|

BUSINESS

& POLITICS IN THE WORLD GLOBAL

OPINION REPORT NO. 885-890 Week: 3 February, 2025- 16

March, 2025 Presentation: 21 March

2025 Amid

climate change, LED-lit ‘plant factories’ enter spotlight Trump’s

freeze on foreign aid could give China an opening on the world stage The 2025 Ramadan Handbook – Lebanon Edition The 2025 Ramadan Handbook – Egypt Edition The 2025 Ramadan Handbook – Saudi Arabia Edition Spotlight*KSA: Views on Brand Engagement Nigerians oppose removal of fuel subsidies, want them reinstated Sudanese

reject domestic violence but see it as a private matter to be handled within

the family Patients struggling with NHS admin The Power of Product Testing with Synthetic Data War in Ukraine: 66% of French people believe that European

support for Ukraine must continue Valentine's Day: Money and love go hand in hand Trump,

Meta and power – what does this mean for Sweden? The

Complex Landscape of Public Opinion on Deportation Obama

Best Liked Among Living Presidents; Biden, Least LGBTQ+

Identification in U.S. Rises to 9.3% A

look at Black-owned businesses in the U.S. Americans

Continue to View Several Economic Issues as Top National Problems Beyond the Buzz: How Canadians are Embracing a Sober Tomorrow Comprehensive

Analysis of Television Consumption in Colombia Ipsos New Zealand Valentine's Day - Love Life Satisfaction 2025 What Worries the World – February 2025 INTRODUCTORY NOTE

885-890-43-30/Commentary:

Beyond

the Buzz: How Canadians are Embracing a Sober Tomorrow

To understand the motivations

behind this shift, the Ipsos Behavioral Science team developed the Ipsos ALC

Framework to help brands address drivers of reduced alcohol consumption. This

framework is based on Self-Determination Theory, which posits that intrinsic

motivation arises when a behavior is perceived as worthwhile, controllable,

and socially connected. Consequently, the ALC framework

consists of three pillars focusing on intrinsic motivation to reduce alcohol

consumption: 1.

Attitudes: Focuses on individuals' health knowledge and attitudes

toward alcohol and alcohol substitutes 2.

Locus of Control: Focuses on a person's perceived control over their

drinking habits and decisions 3.

Connectedness: Focuses on the robust relationship between social

relationships and drinking behaviors Attitudes Previously, moderate alcohol

consumption was believed to be beneficial (e.g., “red wine is good for the

heart”). However, today, there are increasing questions about the impact of

alcohol on health. Nearly two in every five legal drinking age individuals in

ACT express concern about alcohol's health effects, and half report reducing

their intake in 2024. The emphasis on health and wellness in the media has

underscored the negative impact of alcohol — even in moderation.

Non-alcoholic beverages are gaining popularity, with 34% of ACT respondents

also consuming non-alcoholic options. Brands should capitalize on this trend

by promoting low-to-no alcohol beverages that align with consumer health

goals. Considerations for your

business: ·

Do you know if your consumer

base is taking active steps to stay healthy? ·

Are you aware of specific

occasions where health is prioritized over alcohol consumption? Are you

poised to win there? ·

Have you considered the impact

of GLP-1 usage on your business? Locus of Control The rise of alcohol substitutes

has provided consumers with more choices, allowing them to redefine their

drinking habits. The Sober Curious movement marks a departure from older

norms: In 2024, 40% ACT drinkers claimed to set intentional limits on their

alcohol intake; 15% of 18- to 34-year-olds take extended breaks from alcohol

beverages, nearly double from that done by Canadians over 55. When drinking

at bars or parties was the norm, abstaining was often seen as breaking the

norm. However, the Sober Curious movement and the availability of low-to-no

alcohol options at social events have created a new norm where consumers feel

empowered to decide whether to drink. Considerations for your

business: ·

Do you understand your current

consumers' beverage repertoire and alternative options? ·

Does your portfolio cater to

the Sober Curious? ·

Have you developed a strategy

to communicate, engage and win with the Sober Curious effectively? Connectedness Consumers tend to invest in

relationships with like-minded people, often mirroring their behaviors. The

motivation to reduce alcohol consumption is linked to social interactions and

where these interactions occur. Peer groups typically influence drinking

habits; when a group reduces alcohol intake, individuals often follow suit to

fit in or gain acceptance. This shift may lead to shared interests in

low-to-no alcohol beverages. While alcohol is often viewed as a social

lubricant, data suggests younger generations are less likely to frequent bars

and clubs compared to older generations. This change may reduce the perceived

need for alcohol as an aid to socialization, motivating individuals to choose low-to-no-alcohol

options. Nearly 1 in every 5 of 18 to 34 years old drinker in ACT

switch between alcohol and non-alcoholic alternatives. As social dynamics

evolve, mindful and moderate drinking practices are likely to become more

prevalent. Considerations for your

business: ·

Are you clear on the emotional and functional benefits

consumers seek from your brand? ·

What information sources do your consumers use to explore new

offerings? ·

Are you aware of how the on and off premise social occasions

of consumption are evolving? (Ipsos Canada) 14 February, 2025 Source:

https://www.ipsos.com/en-ca/beyond-buzz-how-canadians-are-embracing-sober-tomorrow SUMMARY OF POLLS ASIA (Tokyo) Amid climate change,

LED-lit ‘plant factories’ enter spotlight Japan's plant

factories are rising as climate change impacts farming.

Companies like Itoya Ltd. and Leaf Factory Tokyo grow

vegetables indoors using artificial lighting for stable production. Despite high costs,

demand is growing, making plant factories a potential future for

urban agriculture. (Asahi Shimbun) 22 February, 2025 (Pakistan) A Gallup

& Gilani survey found that 8% of

Pakistanis have carried a knife, gun, or weapon

for security, while 92% have not. (Gallup Pakistan) 19 February, 2025 (Pakistan) A Gallup

& Gilani Pakistan survey found that 20% of

Pakistanis see war with India as somewhat or very likely,

with rural residents (21%) more convinced than urban

residents (15%). Meanwhile, 48% believe war is not likely at all,

with urban respondents (58%) more confident than rural ones. (Gallup Pakistan) 20 February, 2025 (China) Trump’s freeze on foreign

aid could give China an opening on the world stage Trump’s foreign aid

cuts and targeting of USAID have raised

concerns about the U.S. ceding global influence to China,

which invests heavily in infrastructure and energy projects

abroad. While U.S. aid focuses on public health and humanitarian efforts,

China's loans fund megaprojects like Peru’s

Chancay port. Experts warn that reducing U.S. aid

weakens alliances and boosts China’s image as a reliable

partner, despite differences in funding approaches. The shift

may lead to more militarized diplomacy, with China

gaining strategic openings in global development. (Asahi Shimbun) 20 February, 2025 (India) The Maha Kumbh

Mela 2025 in Prayagraj is a once-in-144-years

Hindu pilgrimage, drawing 500+ million visitors. Key

reasons for attendance include spirituality (64%) and culture

(53%). The event is expected to generate

₹2 trillion ($23B), but faces challenges like overcrowding

(69%) and sanitation (49%).

Environmental concerns are mixed (40% worried). The

festival peaks on key dates like Makar Sankranti and Maha Shivaratri. (Ipsos India) 20 February, 2025 MENA (Lebanon) The 2025 Ramadan Handbook

– Lebanon Edition 90%

of Lebanese prefer in-store shopping during Ramadan over online. Ads, despite being

overwhelming, influence 30% of shoppers.

The dominant "Content Explorer"

persona (26%) actively engages with Ramadan content on social media. (Ipsos Lebanon) 12 February, 2025 (Egypt) The 2025 Ramadan Handbook

– Egypt Edition 75% of Egyptians prefer

in-store shopping during Ramadan

over online. Ads influence 60% of shoppers despite

overload. The "Content Explorer" persona (35%)

dominates, actively engaging with Ramadan content on social media. (Ipsos Egypt) 12 February, 2025 (Saudi

Arabia) The 2025 Ramadan Handbook

– Saudi Arabia Edition 67% of KSA shoppers prefer

in-store shopping during Ramadan.

Ads influence 55% despite overload. The "Passionate

Shopper" (29%) dominates, enjoying bustling

markets and Ramadan deals. (Ipsos Saudi Arabia) 12 February, 2025 (UAE) Spotlight*KSA: Views on

Brand Engagement Digital platforms drive

consumer-brand interactions, led by mobile apps and social media.

Younger consumers feel empowered, with 4 in 5

believing they influence brands. 7 in 10

avoid brands lacking social responsibility, and over half

expect brands to engage in social issues. (Ipsos UAE) 4 February, 2025 AFRICA (Nigeria) Majority of Nigerians

oppose fuel subsidy removal, with 58% demanding reinstatement even at the

cost of health and education. Public

dissatisfaction is at a record high, with 93% believing the country is headed in

the wrong direction and 88% rating the economy as bad.

Rising

cost of living, crime, poverty, and unemployment are top

concerns. (NOI

Polls) 21

February, 2025 (Sudan) Sudanese reject domestic

violence but see it as a private matter to be handled within the family Gender-based violence

(GBV) in Sudan has more than doubled since the war began in April 2023, with

6.9 million at heightened risk. Common abuses include rape as a war tactic, intimate partner violence, and

forced marriage. Despite government efforts, weak infrastructure

and conflict hinder accurate reporting and support. While most Sudanese oppose domestic violence, many

still view it as a private matter, and survivors face stigma when reporting.

(Afrobarometer)

13 February, 2025 WEST EUROPE (UK) Patients struggling with

NHS admin Ipsos polling reveals NHS

admin issues impact patient trust and care-seeking behavior.

