetables Shortages

Just over half say climate

change/weather challenges in the UK have contributed a great deal or fair

amount (54%) while around half believe the Russian invasion of Ukraine (49%),

the repurposing of arable land for other uses in the UK (47%) or haulier

labour shortages (46%) have played their parts in causing the shortages.

Around 4 in 10 say the shortages have been caused by the lack of willingness

from farmers to grow fruits and/or vegetables (42%). People are least likely to say the

Covid-19 pandemic (29%) or supermarket labour shortages (33%) have made a

contribution to the food shortages we are currently witnessing. We see a majority of people in the

UK have been affected by the issue with two-thirds (66%) saying they are

finding it harder now, in comparison to 6 months ago, to find fresh fruits

and vegetables in their local supermarkets. Only 8% say they are finding it

less difficult while almost a quarter say there has been no change (23%).

Samira Brophy,

Research Director at Ipsos, said: Here we see many

have been affected by the recent food shortages in supermarkets, with two in

three saying they have found it more difficult to find fresh fruit and

vegetables in their local store. Most recognise the current food shortages as

being caused by long term price pressures on UK farming, alongside the

current issue of energy prices. This suggests the public are tuned into the

history surrounding the current shortages, alongside more immediate challenges.

We have seen in our Ipsos Global Trends 2023 data, that major challenges

facing people give businesses and institutions a clear mandate to offer plans

and solutions. However only 40% of people surveyed in Great Britain believed

that businesses are good at planning for the long term. This highlights a big

opportunity for government and businesses to win over the public with

transparency and demonstrating action in tackling structural change. 6

March 2023

784-785-43-08/Polls 7

In 10 Britons Do Not Think The Government’s Policies Will Improve Public

Services

Confidence in the government’s

long-term policies for both economy and public services falls since last

March Almost two-thirds think Sunak’s

government has done a bad job managing the economy. Labour has small lead as party with

best policies on the economy The Conservatives and the economy /

budget When asked about different aspects

of the government’s record since Rishi Sunak became Prime Minister,

two-thirds or more think his government has done a bad job handling various

aspects of the economy. 7 in 10 (71%) think his government has done a bad job

dealing with the cost of living and 21% a good job, numbers only marginally

better than Boris Johnson’s government achieved in July (17% good job and 75%

bad job). Meanwhile, 68% think his government has done a bad job handling tax

and spending, 66% say bad job on reducing regional inequalities/levelling-up

and 64% say it has done a bad job managing the economy overall, all either

similar or marginally worse than July. Meanwhile, 32% think a Labour

government with Keir Starmer as Prime Minister and Rachel Reeves as

Chancellor would do a better job managing the economy (+6 pts from last March

when compared to Johnson and Sunak), 22% say they would do worse (-5pts) and

38% say it would not make a difference (+4).

This is Labour’s best score since going into opposition. Detailed party comparison figures

show Labour still ahead of the Tories for having the best policies on the

economy (30% vs 24%), taxation (34% to 21%), poverty/inequality (41% vs 12%),

reducing the cost of living (36% to 17%), unemployment (34% to 19%), and

pensions (26% to 17%), though on most its leads have narrowed since October. In tandem with public criticism of

the government’s performance on the economy is economic optimism – despite

improving somewhat in recent months – remaining weak. 61% expect the state of

the economy to worsen in the next year and 23% say it will improve. Whilst

this compares favourably to November when 72% said it would worsen and 16%

said it would improve, the overall net Economic Optimism Index score of -38

still reflects a wide sense of pessimism in the country. Looking ahead to the budget,

satisfaction with Jeremy Hunt’s performance as Chancellor has fallen since

November. 52% are dissatisfied with the job he is doing (+12 points) and 26%

are satisfied (-3). Whilst these scores are better than his immediate

predecessor, Kwasi Kwarteng, these are otherwise the worst scores for a

Chancellor since March 2016. In terms of what Britons would like

the Chancellor to do next week, 53% believe the Government should increase

spending on public services, even if that means higher taxes or more

borrowing, a slight increase since last July. However, only one in four (27%)

actually expect the government to do this. Voting intention and leader ratings

Latest voting intention trends show

no change in the Labour lead (note most interviewing was done before the

announcement of the new Northern Ireland trading arrangements): Labour 51% (no change since