While 52% think NHS communication on appointments and test results is

good, only 43% feel supported in ongoing care. 64% of

patients faced admin problems in the past year, with many chasing

test results or unclear wait times. These issues lead to

perceptions of wasted NHS resources (61%) and discourage 45% from seeking care. (Ipsos UK) 17 February, 2025 (Denmark) The Power of Product

Testing with Synthetic Data Ipsos highlights the

potential of synthetic data in market research, especially for product

testing. While synthetic data

enhances simulations and data augmentation, its accuracy depends on high-quality training data. AI-generated

data cannot fully replicate human

experiences but can augment

insights when strategically used. When accurate, it improves product testing efficiency, cutting

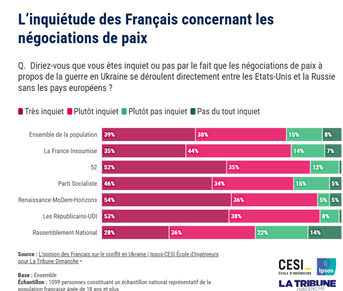

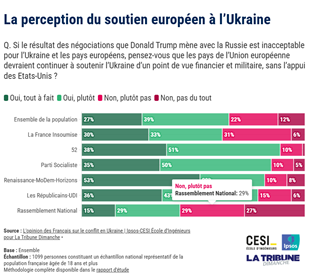

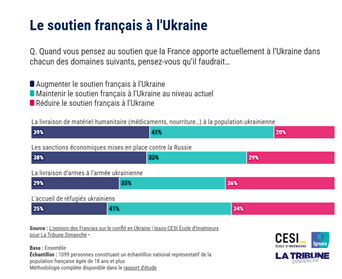

costs and enabling detailed analysis. (Ipsos Denmark) 10 February, 2025 (France) War in Ukraine: 66% of

French people believe that European support for Ukraine must continue A majority of French

people are increasingly concerned about the Ukraine conflict, with 74% worried

about Trump reducing U.S. support for European security and 77% uneasy

about U.S.-Russia peace talks excluding Europe. Despite this, 66% believe

the EU should continue supporting Ukraine militarily and financially, even

without U.S. backing. However, only 38% see a common

European defense as both desirable and realistic. The nation remains divided

on sending European troops, with 49% in favor and 51% opposed.

Support for Ukraine has grown, with rising approval for humanitarian

aid (+7%), weapons (+8%), refugee reception (+6%), and stronger sanctions on

Russia (+10%). (Ipsos France) 22 February, 2025 (Spain) Valentine's Day: Money and

love go hand in hand Spain ranks among the top

European countries in love and sexual satisfaction, with 83% feeling loved and 66% satisfied with their sex lives,

leading Europe in the latter. Millennials report the highest satisfaction in

both aspects (71%). Higher

income correlates with greater love and sexual fulfillment, as 89% of high earners feel loved compared

to 80% of low earners. The Love Life Satisfaction Index places Spain

at 78%, just behind the

Netherlands (79%). While Spain

excels in love and sex, it lags in relationship satisfaction compared to the

Netherlands (92%) and the UK (87%). (Ipsos Spain) 12 February, 2025 (Germany) Hybrid research combines

qualitative and quantitative methods, enhanced by AI, for deeper consumer

insights and innovation. Ipsos’ five-phase approach

includes social media analysis, self-ethnography, interviews, AI-human data

analysis, and workshops. The future lies in AI-driven

personalization, automation, and integrating real and synthetic data,

ensuring adaptability and competitive advantage despite

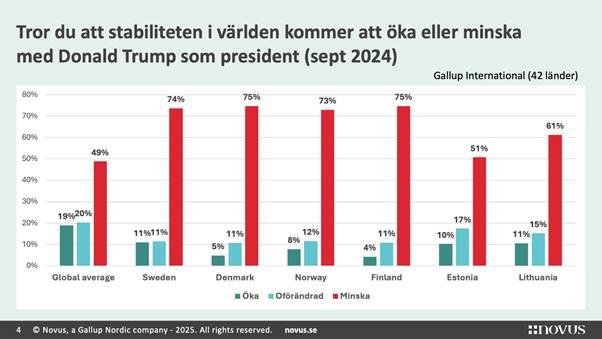

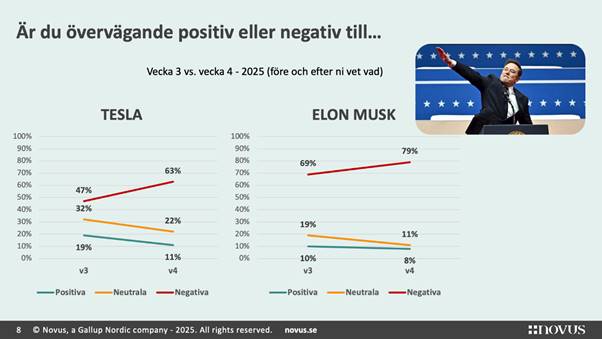

requiring more expertise. (Ipsos Germany) 17 February, 2025 (Sweden) Trump, Meta and power –

what does this mean for Sweden? A Novus and Gallup International survey

found that most Swedes view Trump's presidency as destabilizing, with 81%

believing the U.S. election affects Sweden’s economy and security. Social

media is seen as a key driver of polarization, though traditional media and

politicians also share responsibility. Elon Musk’s actions have damaged

Tesla’s reputation, while concerns over social media’s role in spreading hate

and misinformation remain high. Older Swedes demand more accountability from

platforms, and half believe laws should be tightened to curb harmful

rhetoric, reflecting frustration over the misuse of free speech and declining

media responsibility. (Novus)

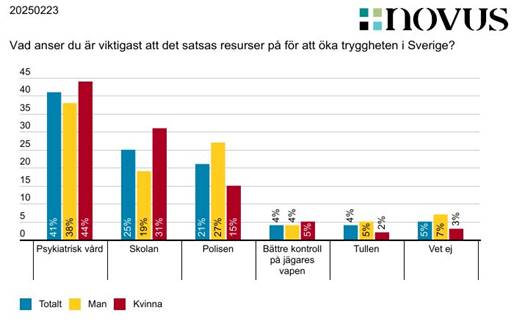

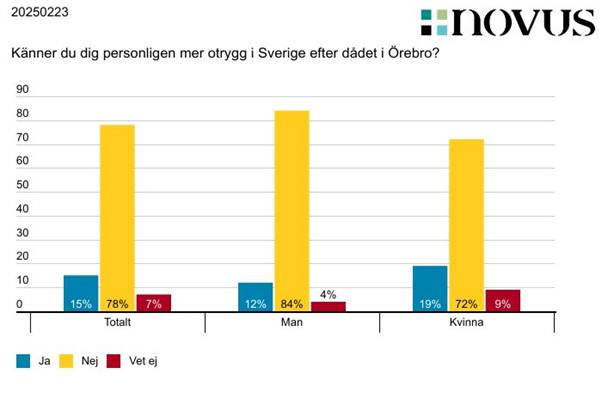

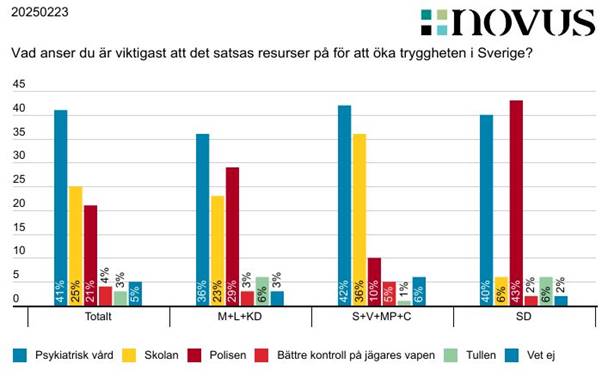

19 February, 2025 (Sweden) A Novus survey on the

Örebro school shooting reveals that 44% of Swedes believe social services

could have identified warning signs, while 27% think no one could have.

Despite the attack, 78% do not feel more unsafe. However, broader concerns

persist, with 35% feeling more insecure overall and 41% advocating for better

psychiatric care over increased policing. Swedes prioritize healthcare and

education to address root causes of crime rather than just law enforcement.

The focus is less on banning weapons and more on societal failures in

identifying and supporting those at risk before violence occurs. (Novus) 24 February, 2025 NORTH

AMERICA (USA) The Complex Landscape of

Public Opinion on Deportation Public opinion on

deportation in the U.S. is highly complex and varies based on how the issue

is framed. While 70% support a pathway to citizenship for undocumented

immigrants, 47% also support deportation, with opinions shifting based on

specific circumstances. Polls show stronger support for deporting those with

criminal records but much lower support for deporting long-term residents,

families, or those brought illegally as children. Differences in survey

results highlight the impact of question wording and context. Overall,

Americans favor a selective approach over mass deportation and recognize the

economic and logistical challenges involved. Policymakers must consider these

nuances when shaping immigration policies. (Gallup USA)

14 February, 2025 Obama Best Liked Among

Living Presidents; Biden, Least A recent Gallup poll shows

Barack Obama as the most favorably viewed living U.S. president (59%), while

Joe Biden has the lowest rating (39%). George W. Bush and Bill Clinton are

viewed more positively than negatively, while opinions on Donald Trump are divided.

Favorability trends follow a typical pattern: high ratings at inauguration,

decline during presidency, low points at exit, and eventual improvement.

Obama is an exception, maintaining strong post-presidency ratings. Trump’s

favorability, currently split, may decline over time, while Biden’s could

improve. Party affiliation significantly influences opinions, with the

sharpest divide seen in Trump’s ratings. (Gallup USA) 11 February, 2025 LGBTQ+ Identification in

U.S. Rises to 9.3% Gallup’s 2024 survey finds

9.3% of U.S. adults identifying as LGBTQ+, nearly double the 2020 figure and

up from 3.5% in 2012. Younger generations drive this increase, with over 22%

of Gen Z adults identifying as LGBTQ+, compared to just 1.8% of the Silent

Generation. Bisexuality is the most common identity, especially among younger

LGBTQ+ individuals. LGBTQ+ identification is

higher among women, liberals, urban residents, and younger generations.

Women, especially in Gen Z and millennials, are more likely to identify as

bisexual. Political and ideological differences are significant, with 21% of

liberals identifying as LGBTQ+ versus 3% of conservatives. Rural areas report

lower LGBTQ+ identification (7%) compared to urban (11%) and suburban (10%)

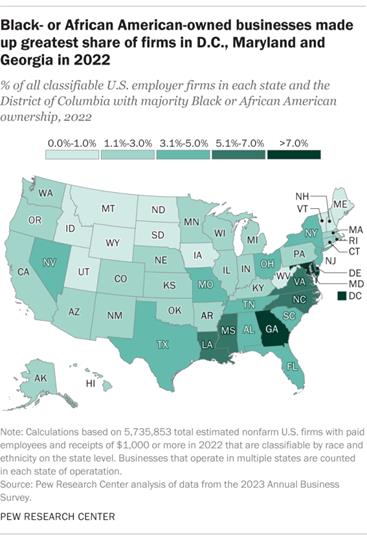

areas. (Gallup USA) 20 February, 2025 A look at Black-owned

businesses in the U.S. A 2023 Pew survey found

that over 20% of Black U.S. adults see business ownership as key to financial

success. Black-owned businesses have grown significantly, rising from 124,004

in 2017 to 194,585 in 2022, with revenue increasing 66% to $211.8 billion.

However, they still make up only 3% of all U.S. firms and 1% of total

business revenue.Most Black-owned businesses (90%) are in urban areas, with

Florida, Georgia, Texas, and California having the highest numbers. The most

common sector is health care and social assistance (26%), followed by

professional services (14%) and transportation (9%).Black business owners are

more often men (54%), middle-aged (50% between 35-54), and well-educated (61%

have at least a bachelor’s degree). Key motivations include financial

independence, work-life balance, and flexibility. For 71%, their business is

their primary income source. (PEW)

12 February, 2025

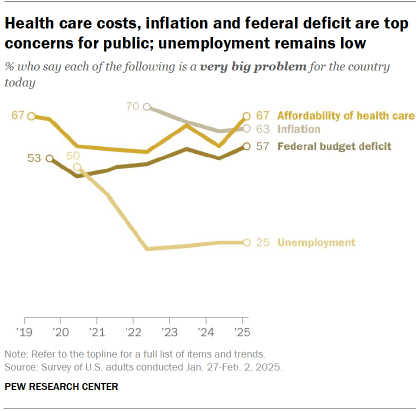

Americans Continue to View

Several Economic Issues as Top National Problems Americans see inflation

(63%), health care costs (67%), and the federal deficit (57%) as top national

problems. While both parties agree on issues like money in politics and

health care affordability, they differ sharply on immigration, gun violence,

climate change, and racism. Republicans prioritize illegal immigration (73%)

and inflation (73%), while Democrats focus on money in politics (78%), health

care (73%), and gun violence (69%). Concerns over moral values and agreement

on basic facts have grown among Democrats but declined among Republicans.

Unemployment remains a low concern for both parties. (PEW)

20 February, 2025 (Canada)

Beyond the Buzz: How

Canadians are Embracing a Sober Tomorrow Consumers are increasingly

reducing alcohol intake for health reasons, with 20% of Canadians avoiding it

and 50% cutting back in 2024. The Ipsos ALC Framework highlights three key

factors driving this shift: Attitudes, as rising health

concerns and media coverage fuel demand for non-alcoholic options (34%

consumption rate); Locus of Control, with 40%

setting drinking limits and younger generations embracing the Sober Curious

movement; and Connectedness, where changing social dynamics and

declining bar visits reduce alcohol’s role in socializing. Businesses must

adapt by catering to evolving consumer preferences and expanding low-to-no

alcohol offerings. (Ipsos Canada) 14 February, 2025 (Colombia) Comprehensive Analysis of

Television Consumption in Colombia In January, Colombian

television remained dominated by national channels, which held 61.43% of

the total share, up from 57.48% in December, despite international

channels comprising 94% of the total offer. Private national

channels took 96.38% of the national audience, with Caracol

(65.88%) and RCN (28.93%) leading. Public channels had a

minor share, with Teleantioquia (27.52%) as the most watched. International

channels held 36.16% of the total audience, with Cliente

Claro, CITYTV, and ESPN leading in cable, while Win Sports

Premium dominated premium channels. Time-slot analysis showed

national

TV peaking at 73% during prime time, while international

channels led during late-night hours. Popular programs like Yo me llamo

and La

casa de los famosos played a key role in national TV’s strong

performance. (CNC) 7 February,

2025 AUSTRAILIA

(New

Zealand) Ipsos New Zealand

Valentine's Day - Love Life Satisfaction 2025 Ipsos’ 30-country study

shows New Zealanders report high love satisfaction,

with 82% feeling loved and 87% of

those in relationships satisfied—close to the global average

but lower than Thailand and the Netherlands (92%). However, romantic/sex

life satisfaction (57%) lags behind countries like Colombia

(74%) and Mexico (72%). Income disparities impact satisfaction,

with 68% of high earners content in their love lives

versus 56% of middle- and 40% of low-income earners.

Generational differences are minimal, though Gen Z and Millennials report slightly

higher sex life satisfaction than older generations. (Ipsos New Zealand) 12 February, 2025 The Roy Morgan

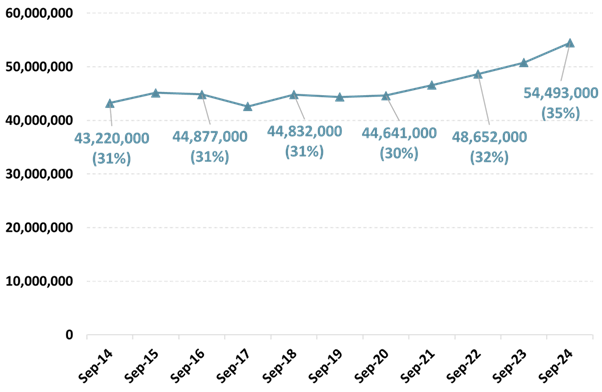

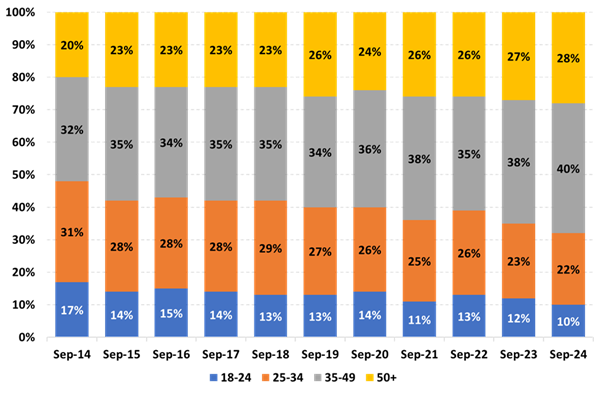

survey (Sept 2024) shows a rise in smoking in Indonesia,

with smokers increasing from 43.2M in 2014 to 54.5M today (35% of the

population). However, fewer young people (under 35) smoke,

dropping from 48% to 32% of total smokers over the decade. In

contrast, smoking among those aged 35+ has surged, now

making up 68% of smokers, with the biggest rise in the 35-49 (40%)

and 50+ (28%) age groups. While fewer young people smoking is

a positive shift, the increase among older age groups raises concerns about

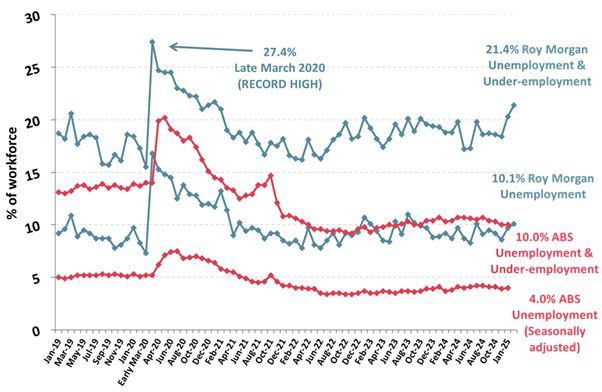

long-term health and rising healthcare costs. (Roy Morgan) 4 February, 2025 In January 2025, Australia's 'real' unemployment rose by 78,000 to 1.62M (10.1%), driven by more

people seeking work. The workforce hit a

record 16.1M, with employment

rising by 219,000 due to a jump

in full-time jobs (+306,000) despite part-time declines (-87,000).

Under-employment also surged,

reaching 1.81M (11.3%), bringing

the total unemployed/under-employed to

3.43M (21.4%), the highest since January

2021. Compared to two years ago,

the workforce has grown by 1.09M,

fueling employment gains. Roy Morgan’s 10.1%

unemployment rate contrasts with the ABS’s 4.0% but aligns with their combined unemployment/under-employment figure of 10.0%. (Roy Morgan) 17 February, 2025 MULTICOUNTRY

STUDIES What Worries the World –

February 2025 Crime and inflation (both

32%) are now the top global concerns, with crime rising in 17 countries,

particularly in Latin America (Argentina

49%, Peru 66%) and Europe (France

38%, Germany 36%). Inflation remains stable, though concerns

increased in Canada (49%) after

new tariffs, while Britain’s worry dropped

to 28%. Unemployment concern (27%) has declined, hitting a record

low in Spain (28%), while rising

in South Korea (40%). Health

care (24%) remains a key issue, with Poland

(39%) and Belgium (25%)

seeing increased concern. Immigration control (17%) has risen slightly, with Germany (44%) experiencing the largest

increase. Economic optimism is highest in Singapore

(80%), India (77%), Malaysia (69%), while Germany’s confidence remains at a record low (25%). (Ipsos

Global) 20 February,

2025 Source: https://www.ipsos.com/en/what-worries-world ASIA

885-890-43-01/Polls:

Amid climate change, LED-lit ‘plant factories’ enter

spotlight

On a main street in

Tokyo’s posh Ginza district, alongside the glittering storefronts of Tiffany,

Bulgari and other luxury brands, the flagship store of stationery retailer

Itoya Ltd. tends a very unusual “farm.” A roughly 60-square-meter

hydroponic farm was installed on the 11th floor when the Itoya building was

rebuilt in 2015. Up to 200 heads of lettuce

are grown pesticide-free, and then made into a fig and blue cheese salad. The

salad is served in a cafe in the building for 1,750 yen ($11.30), including

tax. The company harvests about

20 kilograms of lettuce a day while foreign tourists with shopping bags watch

curiously through the windows and take pictures. “It is one of our goals to

make the shop a comfortable place for customers to spend time at, not just

buy stationery,” a representative said. Itoya’s farm is one

example of “plant factories” that grow vegetables indoors for on-site

consumption regardless of the outside weather. Lighting and temperature

in plant factories are carefully controlled. Plant factories have

attracted attention as the prices of vegetables grown outdoors rise due to

climate change, with new entrants from different industries throwing their

hats in the ring. Leaf Factory Tokyo Co.