January) Conservative 25% (-1) Lib Dem 9% (no change) Greens 5% (no change) Other 9% (-1) In terms of Ipsos’ monthly

satisfaction ratings: Only 15% are satisfied with the way

the government is running the country, while 77% are dissatisfied (including

half, 49%, of Conservative supporters), little changed from January. 27% are satisfied with the job

Rishi Sunak is doing as Prime Minister (+1 pt from January) and 59% are

dissatisfied (+4). Among Conservative voters, 65% are satisfied (+4 pts) and

26% dissatisfied (-2). 34% are satisfied with the job Keir

Starmer is doing as Labour leader (-3 pts since January) and 46% are

dissatisfied (+6). Among Labour supporters 56% are satisfied (-2 pts) and 29%

dissatisfied (+7). Gideon Skinner, head of political

research at Ipsos, said: The economy, inflation and the NHS

are the top issues for voters right now, which means Jeremy Hunt has a big

week ahead as he finalises his Budget. There are some signs of recovery from

the lowest points of last autumn, but the government will be concerned that

overall the public mood remains pretty negative about their record so far,

and with even less confidence they will improve things in the future than a

year ago, particularly when it comes to public services. Labour themselves

still have some convincing to do, especially among former Conservative

voters, but they have opened up a small yet persistent lead on the economy -

which is an important difference in Keir Starmer’s favour compared with the

last few elections. 7

March 2023

784-785-43-09/Polls How

Can Advertising Drive Gender Equality

Marketers have a lot on their

shoulders; pricing and supply chain challenges, driving margin, media

fragmentation and digital disruption all around. Then there’s the pressure,

or even the requirement, to embed social purpose and diversity and inclusion

throughout their business. And in the manifestation of this strategy, they

need to ensure that their advertising

at the very least reflects the world around us, or even progresses

it. The UK’s Advertising Standards Association even revised its advertising

code a few years ago to have the ability to rule against gender stereotyping. To mark International

Women’s Day 2023 and the call to #EmbraceEquity, we explore

our ad testing database to look at how progressive advertising to women is. A woman’s world Women had a difficult time during

COVID-19 – more women lost jobs, had to give up income, or handled home

education while continuing to work. And with the current cost of living

crisis, Kantar’s Global Issues Barometer shows that women are more

susceptible to the implications of recession and inflation, and also felt a

lower sense of wellbeing. “With great power comes great

responsibility”, said Voltaire (and Spiderman’s uncle). Marketers should

recognise they have huge power, in the form of their media investment

dollars, giving exposure and airtime to their messages, seeking to influence

attitudes and behaviours. They have a responsibility to do the right thing

for their brand, but also to consider many other factors in their

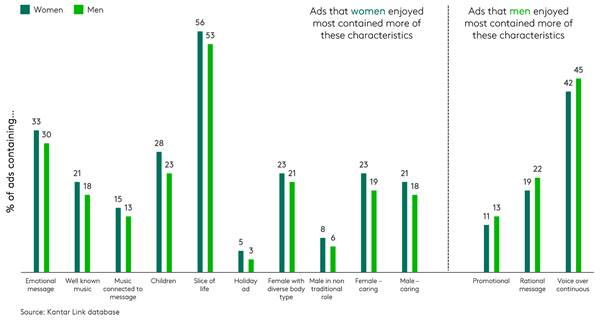

communications strategy, including how gender roles are represented. Response to advertising When we look at our Link

ad testing database of over 250,000 ads to see how men and

women watching the same ad respond, globally we see very little difference in

the various elements that are enjoyed. The few significant differences we did

see at a global level showed the ads that women enjoyed most contain more

emotional messaging (+3%), music that was well known (+3%) and connected to

the brand (+2%). In terms of content, there were more ads with children

(+5%), slice-of-life advertising (+3%) and holiday ads (+2%). With regards to characters in ads,

women enjoyed ads most that feature caring characters (male +3% and female

+3%), females with diverse body types (+2%), and men in non-traditional roles

(+2%) as well as a greater use of ads featuring people with disabilities

(+2%). Among the ads that men enjoy compared to women

we saw higher numbers of ads with rational messages (+3%) and more use of

continuous voiceovers (+2%) and ads with promotions (+2%). Regionally, North America and