grows vegetables inside a four-story building in a residential area of the

capital’s Ota Ward near Haneda Airport. Its parent company is

Otsuka Tekko Co., an iron factory that manufactures auto parts. It started growing

vegetables at its head office on a trial basis in 2020 before going on a

full-scale basis in 2023. It currently grows

lettuce, basil, spinach and five other varieties of vegetables, harvesting up

to 2,000 heads. Many colors of LED lights

are used to grow the vegetables, and changing the light colors, from blue to

red for example, will change the bitterness and color of the produce. After harvesting, the

vegetables are shipped to nearby restaurants or sold in the company’s shop on

the first floor. In Ota Ward, there are

only two hectares of farmland—about half the size of a baseball stadium. “I want to create a model

case for young people to work in agriculture in metropolitan areas with

little farmland,” said President Akihiro Otsuka. In 2020, Plants Laboratory

Inc. provided Seiyu Co., a supermarket chain, with a plant factory system

jointly developed with the University of Tokyo. The Tokyo-based startup

has founded vegetable factories at two Seiyu outlets in the capital, and

the harvested produce is sold at 133 stores in the Kanto region. According to Plants

Laboratory, it has partnered with Tohoku Electric Power Co., Hokkaido

Electric Power Co. and other companies to set up plant factories around the

country. Vegetables are shipped to

supermarket stores and hotels in nearby areas. DEMAND

EXPANSION EXPECTED According to the

agriculture ministry, the number of plant factories in Japan has risen from

93 in March 2011 to 432 in February 2024. Those that use LED lights

and other artificial light sources make up the largest group at 195. While

194 facilities harness natural sunlight, 43 use both natural sunlight and

artificial sources. According to an estimate

by Yano Research Institute Ltd., a market research company in Tokyo, the

market for lettuce plant factories using only artificial lighting peaked at

22.3 billion yen in the business year ending in March 2022. Since then, the

market has faced difficulties in growing further as operators withdraw their

businesses and the industry is restructured. There are also challenges

to overcome. While utility bills are

soaring, large-scale plant factories are located far from urban areas,

leading to increased transportation costs. However, prices of

vegetables grown outdoors have fluctuated rapidly in recent years because of

the severe summer heat and unseasonable weather. Demand for plant

factory-grown vegetables has been growing since the supply and quality is

easier to control. The market is expected to

be worth 24 billion yen in the business year ending in March 2029, according

to the Yano Research Institute. FUTURE

OF AGRICULTURE Hiroyuki Watanabe, a

professor at Tamagawa University specializing in plant environment control

studies who is well-versed in plant factories, said they are unsuitable to

grow wheat, rice and other grain crops that require large spaces. However, plant factories

can steadily produce some kinds of vegetables even with limited space. “It is becoming difficult

to grow vegetables because of global warming and extreme weather events,” he

said. “Although there are

challenges to generating profits, growing vegetables at plant factories can

be a form of agriculture in the future.” 22 February, 2025 Source:

https://www.asahi.com/ajw/articles/15609996 885-890-43-02/Polls:

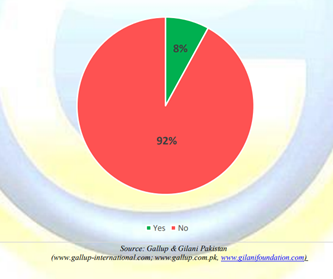

8% of Pakistanis have carried a knife, gun, or other weapon

due to a lack of safety: Gallup and Gilani Pakistan

According to a survey

conducted by Gallup & Gilani, 8% of Pakistanis have carried a knife, gun

or other weapon due to a lack of safety. A nationally representative sample

of adult men and women from across the country was asked the question, “Which

of the following things have you done for reasons of security? [Carried a

knife, gun or other weapon]” In response, 8% said ‘Yes,’ and 92% said ‘No.’

19 February, 2025 Source:

https://gallup.com.pk/wp/wp-content/uploads/2025/02/19.02.2025.daily-pollEnglish-1.pdf 885-890-43-03/Polls:

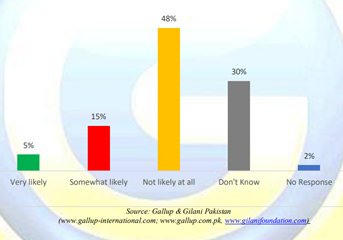

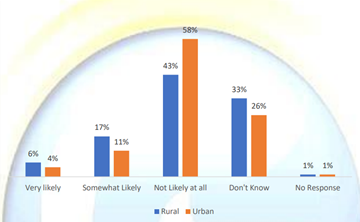

Nearly 1 in 2 Pakistanis (48%) believe that war with India

is not likely at all, 15% more urban residents (58%) than rural residents

(43%) hold a similar opinion: Gallup & Gilani Pakistan Poll

According to a survey

conducted by Gallup & Gilani Pakistan, 1 in 5 (20%) Pakistanis believe

that war with India is at least somewhat likely, with rural residents more

convinced (21%) than urban residents (15%). A nationally representative

sample of adult men and women from across the country was asked the question,

“In your opinion, how likely is a war with India these days??” In response,

5% said ‘Very likely’, 15% said ‘Somewhat likely,’ 48% said ‘Not likely at

all,’ 30% did not know and 2% did not respond.

20 February, 2025 Source:

https://gallup.com.pk/wp/wp-content/uploads/2025/02/20.02.2025.daily-pollEnglish-1.pdf 885-890-43-04/Polls:

Trump’s freeze on foreign aid could give China an opening

on the world stage

WASHINGTON--President Donald

Trump’s restrictions on foreign aid and targeting of a key

agency funding programs around the world may be offering an opening to

America’s biggest adversary — China. From

the dismantling of the U.S. Agency for International Development

to quitting international groups, Trump’s drastic “America First” moves

have raised concerns among some lawmakers and experts about whether the U.S.

is ceding global influence to its rivals, especially at a time when

Washington is fretting over Beijing’s growing clout at the cost to American

interests. Foreign assistance offered the

U.S. a source of “soft power” — allowing it to cultivate goodwill, build

alliances and counter adversaries in a bid to shore up national security

without having to dispatch troops, weapons or other more coercive measures. In Cambodia, the contrast

could not be sharper than China sending $4.4 million to support demining

operations, as Trump halted a $6.3 million grant from the State Department’s

Office of Weapons Removal and Abatement partly meant to clear “U.S.-origin

unexploded ordnances as the remnants of war.” Administration officials say

it’s past time to review how America spends money abroad. Asked if the U.S. was giving

China and Russia an opening for greater global influence, national security

adviser Mike Waltz denied that, telling NBC’s “Meet the Press” recently that

“all too often, these missions and these programs ... are not in line with

strategic U.S. interests like pushing back on China.” In Panama, the Trump

administration got the government to quit the Belt and Road Initiative,

Beijing’s flagship overseas development program, prompting condemnation

from China. Experts and lawmakers disagree

on the impact of the U.S. taking a step back from foreign aid. Lawsuits are

challenging the administration’s freeze on foreign assistance and

moves against USAID, with temporary holds on some of those efforts. “The second Trump

administration will deliver the goal for China” of wielding greater global

influence, Feng Zhang, a visiting scholar at Yale Law School’s Paul Tsai

China Center, said at a recent debate in Washington. Sen. Andy Kim, a Democrat from

New Jersey, was worried for the same reason. “China doesn’t even need to

fight for their influence around the world now because of our own effort,”

Kim said recently on “Meet the Press.” Rep. John Moolenaar, a

Republican from Michigan who chairs the House Select Committee on the Chinese

Communist Party, said it could be time for change on foreign assistance. “I think as we dig into this,

we’re going to find out what’s been working and what hasn’t been working,” he

said. “And then how do we innovate to a new way of promoting American

interests, American values and being clear on what those values are.” Dennis Wilder, a senior fellow

at the Initiative for U.S.-China Dialogue on Global Issues at Georgetown

University, said global influence goes beyond foreign aid, with the U.S.

commanding the world’s most powerful military and its dollar dominating the financial

system. Let’s not “accept at face value

that China is ready or able to step in where the U.S. may be leaving a

vacuum,” Wilder said. The Chinese embassy in

Washington said Beijing is “willing to work with all countries and parties,

including the U.S., to strengthen exchanges and cooperation in the field of

development, so as to promote common development and prosperity among all

countries.” The two countries — the primary

players in global development — are spending foreign assistance differently.

Most Chinese money is issued as debt and typically spent on energy and

infrastructure projects. Most U.S. funds were disbursed

as grants or loans with low or no interest rates in areas like public health

and humanitarian aid, said AidData, an international development research lab

at William & Mary University’s Global Research Institute. In Peru, Chinese money helped

build the $1.3 billion megaport in Chancay, which opened in November

during a visit by Chinese President Xi Jinping. U.S. foreign aid in Peru, by

contrast, was used to finance coffee and cacao as alternatives to cocaine

production. Elsewhere, American dollars

helped fight HIV/AIDS in Africa, treated malnourished children in South

Sudan and provided medical services at an immigrant shelter in Mexico. Acknowledging that the U.S.

should fund tangible foreign projects like ports and factories, Congress in

2018 established an institution to combine government funding with private

investments for projects such as the trans-Africa rail project in Angola. Overall, China spent $1.34

trillion on nearly 18,000 overseas development projects between 2000 and

2021, averaging about $61 billion a year, AidData said. The U.S. disbursed $1.24

trillion in foreign aid, including military assistance, between 2001 and

2023, the research lab said. USAID, created during the Cold

War to counter Soviet influence, is the single largest U.S. government player

in foreign aid. It paid out $43.8 billion in 2023, AidData said. That is

equivalent to less than 1% of total annual government spending. Because of the differences in

the types of projects funded, China is unlikely to step in as the U.S.

retreats, but Beijing still wins because foreign aid is about building

relationships and goodwill, said Samantha Custer, director of policy analysis

at AidData. “These countries are watching

the U.S. and how it engages with its partners and its workers, and they’re

making determinations as to whether the U.S. is a reliable economic and

security partner, and increasingly there are concerns that we are not,” Custer

said. That will feed into Beijing’s

narrative that it’s a responsible partner and global leader while sowing

doubt about the U.S., she said. New York-based China Labor

Watch, which monitors labor conditions and investigates practices such as the

use of forced labor in China, relies on U.S. funding for about 90% of its

budget, and the aid freeze has forced the group to lay off or put on unpaid

leave most of its U.S. staff, group founder Li Qiang said. China now has a strategic

opening as the go-to alternative for countries seeking investments without

political conditions, said Salvador Santino Regilme, an associate professor

of international relations at Leiden University in the Netherlands. “The broader implication of the

U.S. aid freeze is a return to militarized diplomacy, where soft power is

sidelined in favor of hard-power coercion,” he said. 20 February, 2025 Source:

https://www.asahi.com/ajw/articles/15633947 885-890-43-05/Polls:

Maha Kumbh Mela seen as symbol of preserving cultural and

religious traditions: Ipsos IndiaBus Maha Kumbh Mela 2025 Survey

The Prayag Maha Kumbh Mela 2025, underway in Prayagraj,

Uttar Pradesh, a Hindu pilgrimage festival is perceived as a symbol

of preserving cultural and religious traditions, by at least 74% of urban

Indians polled. This is also significant as while the Kumbh Mela is

held every 12 years, Maha Kumbh Mela marks the completion of a 12 Kumbh Mela

cycle – a once in 144 years occurrence, celebrated over 45 days. Interestingly, familiarity about the Maha Kumbh Mela

was seen to be high among citizens with 42% being familiar and 32% claiming

to be somewhat familiar. Though 26% were unfamiliar about the religious mega

event. “Government has gone all out to build

awareness around the Maha Kumbh Mela, given its once in 144 years occurrence

and the religious significance of purifying one’s soul through the holy dip

at the confluence of the holy rivers of the Ganges, Yamuna and Saraswati –

the Triveni ghat, for attaining moksha/ liberation, through the Amrit Snan

and Shahi Snan. And to encourage devotees to visit Prayagraj, govt has made

elaborate arrangements through setting up of a temporary city over 4000

hectares, accommodating the pilgrims, with 1,50,000 tents for lodging and

1,50,000 toilets. Supplemented with mobile health units, emergency medical

services, underwater drones, mobile app and other accoutrements. Prayagraj in

Uttar Pradesh is hosting the Maha Kumbh Mela 2025, the world’s largest

peaceful religious gathering,” said Parijat

Chakraborty, Group Service Line Leader, Public Affairs, Corporate Reputation,

CSR and ESG, Ipsos India. Though Maha Kumbh Mela has already surpassed 500

million visitors, the survey shows that the citizens were in different frames

of mind: 13% claimed to have already visited the

Maha Kumbh Mela, 26% were seen to be in the planning

mode, 22% were unsure, 23% were uninterested and 16% were undecided. Despite all the

uncertainties, the event has witnessed a large turnout. Visitors enamoured with Maha Kumbh Mela,

for different reasons The heightened interest among revellers to visit the

Maha Kumbh Mela 2025, has been for several reasons. The key motivations

emerging in the survey included: for religious/ spiritual experience (64%), for cultural experience (53%), to meet the holy men – the sadhus and

gurus (50%), to witness the large-scale social

gathering (41%), 34% are visiting out of curiosity or for

tourism and 18% claimed to be visiting the holy event

to experience the grand scale of the extravaganza. Economic impact of Maha Kumbh Mela 2025 At least 56% of urban Indians expect a positive

economic impact of the Maha Kumbh Mela on the local community. “Events of such magnitude, and since it is

a rare holy occurrence, has drawn visitors in droves, from across the country

and from overseas, benefiting the local economy. While govt had budgeted a

cost of INR 63.82 billion (USD 740 mn), it is estimated to generate a revenue

of 2 trillion (USD 23 bn) and boosting the local economy,” added Chakraborty. Large scale events come with their own

challenges despite impeccable planning Citizens expect a few challenges emerging due to the

huge influx of citizens in Prayagraj at the Maha Kumbh Mela – the challenges

like overcrowding (69%), sanitation and hygiene (49%), safety and security concerns (49%), transportation and traffic control (46%), environment impact (37%), medical and emergency services (29%) and cultural and religious

sensitivities (16%). At the same time, at least 4 in 10 citizens polled,

expressed their concern about the Maha Kumbh Mela and huge crowds, impacting

the environment negatively. Though the views were largely divided, with 3 in

10 being neutral, 17% expecting no detrimental impact, while 11% were

undecided. “Some of these auspicious dates have seen a

steady rise in the number of visitors. Especially during Makar Sankranti (14

January), Mauni Amavasya (29 January), Vasant Panchami (3 February), Magha

Purnima (12 February) and now Maha Shivaratri (last day of the Maha Kumbh

Mela), and it marks the culmination of the 45-day religious festival,”

stated Chakraborty. 20 February, 2025 MENA

885-890-43-06/Polls

The 2025 Ramadan Handbook – Lebanon Edition

The report reveals that 9 in 10 Lebanese choose in-store

shopping during Ramadan over online shopping. Despite the perception of ad

overload, advertisements contribute to brand memorability and influence the

purchasing decisions of 3 in 10 shoppers. When it comes to Ramadan personas,

the “Content Explorer” (26%) makes up the largest persona in Lebanon. People

who fit this persona are digital enthusiasts who engage deeply with

Ramadan-related programs and content on social media. 12 February, 2025 Source:

https://www.ipsos.com/en-lb/2025-ramadan-handbook-lebanon-edition 885-890-43-07/Polls

The 2025 Ramadan Handbook – Egypt Edition

The report reveals that 75% choose in-store shopping during

Ramadan over online shopping. Despite the perception of ad overload,

advertisements contribute to brand memorability and influence the purchasing

decisions of 3 in 5 shoppers. When it comes to Ramadan personas, The “Content

Explorer” (35%) makes up the largest persona in Egypt. People who fit this

persona are digital enthusiasts who engages deeply with Ramadan-related

programs and content on social media. 12 February, 2025 Source:

https://www.ipsos.com/en-eg/2025-ramadan-handbook-egypt-edition 885-890-43-08/Polls

The 2025 Ramadan Handbook – Saudi Arabia Edition

The report reveals that 67% choose in-store shopping during

Ramadan over online shopping. Despite the perception of ad overload,

advertisements contribute to brand memorability and influence the purchasing

decisions of 55% of shoppers. When it comes to Ramadan personas, The

“Passionate Shopper” (29%) makes up the largest persona in KSA. People who

fit this persona are shopping lovers who indulge in the busy markets and

attractive deals during Ramadan. 12 February, 2025 Source:

https://www.ipsos.com/en-sa/2025-ramadan-handbook-saudi-arabia-edition 885-890-43-09/Polls

Spotlight*KSA: Views on Brand Engagement

The Spotlight report shows that digital platforms are at

the heart of consumer-brand interactions, where mobile apps and social media

are at the forefront, providing effortless ways to connect. This trend is

especially driven by the younger generation. With the abundance of digital

touchpoints, consumers now feel more in control, with 4 in 5 convinced they

can influence brands. This sense of empowerment is shifting consumer

expectations, as people today demand more from brands. Over half think brands

should be involved in social issues, not just business, and 7 in 10 would

avoid brands that aren’t socially responsible, even if they like them. These

expectations are especially strong among younger consumers, who are calling

for more accountability and ethical practices. 4 February, 2025 Source:

https://www.ipsos.com/en-ae/spotlightksa-views-brand-engagement AFRICA

885-890-43-10/Polls

Nigerians oppose removal of

fuel subsidies, want them reinstated

A large majority of Nigerians

disapprove of the government’s decision to remove fuel subsidies, with more

than half calling for their reinstatement even at the expense of other key

sectors such as health and education, the latest Afrobarometer survey shows. Almost two years after the

elimination of the subsidies, public dissatisfaction with the country’s

economic direction has reached record levels. More than nine in 10 Nigerians

say the country is heading in the wrong direction. Nearly as many citizens say

the economy is in bad shape, while three-fourths report poor personal living

conditions. The most important problem

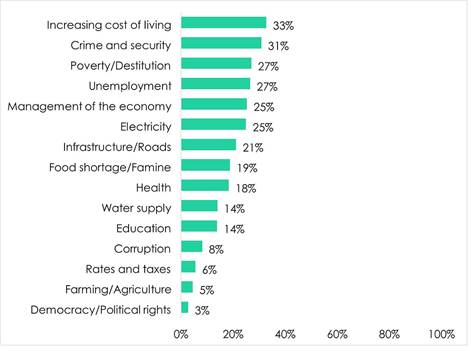

that Nigerians want the government to address is the increasing cost of

living, followed by crime and security, poverty, unemployment, management of

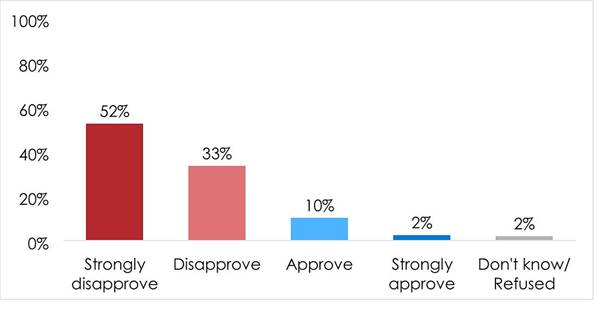

the economy, and electricity. Key findings ▪ A large majority of

respondents “disapprove” (33%) or “strongly disapprove” (52%) of the

government’s decision to remove fuel subsidies. Only 12% approve of their

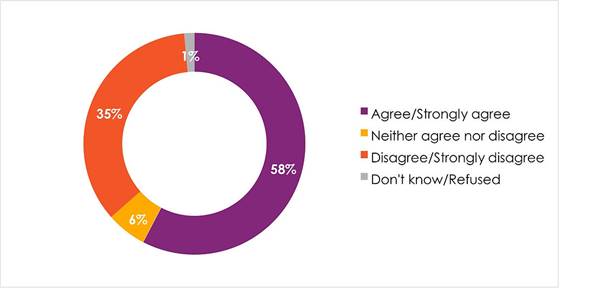

removal (Figure 1). ▪ Almost six in 10 (58%) say

the government should reinstate fuel subsidies even if this means reducing

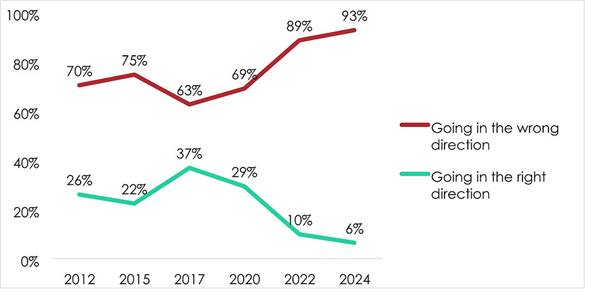

other important expenditures such as health or education (Figure 2). ▪ More than nine in 10