Europe show similar patterns between the genders to those we see at a global

level, whereas Latin America and Asia Pacific show very few differences

between men and women. Differences in advertising between

men and women

As with creative preferences, we

see little difference in which platforms women prefer to see advertising on.

Our Media

Reactions study shows the top five preferred media channels

for women are traditionally offline channels, just like men. There are some differences. Cinema

is the most preferred media channel for women, while it is fourth among men.

One of the reasons for the difference is that women consider cinema ads less

intrusive than men. They also feel more negatively towards advertising on

gaming channels. Driving change I looked at our global Link data

about advertising in the automotive sector, until fairly recently the last

bastion of old-school behaviour. It’s not that long ago that scantily clad

women were draped over car bonnets at automotive shows, presumably to attract

the attention of the mostly male audience. Whatever way you look at that now,

it’s shameful. In fact, our database of global

automotive ads shows that ads that dare to feature women in empowered roles

have greater brand impact. Females with strong personalities and who are

funny make automotive advertising more effective. Women are still few and far

between in automotive ads in these roles, so there’s work to be done here. We see some great examples of ads tackling

gender diversity or challenging gender stereotypes. Heineken’s “Cheers to

all”, our Kantar

Creative Effectiveness Awards winner for TV in 2021, addresses

gender-related drinks stereotypes in a way that is light-hearted rather than

preachy or self-righteous, and for that reason is loved by viewers. Heineken, Cheers to All

Empowering women When brands get the messaging right

it can be truly empowering and even life-changing for women. For our recent

webinar, Harness the power of emotion in digital

advertising, we tested several ads using Link and Facial Coding,

to look at how people responded emotionally. This Kotex Lea Campos ad is a

great example of powerful storytelling. Tested amongst women, it performed in

the top 10% of the database on contribution to brand equity, top 1% for

impact on brand affinity and in the top 25% in terms of emotional engagement

as measured by expressiveness and in the top 5% in enjoyment. Kotex, Lea Campos

5 imperatives for progressive

marketers Based on our analysis and work with

clients around the world, here’s our advice for inclusive and effective

advertising to women… 1. Keep it real As in all matters D&I, we know

that being

authentic helps. It’s not what you do, it’s how you do it. It

doesn’t need to scream ‘LOOK I AM A WOMAN IN A NON-STEREOTYPED ROLE’; it can

be a natural part of communications. 2. Consider humour Emotion enhances the brand impact

of all advertising, including digital. We also know that humour is effective

in advertising, that it’s underused, and that women particularly enjoy humour

in advertising. And there are many types of humour from

belly-laugh to something that raises a wry smile. 3. Avoid stereotypes Here, marketers need to work on

solid insights. In our Link creative testing, we measure whether people think

the ad has progressive

gender portrayals, so we can tell advertisers what works, and what

impact this has on their brand. 4. Technology can help If you use AI, make sure it’s

trained on a big high-quality dataset. Kantar’s AI

creative testing solutions provide results in as few as 15

minutes and are trained on over 250,000 ads in all categories from all over

the world. 5. Getting your creative right

drives profit Our recent analysis of Kantar’s

Link data with WARC’s effectiveness database proves that high-quality

creative drives 4x profit (ROMI). So get all the ingredients

right, test your creative properly, and your advertising will be truly

effective. We are excited to bring you more

great examples of how to get gender right in advertising for our Kantar

Creative Effectiveness Awards launching on Tuesday 18 April. Watch this space

for more insights into progressive advertising that appeals to women and

getting inclusion and diversity right in your campaigns. 07

March 2023 Source: https://www.kantar.com/inspiration/advertising-media/how-can-advertising-drive-gender-equality

784-785-43-10/Polls Romir/M-Holding

Research: Results Of 2022 For The Three Leaders Of The Fast Food Market

Russians spend more money in these

restaurants on weekdays (65.7%). Both in 2021 and in 2022, a large proportion

of buyers are population representatives of the middle-income group (53%).