Nigerians (93%) say the country is going in “the wrong direction.” This

represents increases of 30 percentage points since 2017 (63%) and 4 points

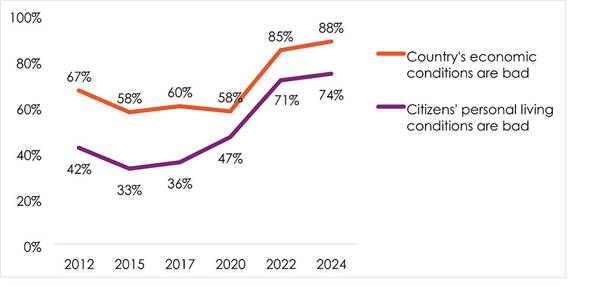

since the most recent survey in 2022 (89%) (Figure 3). ▪ Nearly nine in 10 citizens (88%) say the country’s economic

condition is “fairly bad” or “very bad,” up 30 percentage points from 2020

(Figure 4). o And three-fourths (74%) report poor personal living

conditions. The increasing cost of living

(33%) is the most frequently cited problem that Nigerians want the government

to address, followed by crime and security (31%), poverty (27%), unemployment

(27%), management of the economy (25%), and electricity (25%) (Figure

5). Figure 1: Views on government's decision to remove fuel

subsidies | Nigeria | 2024

Perceptions on fuel subsidy removal Respondents

were asked: Do you approve or disapprove of the government’s decision to

remove fuel subsidies, or haven’t you heard enough to say?

Support for reinstating subsidy removal Respondents

were asked: Do you agree or disagree with the following statement: The

Nigerian government should reinstate fuel subsidies even if this means

reducing other important expenditures such as health or education? Figure 3: Overall direction of the country | Nigeria | 2012-2024

Perception on the overall direction of Nigeria Respondents

were asked: Would you say that the

country is going in the wrong direction or going in the right direction?

Figure 4: Negative

assessments of the country’s economic condition and personal living

conditions | Nigeria | 2012-2024

Assessment of Nigeria's economic/personal living condition Respondents

were asked: In general, how would you describe: The present economic

condition of this country? Your own present living conditions?

Figure 5: Most important

problems | Nigeria | 2024

21 February, 2025 Source: https://www.noi-polls.com/post/nigerians-oppose-removal-of-fuel-subsidies-want-them-to-be-reinstated 885-890-43-11/Polls

Sudanese reject domestic violence but see it as a private

matter to be handled within the family

As of October 2024, 6.9

million Sudanese were considered at heightened risk of gender based violence

(GBV), more than twice the number (3.1 million) estimated before the

war between the Sudanese Armed Forces and the Rapid Support Forces

began in April 2023 (UNFPA, 2024; UN Women, 2024). The most common

types of reported GBV cases include rape as a war tactic, intimate

partner violence, forced marriage, and forced prostitution (UNFPA,

2024). However, obtaining accurate statistics on GBV in Sudan is nearly

impossible because of the country’s poor infrastructure and health-care

system and the protracted conflict, which has restricted communication

and displaced millions (Widaatalla, 2024; World Health Organization,

2023). In collaboration with

international partners, the Sudanese government has taken steps to

address the scourge of GBV in the country. In March 2020, it signed a

Framework of Cooperation on the Prevention and Response to Sexual

Violence in Conflict (United Nations, 2020; Stop Rape Now, 2024). The

country’s National Action Plan for the Implementation of UN Security

Council Resolution 1325 on Women, Peace & Security 2020-2022 aims to

protect women and girls against all forms of GBV (Sudan Ministry of

Labour and Social Development, 2020). Domestic laws directly and

indirectly address GBV, such as the Criminal Act of 1991 (Human Rights Watch,

2009). In April 2021, after years of

pressure from rights activists. the government ratified the Convention

on the Elimination of All Forms of Discrimination Against Women

(Mohiedeen, 2021). However, while Sudan has signed the Protocol to the

African Charter on Human and Peoples’ Rights on the Rights of Women in

Africa (also known as the Maputo Protocol), it has yet to ratify it (African

Union, 2022) as a step toward ensuring key legal safeguards, access to

justice, GBV-related support services, and international

accountability. This dispatch reports on a

special survey module included in the Afrobarometer Round 9 (2021/2023)

survey to explore Africans’ perceptions of gender-based violence. In Sudan, GBV ranks as the

second-most-important women’s-rights issue that citizens say their government

and society must address. Even though a majority say it is “never justified”

for a man to use physical force to discipline his wife, most see domestic

violence as a private matter that should be resolved within the family.

And while most Sudanese think the police take GBV cases seriously, many

also consider it likely that a woman reporting an incident of GBV will

be criticised, harassed, or shamed by other members of the community. 13 February, 2025 WEST EUROPE

885-890-43-12/Polls

Patients struggling with NHS

admin

New Ipsos

polling for the King’s Fund, National Voices and Healthwatch England has

explored people’s experiences of NHS admin, and the impact of that on their

views of the NHS. Read more in the King’s Fund, National Voices and

Healthwatch England long read, Lost in the System: the need

for better admin. Around

half (52%) think the NHS is good at communicating with patients about things

like appointments and test results. However, just 43% think the NHS is good

at ensuring there is someone for patients to contact about their ongoing care

and 28% think it is poor at this, and while 42% think the NHS is good at

keeping people informed about what is happening with their care and

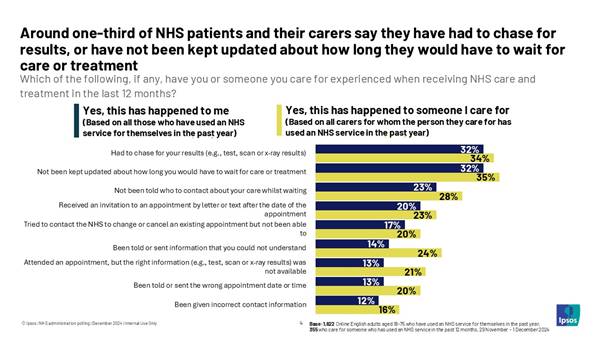

treatment, 32% think it is poor at this. Nearly

two in three patients (64%) have experienced at least one NHS admin problem

in the last year (for themselves or someone they care for). This includes

around one-third of those who have used an NHS service in the last year (for

themselves or for someone else) having had to chase for their results, and

not been kept updated about how long they would have to wait for care or

treatment.

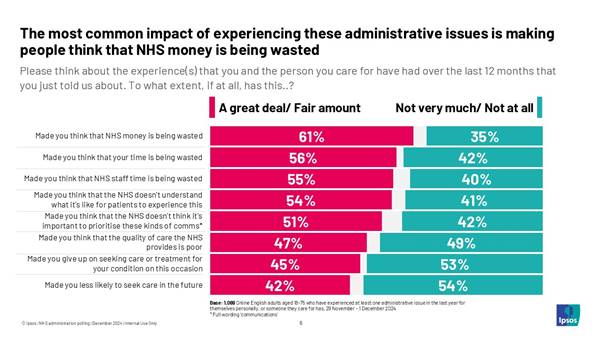

Among

people who have experienced one of these issues, the most common impact of

the experience is making them think that NHS money is being wasted (61%),

that their time is being wasted (56%) and that NHS staff time is being wasted

(55%). It also impacts on patients’ likelihood to seek care, with 45% saying

it made them give up on seeking care or treatment for their condition on that

occasion and 42% that it made them less likely to seek care in the future.

Technical information 1,888

English adults aged 18-75 were asked (online) by Ipsos about how good or poor

the NHS was at communicating on a range of things like appointments and test

results. The research was carried out between 29 November – 1 December 2024.

Quotas were set by age within gender, region and working status. Data are

weighted by age within gender, region, working status, social grade and

education to match the profile of the population. 17 February, 2025 Source:

http://ipsos.com/en-uk/patients-struggling-nhs-admin 885-890-43-13/Polls

The Power of Product Testing with Synthetic Data

Synthetic

data is revolutionizing industries from healthcare to financial services to

automotive, by enabling simulations and data augmentation. At Ipsos, we believe

synthetic data opens up brand new possibilities for market research,

particularly in the area of product testing. However, many businesses remain

uncertain about the quality of synthetic data or how to evaluate it. In this

Ipsos Views paper, our experts provide recommendations for generating and

evaluating high-quality synthetic data and explore how synthetic data can be

applied specifically to product testing. Generating

and evaluating synthetic data To generate synthetic data that effectively mimics

real-world data, an artificial intelligence (AI) model must first be trained

on relevant, real-world data. As discussed in our first paper in the Humanizing AI series, AIs are simply algorithms; they

have no intelligence of their own, until they are trained. It is through

learning from training data that AIs acquire the intelligence we associate

with them. The

evaluation process is also straightforward. Synthetic numerical data should,

at minimum, mirror real-world data on common statistical measures. The closer

synthetic data is to human data, the less risk we assume when using it, but

there is always some risk because synthetic data can never perfectly mimic

real-world data in every aspect. Approaches

to generating synthetic data fall into two categories: LLMs (Large Language

Models) and non-LLMs, distinguished by their textual and numerical nature,

respectively. We explore both approaches in this paper. The

product experience is inherently human How

humans react to products, or life in general, is not captured solely in the

brain as factual or semantic knowledge, our bodies and sensory experiences

play a significant role, too. This

paper presents the findings from our two research streams carried out aiming

to establish the minimum number of human respondents needed to test products

alongside synthetic data to ensure viable results. To discover the key

findings from the research, you can also download our useful infographic.

If an AI has not been

trained on real-world data that is relevant to your business, it will not be

able to generate synthetic data that shares the same properties as real-world

data. It’s as simple as that! Key

takeaways: 1. Synthetic data will never be human. 10 February, 2025 Source:

https://www.ipsos.com/en-dk/humanizing-ai-2-the-power-of-product-testing-with-synthetic-data 885-890-43-14/Polls

War in Ukraine: 66% of French people believe that European

support for Ukraine must continue

French

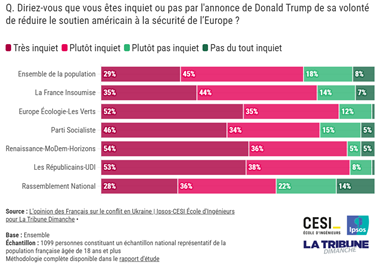

people concerned about the latest developments in the conflict in Ukraine 74% of French people say they are worried by Donald Trump's

announcement of his desire to reduce American support for

European security.

Two

out of three French people believe that European support for Ukraine should

continue Faced

with these announcements of reduced American support, the French believe that

European support for Ukraine must continue: 66% believe that the

countries of the European Union should continue to support Ukraine from a

financial and military point of view, without the support of the United

States if the result of the negotiations that Donald Trump is conducting with

Russia is unacceptable for Ukraine and European countries – a proportion that

varies from 44% among RN supporters to 89% among EELV supporters.

Thus, the

sending of European soldiers to enforce a peace agreement in Ukraine divides

the French: while 49% say they are in favour, 51% say they are opposed. How

do the French view the country's level of support for Ukraine? However, this does not mean a lack of

support for Ukraine. Compared to February 2024, more French people

think that it is necessary to increase the delivery of humanitarian equipment

to Ukraine (39%, +7 pts), the delivery of weapons to the Ukrainian army (29%,

+8

Similarly,

the economic sanctions put in place against Russia are more well received,

with 38% of French people thinking that they should be increased (+10

points). This desire to increase the various forms of support for Ukraine is

particularly strong among EELV, PS, Renaissance and LR-UDI supporters. 22 February, 2025 885-890-43-15/Polls

Valentine's Day: Money and love go hand in hand

Main

findings ·

People with higher incomes are

more satisfied with their love and sex lives. 83% of people in Spain feel

loved. ·

Spain leads the European

ranking in terms of the level of satisfaction with their sexual life: 7 out

of 10 people say they are satisfied with their sexual relationships. ·

Millennials are the most

satisfied with love and sex. Valentine’s Day is approaching

and, to paraphrase John Paul Young in his historic song, “Love is in the

air”. February 14 is the date par excellence to celebrate love and, once

again, Ipsos has published its study “Love life Satisfaction 2025”, which

analyses how people perceive their love and sexual lives. In this edition, Ipsos has

incorporated the Love Life Satisfaction Index, which measures the level of

satisfaction in three aspects: feeling loved, sexual life and relationship.

Latin American and Asian countries have the highest data in this index, while

European countries are conspicuous by their absence, although Spain and the

Netherlands do manage to sneak into the global top 10. Spain, with an index

of 78%, is positioned as the second European country most satisfied with its

love life, just one point behind the Netherlands (79%). But let's look separately at

the three aspects that this index brings together. The majority of Spaniards

say they feel loved, with 83%, again surpassed at European level only by the

Netherlands (85%). Spaniards also show themselves to be highly satisfied with

their relationship with their partner, with 85%. In this aspect, although the

figure is very high, Spain falls in the European ranking. Countries such as

the Netherlands (92%) and the United Kingdom (87%) have higher figures than

Spain. It is in sexual life where people in Spain lead the European ranking,

with 66% saying they feel satisfied with their sexual relations. The

Netherlands with 62% is in second place and Ireland with 59% closes the

European top 3. More

money, more love It is scientifically proven

that being loved, or loving and being loved in return, increases serotonin in

the brain and, therefore, happiness. However, if we add purchasing power to

the equation, we see that the relationship between money and love is directly

proportional. That is, as the study confirms, the higher the income, the

greater the likelihood of feeling loved and sexually satisfied. Thus, 89% of the population in

Spain with high incomes declares that they feel loved, while among people who

earn low incomes this percentage drops to 80%. A similar trend occurs with

romantic and sexual life. People with higher incomes have greater

satisfaction, as stated by 74% of people with higher purchasing power; while

this percentage drops to 60% of Spanish citizens with lower incomes. Love

and sex for generations In general, all generations say

they feel loved in Spain. Baby boomers and millennials feel most loved, with

85%, while generations X and Z, with four points less, remain at 81%. It is in sexual life where the

greatest differences between generations are appreciated, with millennials

being the most satisfied with their romantic and sexual life (71%) compared

to 64% of X, 63% of baby boomers and 62% of Z. 12 February, 2025 Source:

https://www.ipsos.com/es-es/actitudes-amor-relaciones-y-sexo 885-890-43-16/Polls

The Power of Combination: Hybrid Research as the Key to

Substantial Insights and Groundbreaking Innovations

In today's complex world, where

we are flooded with information, it is no longer enough to rely on a single

research method. Hybrid approaches that integrate qualitative and

quantitative methods are not a luxury, but a necessity. They open up new

horizons, especially through the use of artificial intelligence (AI). This

development enables companies to gain indispensable consumer insights and

thus decisively influence the innovation process. Modern

research needs hybrid approaches The question is no longer

whether hybrid approaches should be used, but how they should be optimally

designed. The aim is to efficiently manage the increased effort and the need

for diverse methodological expertise that hybrid research undoubtedly

requires. A full-service institute like Ipsos can do this like no other:

hybrid research approaches, delivered seamlessly from a single source, are

our USP. Hybrid research combines the

best of both worlds: the depth of qualitative approaches and the breadth of

quantitative data. Through the skillful integration of offline and online

methods, data collection in real time or at the participants' own pace, AI-supported

data analysis and activation, a comprehensive understanding of consumer needs

is possible. Why

should I rely on a single method that is sure to miss something when hybrid

approaches offer a full spectrum of deep insights?

A hybrid, multi-stage research

project for a shampoo manufacturer that was carried out in three countries

shows how this can be achieved. Phase 1: Netnography –

Feeling the Pulse of Social Media AI-supported social media

analysis to identify trends. AI was used to examine social media posts on the

topic of hair care. This enabled current trends and opinions to be recorded -

the perfect basis for the further research and innovation process. Phase 2: Mobile

Self-Ethnography – Gaining Authentic Insights Consumers document their daily

use of hair care and shampoo. This gave us an authentic insight into people's

habits and preferences. Phase 3: Online Interviews –

Conducting Deep Conversations and Understanding Diversity Subsequently, individual

interviews deepened the previous data and revealed consumers' wishes,

problems and preferences when using hair care products. Phase 4: Analysis –

intelligently evaluate data for action-oriented insights Here, human and artificial

intelligence work together to analyze all data, identify hidden patterns and

generate valuable insights. This helped the customer make decisions based on

solid data. Phase 5: Workshops –

creatively implementing results The results were presented in

two workshops and used collaboratively: classic and AI-supported. The AI

workshop brought fresh product ideas and claims that were

evaluated by human experts and aligned with the brand strategy. It offered the customer new

opportunities to better understand and interpret consumer needs and to be

creative based on that. This resulted in pioneering products that really meet

the market. This is a clear competitive advantage and helps the shampoo manufacturer

to secure growth for years to come. Hybrid research approaches show

how consumer insights and product innovations go hand in hand. The

combination of different methods enables us to master market complexity and

optimally support innovation processes. Also because the results have a

higher validity. The integration of AI expands the possibilities immensely

and underlines the importance of hybrid methods as the key to success. Hybrid research turns 'what

if' into 'what comes next' and enables us to move forward with confidence. The

Future of Hybrid Research: Automation and Personalization In the future, it will also be

important to combine 'real' and 'synthetic' data in a meaningful way. For

example, a company could acquire its own persona bot based on market

segmentation. This can be used to chat 'personally' with the identified

target groups in order to bring them to life with their needs and attitudes. In the future, the power of the

combination of methods will also lie in the long-term activation and greater

personalization of insights. With the help of AI, research results can be

tailored more closely to the individual needs of companies. For example,

marketing strategies and product developments can be aligned more precisely

in the future.

·

Advantages of hybrid

approaches: They provide more

comprehensive insights and higher validity because they can be flexibly

adapted to different research questions and business challenges. ·

Challenges: Hybrid approaches require

greater effort in planning, coordination and implementation as well as expert

knowledge in different methods. ·

Tools and technologies: Examples such as mobile

ethnography apps, online platforms and AI software demonstrate the effective

combination of tools for data collection. ·

Future prospects: Expanded integration of

data from a variety of sources, including social media, customer feedback,

market research and synthetic data, as well as further automation of

processes and greater personalization of results will further impact

research. 17

February, 2025 885-890-43-17/Polls

Trump, Meta and power – what does this mean for Sweden?

The survey consists of a global study conducted by Novus in

collaboration with Gallup International on world stability with Donald Trump

as president. It has been complemented by a Swedish survey on concerns about

polarization and populism, Elon Musk's statements and their impact on his

company, and the role and responsibility of social media compared to

traditional news media. The majority of the survey was conducted in Sweden from February

6–11, 2025, while the global questions were asked in 40 countries during

September 2024. Novus CEO Torbjörn Sjöström has analyzed the results. Stability in the world with Donald Trump as president of the

United States

According to a Novus and Gallup Nordic survey, conducted in

collaboration with Gallup International ahead of the 2024 US election, the

overwhelming majority of the Swedish people, like our Nordic and Baltic

neighbors, believe that the world would be more unstable with Trump as

president. The fact that this is happening now does not come as a surprise to

citizens. Many remember his previous presidency, and the fact that a second

term would mean even greater instability was unfortunately expected.

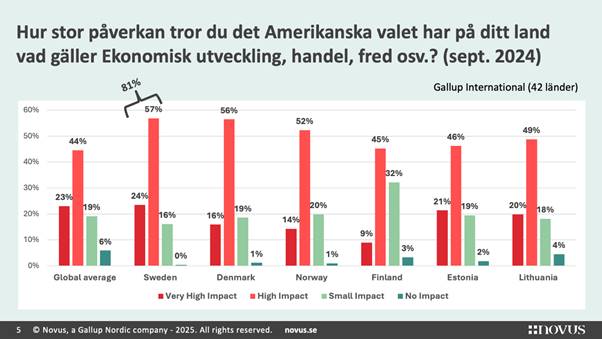

81% of Swedes believe that the US election has a major impact on

Sweden's economic development, trade and peace. Therefore, what is happening

now in Ukraine and Gaza, as well as trade issues such as tariffs, is no

surprise to the Swedish people, nor to our Nordic and Baltic neighbors. Many

saw this coming even before Trump won the US election.