Also, the majority of respondents (40.5%) are adults aged 45 and older. Their

share remained almost unchanged during the year, but the number of young

people among QSR customers has decreased by 12.6%. The market leader is still

"Tasty", this restaurant chain is visited by 37.4% of Russians. The

chain almost managed to maintain penetration compared to 2021, when the brand

McDonald’s was functioned (38,5%). Meanwhile, KFC (32.9%) and Burger King

(24.3%) have increased their audience amid a difficult year. The main dish in fast food

restaurants is burgers, they account for a third of Russians' expenses in

QSR. At the same time, the most popular in Russia is the classic cheeseburger

and chickenburger. Next in popularity are French fries (12%) and rolls (9%). “Despite the

crisis time, the fast pace of life remains, people are trying to save money,

but are not ready to deny habitual. There is a demand for availability,

service speed, relaxed atmosphere, guaranteed taste and expected quality. Fast food restaurants are just covering these

needs," noted Ksenia Paizanskaya, senior customer

relationship director of Romir. 01

March 2023

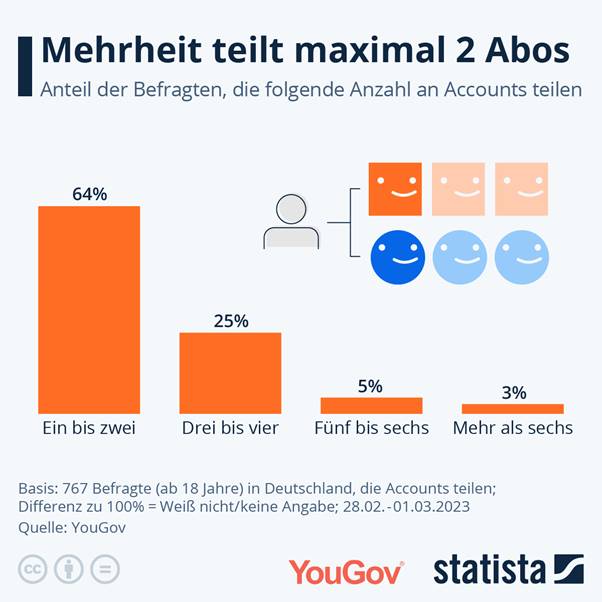

784-785-43-11/Polls Almost

Two Out Of Five Germans Use Account Sharing For Their Streaming Subscriptions

Current YouGov

survey with Statista on the subject of account sharing Streaming, whether music or video,

is widespread. Spotify, Netflix and Co. have become indispensable for

many smartphones, tablets or TV sets and are used regularly. When taking

out subscriptions, it is not uncommon for money to be considered, so that

sharing subscriptions, so-called “account sharing”, is not uncommon. Almost two out of five Germans (38 percent) share their

streaming accounts, including 23 percent within their own household, 8

percent outside the household and 7 percent both. Overall, men use

account sharing more frequently than women (40 vs. 35 percent).

Most commonly

shared up to two accounts Those respondents who share their

streaming accounts are most likely to do so with up to two accounts (64

percent), 25 percent do so with three to four accounts, 5 percent with up to

six accounts, and 3 percent with more than six accounts . Respondents

aged 55 and over say sharing up to two accounts most often (81 percent),

while sharing three to four accounts is most common (32 percent) among

respondents aged 18 to 24, the youngest age group surveyed by YouGov .