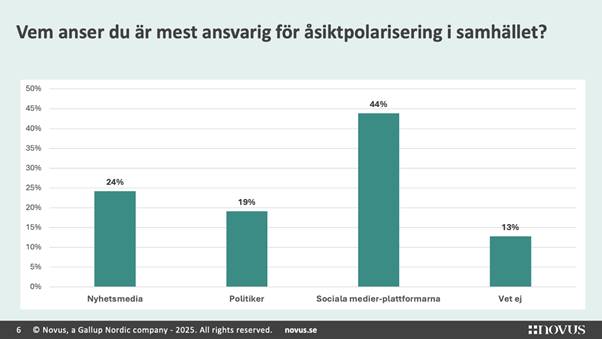

Responsibility for opinion polarization in society

Polarization is the driving force behind the populism that is

spreading in the Western world. According to the survey, Swedes primarily

believe that social media is responsible, but traditional media and politics

also have a great responsibility. The rise of social media, which politicians

and news media are also adapting to. The here-and-now reporting and

provocative posts on social media mean that politicians get to get to the

point and debate, which creates a dynamic where politics is rewarded by the

logic of social media. However, this does not mean that politicians and the media are

free from responsibility. They still have their own responsibility, even if

the disruptive effect of social media has changed the public discourse. This survey was conducted during the period February 6–11, 2025,

unlike the previous questions that were asked in approximately 40 countries

globally during September 2024.

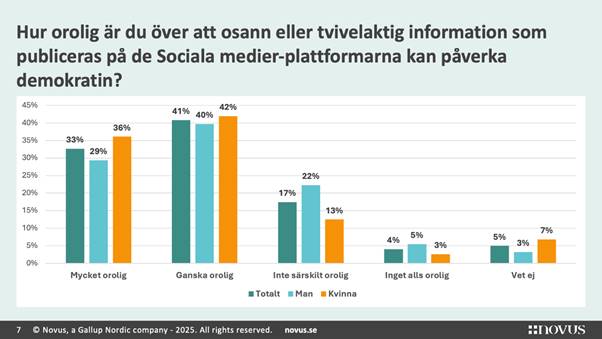

The Swedish people are well aware of the effects that social

media platforms have on society, and the concern for democracy is palpable,

something Novus has reported on for over five years through various surveys.

Fake posts on social media have sometimes also been spread further in

traditional news media. At the same time, this reflects how the media and politicians

themselves talk about the role of social media, often without reflecting on

their own responsibility in the development.

Elon Musk's impact on companies linked to him

Elon Musk's provocative gesture was truly provocative and

immediately damaged both Tesla's reputation and his own. We have found in

other recent surveys that Musk is considered a burden to both Tesla and X. This reputational loss is due to his arm waving and shows that

there is no doubt at all about how the Swedish people perceived the gesture.

They saw exactly what it looked like, and how it was interpreted. It was not

something positive for Tesla or Musk.

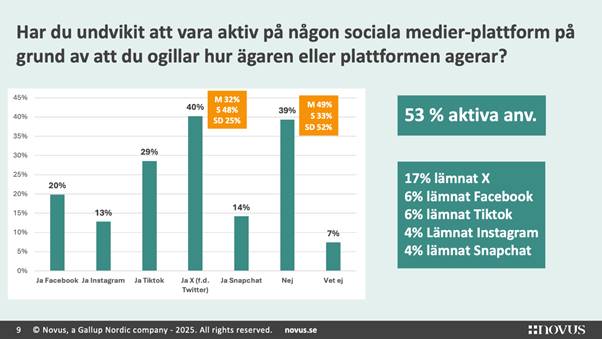

47% of Swedes are not active on social media, an important

aspect to keep in mind when describing these platforms as democratic arenas.

With a voter turnout of over 80% in Sweden, it is clear that more people

participate in the democratic system than in the debate on social media. Previous Novus surveys show that many people refrain from

expressing themselves on social media for fear of hate and threats. But it is

also about wanting to stay updated on the activities of friends and

acquaintances, rather than participating in discussions themselves. The silent majority is a force that is often underestimated.

They stand up when needed, they react to what is happening, but they have no

interest in standing on a stage and trumpeting it. If this silent majority is

marginalized or intimidated into passivity, society loses a central part of

the democratic conversation. Silence is often misinterpreted as acceptance,

when in fact it is more often about distancing.

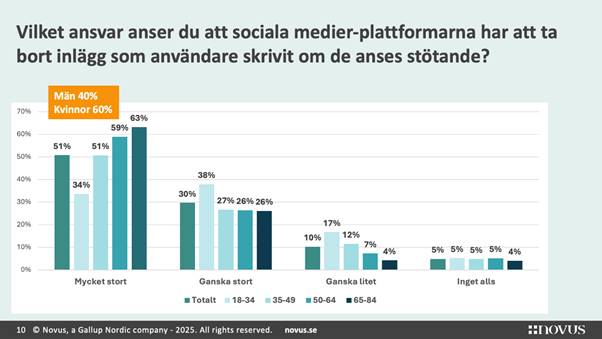

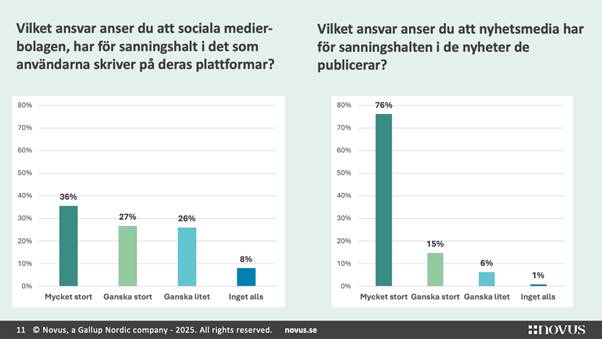

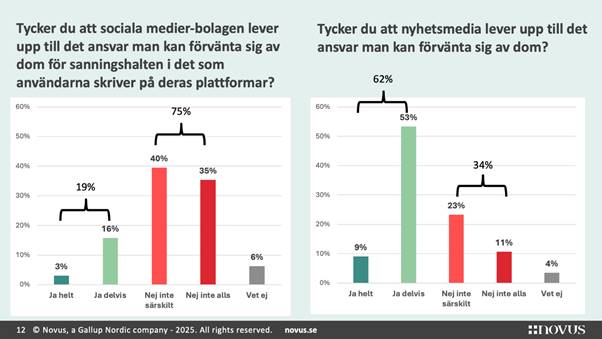

Social media responsibility

Social media is considered to have a great responsibility, but

it is worth noting that the responsibility is greatest among the older

generation, which is less digital; the younger generation understands more

and places fewer demands on the platforms than the older generation.

It is clear that many believe that social media has a great

responsibility for what they publish, but compared to editorial news media,

the difference is striking, as it should be. One in three Swedes believes

that social media has little or no responsibility, since they understand that

it is private individuals who write. Compared to what news media produces,

only 7% believe that the media has little or no responsibility. The difference between editorial media and social media is

something that citizens understand to a fairly large extent.

While there is a difference between social media and editorial

media, many believe that social media does not take responsibility. This is

probably where knowledge of algorithms comes in, where the platforms can

reward falsehoods, hatred and threats. However, the low level of trust in

editorial news media's responsibility should be a wake-up call. Only 9%

believe that news media fully take the responsibility that can be expected.

One in three Swedes believes that the media does not take very much or no responsibility

at all in relation to what should be expected. Given that it is believed that the responsibility that editorial

media has for what is published is much greater than what is expected of

social media, it is a reminder for editorial media to reflect on what they

themselves do, not just criticize social media's shortcomings.

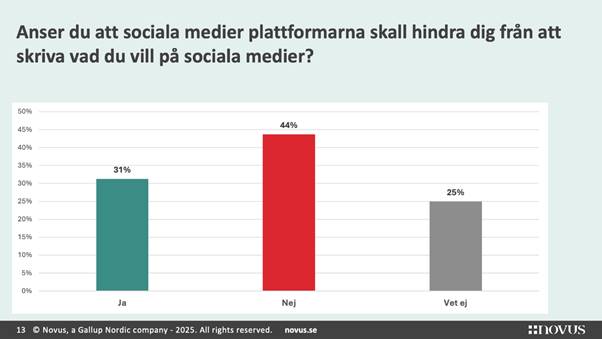

One in three Swedes believes that social media should prevent

users from writing whatever they want. This is a bit of a philosophical

question, we may all have written something we regret, but here it is more

about people not wanting to see hate and threats on social media. The Swedish

people do not appreciate that kind of tone in the public space. In connection with the Koran burning, our surveys showed that a

large proportion of Swedes wanted to ban demonstrations that could be

perceived as provocative or offensive to someone. Which is, after all, the

very essence of demonstrations and freedom of expression. At the same time,

there is great resignation and frustration over how much space unacceptable

behavior is given in the public sphere, and that the state often protects the

one who provokes, rather than the one who is provoked. This also has consequences

for Sweden's national interests, as in the case of the Koran burning, which

threatened to destroy Sweden's chances of becoming a member of NATO. Behind this, a misinterpretation of freedom of expression is

also beginning to emerge that the Swede does not stand behind. A perception

that you have the right to say anything without having to bear the

consequences. Provoking an entire religion and then demanding protection from

the police by invoking freedom of expression is an example of this. To put this in a more everyday context, imagine someone walking

up to the biggest man in the pub and saying something incredibly offensive,

then hiding behind the guards when he justifiably gets angry. It is not

illegal to say what you want in Sweden, but you have to be prepared for the

consequences, even though no one has the right to break the law in response

to what someone says. It is extremely un-Swedish to openly provoke someone

and then demand protection against your own actions. This is an important

aspect to consider when looking at these figures that emerge from the

surveys.

We asked the following question to further demonstrate what the

previous question indicated. We do not want hatred, threats and lies to take

up such space in the public sphere. Most Swedes would never even think of

expressing themselves in the way that leading figures in power and public

figures suddenly do, and we see the damage it causes. Since this is now

happening and leading to negative consequences, there is a growing feeling

that it may have to be banned. The reason is that constitutional laws, including

freedom of expression, are perceived to be abused for personal gain. We do

not want rights-grabbing or anti-democratic behavior to be allowed to occur

under the protection of our democratic principles. At the same time, the solution is not prohibition. Rather, this

is an expression of resignation, where every second Swede feels that

legislation seems to be the only solution. Previously, this type of norm has

been maintained by the collective conscience, where news media acted as a

yardstick and questioned the behavior of public figures. But today, behaviors