Half of the

account sharers would cancel their subscription if there were additional

costs 48 percent of those who use video

or audio streaming accounts would not be willing to pay more money for

account sharing in the future than they do now: they would cancel their

subscription if they had to pay more money for account sharing . In this

case, 26 percent would prevent account sharing in order to avoid additional

costs. A good one in six account sharers (16 percent) would accept additional

costs in order to be able to continue sharing the accounts.

March

09, 2023

784-785-43-12/Polls Every

Fourth German Can Imagine A Workation For Himself

YouGov Releases

Potential Workationer Audience Analysis Cologne, March

9th, 2023. The ITB, the world's largest travel and

tourism fair, still takes place in Berlin today. One of many topics at

the fair is "workation". The international data &

analytics group YouGov has dedicated itself to this in a target group

analysis. The term "workation" means the combination of work

("work") and vacation ("vacation"). 25 percent of Germans have not yet

done any workation, but can imagine doing so in the future. The target group

of “potential workationers” – often middle-aged and allergic to stress The “potential workationers” are significantly more common

between the ages of 45 and 54 compared to the general population (25 vs. 20

percent). In this potential group, 36 percent have a university or

technical college degree (vs. 30 percent of the total population). 75

percent of "potential workationers" say that stress makes them ill

(vs. 66 percent), 51 percent like to volunteer for a good cause in their free

time (vs. 44 percent). 88 percent say it's okay to be a father these

days (vs. 78 percent), and 79 percent say it's important to be physically

attractive (vs. 69 percent of the general German population). Half of the

potential group hopes for a better work-life balance through workation 49 percent of those Germans who can

imagine a job hope for an improved work-life balance or more free

time. Spain is their number one choice for a job (24 percent), followed

by Italy (22 percent) and New Zealand (20 percent). The current YouGov target group

analysis "Potential

Workationers" shows, among other things, the demographic

characteristics of those Germans who can imagine doing a workation. The

analysis also sheds light on the target group's attitudes towards work,

leisure and travel and shows what they expect from a workation. March

09, 2023 NORTH

AMERICA

784-785-43-13/Polls Immigrants

And Children Of Immigrants Make Up At Least 15% Of The 118th Congress

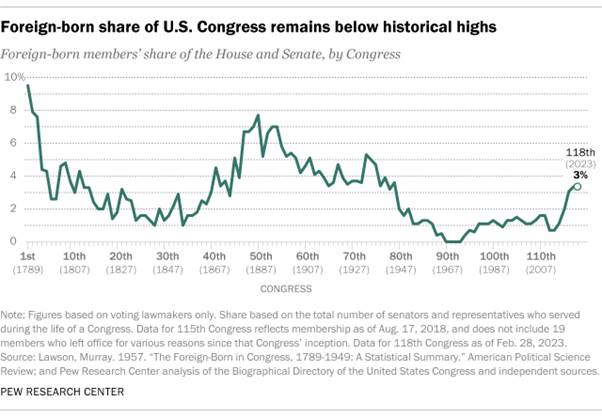

There are currently 18 foreign-born

voting members of Congress, including 17 in the House of Representatives and

one in the Senate – Democrat Mazie Hirono of

Hawaii, who was born in Japan. Together, they represent 3% of all

voting members across both legislative chambers. At least 63 additional

lawmakers – 47 representatives and 16 senators – have one or more immigrant

parent. Overall, these children of immigrants make up 12% of the House and

Senate.

Both the number and share of

foreign-born members in the current Congress are the same as in the

previous Congress. The share remains substantially below

historical highs. For example, about

8% of lawmakers were immigrants in the 50th Congress of

1887-88, during a broader wave of immigration from Europe to the United

States. The share of immigrants in the current Congress is also far below

the foreign-born

share of the U.S. population as a whole, which was 13.6% in

2021. Children of

immigrants, though, have increased their representation in Congress in

recent years. Their share has increased from 10% (or 52 members)

in the

115th Congress of 2017-18, when the Center began tracking this

biographical information. Looking at all 81 immigrants and

children of immigrants in the current Congress, Democrats make up a much

larger portion of the group than Republicans. Among the 17 senators who are

foreign born or have an immigrant parent, 12 are Democrats, four are

Republicans (Sens. Marco

Rubio of Florida, Jim

Risch of Idaho, John

Thune of South Dakota and Ted Cruz of Texas)

and one is an independent – Sen. Bernie

Sanders of Vermont, whose father emigrated from Poland.

In the House, 48 of the 64

lawmakers who are immigrants or children of immigrants are Democrats, while

16 are Republicans. The latter group includes New York Republican Rep. George

Santos, who is the son of Brazilian immigrants. However, key aspects of

Santos’ biography have been called

into question. Immigrants and children of

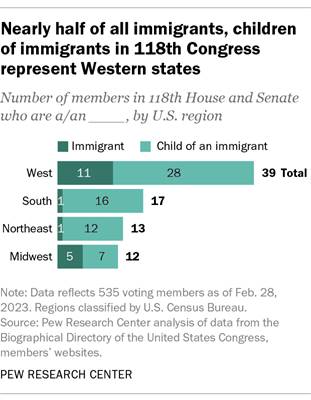

immigrants represent 25 states in Congress. About a quarter of these members

(26%) represent California – the largest share representing any one state.

Smaller shares represent Florida (9%), Illinois (7%) and New York (6%). There are also regional trends.

Almost half of members who are immigrants or children of immigrants (48%)

hail from states in the West – 39 members in all. The South ranks as the

second-most common region represented by this group, with 17 lawmakers,

followed by the Northeast (13) and the Midwest (12).

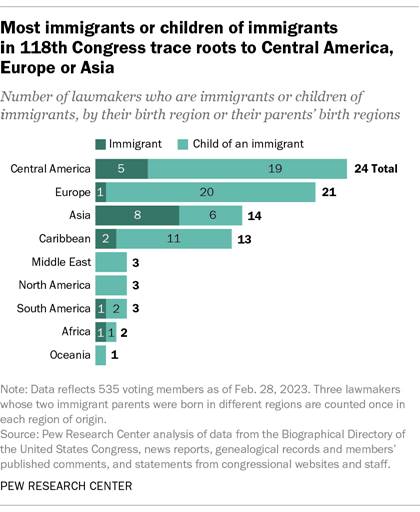

In a change from previous

Congresses, Central America has surpassed Europe as the most common origin

region for lawmakers who are immigrants or the children of immigrants.

Three-in-ten members in this group claim heritage in Central American

countries. About a quarter or fewer have roots in Europe (26%), Asia (17%)

and the Caribbean (16%). Twenty-two lawmakers who are

immigrants or have at least one immigrant parent have roots in Mexico, by far

the largest number from any one country. The next most common countries of

origin are Cuba with nine lawmakers, Germany with six and India with five.

(Some lawmakers in this analysis are tallied under more than one country and

region because their parents emigrated to the U.S. from different nations.)

Of the new members of Congress this

year, Democratic Rep. Becca Balint, whose Hungarian

father survived the Holocaust, is the first

woman and openly gay person to represent Vermont in Congress.

And Democratic Rep. Robert Garcia of California, who emigrated from Peru at

age 5, is the first

openly gay immigrant to serve in Congress. Under the U.S. Constitution, an

immigrant taking office in the House must be a U.S. citizen for seven years

or more, be age 25 or older and live in the state where they are elected.

Nine years of citizenship are required to serve in the Senate, and the member

must be 30 or older and live in the represented state when elected. FEBRUARY

28, 2023

784-785-43-14/Polls Gender

Pay Gap In U.S. Hasn’t Changed Much In Two Decades

The gender gap in pay has remained

relatively stable in the United States over the past 20 years or so. In 2022,

women earned an average of 82% of what men earned, according to a new Pew Research Center analysis of median hourly earnings of both

full- and part-time workers. These results are similar to where the pay gap

stood in 2002, when women earned 80% as much as men.

While the gender pay gap has not

changed much in the last two decades, it has narrowed considerably when